Disclosure: Atrium Mortgage Investment Corporation has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

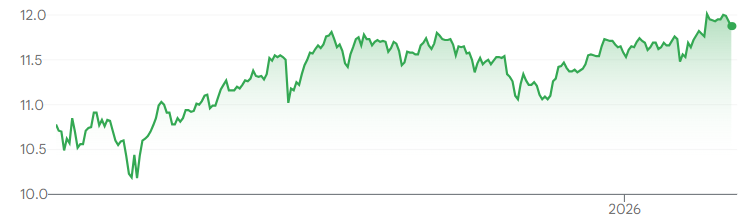

Price and Volume (1-year)

* Atrium Mortgage Investment Corporation has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise stated.

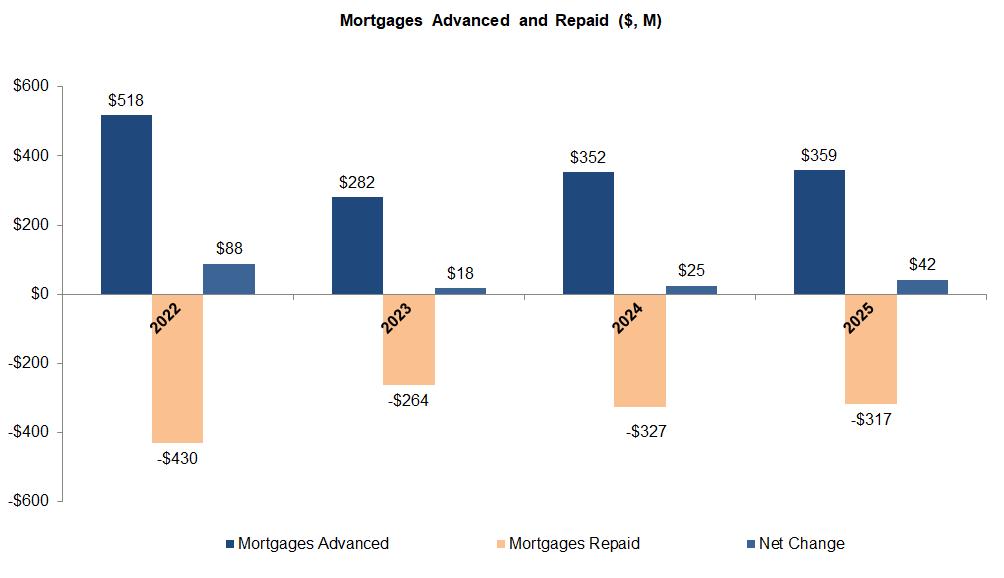

Loan advances rose 2% YoY, while repayments were down 3% YoY, resulting in net mortgages outstanding increasing 3% YoY to $892M vs our forecast of $900M

Portfolio Update

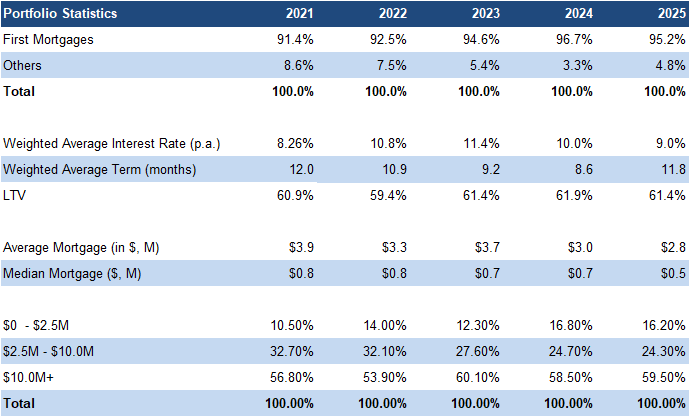

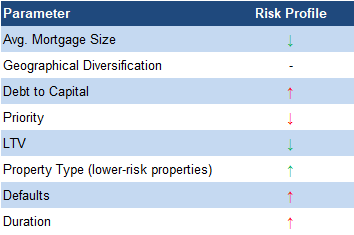

First mortgages and LTV declined slightly

Duration rose due to turnover

Lending rates eased following BoC rate cuts; since peaking in 2023, lending rates are down 2.40 pp vs a 2.75 pp decline in the benchmark rate, indicating MIC lending rates are less elastic

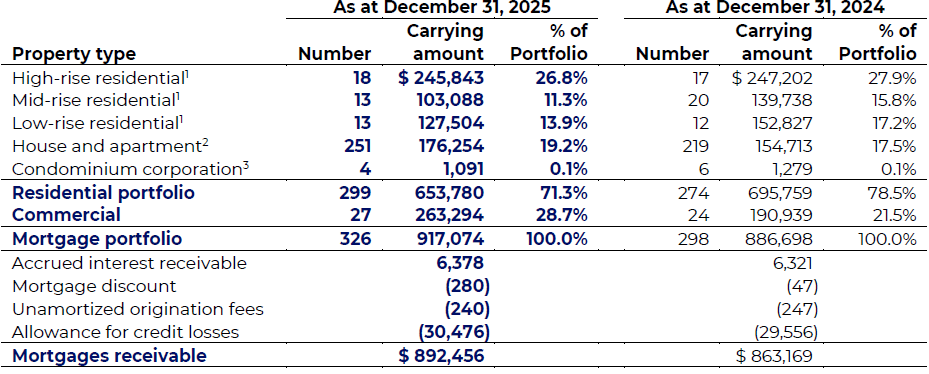

Mortgages by Property Type

Source: Company Data / FRC

Increased exposure to revenue generating commercial properties, and already built single-family units, while scaling back on residential development projects, implying a lower risk profile

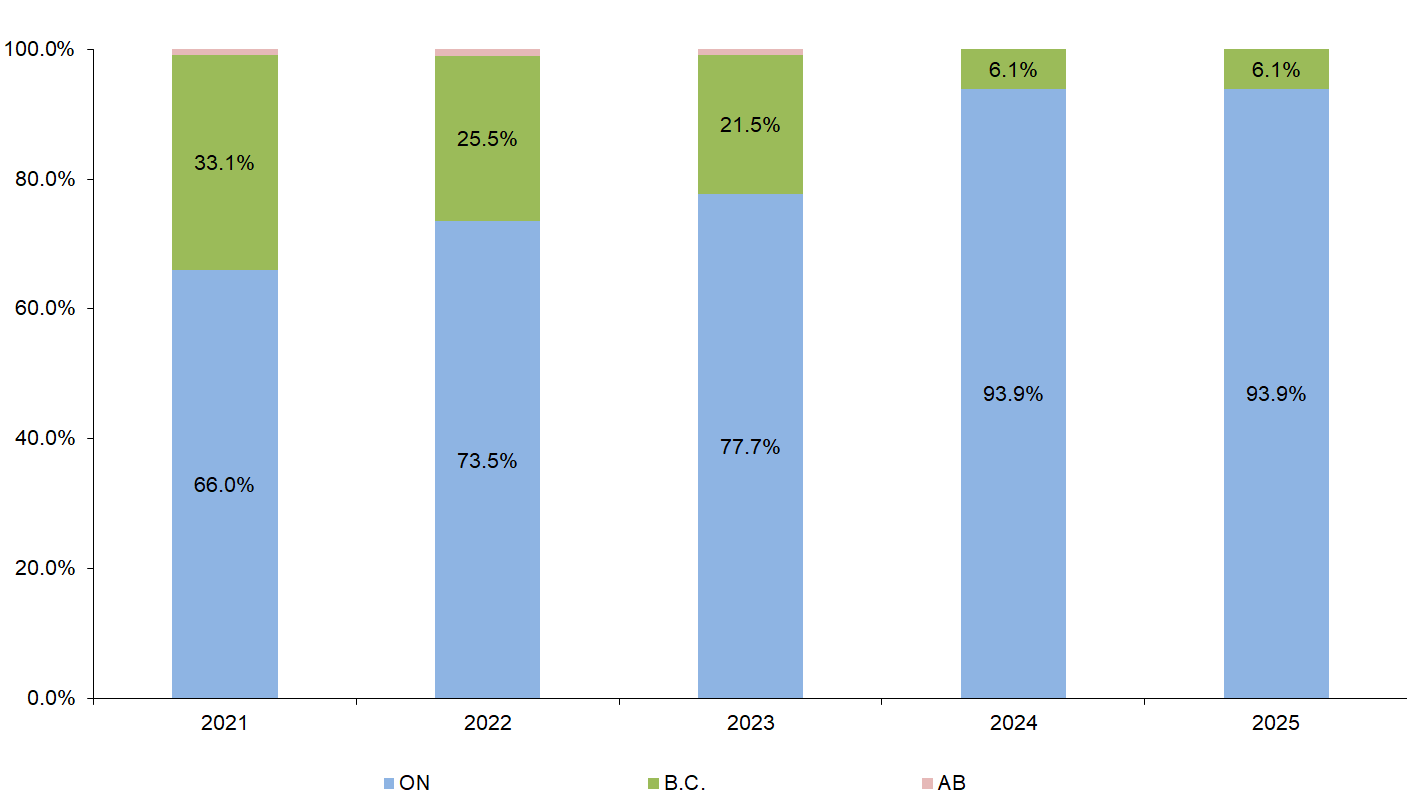

Mortgages by Region

No changes in provincial exposure

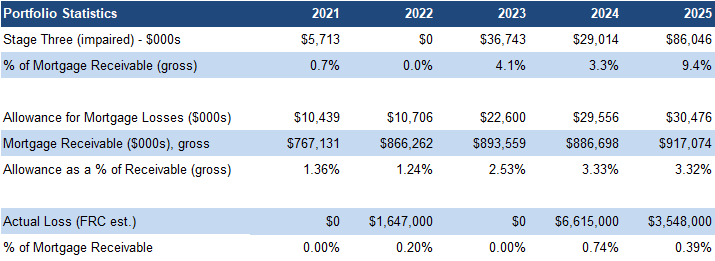

Stage two mortgages (high credit risk, not impaired) plus stage three (impaired) declined 12% QoQ

However, stage three mortgages rose 53% QoQ to 9.4% of total mortgages, driven by a single $31M loan that moved into impairment; management noted on the earnings call that this loan was fully repaid after year-end, which should reduce stage three levels

Source: FRC / Company

*Red (green) indicates an increase (decrease) in risk level.

Source: FRC

This explains why loan loss allowances remained largely flat QoQ

Overall, we believe the portfolio’s risk profile has edged higher, with four negative indicators versus three positive

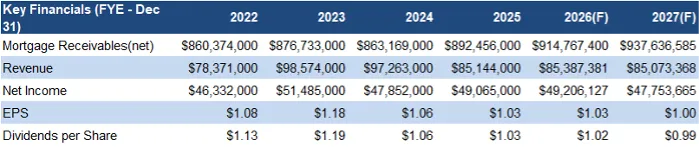

Financials

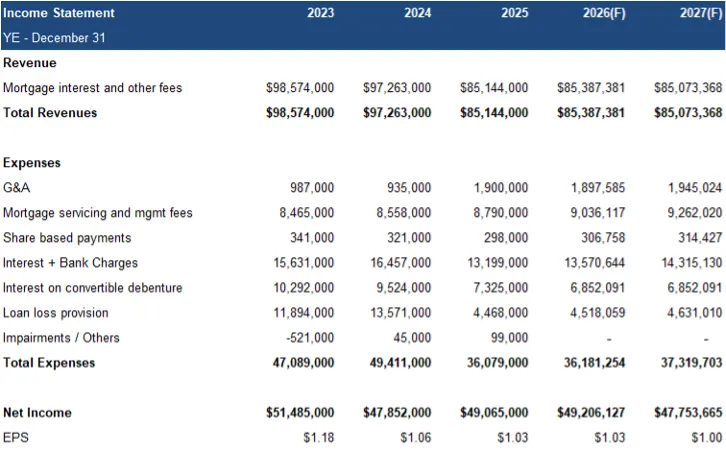

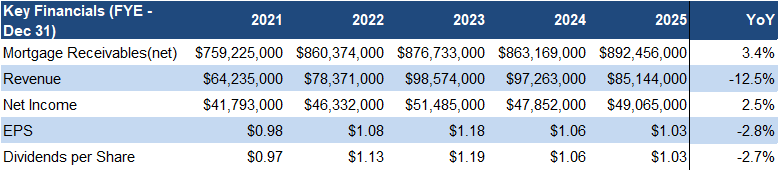

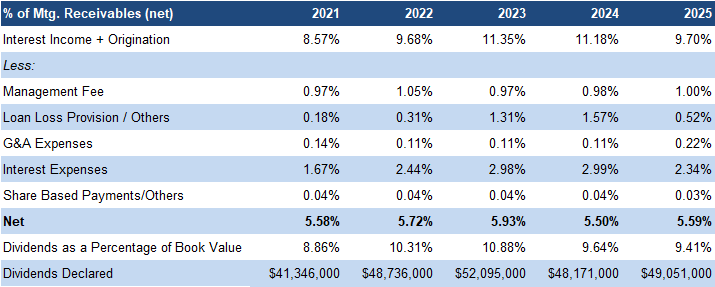

Revenue fell 13% YoY, amid lower lending rates, but beat our estimate by 0.3%

EPS declined 3% YoY, less sharply than revenue, beating our estimate by 3%, supported by lower loan loss provisions

Dividends were down 3% to $1.03/share, 4% above our estimate, reflecting an 8.84% yield

*The calculations in the above table are approximate as we used the average of beginning and end of period mortgage s outstanding.

Annual regular dividends held steady at $0.93/share, reflecting an 8.00% yield

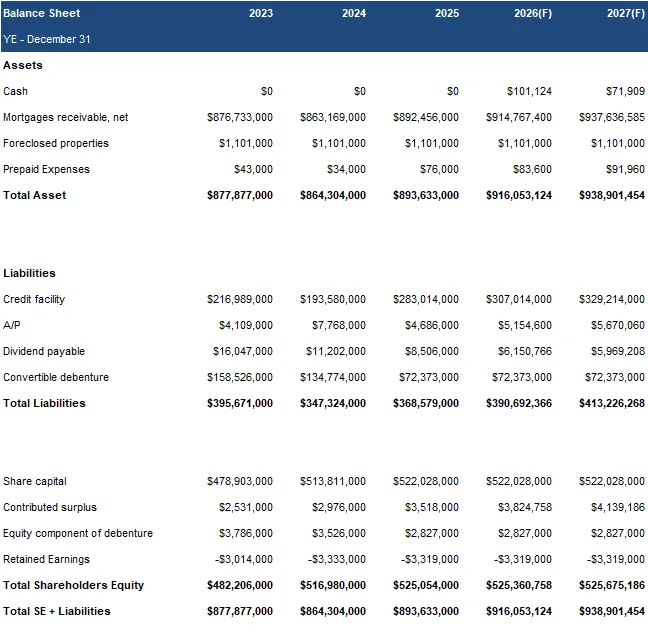

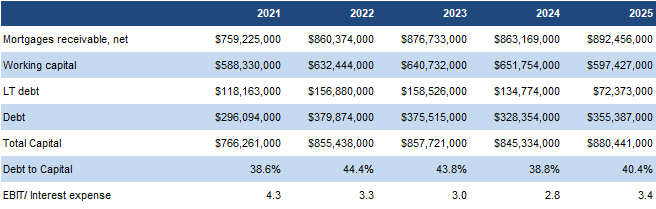

Debt-to-capital increased slightly to 40%, but stayed under the 10-year average of 42%

Source: Company / FRC

Notably, AI’s lending syndicate increased its credit facility by $40 million to $380 million, which we view as a strong vote of confidence in the company’s portfolio

FRC Forecasts & Valuation

Source: FRC

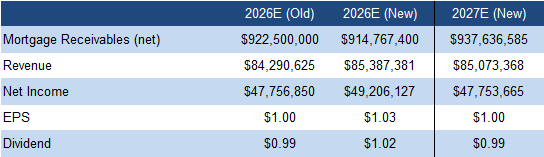

As Q4 loan loss provisions came in below expectations, we are raising our 2026 EPS and dividend forecasts

Source: FRC

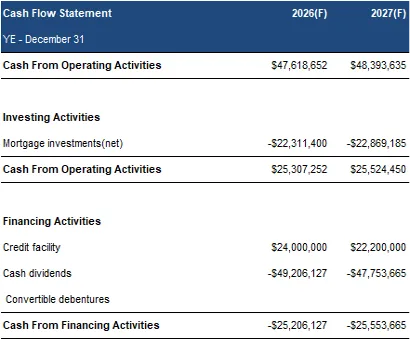

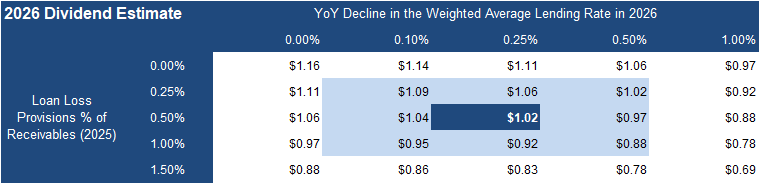

Our estimate for the 2026 dividend varies between $0.88 and $1.02/share, as loan loss provisions and lending rates vary

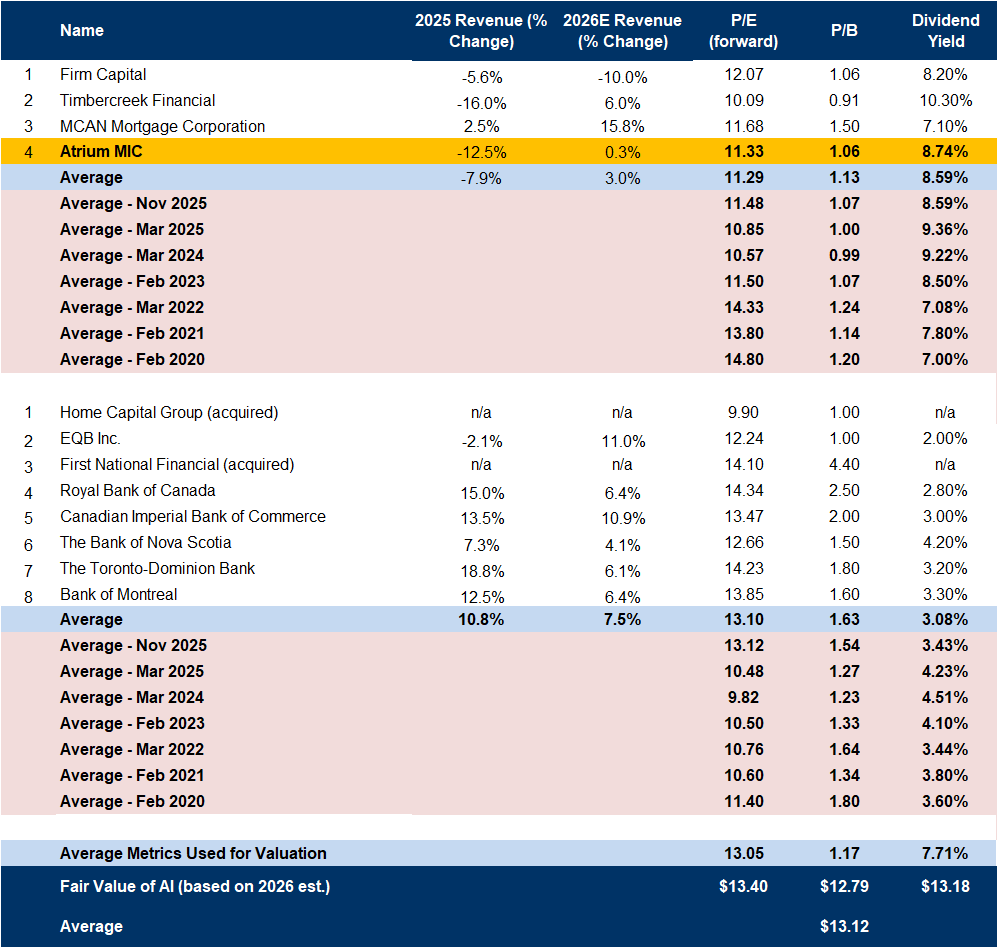

Source: S&P Capital IQ / FRC

Sector multiples are up 3% YoY, and 1% since our November 2025 report

On average, MICs and banks are expected to report 6% revenue growth this year vs 3% in 2025, potentially driven by higher lending volumes

Our fair value estimate increased from $13.00 to $13.12/share, driven by higher sector multiples, and our upward revision to earnings and dividend forecasts

We are reiterating our BUY rating , and adjusting our fair value estimate from $13.00 to $13.1 2 /share, implying a potential return of 22% (including dividends) in the next 12 months. Despite a 13% YoY revenue decline, results exceeded our expectations, driven by lower loan loss provisions, and solid mortgage growth. With a growing focus on lower-risk properties, and an attractive 8-9% dividend yield, we believe AI is well-positioned to benefit from a gradual rebound in residential real estate.

Risks

We believe the company is exposed to the following risks:

Maintaining our risk rating of 3 (Average)

APPENDIX