Disclosure: Capital Direct 1 Income Trust has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

* Capital Direct I Income Trust has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

Portfolio Summary

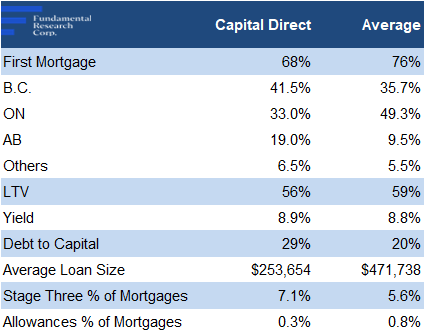

The table below compares CD IT ’s portfolio with other MICs (AUM $100M+) focused on already-built single-family residential units.

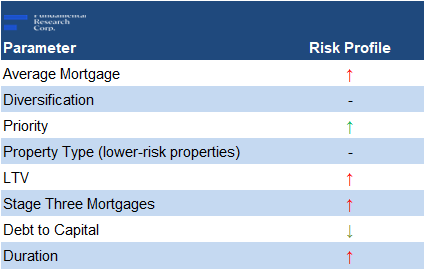

We believe CDIT operates a low-to-mid risk MIE

Lower first-mortgage exposure implies higher risk, partly offset by smaller loan sizes and lower LTVs

Source: FRC / Various

Leverage is higher, reflected in a higher debt-to-capital ratio

The yield is slightly higher despite management charging both management and performance fees, unlike most comparable MIEs, which typically do not have performance-based compensation

The sector has seen two material transactions recently (listed below). Discussions with MIC managers indicate several are actively pursuing M&A to scale their platforms, drive synergies, and achieve cost savings across administration, operations, and staffing. We believe t hese efficiencies can support higher yields, and attract additional capital. While CD IT has not indicated any acquisition plans, we would not be surprised to see either a strategic transaction, or a potential bid from a larger player.

September 2025: Alta West Mortgage Capital Corporation acquired Premiere Home Mortgage for an undisclosed amount.

October 2025: Neighbourhood Holdings acquired Fisgard Asset Management for an undisclosed amount, creating one of Canada’s largest alternative mortgage lenders with over $750M in AUM across 1,550 mortgages .

Portfolio Update

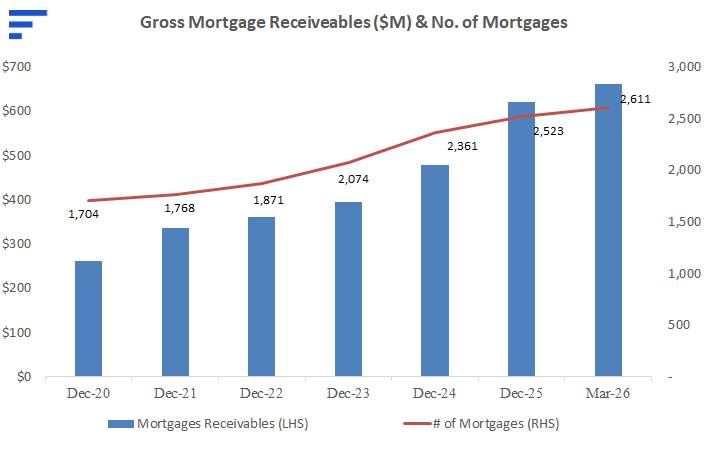

In 2025, mortgage receivables were up 30% to $616M, 15% above our forecast

In Q1-2026, receivables increased 7% QoQ to a record $659M

Source: Company / FRC

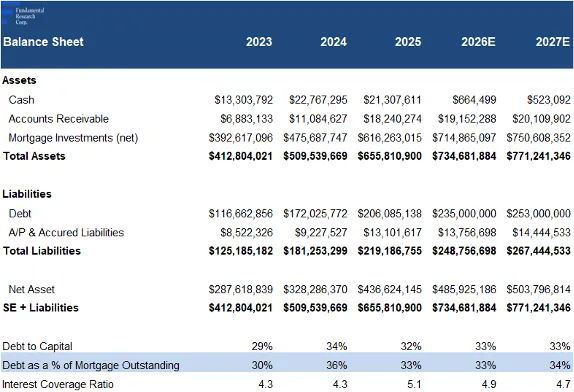

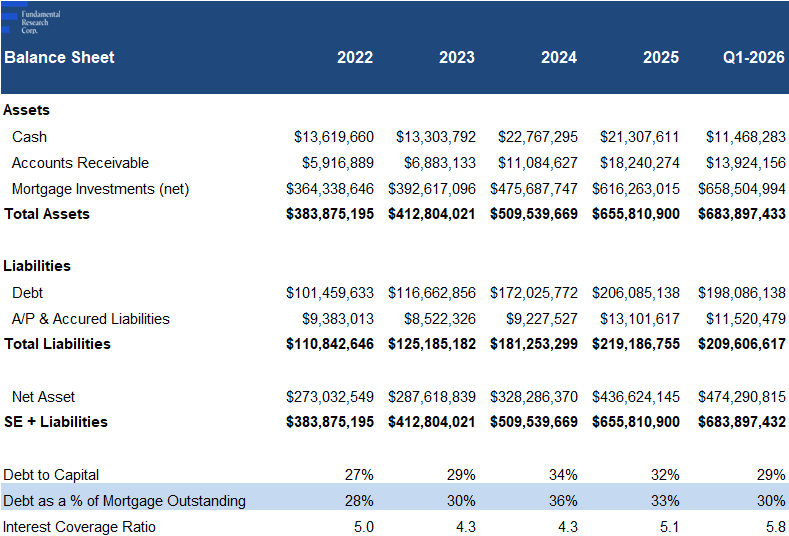

At the end of Q1-2026, debt-to-capital was 29%, in line with comparables (20%–40%)

The interest coverage ratio is on the higher end of comparables (3x–5x), implying stronger debt servicing capacity

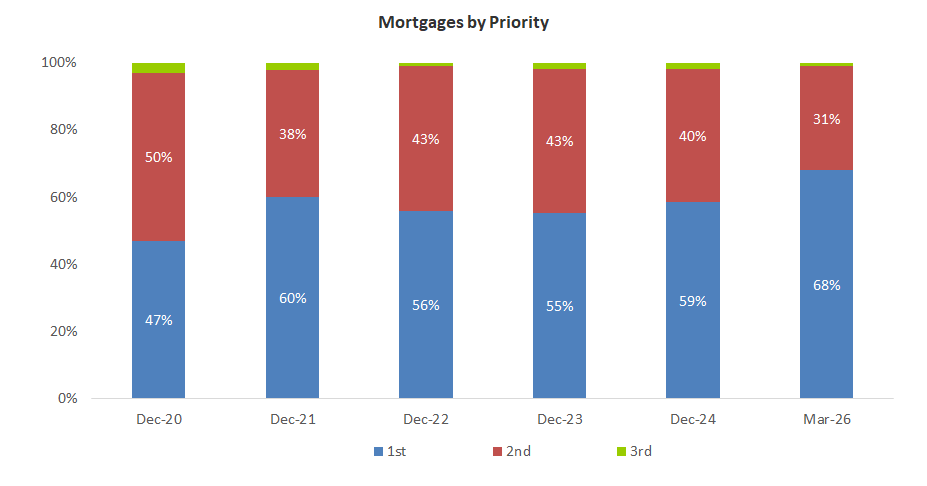

At the end of Q1-2026, exposure to first mortgages increased 9 pp since year-end 2024 to 68%, implying a lower risk profile

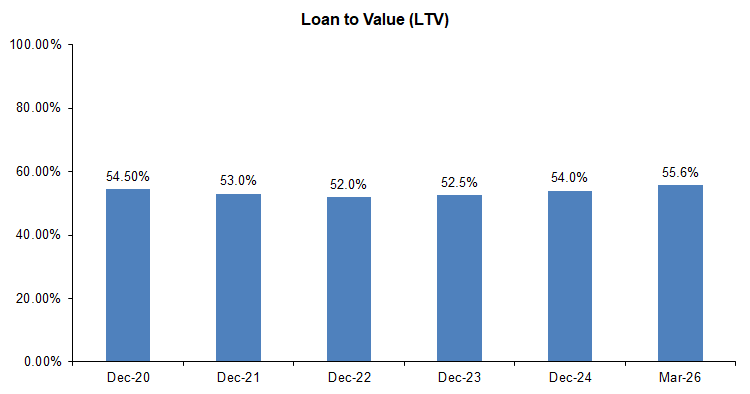

LTV increased slightly, but remains below the sector average of 59%, implying lower relative risk

Source: Company / FRC

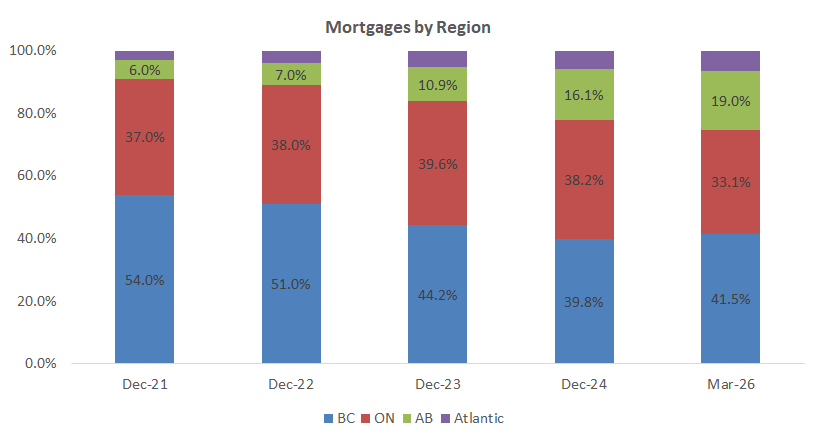

Increased B.C. and Alberta exposure, with a corresponding decrease in Ontario

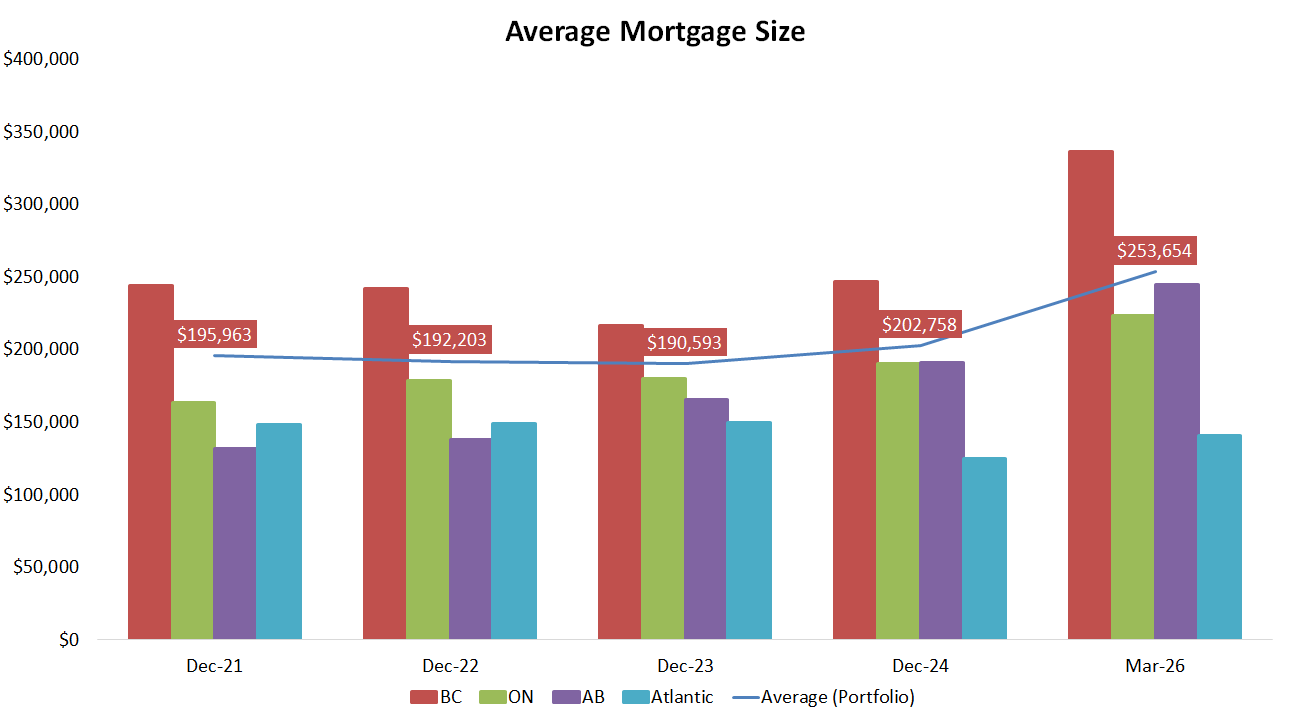

The average mortgage size increased 25% since the end of 2024 to $254k

Source: Company / FRC

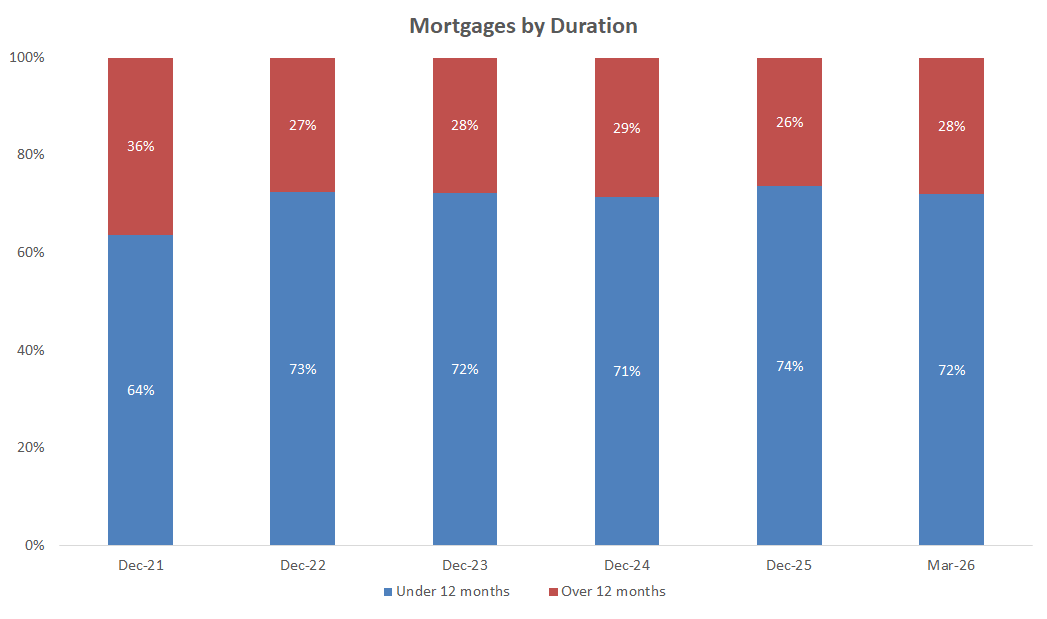

Duration increased but remains in line with the historical average; generally higher duration implies greater interest rate risk

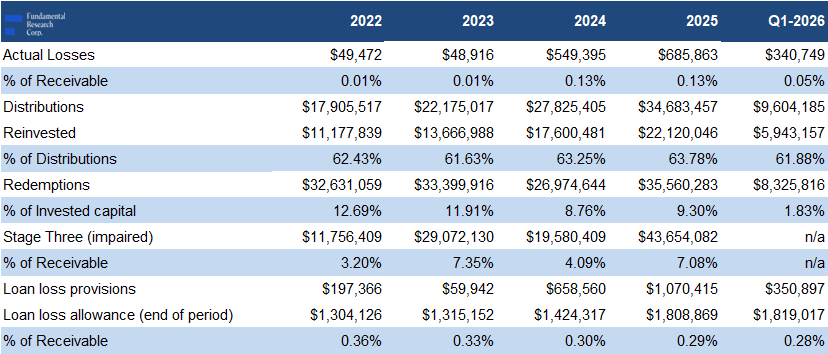

In 2025, stage three (default) mortgages increased 3 pp YoY to 7% of mortgages, above the sector average of 6%, implying elevated risk levels

However, allowances were 0.3% of receivables, well below the 0.8% sector average, suggesting management does not expect material losses from defaults

Source: FRC

In summary, we believe the portfolio’s risk profile has remained stable despite more red than green signals, with higher default risk offset by the increase in first mortgages

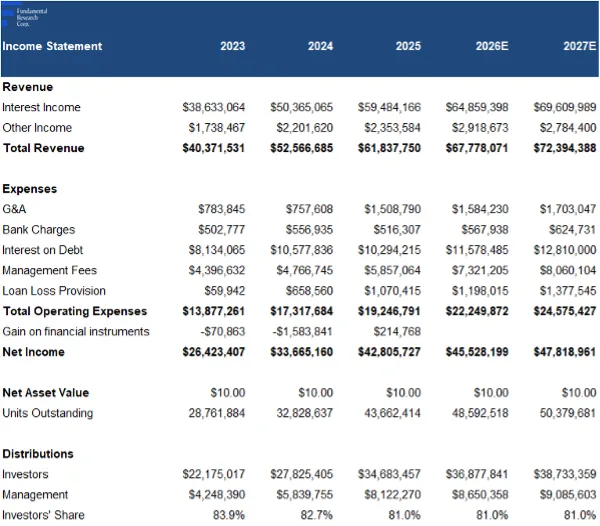

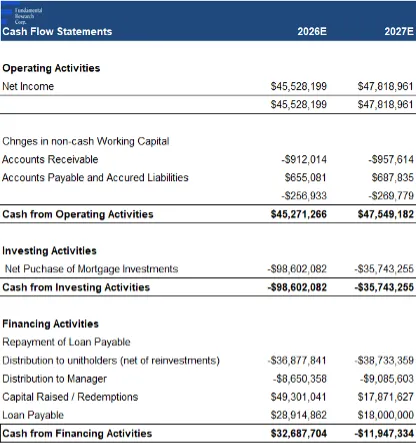

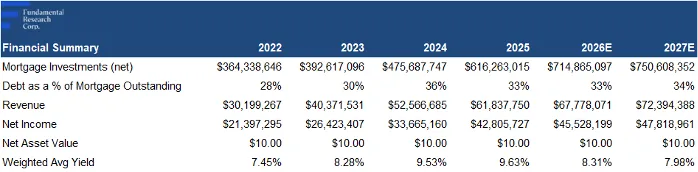

Financials

Note that the above figures may be slightly different from the figures reported by Capital Direct due to the difference in the method of calculation. We used the average of the opening balance, and year-end balance of the mortgages outstanding, and invested capital, to arrive at the above figures.

Source: Company / FRC

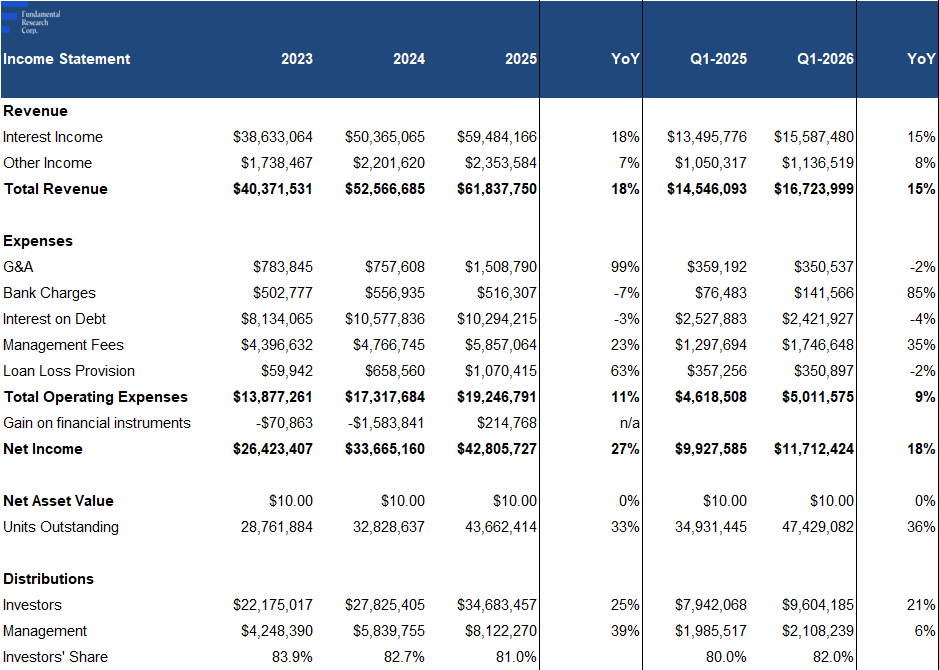

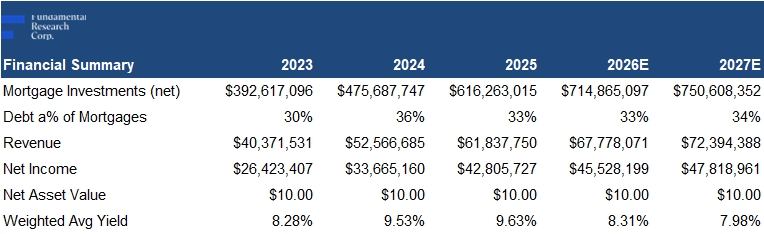

2025 revenue rose 18% YoY, beating our estimate by 8%, driven by higher mortgage receivables, partially offset by lower rates

Net income was up 27% YoY, beating our estimate by 12%

In Q1-2026, revenue and net income were up 15% YoY, and 18% YoY, respectively

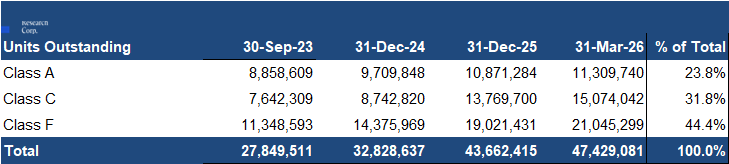

Units Outstanding and Ownership

Source: Company / FRC

47M units outstanding at the end of Q1-2026, up 44% since the end of 2024

Source: Company / FRC

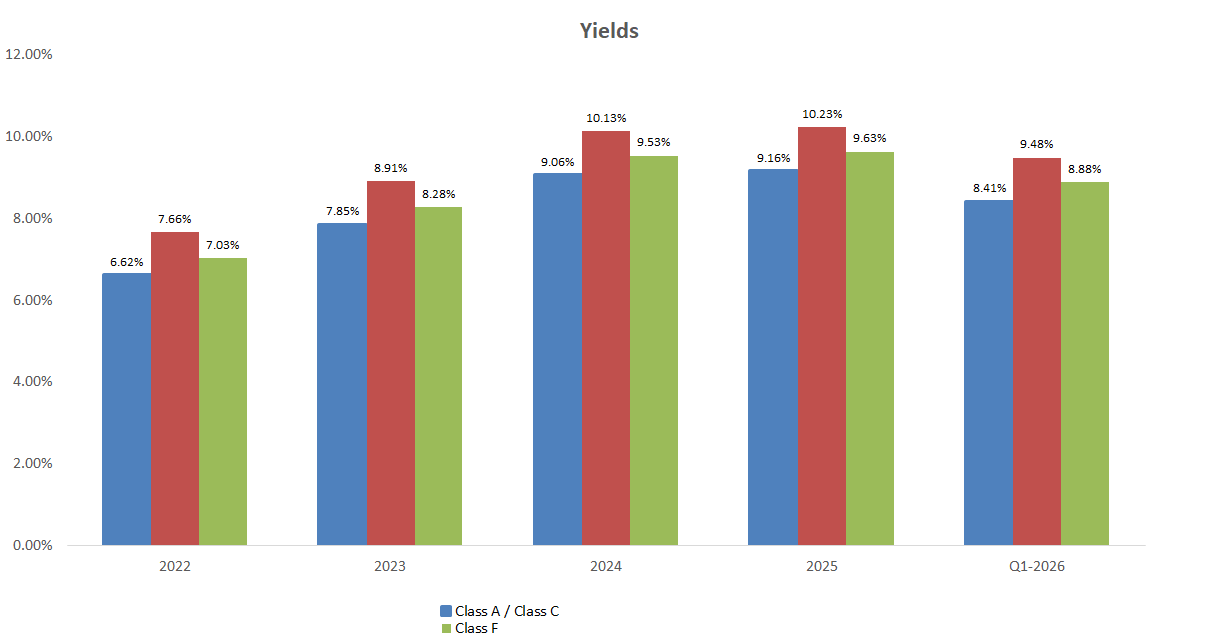

The yield rose from 9.53% in 2024, to 9.63% in 2025 (vs 9.29% forecast), then declined to 8.88% in Q1-2026 amid lower rates

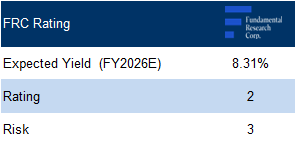

FRC Projections and Rating

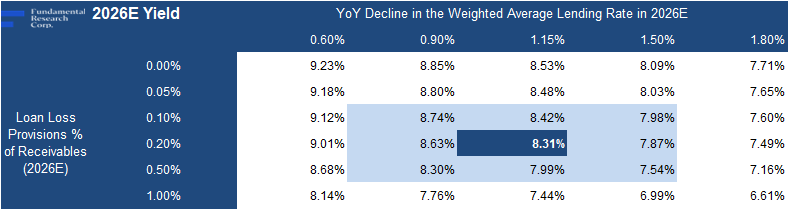

With rates peaking last year, we expect yields to decline in FY2026

We are projecting a yield of 8.31% in FY2026 vs 9.63% in 2025

Source: FRC

Our FY2026 yield estimate varies between 7.54% and 8.74%, as loan loss provisions and lending rates vary

We reiterate our overall rating of 2, and risk rating of 3. CDIT remains a leading Canadian MIE, delivering strong earnings supported by record mortgage receivables, and above-average yields. While we expect yields to moderate, we view CDIT as well-positioned in a consolidating sector. The macro backdrop remains supportive, with stable interest rates, and lower expected default risk, supporting mortgage demand and portfolio stability.

Risks

APPENDIX