Disclosure: Silver X Mining Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

Price and Volume (1-year)

* QP: A. David Heyl, C.P.G., Consultant for Silver X Mining. Silver X Mining has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in US$ unless, except for share price, fair value estimates, and MCAP data, which are in C$.

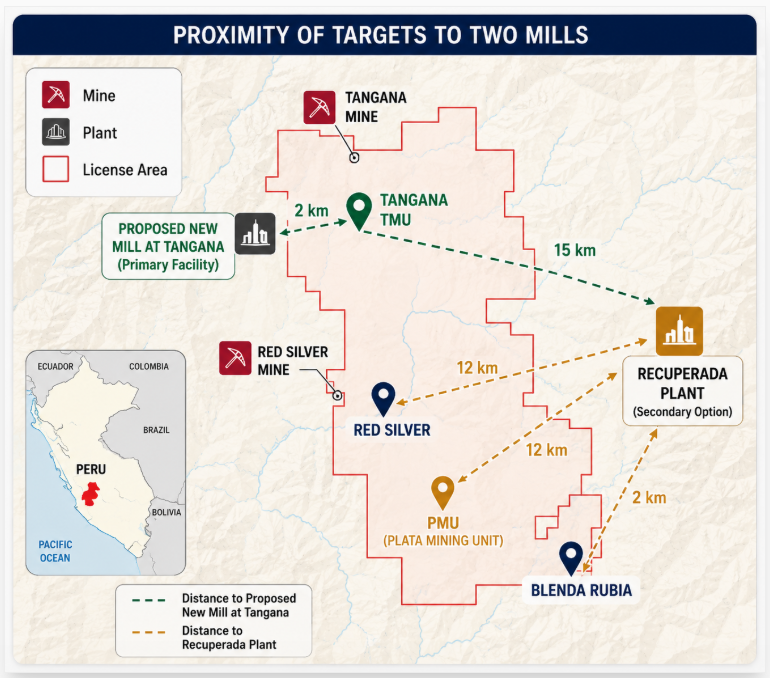

Portfolio includes the producing TMU, advanced-stage PMU, Red Silver and Blenda Rubia targets, and 200+ exploration targets, all within the Huancavelica region of Peru

Portfolio Overview

District-scale consolidation provides infrastructure synergies, lower CAPEX/OPEX, and an accelerated path from exploration to production

Source: FRC

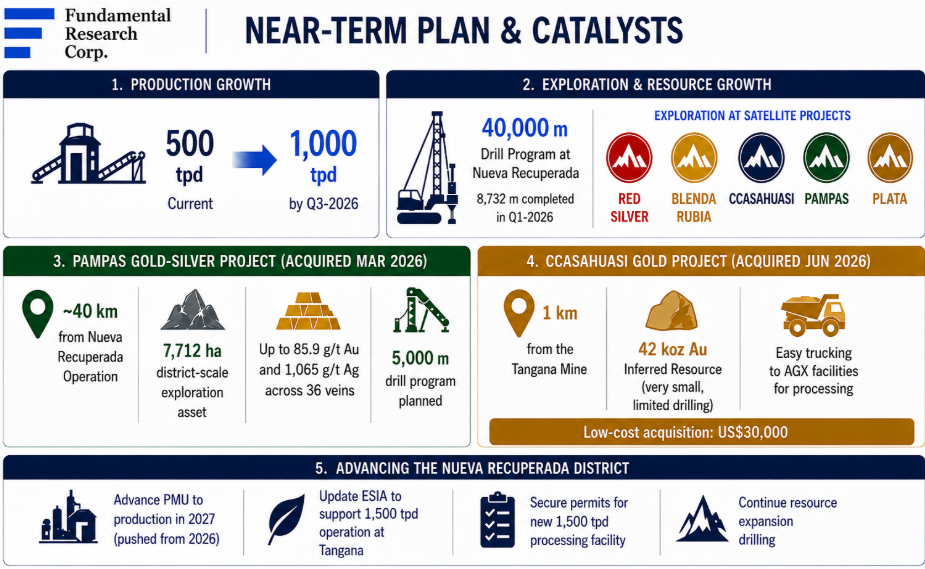

AGX plans to operate two 1,500 tpd milling facilities: a new mill at Tangana and the expanded Recuperada mill, which is scheduled to increase from 720 tpd to 1,000 tpd in Q3-2026 (permitted) and ultimately to 1,500 tpd upon receipt of permits

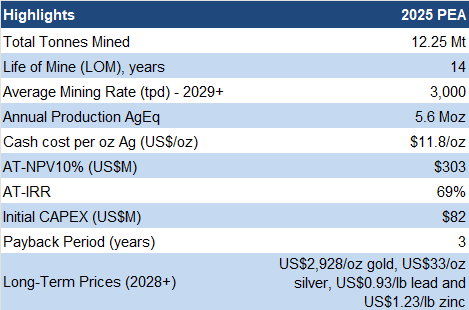

The 2025 PEA highlights the potential to increase annual production from ~1 Moz to 6+ Moz

AT-NPV10% of $303M, using $33/oz silver (spot: $66/oz), and $12/oz in cash costs

Source: Company

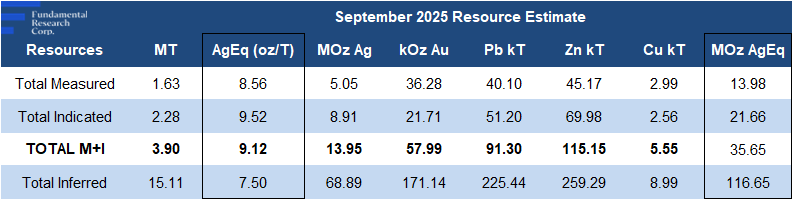

The PEA accounted for just 64% of resources, indicating further upside for NPV and IRR

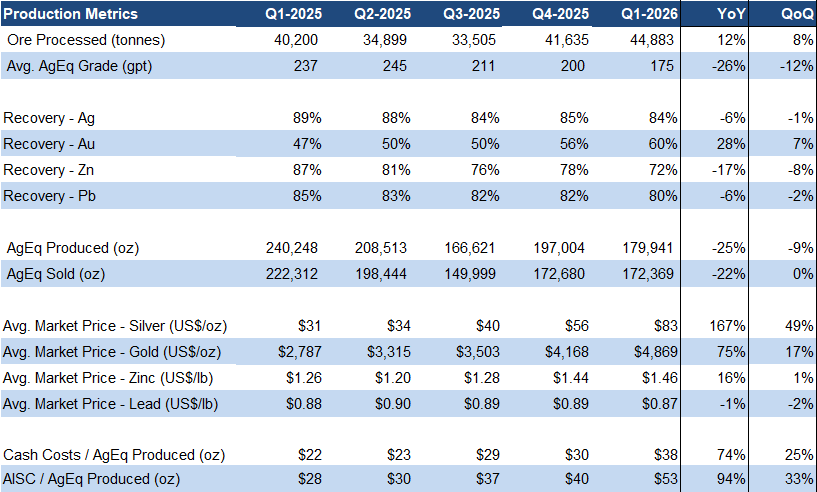

Production and Key Operating Metrics

Source: Company

Q1 production was in line with our estimate

Silver production +9% QoQ to 106 koz

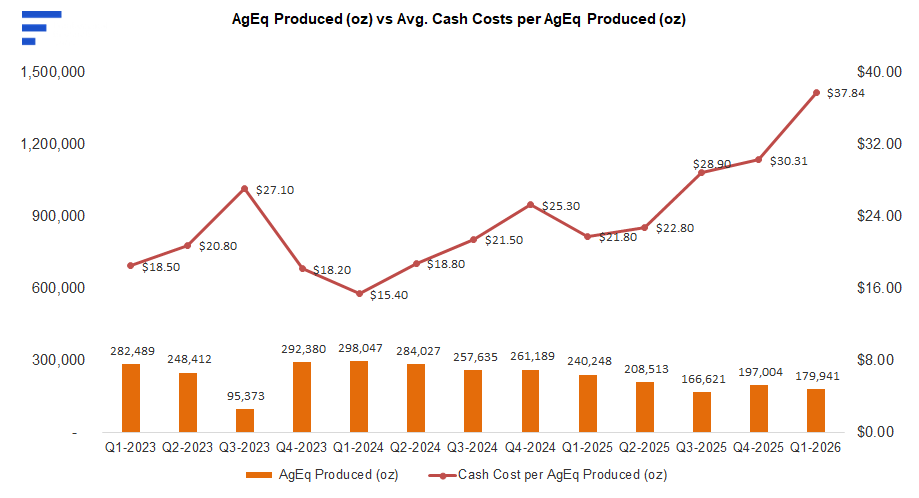

AgEq production fell 9% QoQ to 180 koz

Silver production rose on higher grades, but AgEq output fell as higher silver prices lowered by-product metal conversions

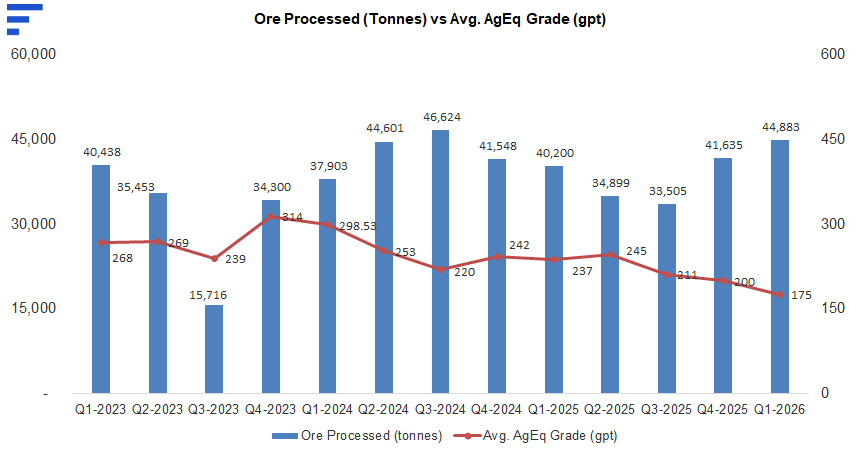

We expect grades across all metals to improve going forward as Q1 grades were materially below resource model assumptions

Source: FRC/Company

Cash costs rose 25% QoQ, driven by higher royalties resulting from stronger metal prices, in line with our estimate

Source: FRC

Targeting annual production of 6 Moz AgEq by 2029, potentially sourcing ore from TMU, PMU, Red Silver, and Blenda Rubia

Evaluating newly acquired projects as potential standalone operations with dedicated processing facilities

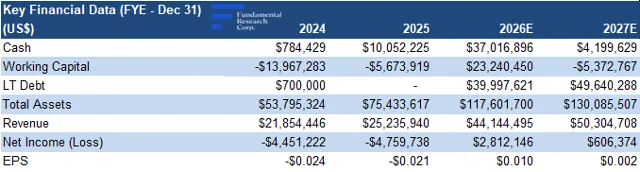

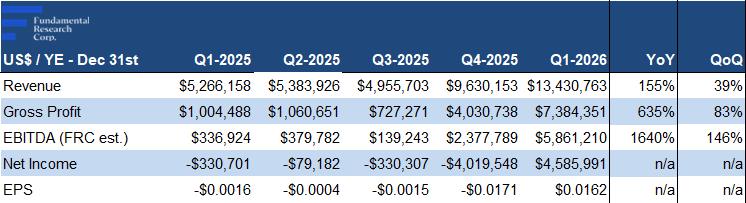

Financials

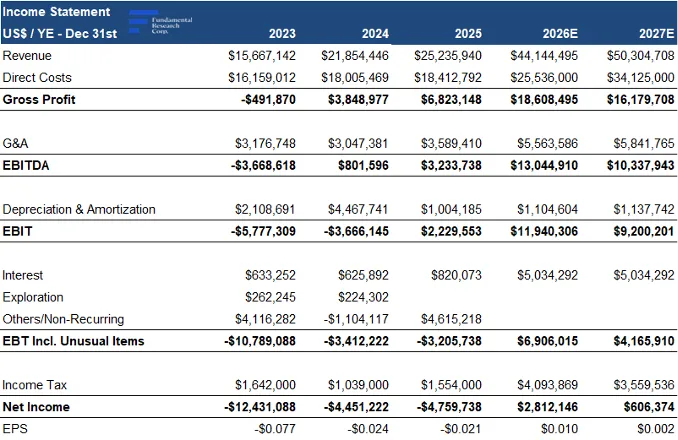

Revenue +39% QoQ on higher production, and stronger metal prices exceeding our estimate by 8%

EBITDA +146% QoQ; 14% above our forecast

Source: FRC

EPS turned positive for the first time: ($0.017) → $0.016 vs. our forecast of $0.0035

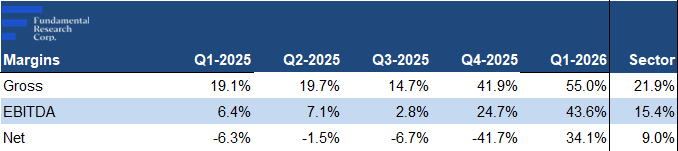

Margins significantly above sector averages

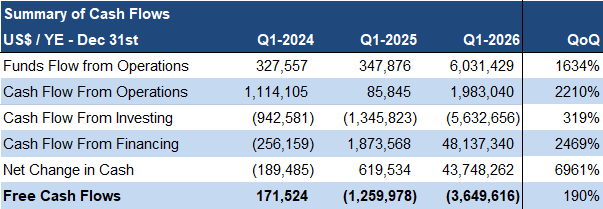

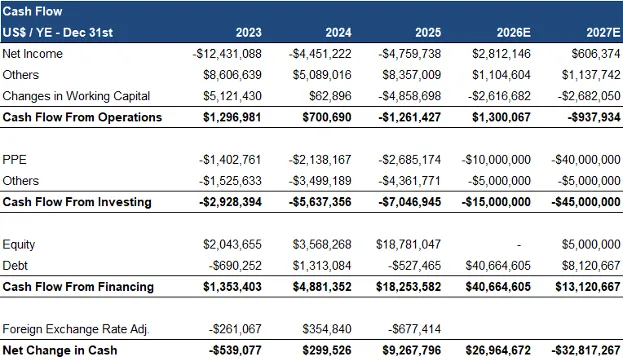

Operating cash flow increased sharply; FCF declined due to higher exploration spending, property & equipment investments, and acquisitions

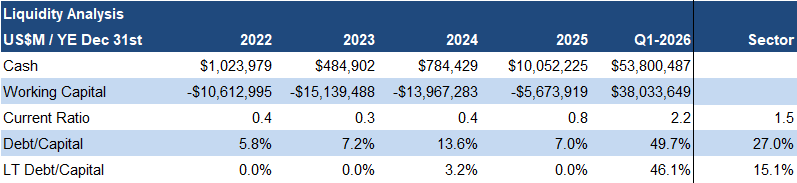

Cash balance increased significantly, driven by $50M convertible debt refinancing completed in Q1

Source: FRC / Company

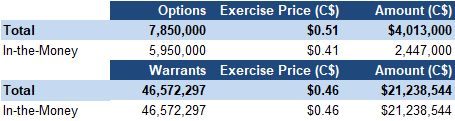

Can raise another $17M from in-the-money options/warrants

FRC Projections

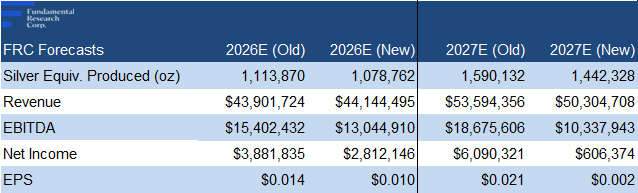

Given the recent pullback in metal prices, we are lowering our 2026 revenue and EPS forecasts

Source: FRC

We are also trimming our production forecasts slightly as our previous ramp-up timeline was a bit aggressive

Comparables Valuation

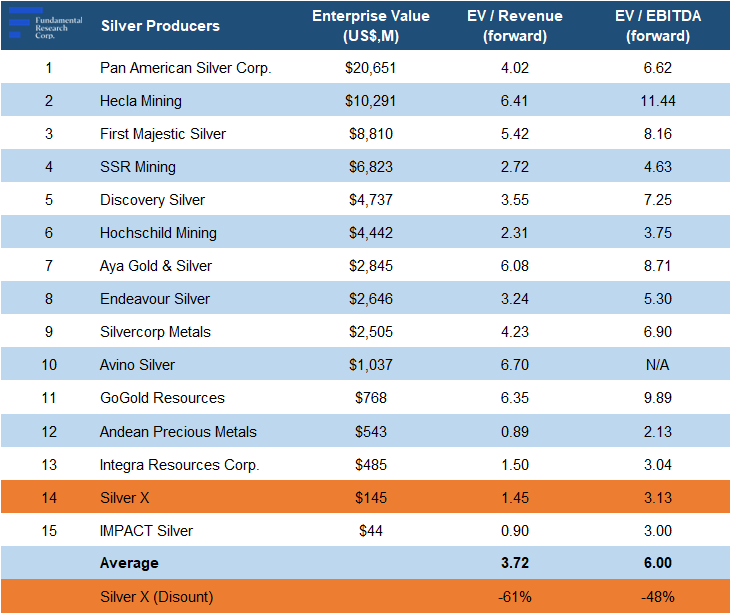

AGX’s forward EV/Revenue is 1.45x (previously 1.57x) vs the sector average of 3.72x (previously 3.64x), a 61% discount

Source: FRC / S&P Capital IQ / Various

AGX’s forward EV/EBITDA is 3.13x (previous 3.40x) vs the sector average of 6.00x (previously 6.04x), a 48% discount

Applying the sector averages, we arrived at a comparable valuation of $1.81/share (previously $1.88/share), driven by our lower revenue and EBITDA forecasts

DCF Valuation

Source: FRC

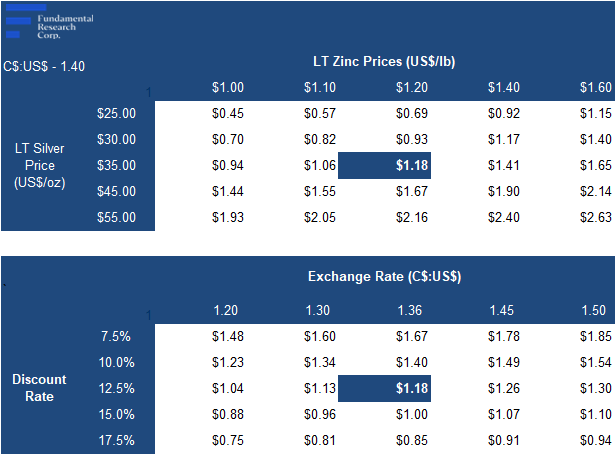

Our DCF valuation declined from $1.20 to $1.18/share, driven by lower revenue forecasts and partly offset by a weaker US$

We are reiterating our BUY rating, and adjusting our fair value estimate from $1.54 to $1.49/share (the average of our DCF and comparables valuations). While we have slightly lowered our production forecasts, AGX continues to execute well, with production, earnings, and liquidity all trending positively. We believe its growth potential and attractive valuation are not fully reflected in the current share price.

Risks

We believe the company is exposed to the following key risks:

Maintaining our risk rating of 4 (Speculative)

APPENDIX

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?