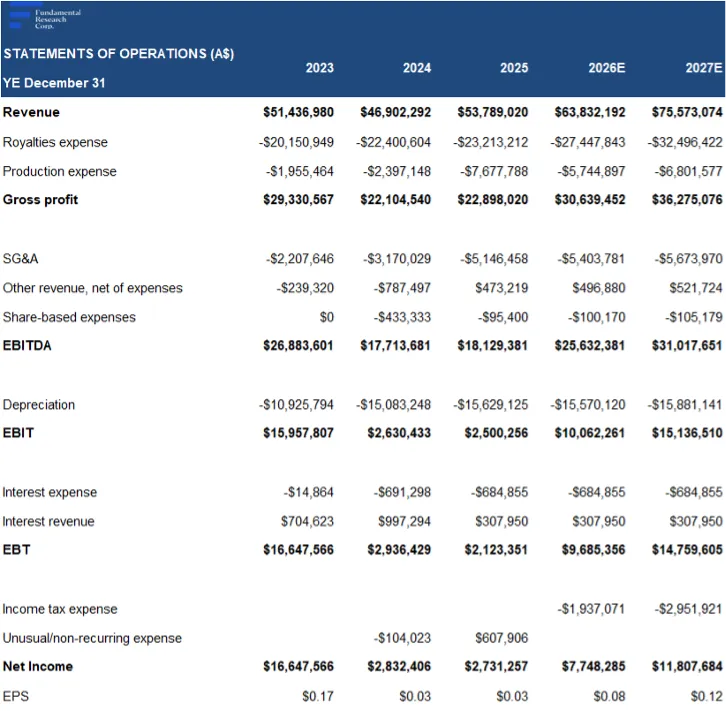

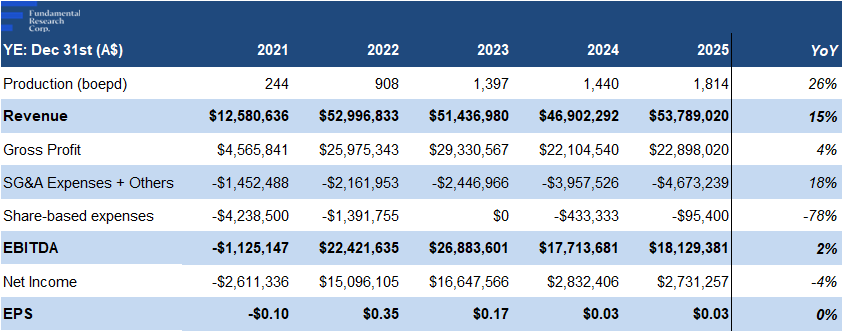

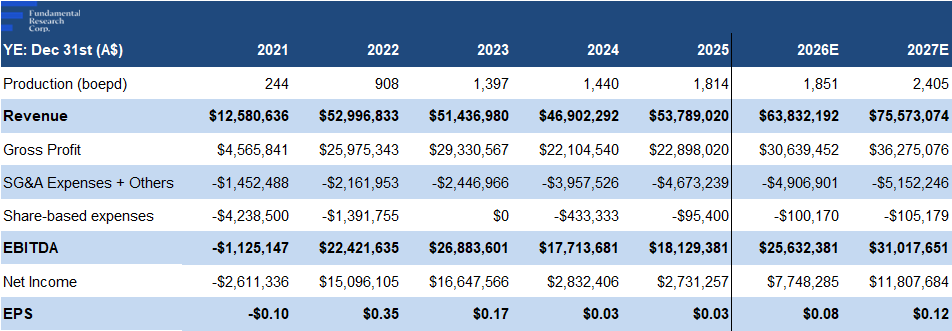

- Strong Growth & Execution: BRK’s production has grown from 244 barrel of oil equivalent per day/boepd (2021), to ~1,700 boepd from nine wells. From 2021 to 2025, revenue increased from $13M to $54M, and EPS improved from ($0.10) to $0.03. Free cash flow turned positive in 2025. Notably, all nine wells were successfully drilled, and completed on the first attempt, underscoring strong technical execution. A key advantage is its low production cost structure of $5–$10/boe (spot: $94/bbl), supporting resilient profitability, even if oil prices normalize from recent geopolitically driven highs, as Middle East tensions ease.

- Large Undeveloped Resource Base: BRK has produced 3.5 million barrels of oil equivalent (mmboe) since 2021, while retaining 12.52 mmboe of remaining reserves, supporting 19 future drilling locations. We estimate cash from operations will comfortably fund development of the 19 additional wells, limiting financing risk, and share dilution.

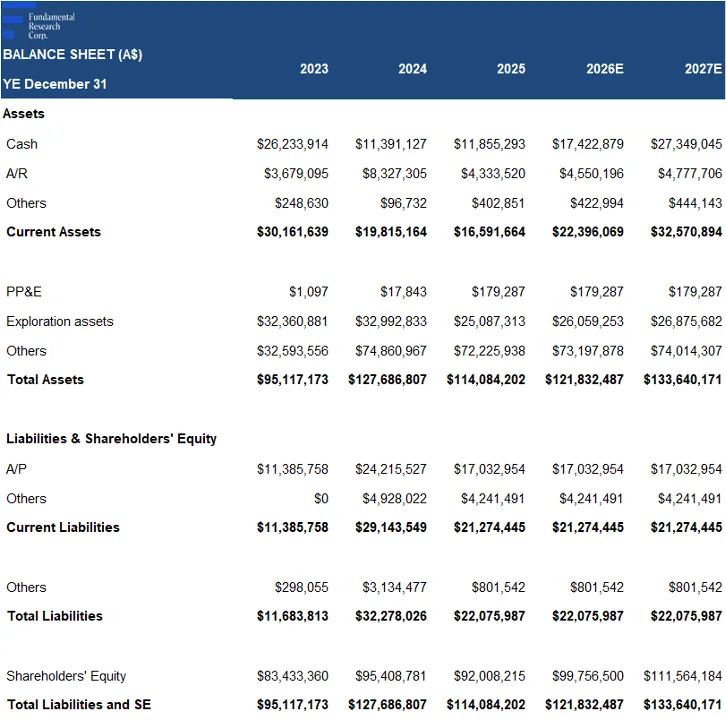

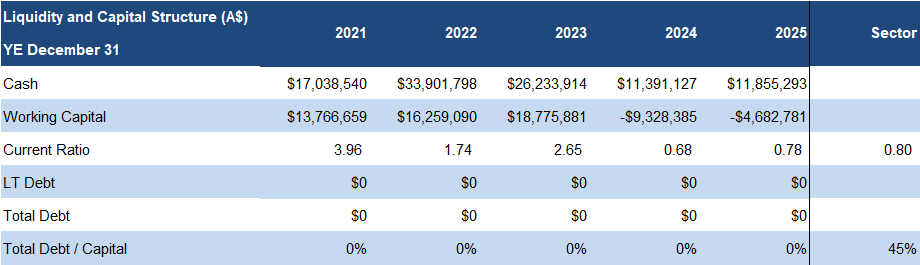

- Strong Financial Position: Debt-free balance sheet supported by a $35M undrawn credit facility, providing financial flexibility for continued development.

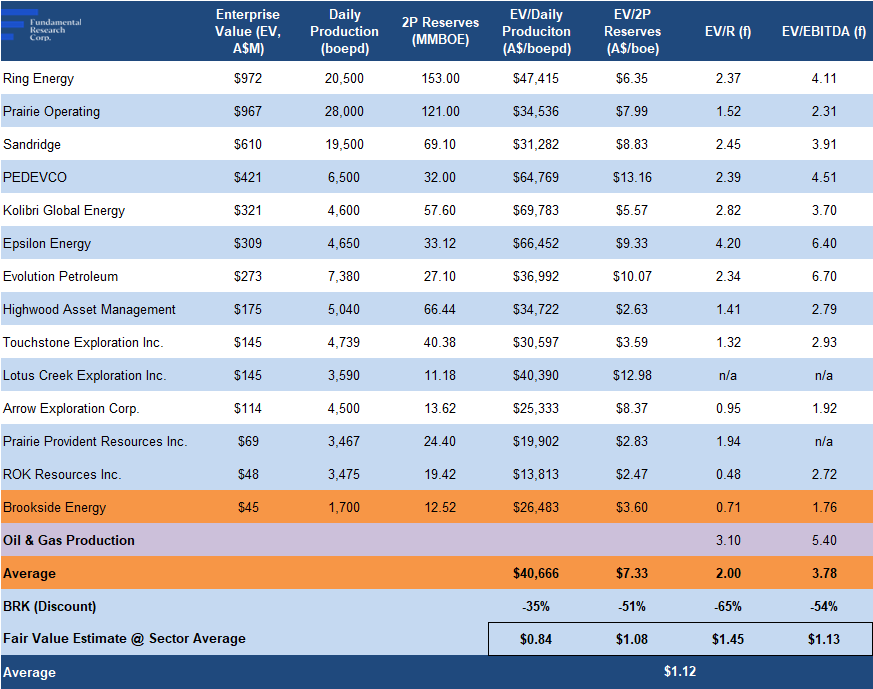

- Valuation Disconnect & Multiple Catalysts: BRK trades ~51% below comparables across key metrics - EV/Forward Revenue 0.71x vs 2.00x, EV/Forward EBITDA 1.76x vs 3.78x, EV/daily production $26k vs $41k, EV/2P reserves $3.60x vs $7.33x.

- Multiple Near-Term Catalysts: We anticipate record revenue this year, driven by higher production, and oil prices. Key catalysts include an ongoing two-well drilling program, and continued land expansion through leasing. The company is also executing a share buyback program, signaling management’s view of undervaluation, and an NYSE American ADR listing (targeted for H1-2026), which we believe should broaden the investor base, and improve liquidity.

Key Risks

- Highly dependent on oil prices

- Oil prices are volatile, and driven by macro and geopolitical factors

- Exploration and drilling success is uncertain

- High upfront drilling and completion costs

Price and Volume (1-year)

| |

YTD |

12M |

| BRK |

23% |

48% |

| ASX |

1% |

10% |

| Sector* |

30% |

46% |

* Brookside Energy has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in A$ except commodity prices, which are in US$.

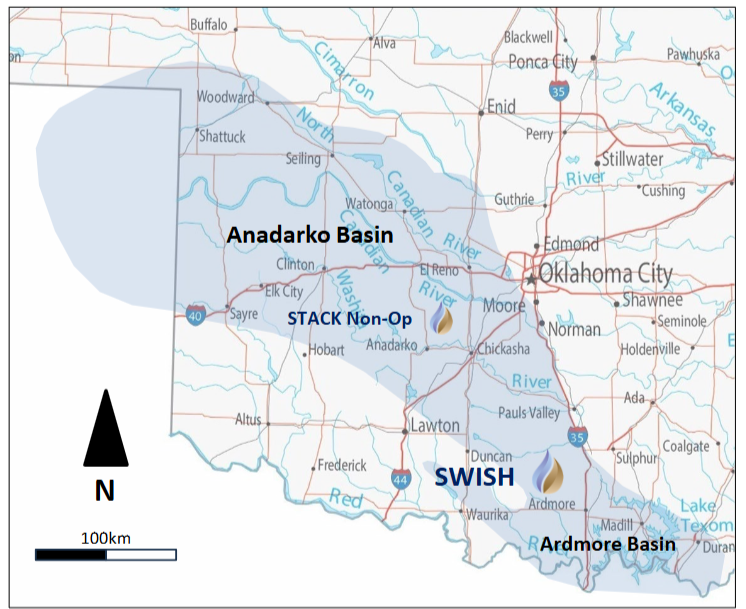

Anadarko Basin (Oklahoma, USA)

BRK operates in the Anadarko Basin, one of North America’s most productive hydrocarbon regions.

Headquartered in Perth, Western Australia, and operating in the U.S. since 2015, with operations in Tulsa, Oklahoma

Anadarko Basin: Location and Extent

Source: Novi Labs

BRK’s portfolio sits within the Anadarko Basin, which covers ~58,000 sq miles (150,200km²), mainly in western Oklahoma, with extensions into Texas, Kansas, and Colorado

Oil exploration in the basin began in the early 20th century

The basin has a production history of over 100 years, yielding tens of billions of boe from thousands of wells. To put this in perspective, global oil production is ~ 100 mm boe per day. The basin is actively developed by several major and mid-sized oil and gas companies.

The basin is considered mature, but since around 2010, it has seen renewed activity driven by shale development. Shale reservoirs contain oil trapped in low-permeability rock, meaning the rock does not easily allow fluids to flow, unlike conventional reservoirs where oil flows naturally into wells. Sha l e p roduction involves horizontal drilling, and multi-stage hydraulic fracturing, in stages, to create flow pathways. This modern method, widely adopted since the mid-2000s, contrasts with conventional production, which relies mainly on vertical wells, and natural reservoir pressure.

A mature basin revived by horizontal drilling and fracking

According to various sources, the basin is still estimated to host tens of billions of boe in recoverable resources, supporting multiple decades of remaining drilling potential.

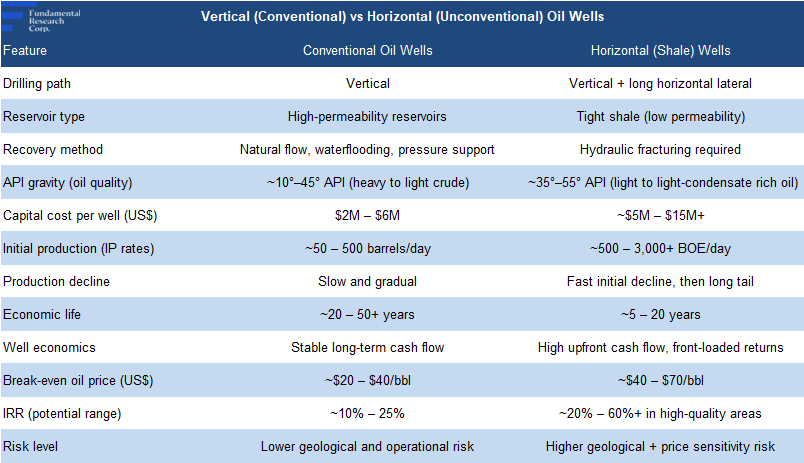

Horizontal vs Conventional Drilling

Source: Rigzone

Horizontal drilling + fracking has transformed oil production by boosting output, improving recovery, and unlocking shale resources previously uneconomic

The U.S. is the world’s largest oil producer at 13.5 mmboe/day, or 13% of global output

Shale oil makes up over 60% of U.S. production

Source: FRC

Conventional wells tend to generate lower, but more stable returns, while shale wells require higher upfront costs, but can deliver higher, more variable returns with greater risk

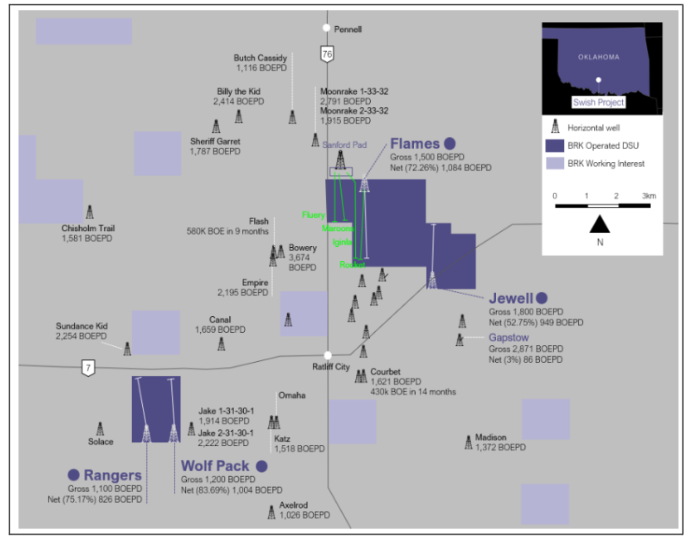

BRK Operating Areas in the Anadarko Basin

Source: Company

Located in a highly active oil and gas region, with established operators such as Continental Resources, and mid-sized players including Mach Resources, Citation Oil & Gas, and Flywheel Energy, which have expanded their positions through multi-billion-dollar acquisitions

BRK holds over 5,000 acres in the SWISH play, a newer, less developed extension of the established STACK (central Oklahoma), and SCOOP (south-central Oklahoma) shale developments.

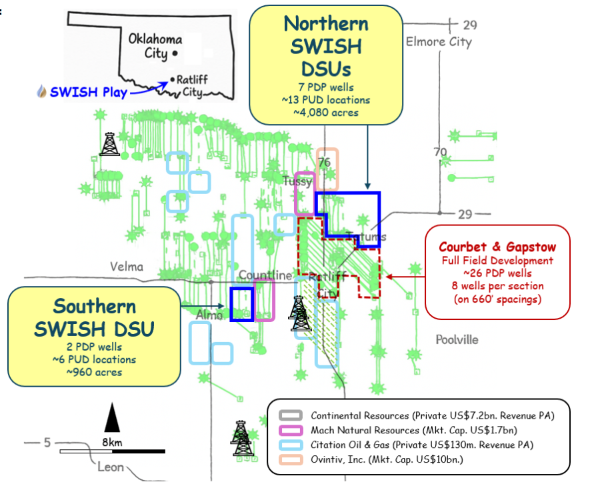

BRK – Key Targets

As it is relatively untapped, the SWISH play offers substantial drilling opportunities, and production potential

Source: Company

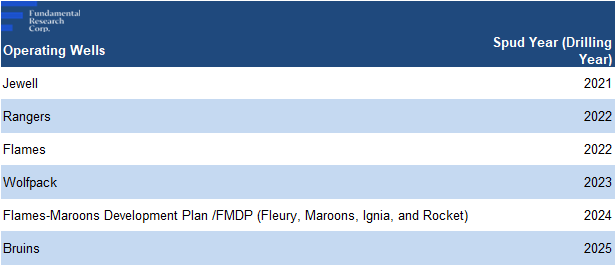

BRK operates nine producing wells (PDP), and 19 proved undeveloped locations (PUDs/planned for future development), across 5,000+ acres

The company’s current production profile includes:

a) Nine operating wells (53–78% working interest/ownership share) in the SWISH play:

BRK has a 100% success rate, with all nine wells successfully drilled on first attempt

Well Locations

Source: Company

These nine wells currently produce 1,700 boepd net for BRK

b) A non-operated working interest (~16% Net Revenue Interest) in eight wells within the SWISH play, operated by Continental Resources; online since early 2025. This revenue stream contributes to only a minor portion of the company’s overall production.

Production increased from 244 boepd in 2021, to 1,700 boepd currently, driven by new producing wells

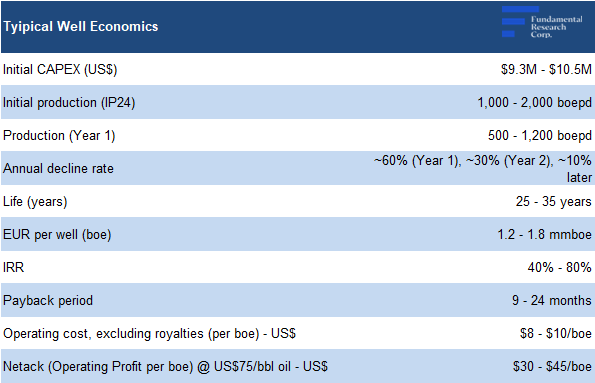

Production Data and Key Metrics

Source: FRC / Company

At ~200 boed on average, each well is anticipated to remain productive for ~20 years

Operating costs are relatively low at $5–$10/boe, versus a sector range of $5–$15/boe, and compared to the current spot price of $94/bbl; however, high upfront drilling costs, and variable success rates, result in volatility in overall returns

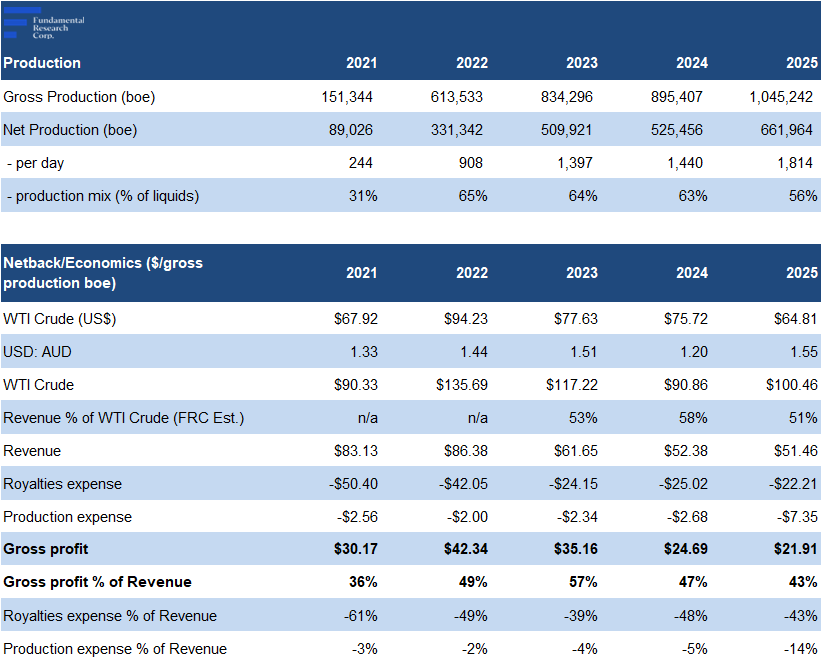

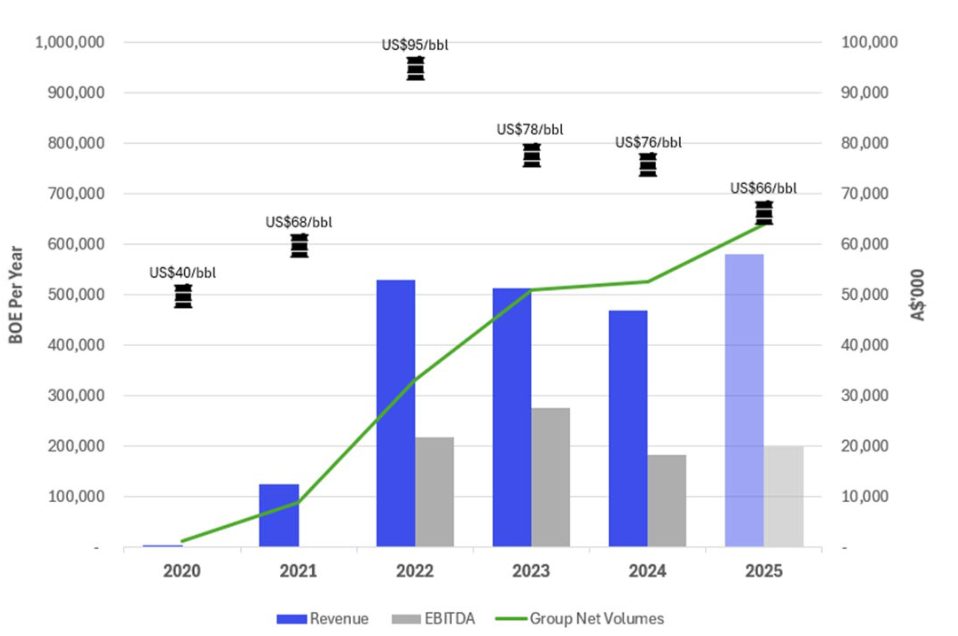

Revenue / EBITDA / Production

Source: Company

Revenue rose from $13M in 2021, to $54M in 2025, while EBITDA improved from ($1M) to $18M

Netback, reflecting operating profit per boe, has tracked oil prices, and averaged $27/boe in the last three years, indicating strong margins

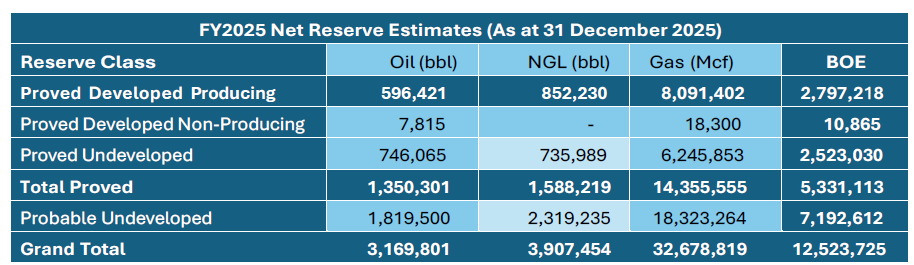

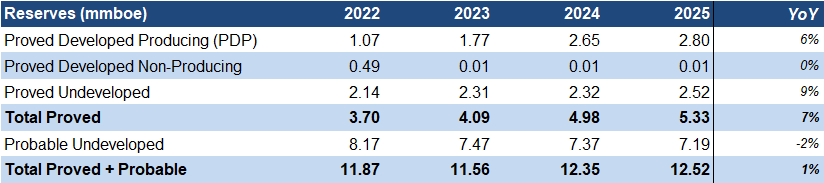

Reserves & Expansion Potential

BRK has produced over 3.5 mmboe since 2021, with 2.8 mmboe remaining in the existing nine wells, and 9.81 mmboe from 19 undeveloped targets, totaling 12.52 mmboe in remaining reserves

Source: Company / FRC

Like most shale developments, BRK operates in stacked pay areas, where multiple hydrocarbon zones can be accessed from a single well pad. This enables higher recovery , and improved capital efficiency, by reducing drilling costs, while increasing output potential.

Future Targets

Source: Company

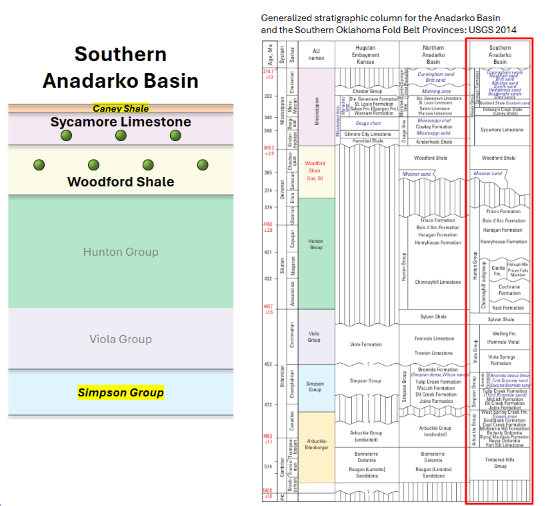

Given the stacked pay potential, we believe there is significant expansion potential beyond current reserves, which are primarily in the Sycamore and Woodford formations (~7,000–10,000 ft deep; ~200–400 ft of productive reservoir thickness; laterals ~13,000–18,000 ft)

Additional upside exists in the overlying Caney Shale (~5,000–7,000 ft deep), and the deeper Simpson group (>9,000–12,000+ ft), which are not included in current reserves

Other operators in the region have had success in the Caney and Simpson formations

Additional reserve and production growth opportunities include the Riverbend AOI (area of interest). Identified in late 2025 within the Anadarko Basin, it covers ~24 sq. miles, and is positioned on trend with prolific wells that have produced >7 mmboe of oil, and 11 bcf of liquids-rich gas. Early technical work by BRK indicates significant oil-in-place potential, and the company is currently leasing prospective areas for future development.

Near-Term Plans & Catalysts

- Optimize performance across existing wells

- BRK is currently pursuing the first two of the remaining 19 potential wells (projected CAPEX of $9M per well, to be funded through cash from operations), which are expected to come online in H2 - 2026.

- Advance the Riverbend AOI through leasing prospective areas

- Evaluate development potential of additional zones ( Simpson Group and Caney Shale ) within the existing land package

Multiple near-term catalysts with potential to drive production and reserve growth

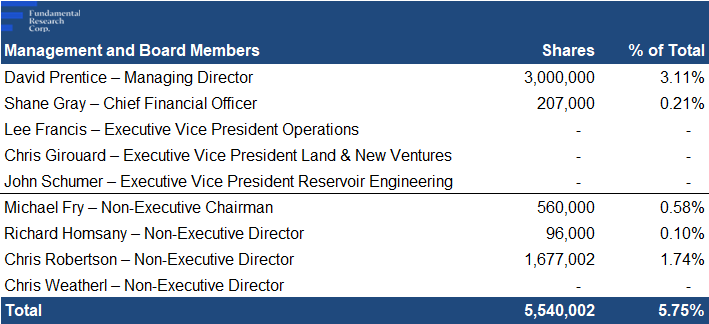

Management and Directors

Source: S&P Capital IQ / FRC

Management and the board own ~6% of BRK’s equity

Four of five directors are independent

Brief biographies of the company’s management team and board members follow:

David Prentice – Managing Director: Senior resources executive with 35 years’ experience in corporate finance and management. Built strong oil and gas expertise in the U.S. Mid-Continent region. Managing Director of BRK and Chairman of Black Mesa Energy.

Shane Gray – Chief Financial Officer: CFO with 15+ years in upstream oil and gas, including private equity-backed El Toro Resources (Wexford Capital). Experienced in M&A and IPO preparation. CPA, University of Oklahoma graduate, and COPAS member.

Lee Francis – Executive Vice President Operations: 40+ years in engineering and operations across upstream and midstream sectors. Former EVP at Red Fork Energy and founder of CEI Petroleum (successfully sold). Professional engineer with a degree from Oklahoma State University.

Chris Girouard – Executive Vice President Land & New Ventures: 40+ years in petroleum land management across the oil and gas industry. Leads acquisitions, contracts, compliance, and new ventures. Founded and exited multiple oil and gas companies; University of Oklahoma graduate.

John Schumer – Executive Vice President Reservoir Engineering: 20+ years in oil and gas exploration and reservoir engineering. Former Team Lead at QEP Resources with experience in development strategy, reserves, and acquisitions. Began career at Schlumberger.

Michael Fry – Non-Executive Chairman: Corporate finance professional with capital markets and treasury expertise. Former member of the Australian Stock Exchange. Non-executive director of Atrum Coal Limited.

Richard Homsany – Non-Executive Director: Corporate lawyer and CPA with leadership roles across multiple listed companies including Toro Energy Limited and Mega Uranium Ltd. Principal of Cardinals Lawyers and former partner at DLA Piper. Also chairs several ASX and TSX-listed resource companies.

Chris Robertson – Non-Executive Director: 34+ years of global investment experience with 20 years in senior portfolio management roles. Significant shareholder in BRK since 2016 with strong strategic insight. Holds advanced business degrees from Macquarie Graduate School and Massey University.

Chris Weatherl – Non-Executive Director: Petroleum engineer with 25+ years of experience across major basins. Held senior roles at Apache Corporation and multiple private equity-backed firms. Most recently COO of Rimrock Resource Operating, driving growth through data-led strategy.

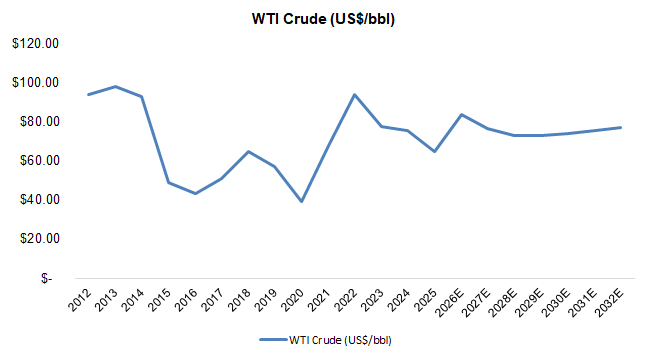

Oil & Gas Price Outlook

Source: FRC / GLJ / Sproule

Consensus near and long-term price forecasts remain well above the 10-year average of $64/bbl, suggesting a supportive pricing backdrop for stronger netbacks, and improved economics

Financials

*Sector: Oil & Gas Production

Production increased from 244 boepd in 2021, to 1,814 boepd in 2025

Revenue rose from $13M in 2021, to $54M in 2025, while EPS improved from ($0.10) to $0.03

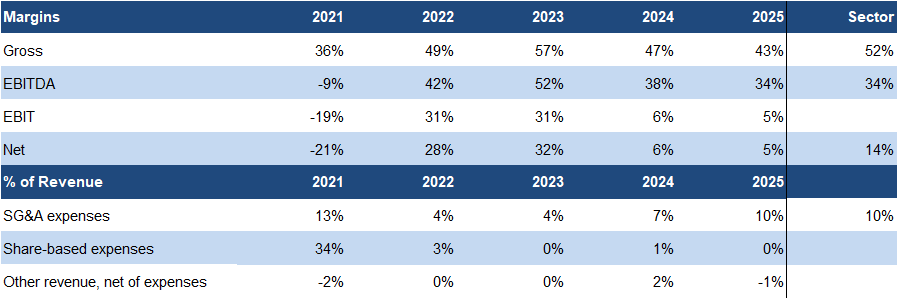

EBITDA margins align with the sector, while net margins are lower due to higher early-life depreciation from steep decline rates in horizontal wells

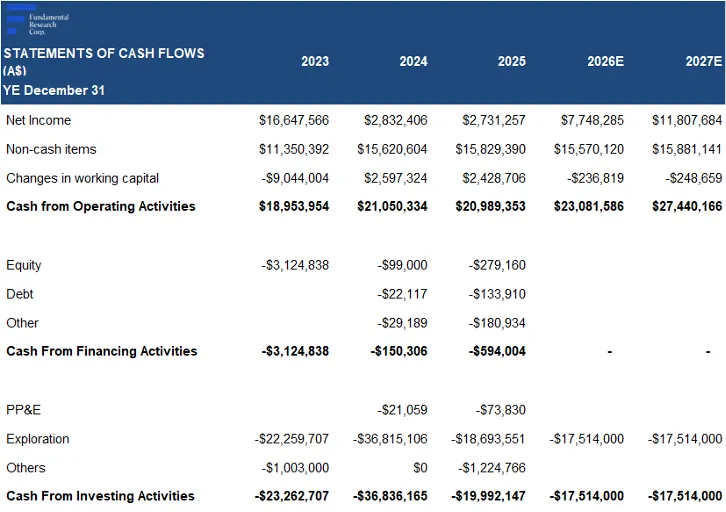

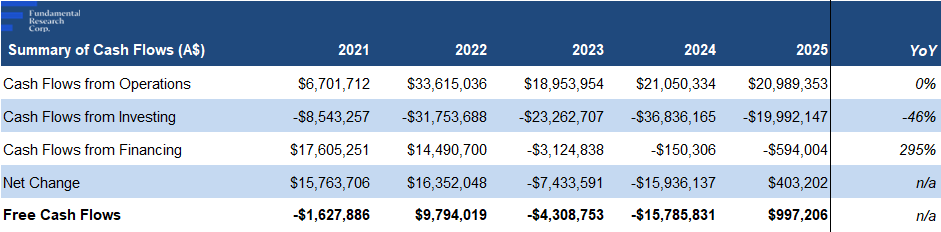

Free cash flows turned positive in 2025

Relatively strong balance sheet with no debt, unlike most producers, with a $35M undrawn credit facility available for future development

Source: FRC / Company

No outstanding options/warrants

BRK vs Junior Oil and Gas Producers

Source: FRC / S&P Capital IQ

BRK trades at an average discount of 51% to comparables across key metrics, including EV/Revenue (0.7x vs 2.0x), EV/EBITDA (1.8x vs 3.8x), EV/boepd ($26k vs $41k), and EV/2P reserves ($3.6 vs $7.3)

Applying sector multiples, we arrive at a comparable valuation of $1.12/share

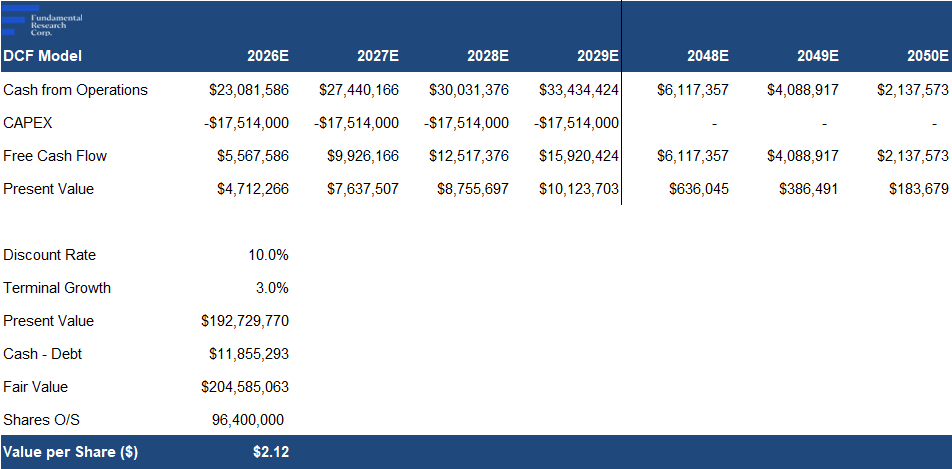

FRC Projections and Valuation

Source: FRC

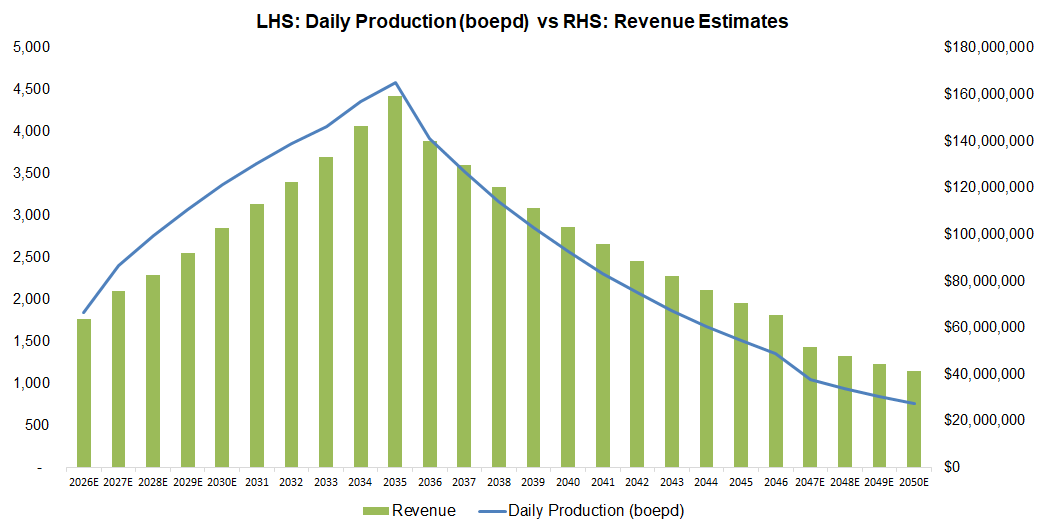

Our DCF valuation on BRK is $2.12/share, based solely on current reserve estimates, including potential cash flows from the nine producing wells, and 19 undeveloped targets

We assume two new wells per year, reaching 28 total wells by 2034

Source: FRC

For conservatism, we assign no value to upside from further development of the Simpson and Caney Shale formations within the existing land position, or from broader regional exploration and development opportunities

We are initiating coverage with a BUY rating, and a fair value estimate of $1.62/share (the average of our DCF and comparables valuations). We believe BRK offers exposure to a high-quality U.S. shale basin, with a robust inventory of undeveloped drilling targets, and regional exploration potential. The company has demonstrated strong execution, rapid production and earnings growth, a low-cost structure, and a debt-free balance sheet, supporting self-funded development . Despite these fundamentals and multiple near-term catalysts, BRK trades at a material discount to peers, presenting an attractive opportunity.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- Production and projections are highly dependent on oil prices

- Oil prices are volatile, and influenced by macroeconomic and geopolitical factors

- Exploration and drilling success is uncertain

- High upfront costs associated with drilling and completing new wells

- Regulatory, environmental, and permitting requirements may affect operations

- Access to financing may be sensitive to commodity price cycles

We are assigning a risk rating of 3 (Average)

APPENDIX