Kidoz Inc.

Record Revenue / Child-Safety Rules Driving Gaming Migration

ByFRC Analysts

Disclosure: Kidoz Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

- Margin pressure (key surprise): Gross margins compressed 6 pp YoY, which caught us slightly off guard. Management attributes this to a deliberate shift toward bulk sales at discounted pricing to drive repeat business, with a modest drag on margins. Despite the decline, we note that KDOZ’s margins remain in line with sector peers.

- Earnings & cash flow improvement: EPS increased 29% YoY to $0.003, missing our forecast of $0.008, due to lower gross margins. Free cash flow grew 27% YoY.

- Balance sheet strength: No outstanding debt, and ongoing profitability, mean there is no reliance on external financing, or risk of share dilution.

- Resilient digital ad growth: Global digital ad spend remains strong, expected to grow ~8% in 2026 (~9% in 2025), driven by continued digital shift, mobile usage growth, and AI-based ad optimization.

- Stricter child-safety regulations → gaming migration: Policies such as Australia’s under-16 social media restrictions, EU Digital Services Act enforcement, and U.S. COPPA crackdowns are limiting children’s access to social media, shifting engagement to mobile gaming, and child-safe apps, supporting Kidoz’s audience base.

- Valuation & outlook: We expect record revenue and EPS in 2026. KDOZ trades at 1.20x forward EV/Revenue vs 2.81x sector average (~58% discount), highlighting significant valuation upside.

Price and Volume (1-year)

* Kidoz Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures are in US$, except share price, fair value, and MCAP data, which are in C$.

Two offerings on the same underlying platform, serving different audience segments across the full demographic spectrum

Company Overview

KIDOZ is a child-safe network that delivers ads through a platform integrated into mobile games, and apps

Launched in 2023, Prado adapts Kidoz’s core technology, and extends it to serve a broader, non-kid mobile audience

Reaches 500M+ gamers every month across 40k+ games

Source: Company

Used by major brands such as Disney (NYSE: DIS), LEGO (NYSE: LEGO), Mattel (NASDAQ: MAT), McDonald’s (NYSE: MCD), and others, reflecting trust from leading global advertisers

Three straight years of revenue growth; turned profitable in 2024

Sector Trends & Implications

Source: FRC / Various

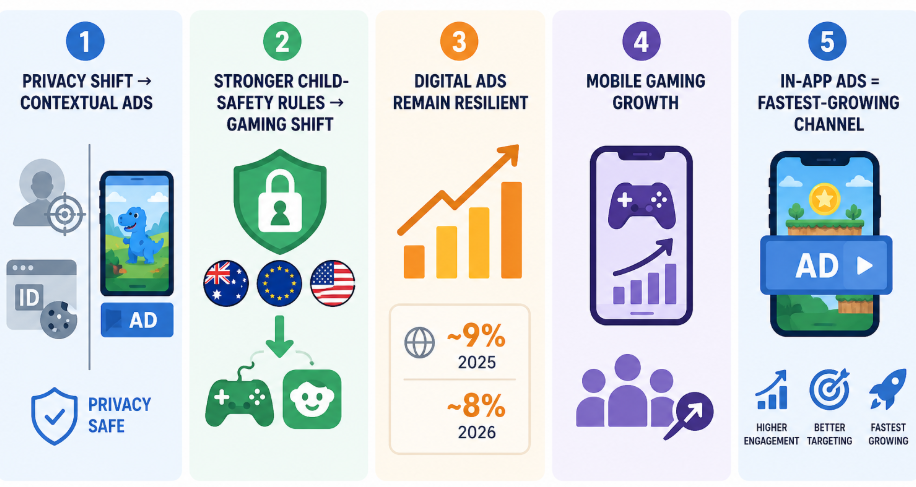

Kidoz is positioned at the intersection of privacy-first advertising, mobile gaming growth, and accelerating in-app ad demand

- Shift to contextual, privacy-first ads: Privacy laws are accelerating the move away from identity-based targeting toward contextual advertising, where ads match content rather than user identity. We believe Kidoz benefits directly as a privacy-safe, contextual ad network built for kids.

- Stricter child-safety regulation → gaming migration: Policies such as Australia’s under-16 social media restrictions, EU Digital Services Act enforcement, and U.S. COPPA crackdowns are limiting children’s exposure to social media. This is shifting attention toward mobile gaming and kid-safe apps, supporting Kidoz’s audience base.

- Resilient digital ad growth: Global digital ad spend remains strong, expected to grow ~8% in 2026 (~9% in 2025), driven by continued digital shift, mobile usage growth, and AI-based ad optimization.

- Mobile gaming expansion: Mobile gaming continues to grow at a high-single to double-digit rate, supported by rising smartphone penetration across all ages, expanding opportunities for Kidoz.

- In-app advertising acceleration: In- app ads (ads inside mobile apps and games) are the fastest-growing digital ad format due to higher engagement, incremental reach, and stronger performance versus web display. Kidoz is directly exposed to this high-growth channel.

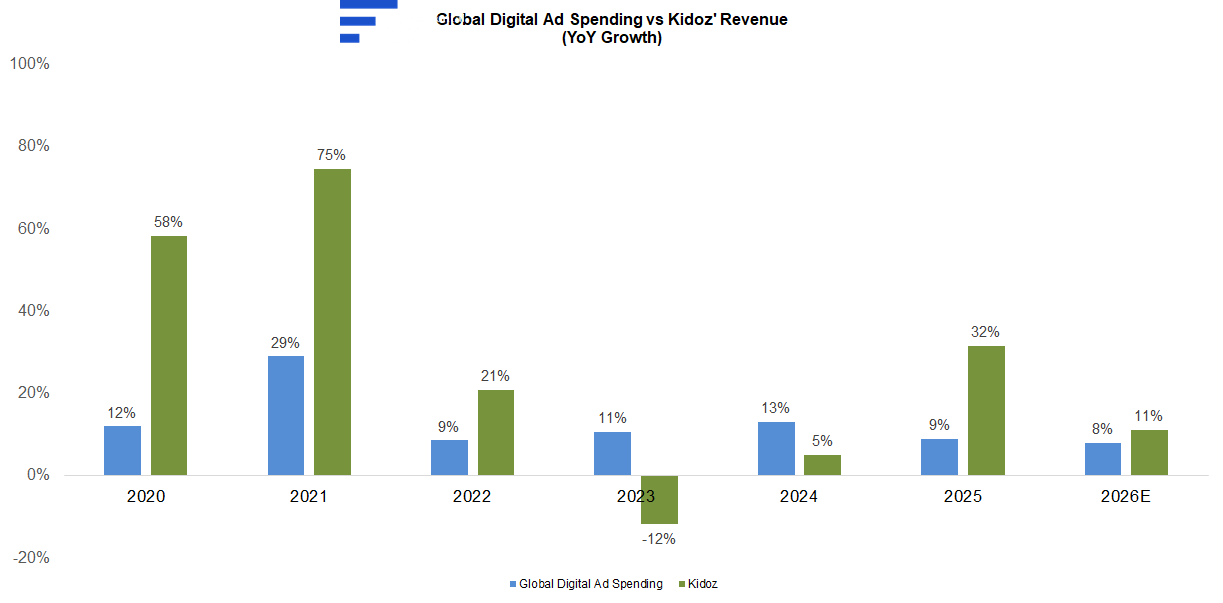

Historically, we estimate that KDOZ's revenue growth outpaced global digital ad spending growth by 2.1x on average

Source: FRC / Various

Financials

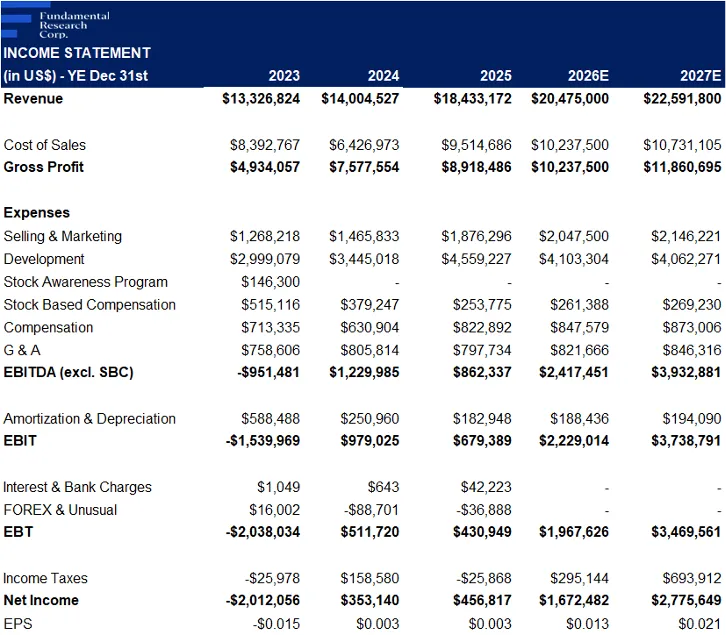

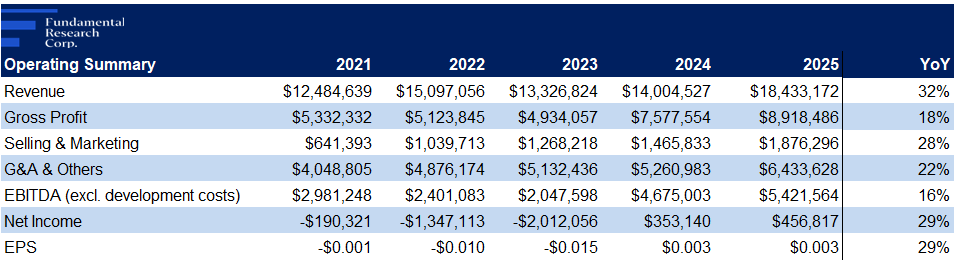

2025 revenue was up 32% YoY, to a record high of $18M, 3% above our estimate

Source: FRC / Company

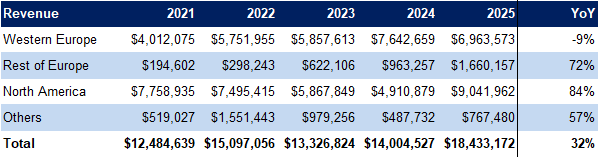

North America accounted for 49% of revenue, up from 35% in 2024

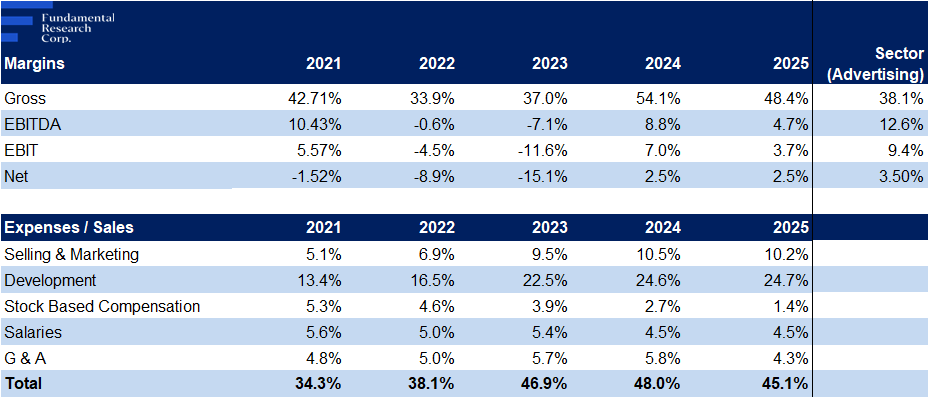

Gross margins fell 6 pp YoY to 48%, 5 pp below our forecast, due to shifting prioritisation of higher volume /lower-margin revenue. We are lowering our near and long-term margin forecasts accordingly. Note that the advertising industry’s average gross margin is ~38%, compared to ~40–60% for digital ad companies, indicating Kidoz remains within the broader industry range.

Gross margins compressed 5 pp YoY

G&A, development, and other expenses rose 27% YoY, in line with our estimate, mainly due to higher staff and infrastructure costs, to support growth and increased R&D spending on AI integration; a strategic investment we view positively for competitiveness

In our view, stronger-than-sector revenue growth in 2025 suggests the company’s R&D investments are proving effective

Higher revenue, partially offset by higher costs, drove EPS up 29% YoY to $0.003, vs our $0.008 forecast

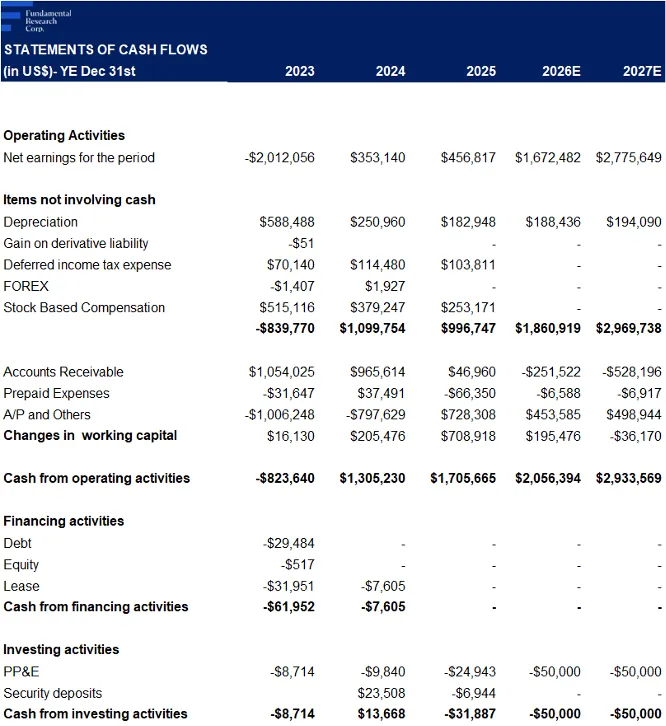

Free cash flows were up 27% YoY

Source: FRC/Company

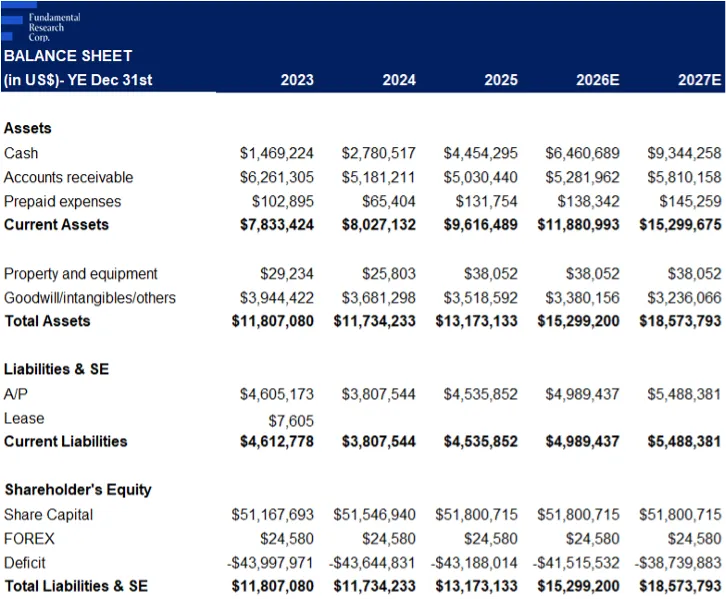

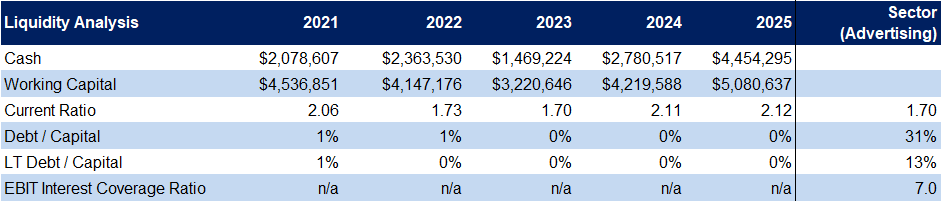

Balance sheet remains healthy with zero debt; as the company is profitable, we see no need for financing or potential share dilution

FRC Projections and Valuation

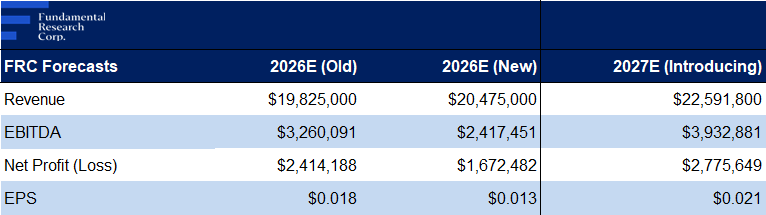

We are raising our short- and long-term revenue forecasts, supported by a strong Q4, and robust ad outlook, while lowering EPS forecasts due to gross margin pressure

Source: FRC

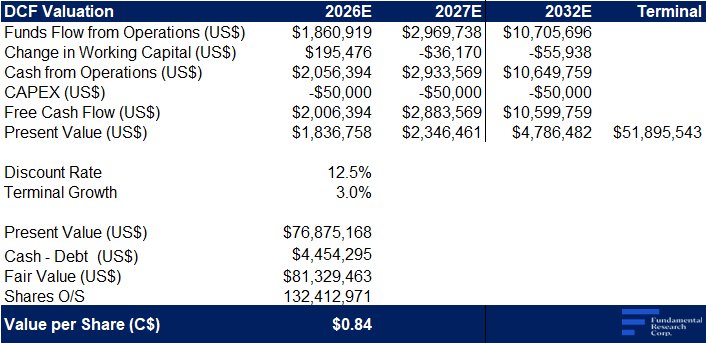

As a result, our DCF valuation declined from $0.90 to $0.84/share

Digital AdTech Companies

Source: S&P Capital IQ / FRC

KDOZ is trading at 1.20x forward EV/Revenue (previously 1.46x), but still below the sector average of 2.81x (previously 2.54x), a 58% discount

Our comparables valuation increased from $0.51 to $0.64/share, driven by a higher sector multiple, and a stronger 2026 revenue outlook

We are reiterating our BUY rating, and raising our fair value estimate from $0.70 to $0.74/share (the average of our DCF and comparables valuations). KDOZ delivered record revenue growth, and continued strong cash generation, supported by disciplined balance sheet management. While margins came under pressure from a deliberate shift toward higher-volume sales, we view this as a trade-off for scale, and long-term growth, with valuation remaining attractive versus comparables.

Risks

We believe the company is exposed to the following key risks:

- Operates in a highly competitive space

- Unfavorable changes in regulations

- Ability to attract publishers and brands will be key to long-term growth

- FOREX

- Reliance on digital ad spending trends Changes in U.S. or global tariff policies that could affect client budgets

- Data privacy or security breaches could impact advertiser trust and platform reputation

Maintaining our risk rating of 4 (Speculative)

APPENDIX