Disclosure: White Cliff Minerals Limited has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Risks

Price and Volume (1-year)

* White Cliff Minerals Limited has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in A$ unless otherwise specified.

Two polymetallic projects in the Canadian Arctic

Fully focused on the Rae project following agreement to sell the Great Bear Project to Hydrocarbon Dynamics Ltd. (ASX: HCD/ MCAP: $4M) for $5.8M ($1.2M cash + $4.6M shares)

Portfolio Overview

Source: FRC

Upon closing, $3.3M in HCD shares will be distributed to WCN investors as dividends

The Rae project is located near mines/assets held by majors including Agnico Eagle Mines Limited (NYSE: AEM), B2Gold Corp. (TSX: BTO), Burgundy Diamond Mines (ASX: BDM) and Rio Tinto (NYSE: RIO); proximity to major operators enhances potential acquisition appeal if a discovery is made

Rae Copper-Silver Project (100% interest)

Ownership and Location

The Rae project covers 2,180 km 2 in Nunavut within the Coppermine River Group, an area known for very high-grade copper mineralization.

WCN gained control of the project in 2023

All Weather Air-Strip on Site

Source: Company

75 km from Kugluktuk and the coast, near a deep-water port

All-weather airstrip on site; rare in the Arctic; improves access, and lowers logistical costs, which are typically higher for remote projects

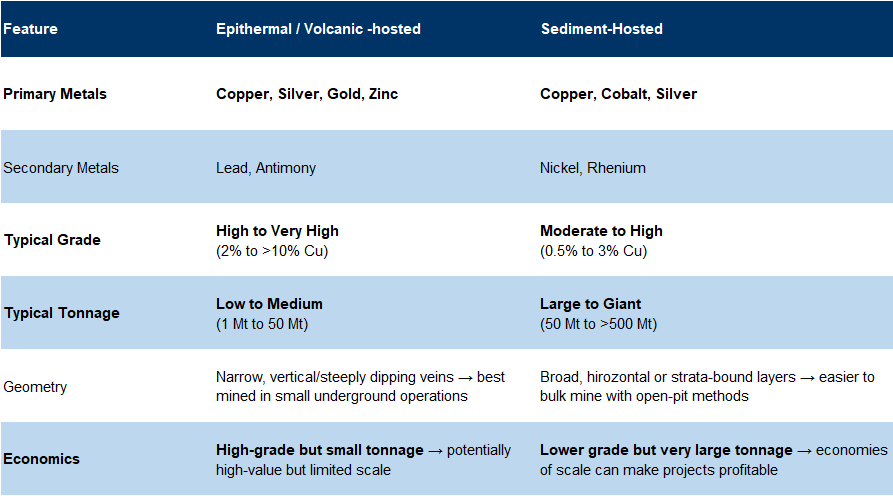

History and Mineralization

Copper was first discovered in the region in the 1700s. The property hosts multiple high-grade copper prospects, including both epithermal/volcanic-hosted, and sediment-hosted deposits. These deposit types often support lower-cost operations because they are close to the surface, rich in copper (high-grade), and easy to process using standard methods

Source: FRC / Various

High-grade epithermal copper deposits are often rich in copper but generally small in scale

In contrast, sediment-hosted copper deposits usually contain large volumes of copper, as seen in notable examples such as the Kupferscheifer in Poland and Germany, and the Central African Copperbelt in the DRC and Zambia

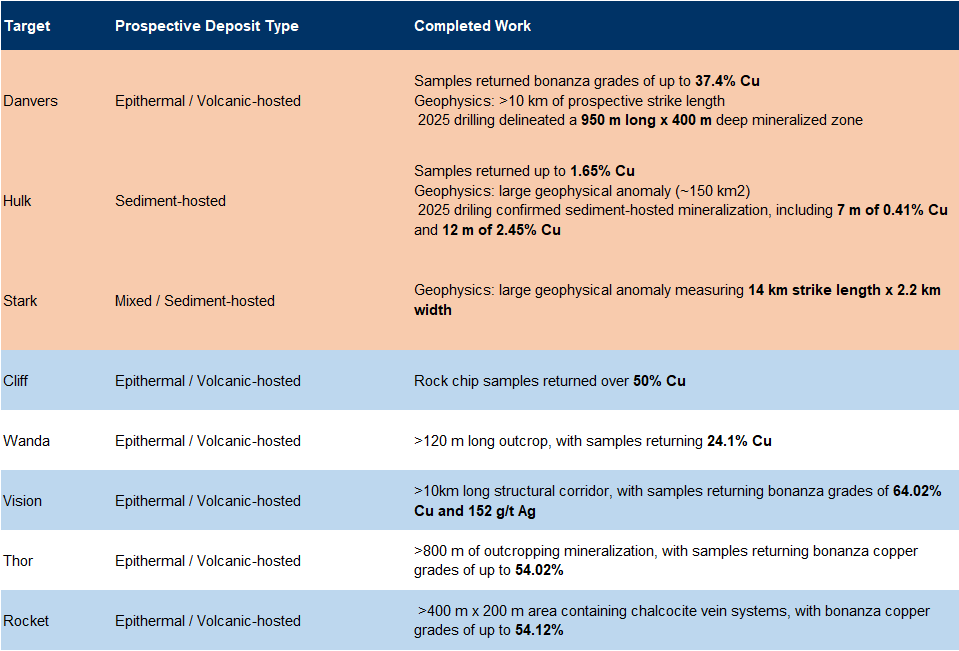

The table below lists all targets identified to date.

Main Targets

Several targets have been identified, though no independently verified resources (NI 43-101 – Canadian / JORC – Australian) have been defined to date

Targets highlighted in orange represent near-term priorities

Source: FRC / Company

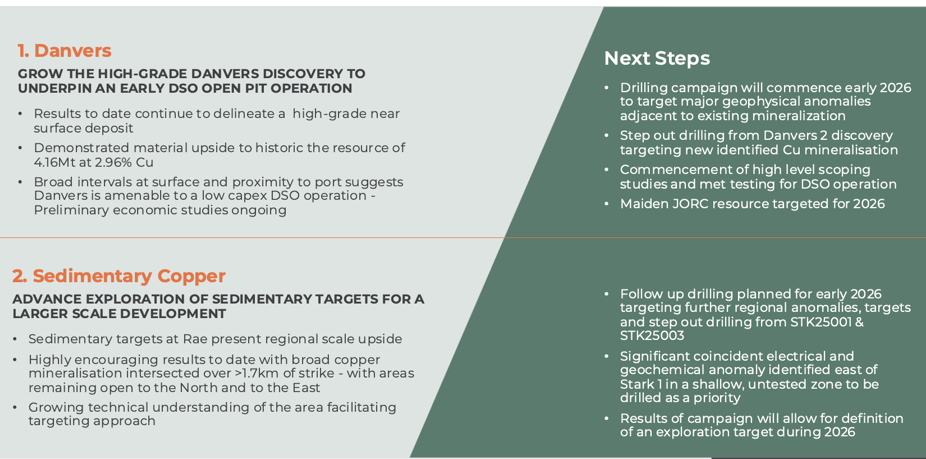

Danvers is the most advanced prospect, with most past work focused on this target

The other focus areas are Hulk and Stark

The following section outlines the key targets in detail.

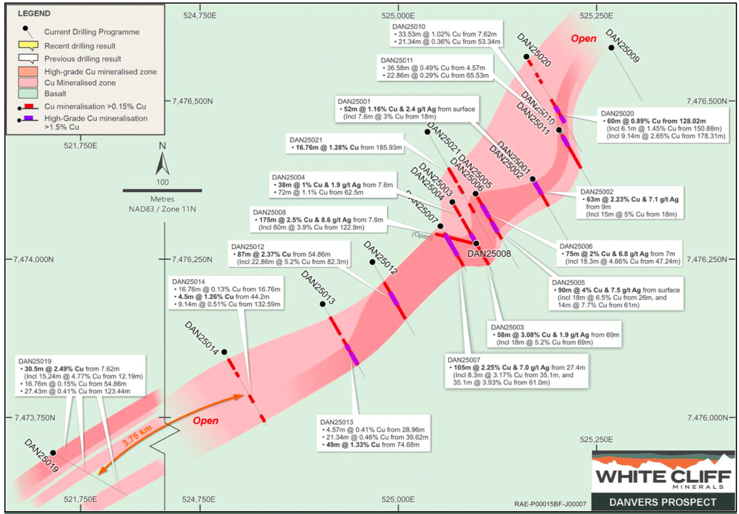

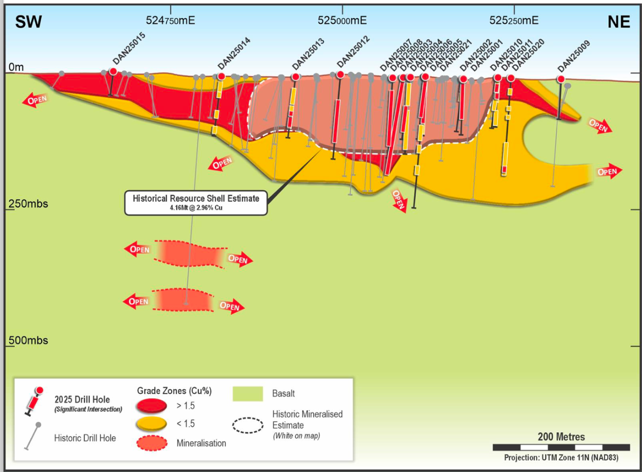

Danvers

Two mineralized zones (targets) have been identified to date: Danvers 1 and Danvers 2. Based on older records (not independently verified), Danvers 1 hosts a historical resource of 270 Mlbs of copper, at an exceptionally high average grade of 2.96%, within an area measuring 375 m long by 200 m deep.

Prospective areas for high-grade epithermal, and volcanic-hosted copper deposits

Recent drilling by WCN (21 holes, 3,535 m) confirmed high-grade copper at Danvers 1, and expanded the area where copper is known to occur, both along its length and at depth. The drilling also discovered Danvers 2, a new zone located 4 km southwest of Danvers 1. Mineralization at Danvers 1 now stretches 950 m, compared with the historical resource that covered only 375 m, suggesting a potential 150% increase in resources.

2025 Drill Highlights - Danvers

Source: Company

The 2025 drill campaign returned multiple high-grade intercepts over long intervals, demonstrating the continuity of copper-rich material across Danvers 1

Danvers 1: 175 m at 2.5% Cu, 58 m at 3.08%, 63 m at 2.23%, and 18 m at 6.5% Cu

Danvers 2: 15 m at 4.8% Cu, within a broader 30.5 m zone averaging 2.5% Cu

For context, most operating copper mines operate at 0.5–1.0% Cu

Danvers 1: 3D Model

Danvers 1 measures 950 m in length and over 400 m in depth, and remains open both along strike (length), and at depth

The historical resource covered only 375 m of strike

Preliminary Magnetic Data

Source: Company

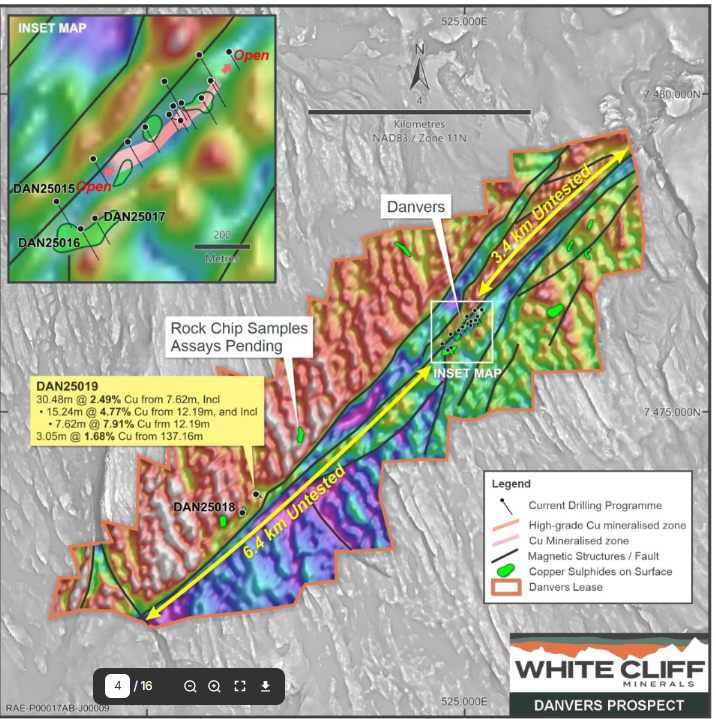

The recently discovered Danvers 2, located 4 km southwest of Danvers 1, is a largely untested area

As shown on the map, approximately 10 km of the total project length remains untested

Danvers 1, at 950 m in the middle of the project, highlights the significant potential, showing significant opportunities for future exploration, and expansion

A geophysical survey completed last year identified several areas of interest along 10 km of untested ground, highlighting potential for new discoveries.

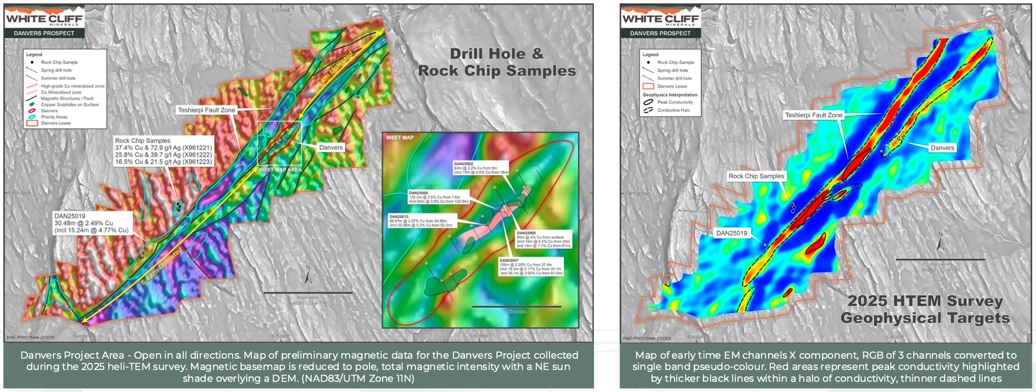

Resource Upside - Danvers

The red and yellow zones on the right show where the geophysical survey detected metal-like conductivity underground.

Source: Company

Multiple promising targets

Other Key Targets: Hulk – Stark

At the Hulk target, copper extends across 20 km, and is concentrated in three fault-controlled basins (areas where underground fractures have created pockets that trap copper), with the main mineral layer located 200–300 m below the surface.

2025 Drill Highlights - Hulk

Source: Company

While Danvers targets high-grade epithermal/volcanic-hosted copper (smaller but very rich deposits), the Hulk and Stark targets focus on sediment-hosted copper (typically lower grade but potentially much larger and deeper deposits)

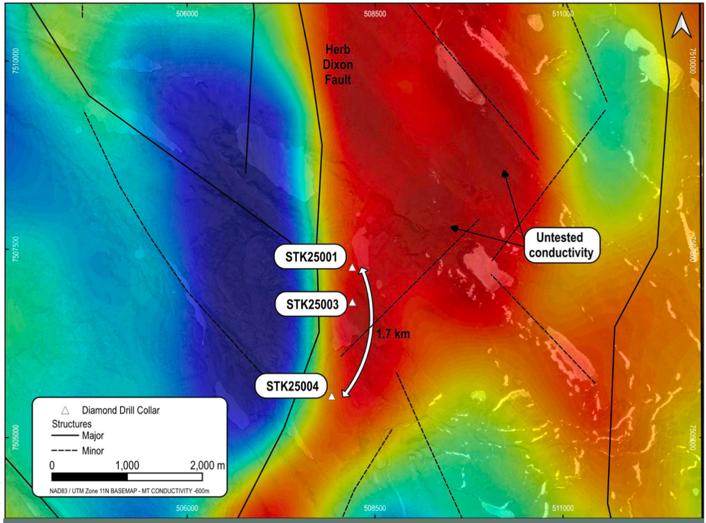

Geophysical Anomaly – Stark

*Red and yellow areas show where the survey detected metals

Source: Company

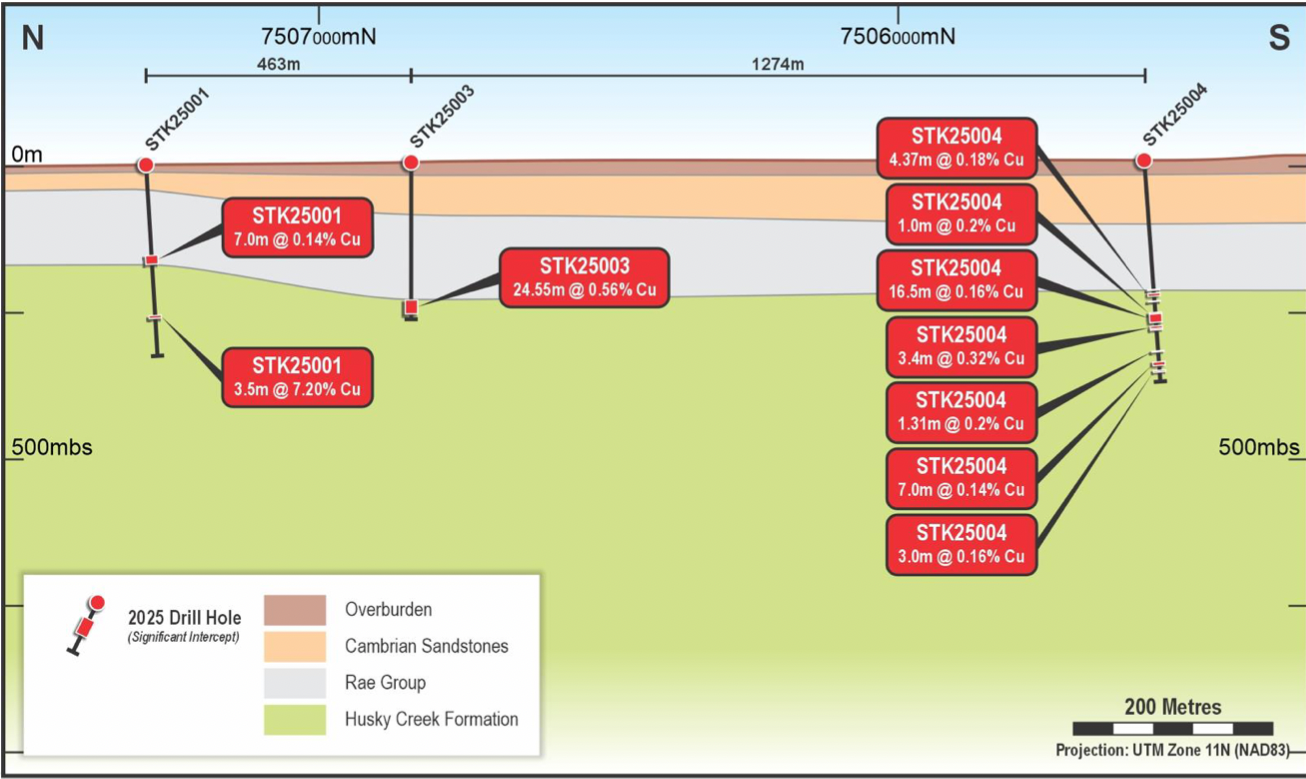

The Stark target is along the Herb Dixon fault, a big underground fracture that stretches over 25 km

Management Plans

The company is pursuing a dual strategy to advance the project:

Management Plans

Source: Company

Follow up drilling planned for all key targets

We anticipate a maiden resource estimate for Danvers by year-end

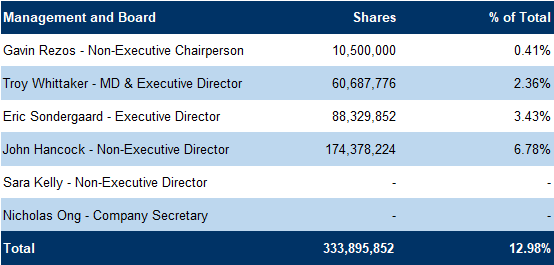

Management and Board

Share Ownership

Source: Company

Management, board, and advisors own 19%

Three out of five directors are independent

We believe management and the board bring a strong mix of technical expertise, and capital markets experience

Brief biographies of the management team and board members, as provided by the company, follow:

Gavin Rezos – Non- Executive Chairperson

Mr. Rezos has held Chairman, Board and CEO positions of companies in the resources, materials and technology sectors in Australia, Europe, the UK, the US and Singapore and was formerly Chairman of Vulcan Energy Resources Limited, an Investment Banking Director at HSBC Group PLS and a non-executive director of Iluka Resources Limited, and of Rowing Australia.

Troy Whittaker – Managing Director

Mr. Whittakers an executive with more than 20 years of experience, spanning successful international project evaluation, development, and the operation of multi-billion-dollar assets globally across a broad range of commodities, including iron ore. He has a proven track record of leadership. He has held senior roles with major global mining companies Fortescue Metals Group Ltd and Anglo American UK and who’s post graduate qualifications include Mineral & Energy Economics and Logistics & Supply Chain Management.

Eric Sondergaard – Executive Director

Mr. Sondergaard is a registered Professional Geoscientist and a graduate of the University of Calgary in Canada. He brings over 20 years of operational experience in the mining industry, including significant expertise in frontier exploration and project management.

John Hancock – Non-Executive Director

Mr. Hancock has over 25 years experience in financial markets, commodities, public relations, crisis management, fund raising and philanthropy and is currently Chair of his family office Astrotricha Capital SEZC. He has assisted global funds raising and deploying over $1B in investments, throughout Australia and Canada. Academic qualifications include a Master of Business Administration, International Directors Course at Australian Institute of Company Directors, and a Graduate Certificate of Applied Finance and Investment from the Financial Services Institute of Australia.

Sara Kelly – Non-Executive Director

Ms. Kelly has over 20 years’ experience as a corporate lawyer, with deep expertise in corporate governance, compliance and risk management. She has advised on a wide range of domestic and cross border transactions, including capital raisings, asset acquisitions and disposals, joint ventures and corporate restructures. Ms. Kelly has been a Partner at Edwards Mac Scovell, a boutique litigation, insolvency and corporate firm based in Perth, Western Australia. She currently serves as Non Executive Chair of Midas Minerals Limited and as Executive Director of Energy Transition Minerals.

Nicholas Ong – Company Secretary

Mr. Ong brings over 20 years of experience in listing rules compliance and corporate governance. He is a non-executive director and company secretary of several ASX listed companies, and has extensive experience in mining project financing as well as mining and offtake contract negotiations. He is a fellow member of the Governance Institute of Australia and holds a Bachelor of Commerce and a Master of Business Administration from the University of Western Australia.

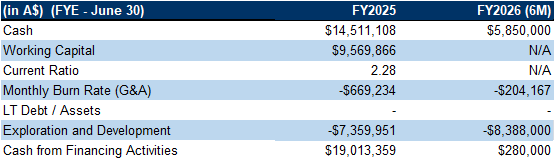

Financials

Source: FRC / Company

Strong balance sheet with $5.85M in cash as of December 2025, plus an additional $1.20M expected from the sale of the Great Bear project

Source: FRC / Company

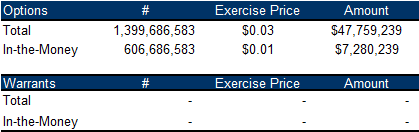

Can raise up to $7.28M from in-the-money options

FRC Projections and Valuation

Source: FRC / S&P Capital IQ / Various

Recent exploration shows mineralization at Danvers 1 now extends 950 m × 400 m vs the historical 375 m × 200 m (270 M lbs), a potential 400% increase

The discovery of Danvers 2, and other promising untested targets, indicate further upside

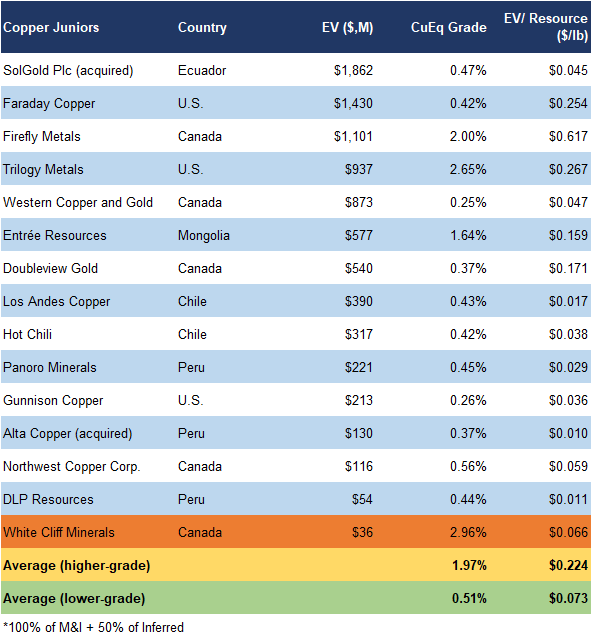

We are using twice the historical resource for valuation, a conservative assumption at this stage

Based on the above assumption, WCN is trading at $0.07/lb, vs a sector average of $0.22/lb for high-grade copper juniors, a 71% discount

Applying the sector average to WCN’s resources, we arrived at a fair value estimate of $0.048/share

We are initiating coverage with a BUY rating, and a fair value estimate of $0.048/share. WCN provides exposure to high-grade copper through its district-scale Rae project, with upside potential from expanding mineralization at Danvers 1, the discovery of Danvers 2, and several untested regional targets. Supported by high management ownership, a strategic location near majors, and a 71% discount to peers, we expect the stock will gradually align with our fair value as the market becomes more aware of Rae’s potential.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are assigning a risk rating of 5 (Highly Speculative)