Disclosure: Silver X Mining Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

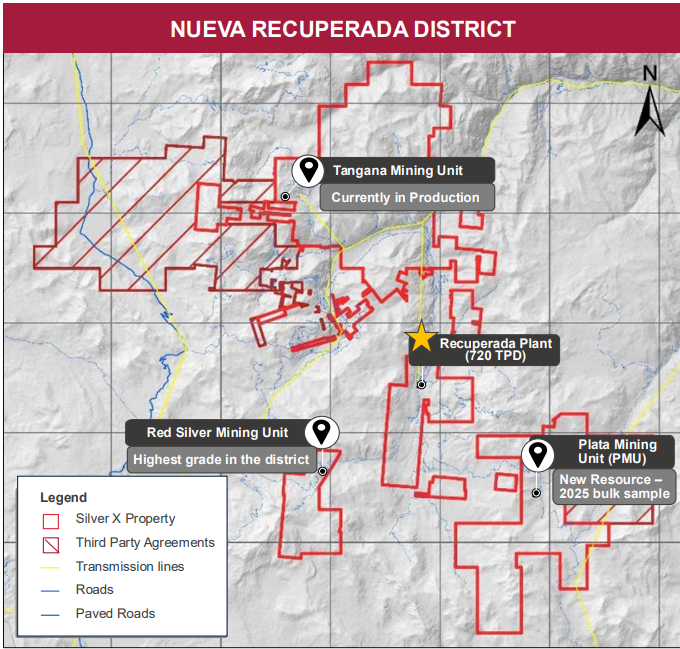

The Nueva Recuperada project includes the producing Tangana mine unit (TMU) with a 720 tpd processing plant, the advanced-stage Plata mining unit (PMU), and four exploration projects Extensive vein fields with 200+ targets, and 500+ outcrop veins

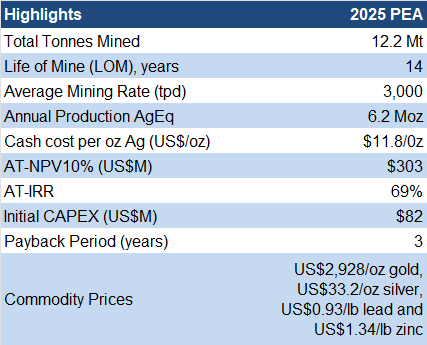

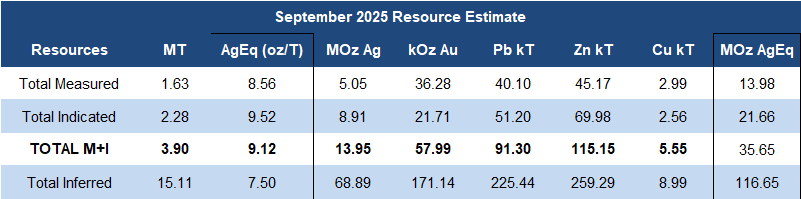

The 2025 PEA highlights the potential to increase annual production from ~1 Moz to 6 Moz AGX’s expansion plan involves two milling facilities: a new 1,500 tpd mill at Tangana, and the existing Recuperada mill (15 km south of Tangana), which will be expanded from 720 tpd to 1,500tpd Recuperada will be dedicated to processing ore from the PMU The PEA returned an AT-NPV10% of $303M, using $33/oz silver (spot: $64/oz), and $12/oz in cash costs

Project Overview

(QP: A. David Heyl, C.P.G., Consultant for Silver X Mining) Source: Company

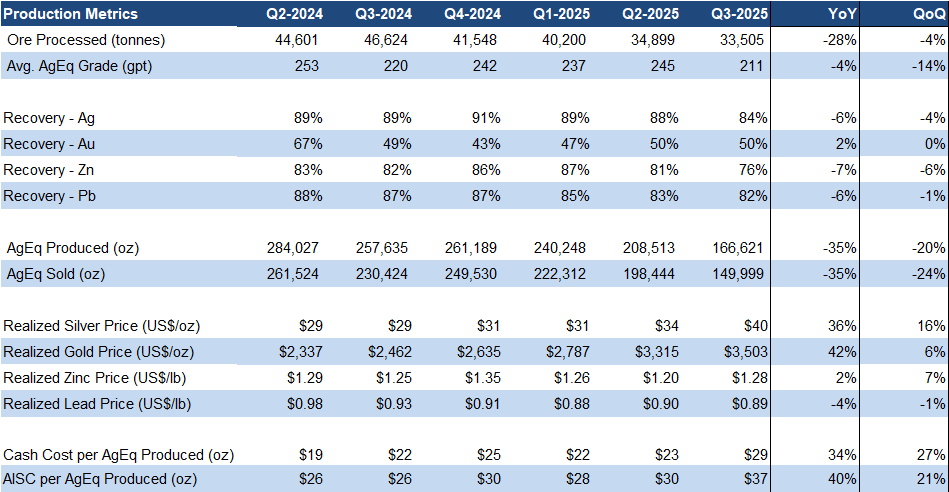

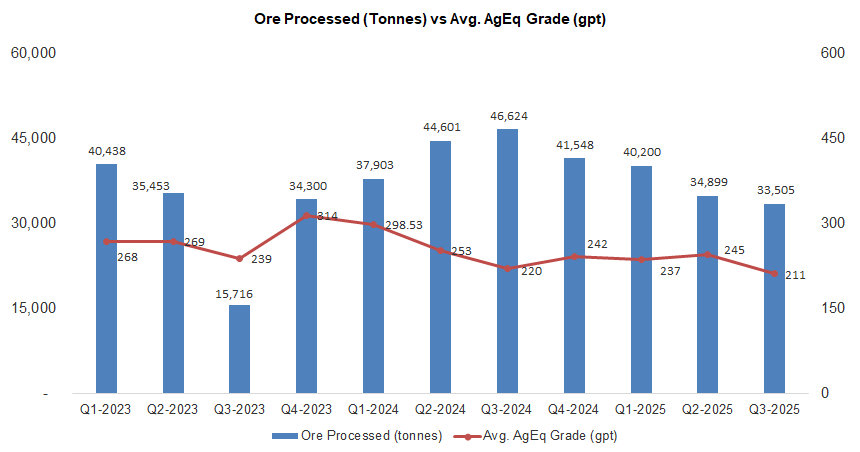

The PEA accounted for just 64% of resources, indicating further upside for NPV and IRR Production has declined QoQ over the past three quarters, driven by lower throughput and grades

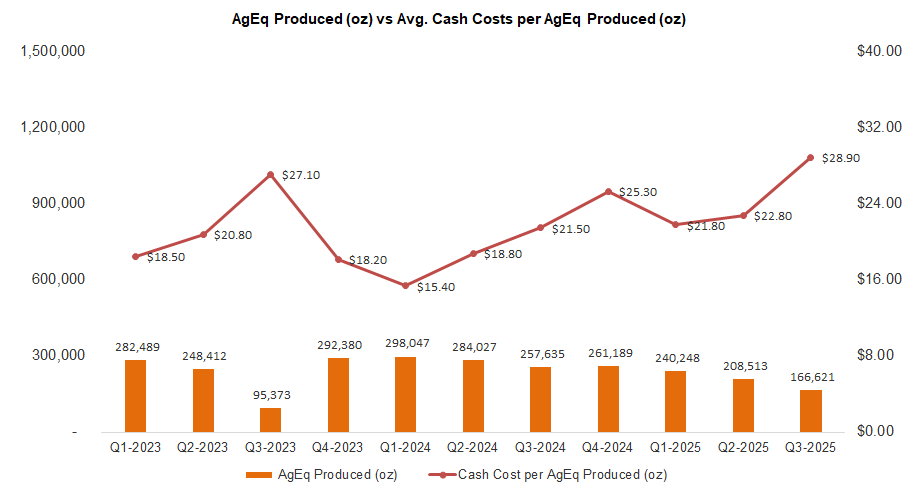

Q3 production fell 20% QoQ to 167 Koz AgEq, 11% below our estimate

( QP: A.

David Heyl, C.P.G. , Consultant for Silver X Mining) Source: Company

Q 3 Production and Key Operating Metrics

Source: FRC/Company

Source: FRC/Company

Cash costs rose 27% QoQ, 24% above our estimate, due to lower production

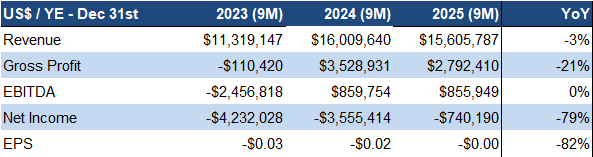

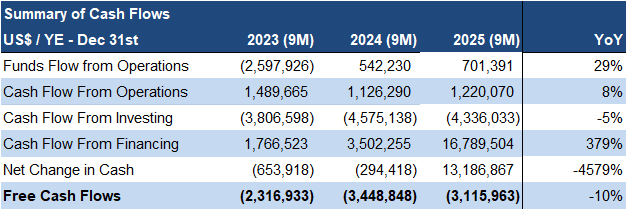

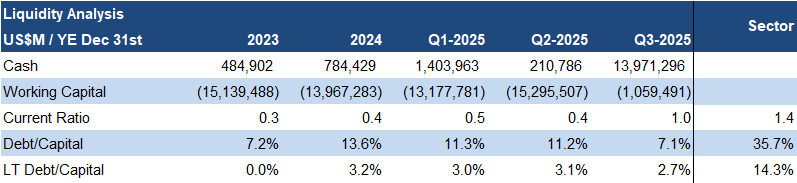

Revenue fell8% QoQ on lower production despite higher metal prices, missing our estimate by 9%EBITDA, EPS, and gross margins all slipped QoQ Last quarter, AGX turned around its working capital, cutting the deficit from $15M to $1M through a C$22 M equity financing, and has since added another C$1M from warrant exercises

Source: FRC/Company

Near-term plans include: Advanc ing the PMU to production in 2026 Update the Environmental and Social Impact Assessment (ESIA) to support a potential 1,500 tpd operation at Tangana Secure permits to build a new 1,500 tpd processing facility Resource expansion drilling Q 3 Financials

Source: FRC/Company

Source: FRC/Company

Source: FRC

Source: FRC

Source: FRC

Source: FRC

/ Company

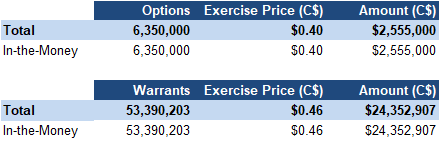

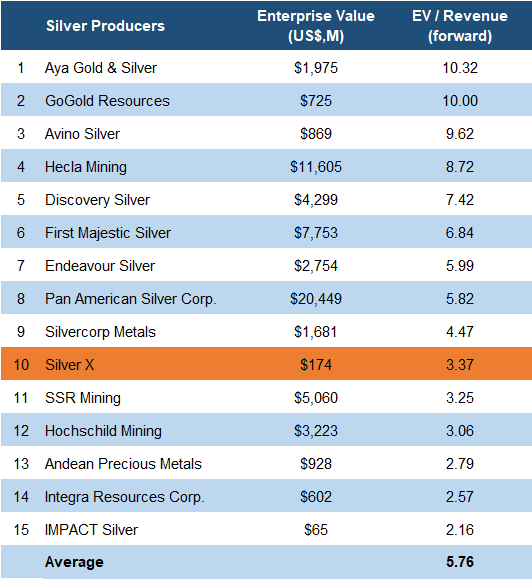

Can raise another C$27 M from in-the-money options/warrants AGX’s forward EV/Revenue is 3.37x (up from 2.79x) vs the sector average of 5.76x (up from 3.95x), a 42% discount Applying the sector average yields a comparable valuation of C$1.64/share (previously C$1.00/share)

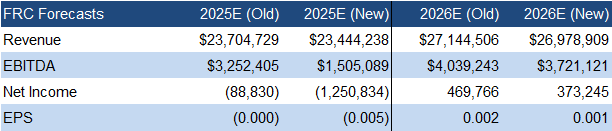

We are lowering our near-term production forecasts while raising our near and long-term metal price forecasts

Comparables Valuation

Source: FRC / S&P Capital IQ / Various

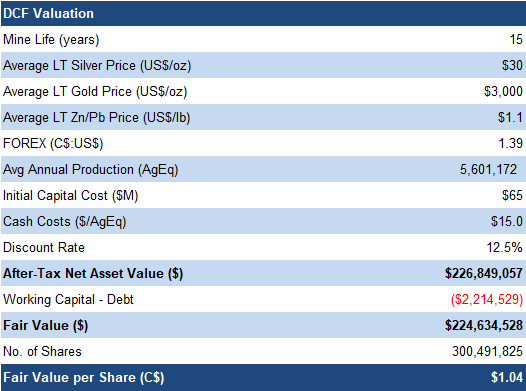

DCF Valuation

Source: FRC

As a result, we are lowering our 2025–2026 EPS estimates while raising our longer-term (2027+)

EPS forecasts Consequently, our DCF valuation rose from C$0.86 to C$1.04/share

Source: FRC

Source: FRC

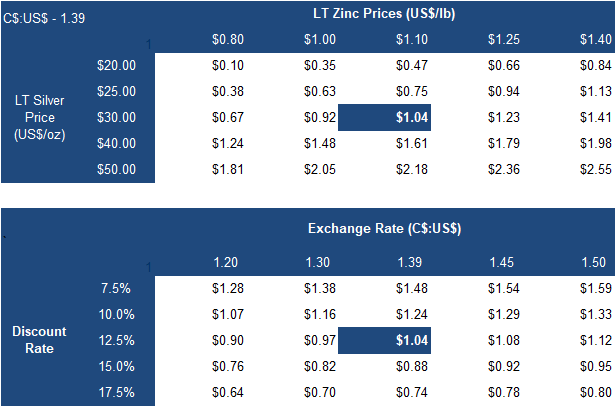

Our valuation remains highly sensitive to metal prices

We are reiterating our BUY rating, and adjusting our fair value estimate from

C$0. 95 to C$ 1.3 4 /share (the average of our DCF and comparables valuations).

While Q3 production missed expectations due to temporary operational issues, these have been resolved, and ramped-up throughput, along with planned expansion to ~1,000 tpd , and a major drill campaign, point to strong production growth potential.

Risks We believe the company is exposed to the following key risks: Metal prices Exploration and development FOREX Negative working capital The upcoming PEA might not be promising

Maintaining our risk rating of 4 (Speculative