- Macroeconomic backdrop: We expect rates to stay stable through 2026, as unemployment levels have eased since peaking in September 2025, and inflation remains moderate. A stable rate environment should support lower default risk, and improving mortgage origination momentum.

- Portfolio focus: Development and construction activity remains subdued amid lower immigration, weaker GDP growth, geopolitical uncertainty, and U.S. trade tensions. Management continues to shift toward lower-risk property types, including single-family residential, and income-producing commercial assets. AI also plans further expansion into Alberta and B.C., including a new Alberta office, which should improve geographic diversification, given Ontario currently represents over 90% of the portfolio.

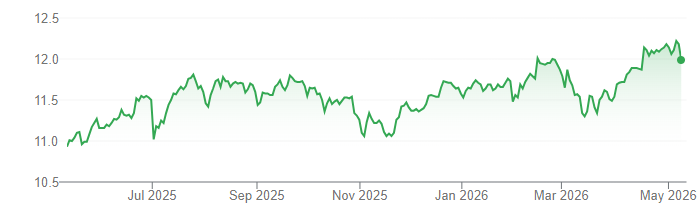

- Market positioning: Historically, declining rates have benefited MICs and financials. However, MICs have lagged broader financials over the past year (+10% YoY vs +39% YoY), and traded more in line with REITs (+12% YoY), reflecting continued weakness in residential real estate sentiment. We believe a gradual housing market recovery should support MIC stocks this year.

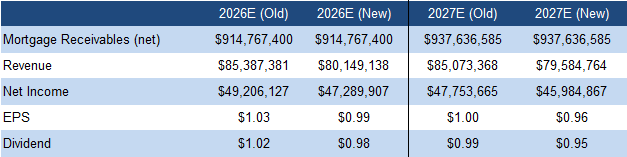

- 2026 Outlook: We now project a dividend of $0.98/share (previously $1.02/share), implying an 8.28% yield.

Price and Volume (1-year)

| |

YTD |

12M |

| AI |

4% |

10% |

| TSX |

7% |

33% |

| XFN (Financial) |

8% |

39% |

| XRE (REIT) |

8% |

12% |

* Atrium Mortgage Investment Corporation has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise stated.

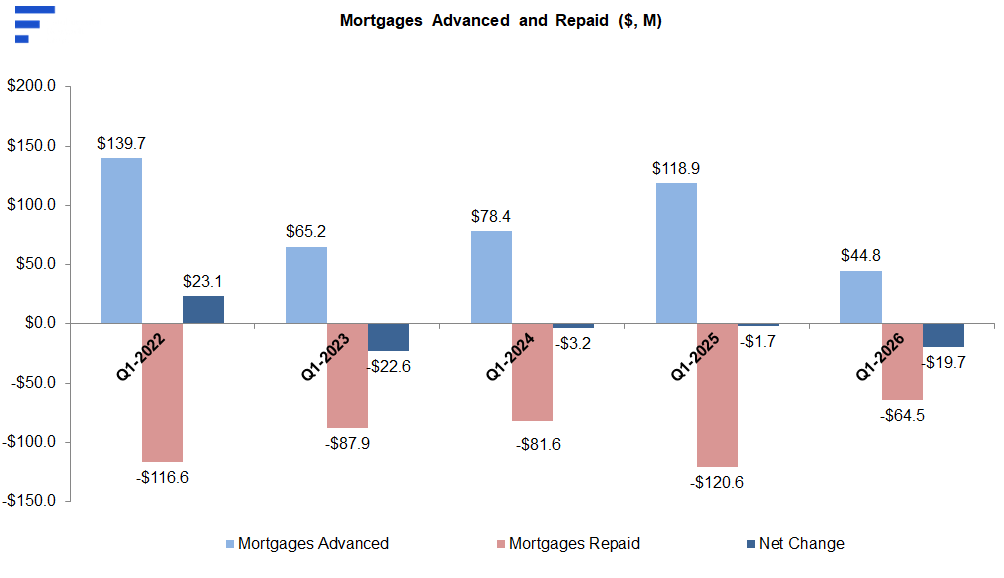

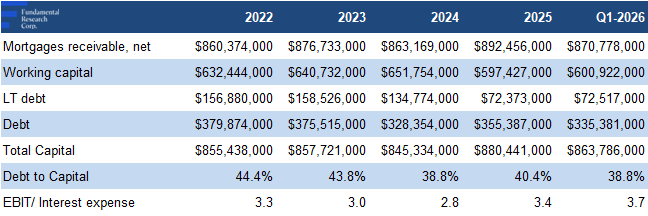

Loan advances declined 62% YoY, marking the softest Q1 in more than a decade, while repayments fell 47% YoY, driving a 2% QoQ decline in net mortgages outstanding to $871M

Portfolio Update

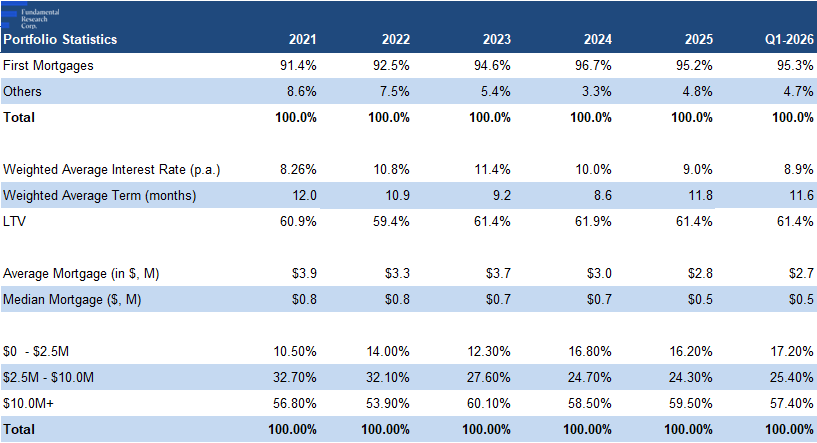

First mortgages and LTVs remained relatively stable QoQ

AI’s lending rates continued to ease following BoC rate cuts; since peaking in 2023, rates have declined 2.50 pp vs a 2.75 pp decline in the benchmark rate, suggesting AI’s rates are less elastic

Credit facility borrowing costs also declined QoQ, from 5.08% to 4.57%, partially offsetting spread compression

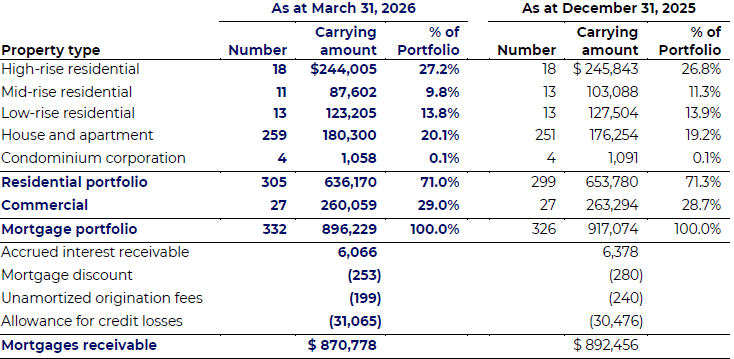

Mortgages by Property Type

Source: Company Data / FRC

Exposure to property types remained unchanged, with continued focus on revenue-generating commercial properties, and built single-family units, relatively low risk segments vs development projects

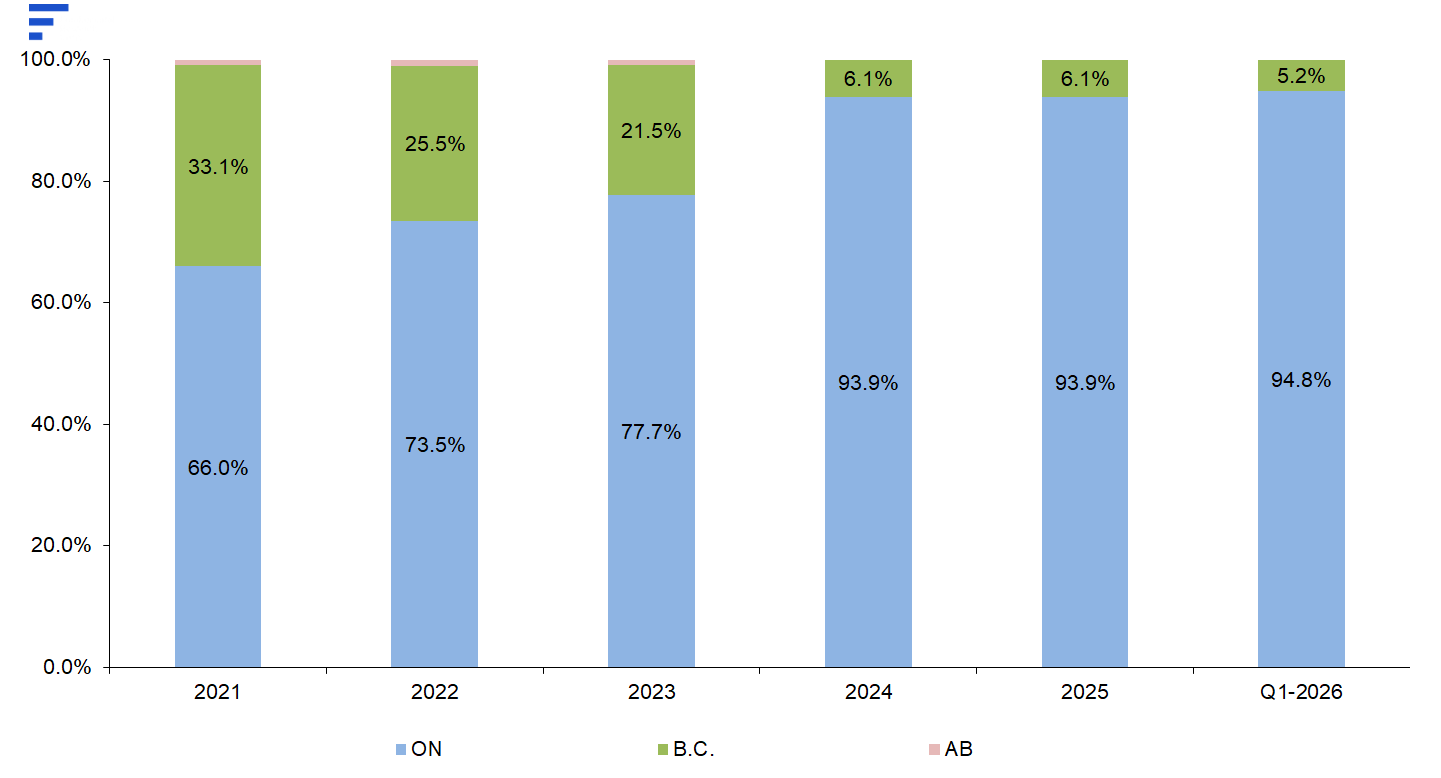

Mortgages by Region

Continued to increase exposure to Ontario, weighing on geographic diversification

However, AI plans to expand further into Alberta and BC in coming quarters, including opening a new Alberta office to support grow

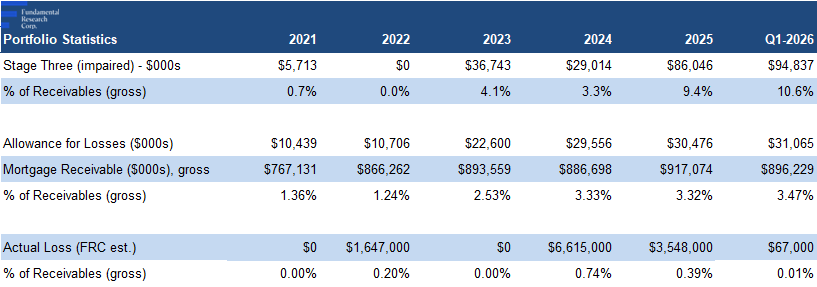

Stage three (impaired) mortgages rose 10% QoQ to $95M on one additional default

Source: FRC / Company

AI expects two loans ($41M) to be repaid or refinanced by May-end, which should reduce stage three exposure from 11% to 6% of total mortgages vs 9% at year-end 2025, and a historic average of 3%

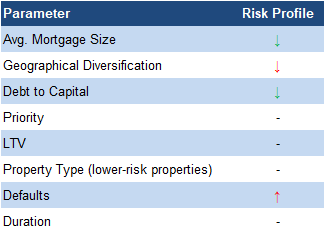

*Red (green) indicates an increase (decrease) in risk level.

Source: FRC

Overall, we believe the portfolio’s risk profile has edged higher, primarily driven by higher impaired mortgages

Financials

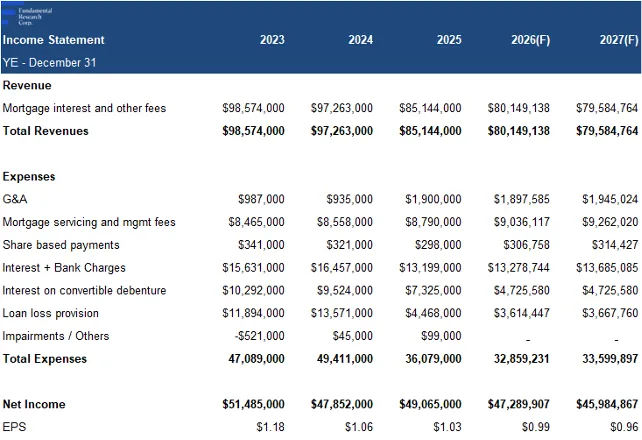

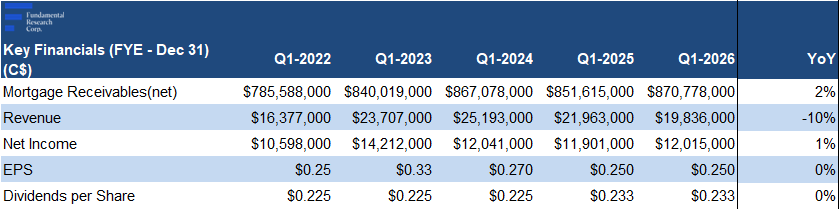

Revenue declined 10% YoY on lower rates, partially offset by higher mortgage receivables, and came in 6% below our estimate

*The calculations in the above table are approximate as we used the average of beginning and end of period mortgages outstanding.

Net income increased 1% YoY due to lower loan loss provisions, but was 4% below our estimate

Annual regular dividend held steady at $0.93/share

* Our calculations are slightly different from the company’s calculations.

Source: Company / FRC

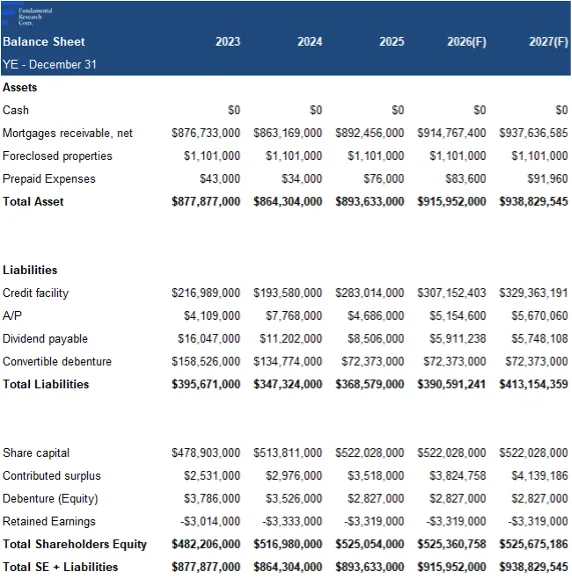

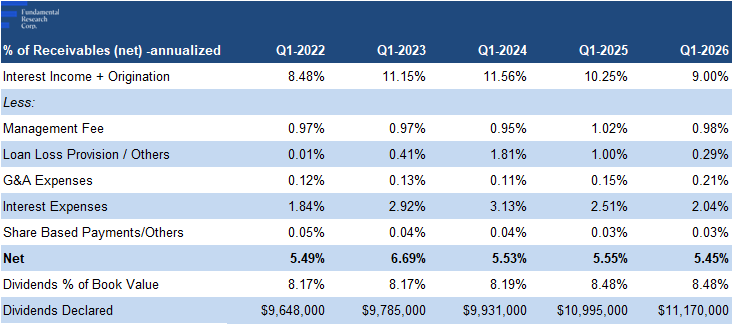

Debt-to-capital decreased slightly, driven by softer lending activity

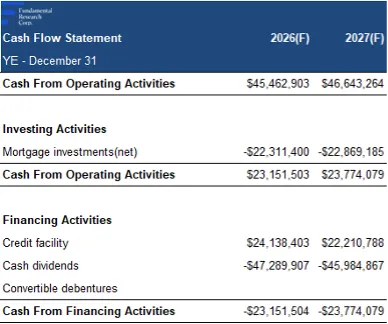

FRC Forecasts & Valuation

As Q1 revenue and EPS came in below expectations, we are lowering our full-year estimates

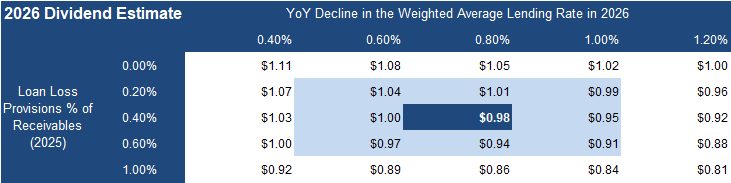

Our estimate for the 2026 dividend varies between $0.91 and $1.04/share, as loan loss provisions and lending rates vary

Source: FRC

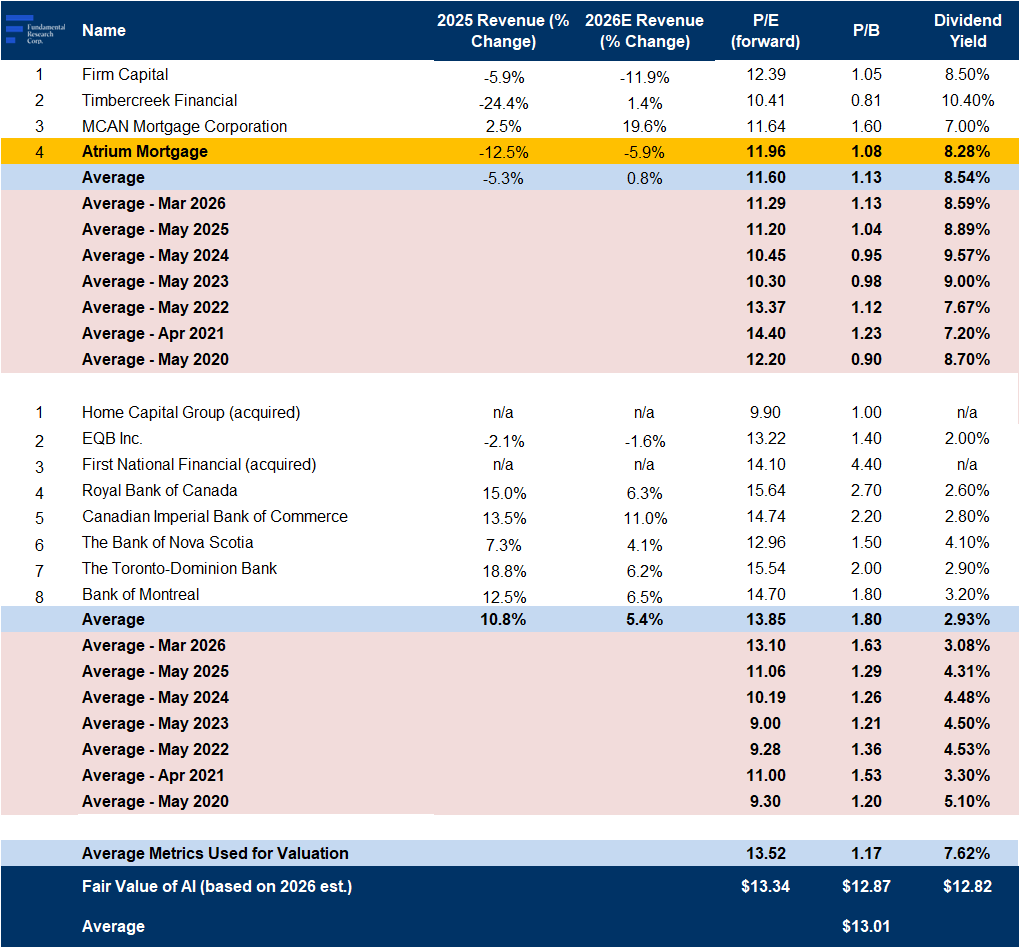

Source: S&P Capital IQ / FRC

Sector multiples are up 6% YoY, and 2% since our March 2026 report

On average, MICs and banks are expected to report 6% revenue growth this year vs 4% in 2025, primarily driven by lower rates

Our fair value estimate decreased from $13.12 to $13.01/share, driven by a lower EPS forecast, partially offset by higher sector multiples

We reiterate our BUY rating, and adjust our fair value estimate from $13.12 to $13.01/share, implying a potential return of 19% (including dividends) in the next 12 months. Soft Q1 lending activity led to lower revenue and declining mortgages, though lower loan loss provisions helped support earnings. Looking ahead, a stable interest rate environment, and easing credit conditions, should support improved mortgage origination, and lower default risk. We believe a gradual housing recovery should support MIC stocks this year.

Risks

We believe the company is exposed to the following risks:

- Diversification – over 90% of Atrium's mortgages are secured by properties in ON

- Credit

- A downturn in the real estate sector may impact the company’s deal flow

- Timely deployment of capital is critical

- Investments in mortgages are typically affected by macroeconomic conditions, and local real estate markets

- Highly competitive sector

- Like most MICs, the company uses leverage to fund mortgages

- Default rates can rise during recession

- Geopolitical risks and the potential for a tariff-induced recession

Maintaining our risk rating of 3 (Average)

APPENDIX