Disclosure: Delivra Health Brands Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

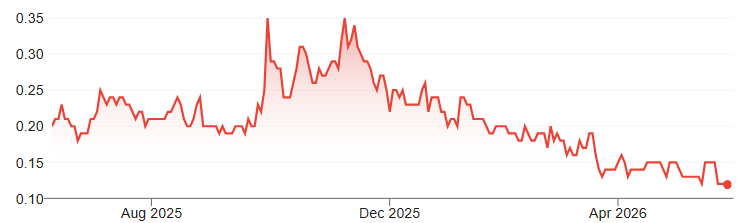

Price and Volume (1-year)

Quick insights from the CEO in our short interview

* Delivra Health has paid FRC a fee for research coverage and distribution of reports. All figures in C$ unless otherwise specified. See last page for other important disclosures, rating, and risk definitions.

Overview

Product portfolio includes sleep aid, anxiety relief, and pain relief formulations

Products

Source: Company / FRC

Asset-light model with outsourced manufacturing and packaging across North America

Two Primary Brands: Dream Water (sold in the U.S./Canada/the Middle East), and LivRelief (sold in Canada)

Available at 30k+ outlets in the U.S., and Canada, including major retailers, airports, and pharmacy chains

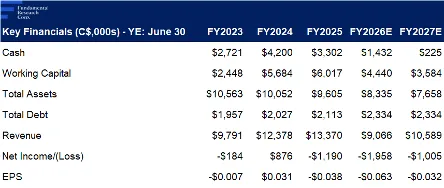

Financials (Year-End: June 30th)

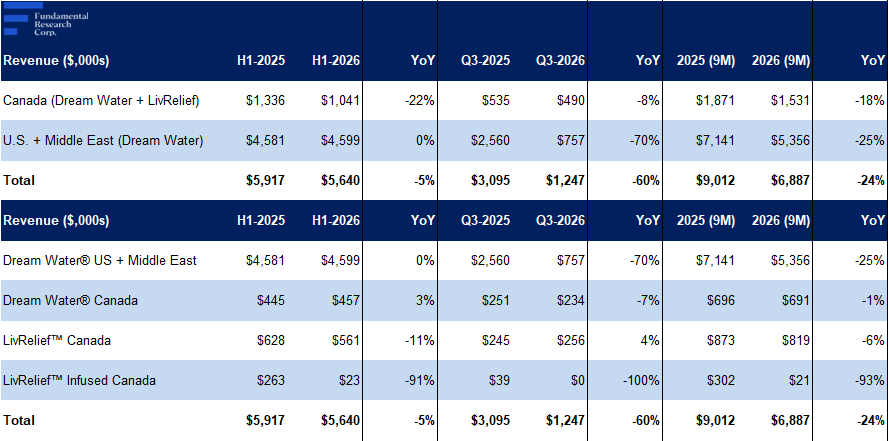

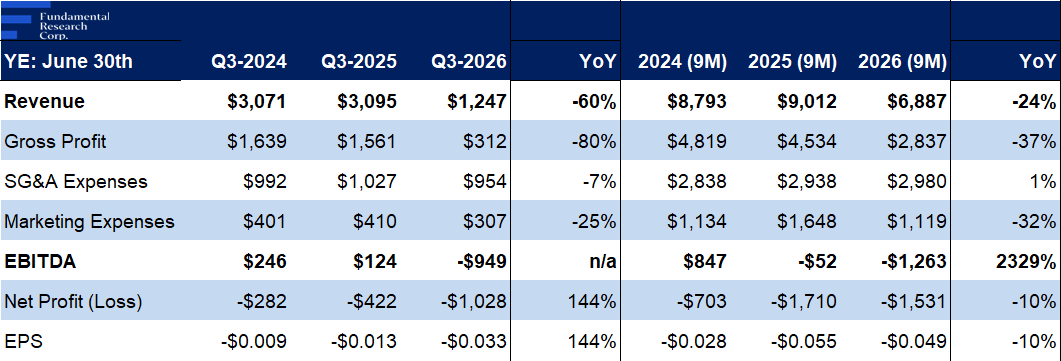

Q3 revenue -60% YoY, 29% below our estimate, driven by weak Middle East sales; Orders from the largest international distributor fell 89% YoY

Source: Company Filings, FRC

Although orders began to pick up in Q4, we still expect a weak quarter

We believe Middle East shipments will gradually normalize in the coming months as U.S.-Iran negotiations continue to progress

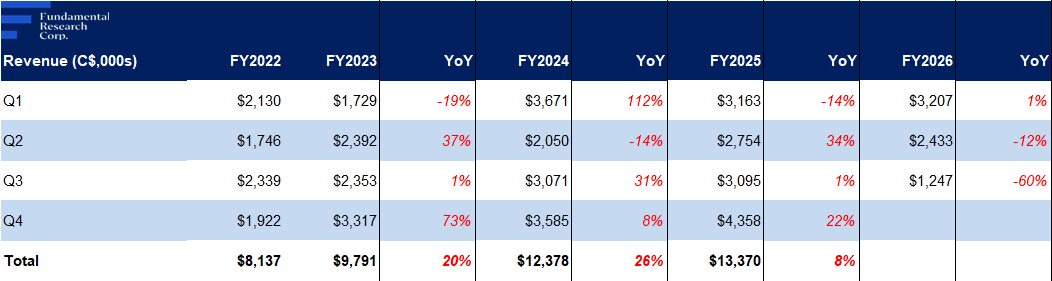

* Historically, quarterly revenue has been volatile due to the timing of orders from large customers

Bright spot: North American e-commerce sales increased 22% YoY on average across its brands, indicating strong engagement and repeat purchasing

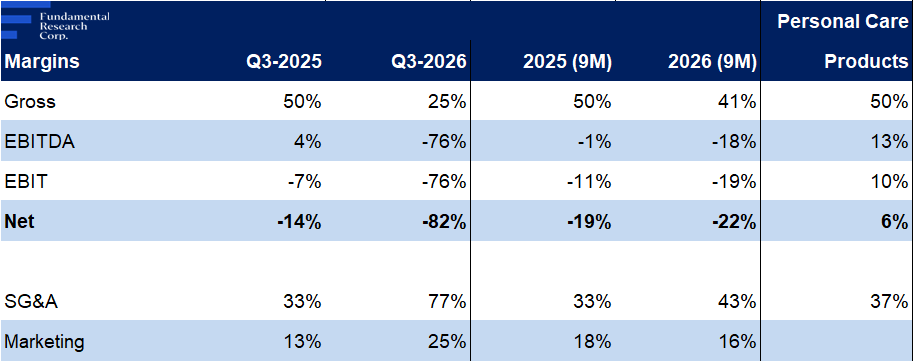

Gross margin down 25 pp YoY, 23 pp below our estimate, primarily due to lower sales

SG&A down 7% YoY; marketing expenses down 25% YoY in response to weaker revenue

EBITDA turned negative; EPS declined from ($0.01) to ($0.03), vs our estimate of a modest $0.003 profit

Source: Company Filings, FRC

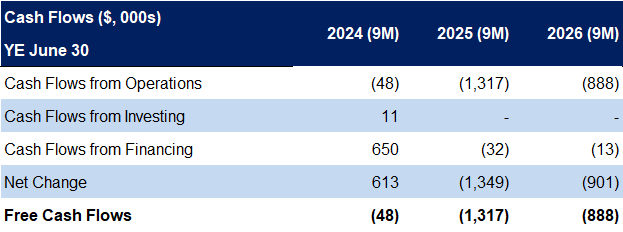

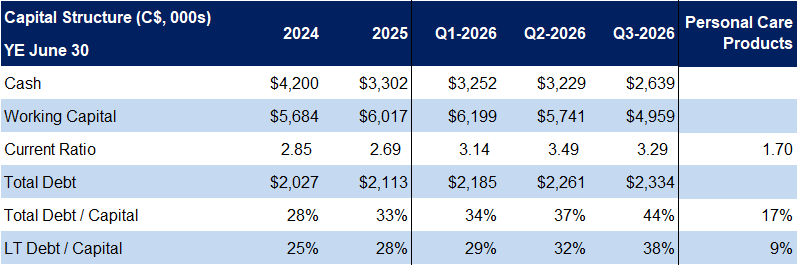

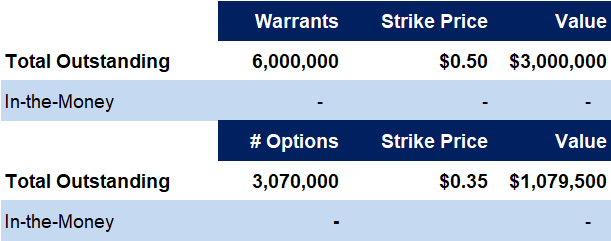

Balance sheet remains healthy despite weak operating performance

Source: Company Filings, FRC

No outstanding options/warrants are in-the-money

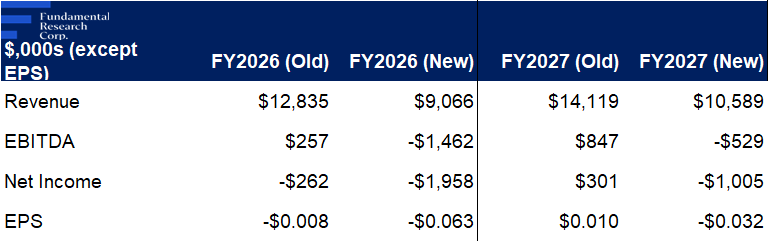

FRC Projections and Valuation

Source: Company Filings, FRC

Near-term estimates have been reduced following weaker Q3 results; FY2028+ forecasts remain unchanged

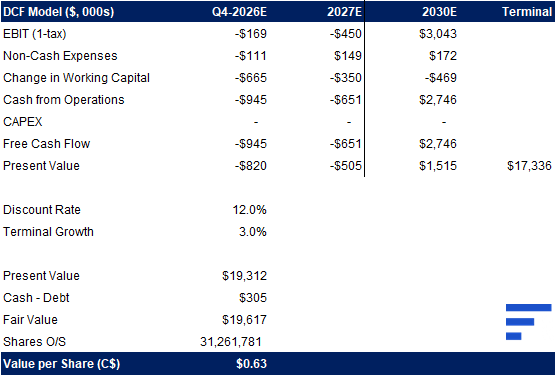

DCF Valuation

Source: FRC

As a result, our DCF valuation declined from $0.75 to $0.63/share

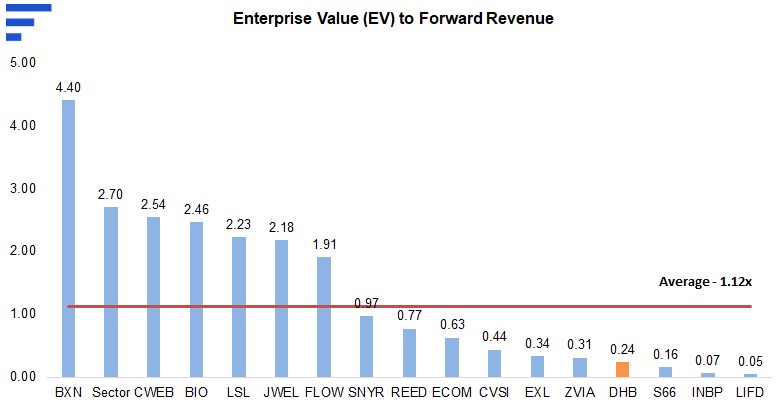

Comparables Valuation

Source: FRC/S&P Capital IQ

DHB is one of the most undervalued stocks on our list within the Personal Care Products sector

Comparables Valuation

The average sector forward EV/Revenue is up 9% since our previous report in March 2026

Source: FRC/S&P Capital IQ

DHB trades at 0.24x forward revenue vs the sector average of 1.12x, a 79% discount (69% previously)

Applying the sector EV/Revenue multiple yields a valuation of $0.41/share ($0.45/share previously), reflecting lower revenue forecasts partially offset by the higher sector multiple

Recent M&A Transactions

Source: FRC/S&P Capital IQ

Recent sector M&A transactions averaged 2.2x revenue vs DHB at 0.24x, an 89% discount

We are reiterating our BUY rating, while adjusting our fair value estimate from $0.60 to $0.53/share (the average of our DCF and comparables valuations). We view the recent revenue shortfall as a temporary geopolitical disruption rather than a deterioration in DHB 's underlying business. Given the c ompany's solid balance sheet, multiple growth initiatives, and deeply discounted valuation, we believe the risk/reward profile remains attractive.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining our risk rating of 3 (Average)

APPENDIX

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?