Disclosure: Doubleview Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

*QP: Erik Ostensoe, P.Geo., Consulting Geologist of Doubleview Gold Corp. Doubleview Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

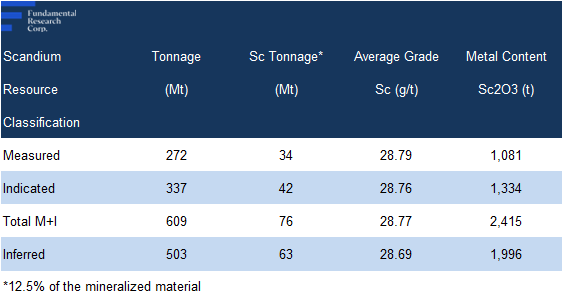

The Hat project, located in B.C.’s Golden Triangle, hosts polymetallic porphyry mineralization containing copper, gold, silver, cobalt, and scandium

Hat Polymetallic Project, B.C. (100% interest)

Project Location

Strategically situated near renowned production and development projects such as Red Chris, Galore Creek, and Schaft Creek

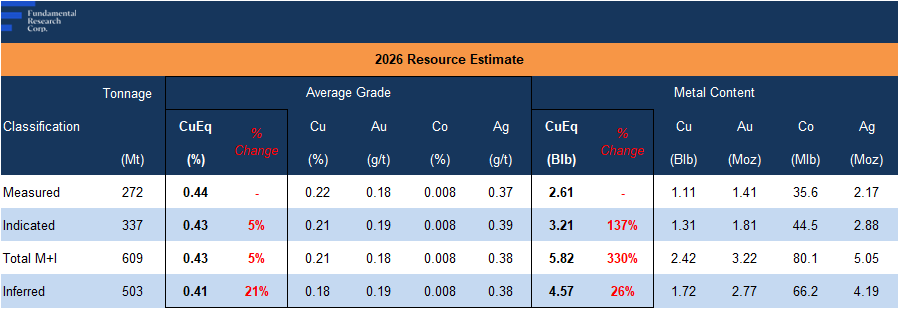

While grades are consistent with similar-style deposits (known as porphyry projects, typically large with relatively low grades), we note that the 10+ Blbs CuEq resource is notable, exceeding the usual range of 2–6 Blbs CuEq, implying potential for a longer mine life, and superior economics

Source: Company / FRC

Source: Company / FRC

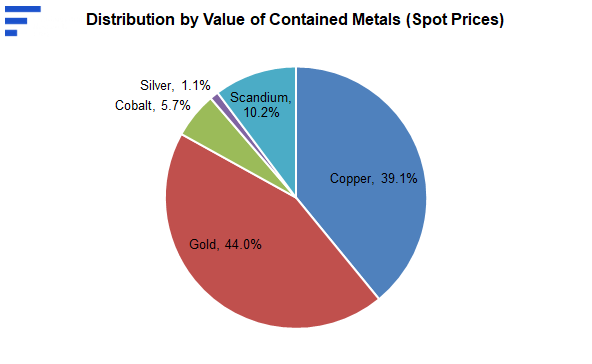

Based on spot prices, we note that gold accounts for 44% of resources, followed by copper (39%), scandium (10%), cobalt (6%), and silver (1%)

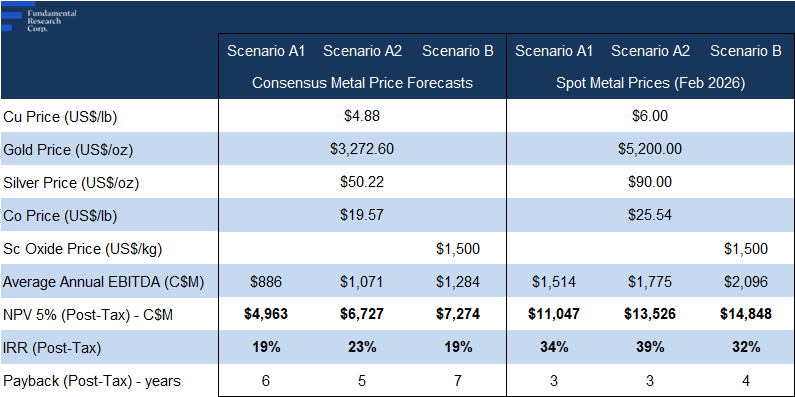

Preliminary Economic Assessment

* A1 used recovery rates from past test results; A2 assumed potential higher recoveries through optimization; and B added a new circuit to potentially recover scandium.

Source: Company / FRC

Large-scale open-pit operation with a 25-year mine life

AT-NPV5% of $7B, with an IRR of 19%, using $4.88/lb copper (spot: $6.09/lb), and $3,273/oz gold (spot: $4,741/oz)

Using $6/lb copper, and $5,200/oz gold, AT-NPV5% rises to $14B, with an IRR of 39%, well above the 15% IRR considered attractive for mining projects

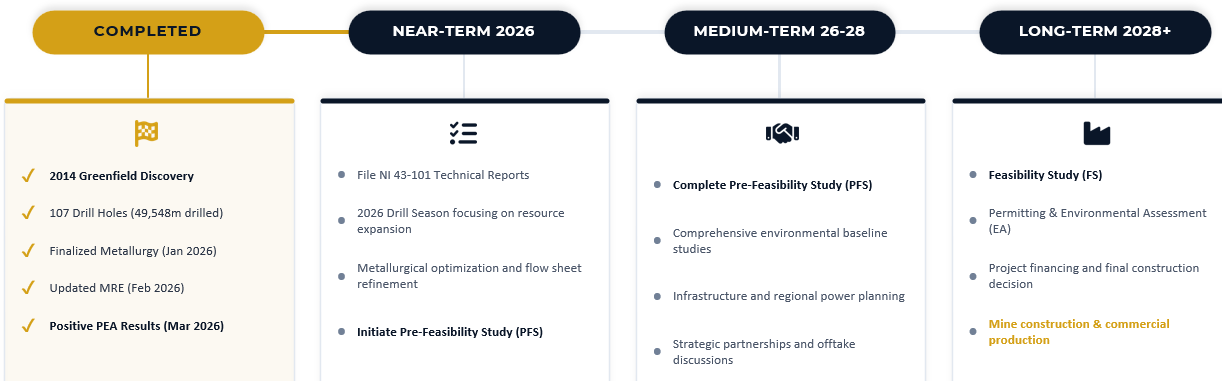

Next Steps

Next steps: resource upgrade and expansion, metallurgical tests, and a PFS, demonstrating management’s proactive approach to further de-risk the project

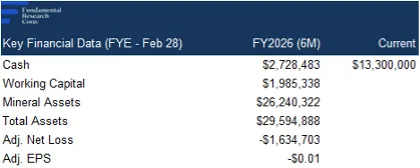

Financials

Source: FRC / Company

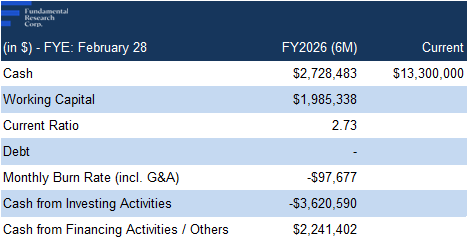

Strong balance sheet, providing funding flexibility for exploration and development without near-term equity dilution

Source: FRC / Company

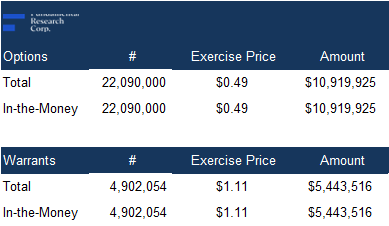

In-the-money options and warrants can bring in $16M

FRC Valuation and Rating

Source: FRC / S&P Capital IQ / Various

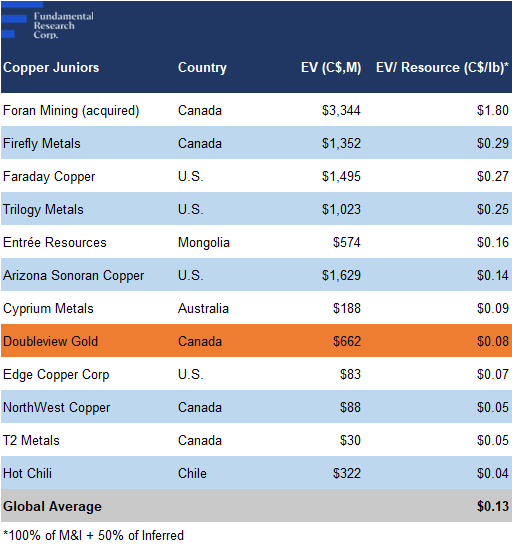

Relative to copper juniors, DBG is trading at $0.08/lb (previously $0.06/lb) vs the comparables average of $0.13/lb (previously $0.10/lb), a 35% discount

Applying the comparables’ average to DBG’s resource, we arrive at a fair value estimate of $4.10/share (previously $3.12/share)

Source: FRC / S&P Capital IQ / Various

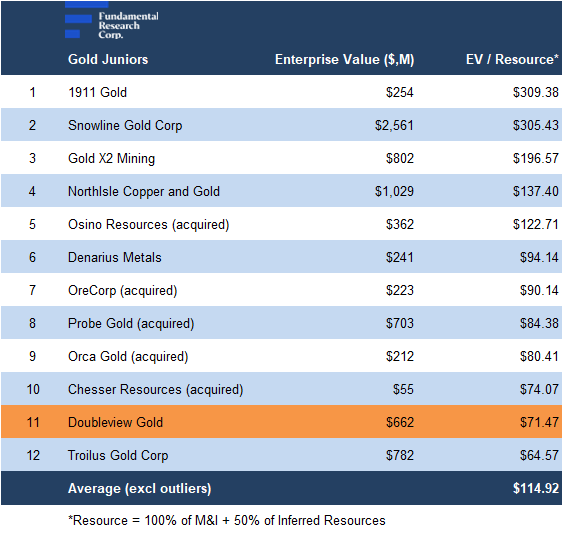

We are refining our gold comps to the $500M–$1B MCAP range, where DBG sits, rather than the prior $100M–$500M set

Relative to gold juniors, DBG is trading at $71/oz (previously $57/oz) vs the comparables average of $115/oz (previously $74/oz), a 38% discount

Applying the comparables’ average to DBG’s resource, we arrive at a fair value estimate of $4.15/share (previously $2.61/share)

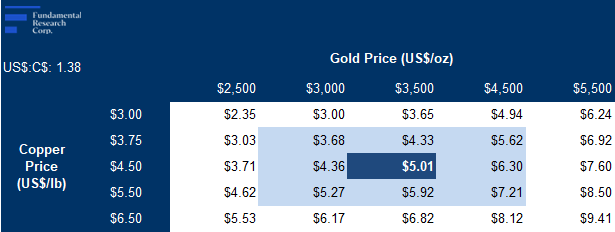

We are raising our long-term copper price forecast from $3.75 to $4.50/lb (spot: $6.09/lb), as the Middle East conflict, and higher oil prices, accelerate the global shift toward electrification, and energy security, for which copper plays an indispensable role

We believe the market will shift from surplus to deficit in 2026

Notably, our updated forecast remains on the lower end of long-term consensus estimates

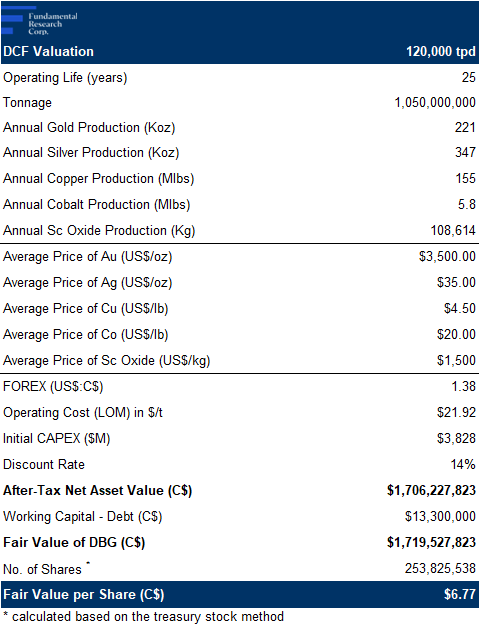

As a result, our revised DCF valuation is $6.77/share (previously $4.56/share)

Source: FRC

The average of our DCF and comparables valuations is $5.01/share (previously $3.43/share)

We are reiterating our BUY rating, and raising our fair value estimate from $3.43 to $5.01/share (the average of our three valuation models). Record copper pricing, and supply constraints, are driving a sector re-rating, with expectations of a shift from surplu s to deficit this year. Now in the $500M–$1B MCAP range, we believe DBG will increasingly be compared to larger companies, boosting visibility and institutional attention, and potentially narrowing the gap between its share price, and our fair value over time.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaininga risk rating of 5 (Highly Speculative)