Disclosure: Monument Mining Limited has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

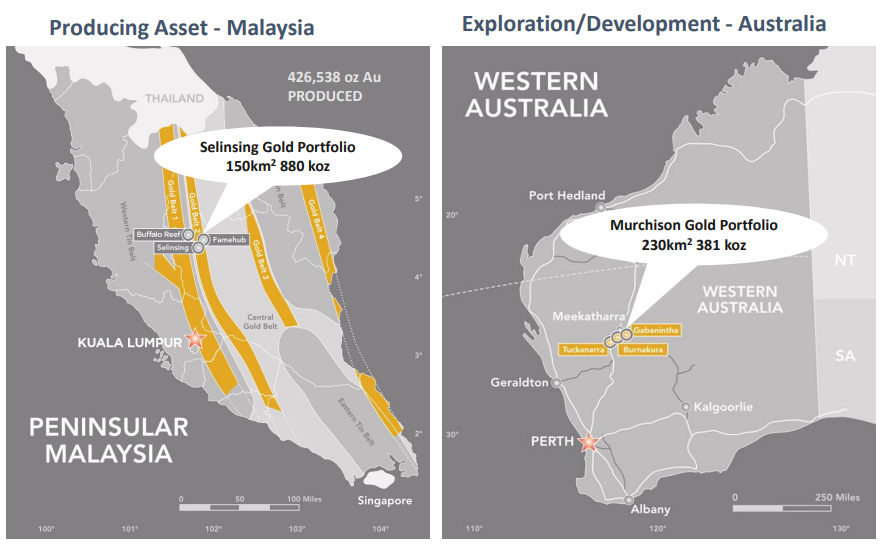

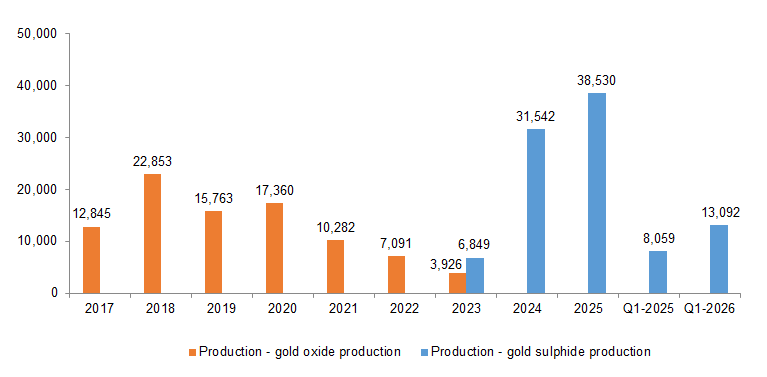

Owns a producing gold mine in Malaysia, and exploration projects in Western Australia Total compliant resources of over 1.2 Moz Au MMY has been processing sulphide materials since December 2022, producing a total of 90 Koz by September 2025 Q1-FY2026 production was up 62% YoY, and 6% QoQ, beating our estimate by 12%, driven by higher throughput and grades

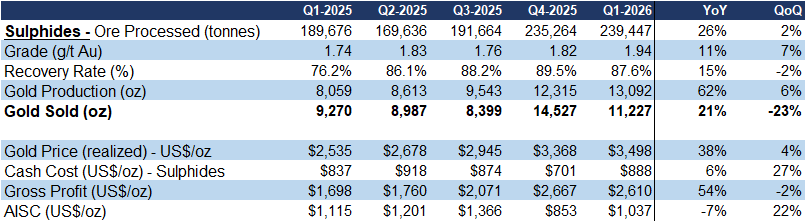

Cash costs were up 6% YoYto $888/oz, vs our estimate of $875/oz, mainly due to higher gold-price-linked royalty payments

Portfolio Summary

Production (Year-End: June 30th) - Oz

Source: FRC

Source: FRC

/ Company

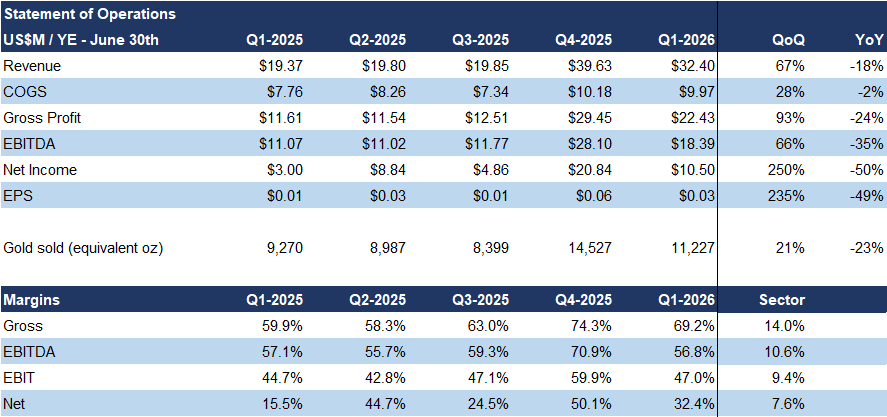

Gross profit was up 54% YoY to $2,610/oz With 550-600 Koz of sulfide resources remaining, we believe the mine could produce forapproximately 12 more years Driven by higher production and gold prices, Q1revenue rose 67% YoY, EBITDA +66%, and

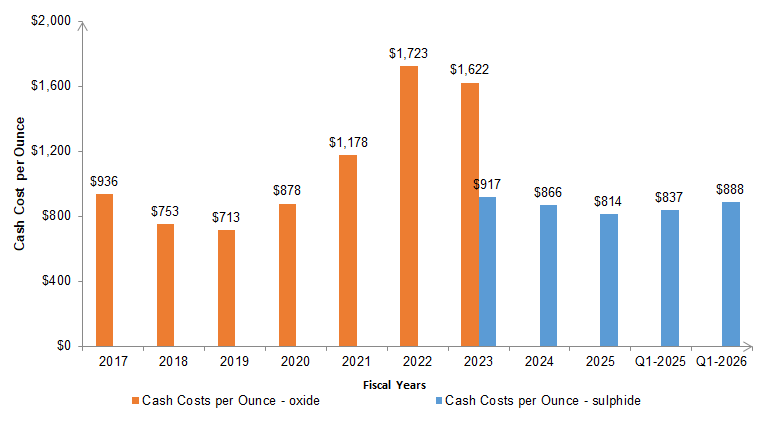

Cash Costs Per Oz

Source: FRC / Company

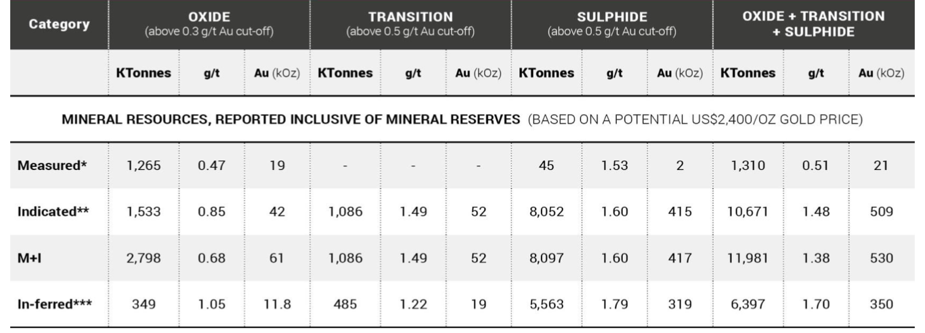

Reserves and Resources (Snowden NI 43-101 Technical Report: 2019)

* Qualified Person - Frank Blanchfield, an employee of Snowden Source: Company

EPS +235%Revenue topped our forecast by 10%, with

Financials (Year-End: June 30th)

Source: FRC / Company

Source: FRC / Company

Source: FRC / Company

Source: FRC / Company

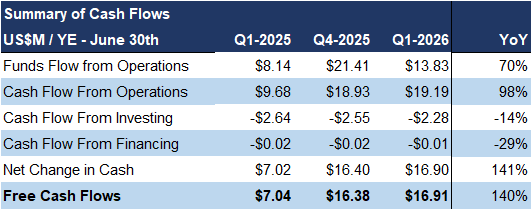

EPS ahead by 5%Margins improved across the board and remained well above sector averages FCF surged 140% YoY

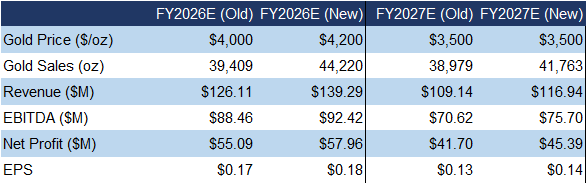

FRC Projections and Valuation

Source: FRC

Source: FRC/S&P Capital IQ

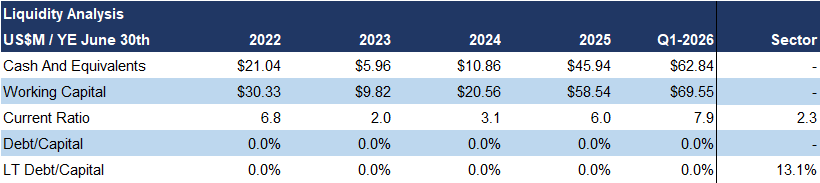

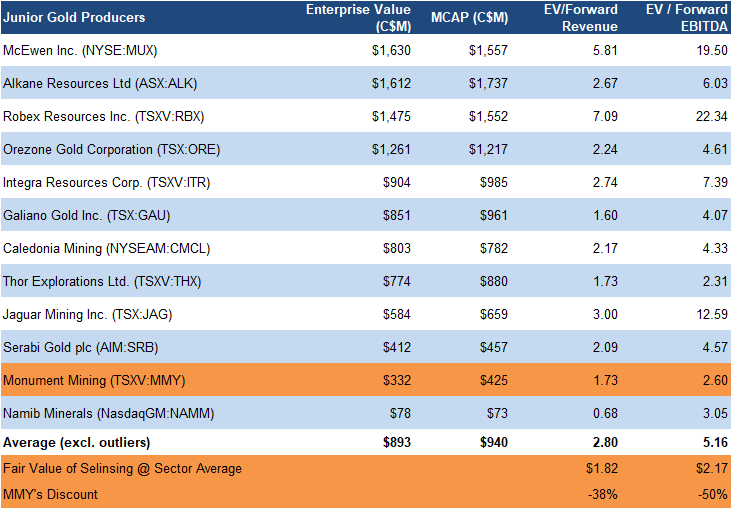

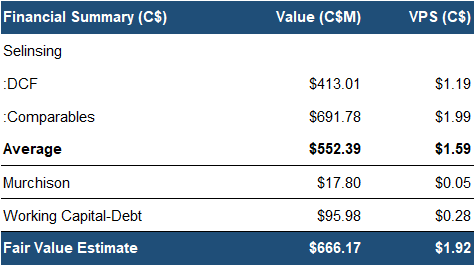

As a result, the balance sheet strengthened, with $70 M in working capital and no debt With production exceeding our forecasts and gold prices trending higher, we are raising our estimates across the board Sector multiples have risen17% since our November 2025 report, driven by higher gold prices MMY is trading at a 44% discount (previously 50%) to comparablejunior gold miners Applying sector multiples, we arrived at a fair value estimate of C$1.99/share (previously C$1.64/share) on the Selinsing mine Using a sum-of-parts valuation, we arrived at a fair value estimate of C$1.92/share (previously C$1.50/share)

Source: FRC

We are reiterating our BUY rating, and raising our fair value estimate from C$ 1.50 to C$ 1.92 /share. MMY’s strong operational performance, robust balance sheet, and special dividend reflect its financial strength. The company remains undervalued relative to peers despite a 251 % YoY share price surge , and promising drill results suggest potential mine life extension, and lower cash costs.

Risks We believe the company is exposed to the following key risks: The value of the company is dependent on gold prices FOREX Operational Exploration and development

We are maintaining our risk rating of 3 (Average)