Disclosure: Sonoro Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Qualified Person: Stephen Kenwood, P.Geo., Director of Sonoro Gold Corp.

* Sonoro Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

Two gold projects in Mexico: the advanced-stage Cerro Caliche gold project (flagship asset), and the early-stage San Marcial gold-silver project

Management plans to spin-off the San Marcial project into a publicly listed company

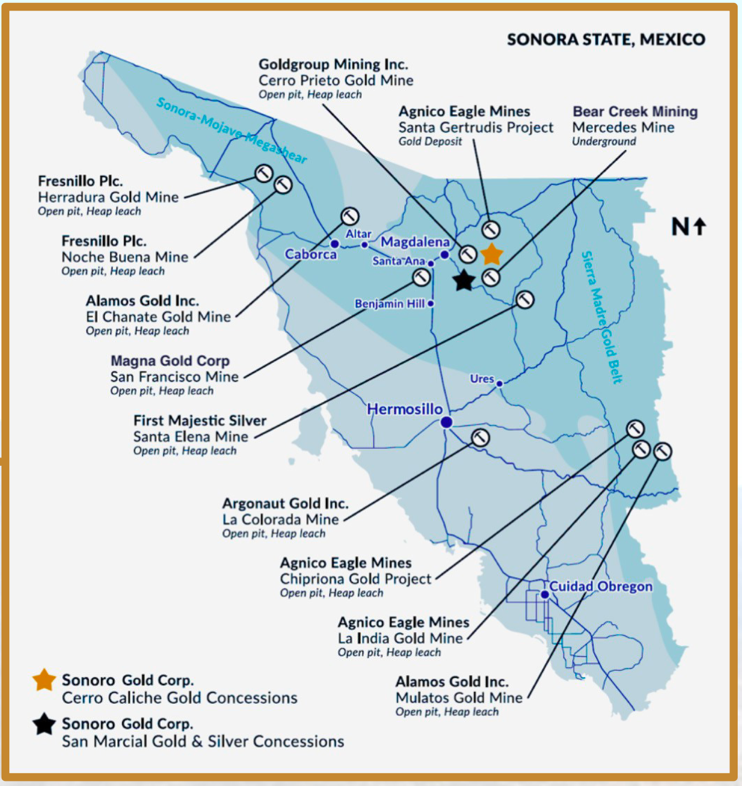

Near several well-known operating mines

Portfolio Summary

Source: Company

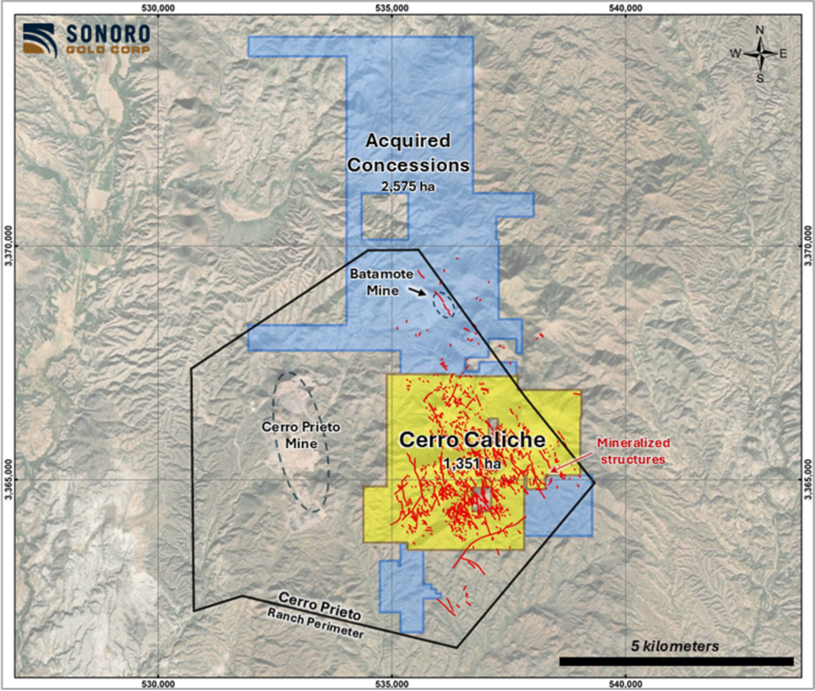

In January 2026, SGO acquired 10 additional claims , expanding the Cerro Caliche project from 1,350 to 3,924 hectares, signalling management’s strong commitment to advancing and growing the project. The new claims are located right next to the current property, along both the northern and southern boundaries. By expanding the land position in this way, we believe the company increases the chances of potentially making new gold discoveries , and adding more value to its main project.

Located three hours south of Tucson, Arizona

The Cerro Caliche project consists of 25 contiguous mining concessions, all 100% owned by SGO. In Mexico, mineral rights are controlled by the government, while surface rights belong to the landowner. SGO currently holds a 25-year surface lease covering 3,908 ha, shown within the black outline on the map below, except for the 1,009 ha oval-shaped area, where Goldgroup Mining’ s (TSXV: GGA/MCAP: $444M) Cerro Prieto mine operates. In 2028, the lease will expand to include the oval-shaped area, increasing SGO’s total controlled land to 5,007 ha. At that point, we believe GGA would need to negotiate surface rights with SGO , creating a potential M&A catalyst.

Cerro Caliche Concession Map

Source: Company

Cerro Caliche is located near several established projects, and within close proximity to two operating mines owned by Highlander Silver (TSX: HSLV) and Goldgroup Mining, and an exploration project held by Agnico Eagle (NYSE: AEM)

Regional M&A opportunities are emerging as GGA’s mine nears depletion, positioning SGO as an attractive target if Cerro Caliche receives its environmental permit

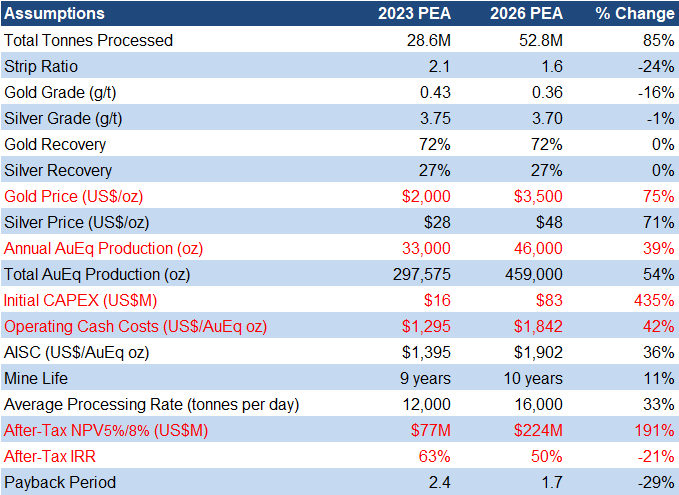

2026 vs 2023 PEA: Cerro Caliche Gold Project (100% Interest)

The 2026 update improves on the 2023 study by adding more resources, increasing the mining rate (throughput) from 12,000 to 16,000 tonnes per day, boosting annual production to 46 Koz AuEq (up from 33 Koz), and extending mine life to 10 years (up from nine).

Open-pit, heap-leach operations are generally low-CAPEX, and quicker to bring into production; the project’s initial CAPEX is US$83M vs US$100–US$300M for similar-sized new gold mines

AT NPV8%: US$224 M, AT IRR: 50% (US$3,500/oz gold; spot: US$5,090/oz); for context, we view IRR >15% as strong for mining projects

By comparison, the 2023 PEA had an AT NPV of just US$77 M, and that was calculated using an even lower 5% discount rate

With higher gold prices, OPEX and CAPEX estimates have also increased but remain very reasonable, with strong margins

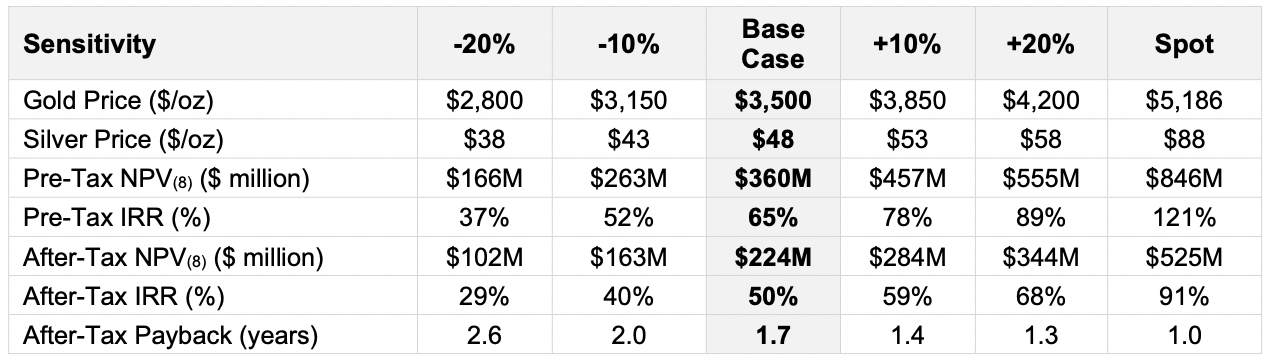

Sensitivity Analysis

(QP: Stephen Kenwood, P.Geo., Director of Sonoro Gold Corp.)

Source: Company

At US$5,186/oz gold, the economics are even more compelling, with an after-tax NPV8% of US$525 M and an IRR of 91%

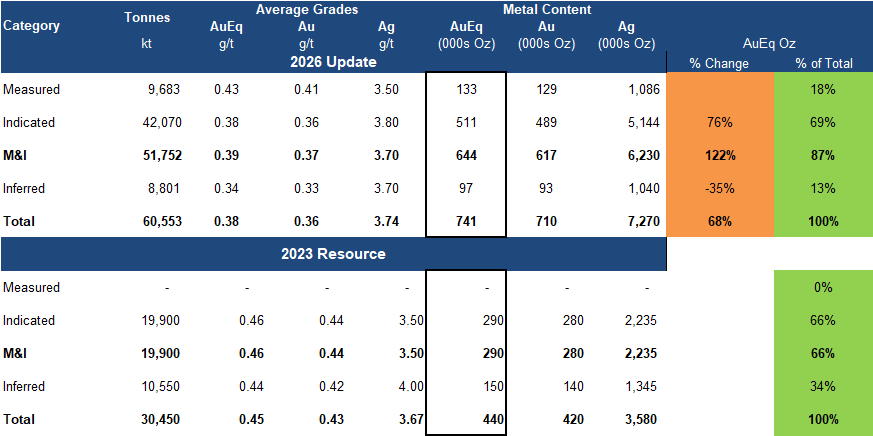

Resource Estimate

(QP: Stephen Kenwood, P.Geo., Director of Sonoro Gold Corp.)

Source: Company / FRC

M&I resources (higher-confidence categories) increased 122% to 644 Koz AuEq, now accounting for 87% of total resources versus 66% previously, reflecting increased overall confidence

Total resources rose 68%, in line with our December report prediction that they could increase 50–100%

We see potential for resource expansion, as only 30% of the property’s identified mineralized zones ( targets ) have been drill-tested. Additionally, a 2023 study by SRK Consulting estimated potential to add 125–285 Koz AuEq (0.26–0.39 g/t) of lower-grade resources by drilling beyond the current pit shells.

Lower-grade material (less-rich ore) was added to the new estimate, which is now economic due to higher gold prices; as a result, overall grades fell 15% to 0.38 g/t AuEq, but this should not be seen as negative; it simply means the newly added material will cost more to extract and process

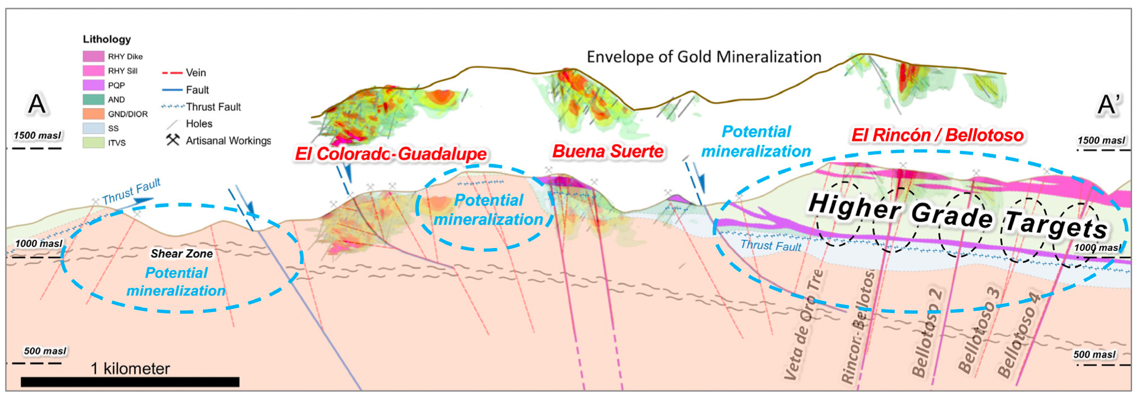

Resource Expansion Potential

Source: Company

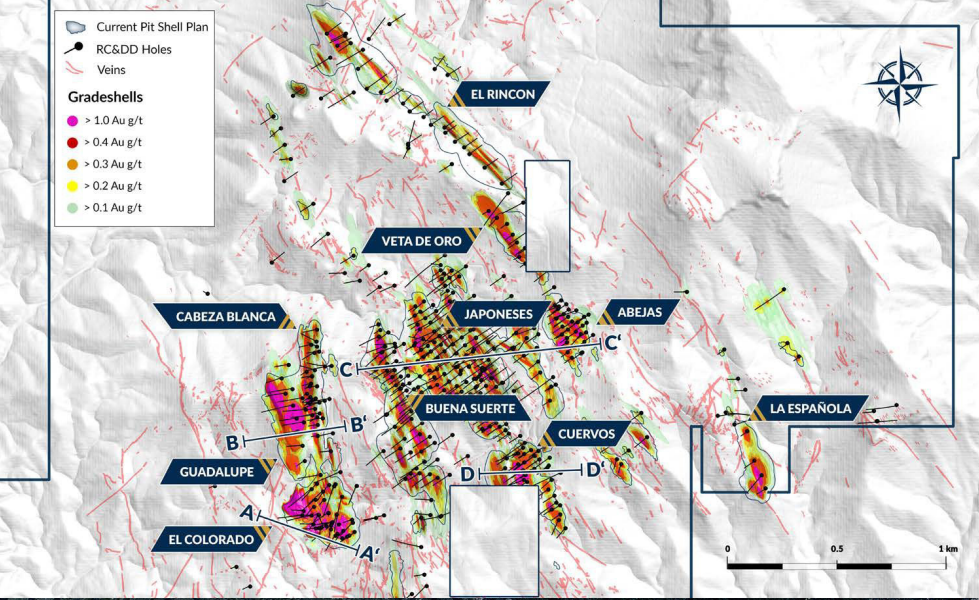

Targets

Source: Company

Several additional targets remain to be explored

SGO is planning a 56-hole, 8,890 m resource expansion drill program in 2026

Permitting and Upcoming Plans

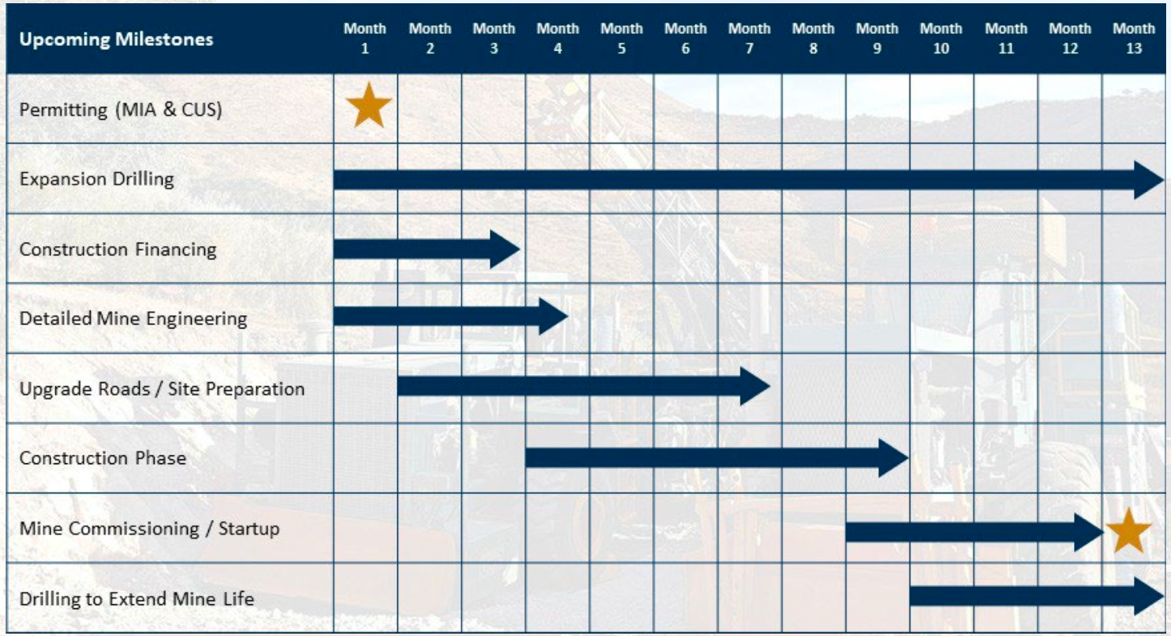

SGO has submitted an Environmental Impact Statement ( Manifestación de Impacto Ambiental, or MIA) , including a mine plan, environmental baseline studies, and socio-economic assessments. MIA approval is required before construction or mining can begin. Management expects a decision in H1 -2026 , though we note that delays are possible given the current backlog of applications. In addition to the MIA, SGO plans to submit applications for a Change of Land Use permit and a Water Use permit in H1-2026. We note that these approvals are relatively straightforward, and should be granted within a few months of submission.

Management’s Projected Timelines

Source: Company

MIA approval is the final major regulatory step before advancing to construction

Permitting underway

Following MIA approval, SGO expects to move quickly to construction and begin production within 13 months

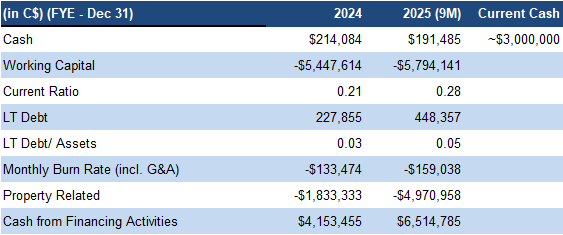

Financials

$3M in the treasury

Expecting $2.10M VAT refund this quarter

Source: FRC / Company

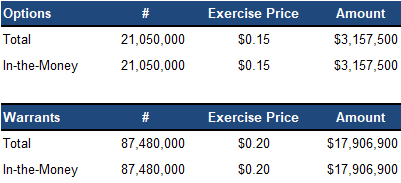

Can raise up to $21M from in-the-money options and warrants

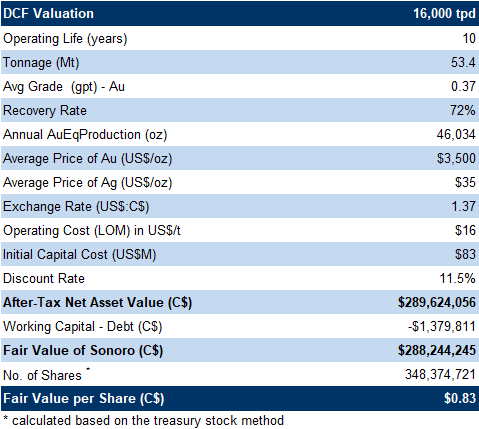

FRC DCF Valuation

Given the resource update, and the PEA, we are raising our DCF valuation from $0.70 to $0.83/share

Source: FRC

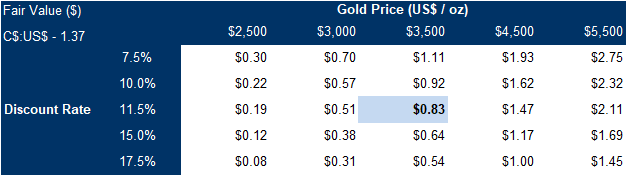

Our valuation remains highly sensitive to gold prices

We are reiterating our BUY rating, and raising our fair value estimate from $0.70 to $0.8 3 /share. The substantial resource growth and highly attractive PEA economics underscore significant upside potential, with the stock currently trading at a small fraction of its net present value. As Cerro Caliche nears permitting and production, and with only a portion of the property drilled, there remains considerable opportunity for further resource expansion and value creation.

We base our valuation solely on a DCF model, as few projects offer a similarly low-CAPEX, quick-to-production profile

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining our risk rating of 5 (Highly Speculative)