Disclosure: Zepp Health Corporation has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Zepp Health has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in US$ unless otherwise specified.

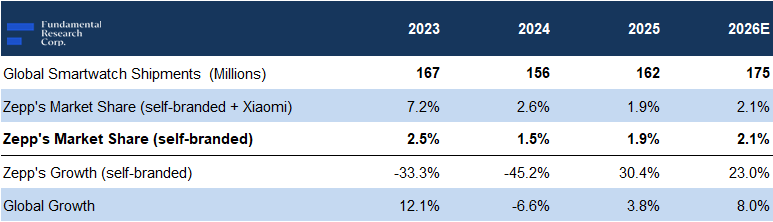

Zepp ranks seventh in global smartwatch sales, behind Apple (NASDAQ: AAPL), Samsung (KOSE: 005930), Garmin (NYSE: GRMN), Fitbit/Google (NASDAQ: GOOGL), Xiaomi (SEHK: 1810), and Huawei. For perspective, Apple ships ~35M units annually; Zepp ships ~3M

Self-branded product shipments jumped 30% in 2025, beating our forecast by 3%, while global smartwatch shipments grew only 4% YoY

Unit Sales & Other Key Metrics

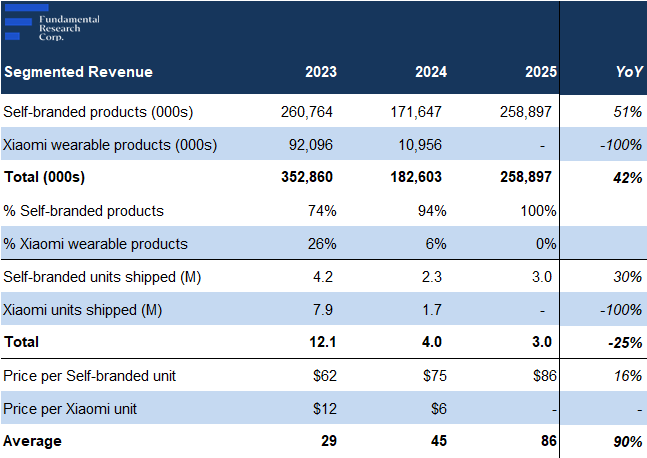

Zepp does not disclose segmented results:

Source: FRC / Company

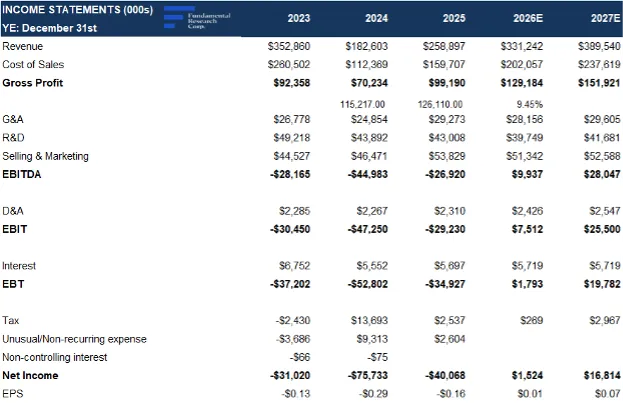

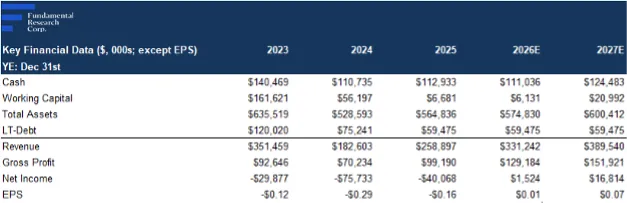

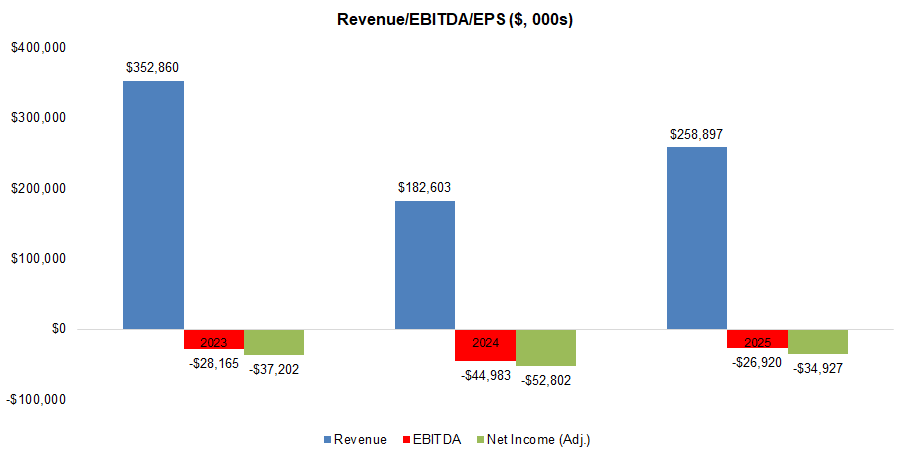

Revenue rose 41% YoY to $259M, exactly in line with our estimate, driven by stronger unit sales, and a 16% YoY increase in selling prices

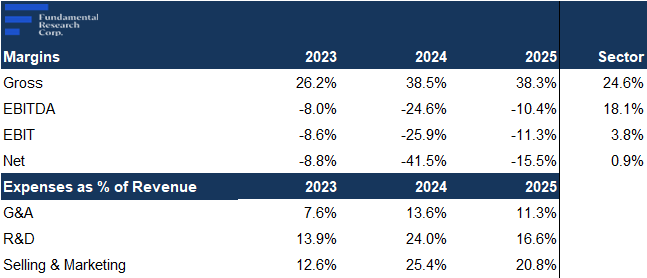

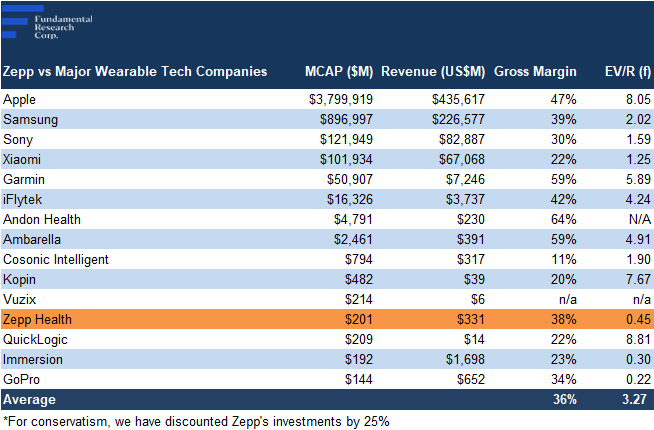

Gross margins remained steady YoY, beating our estimate by 0.6 pp, and beating the industry average for wearable tech (36%), and consumer electronics (25%)

We believe new higher-priced product launches should support margin growth in 2026

Source: Company, FRC

Zepp spent 21% of revenue on sales/marketing, while most majors typically spend 5-10%; a key reason unit sales grew faster than the sector

EPS rose YoY from ($0.29) to ($0.16) on higher revenue, but missed our ($0.11) estimate, due to several one-time operating costs

Operating expenses rose 9% YoY, 8% above our estimate, primarily due to one-time items including costs related to IP protection, prepaid marketing expenses, and investments in sales and distribution infrastructure. Excluding these, expenses would have been broadly in line with our estimate, and roughly flat YoY.

Source: Company, FRC

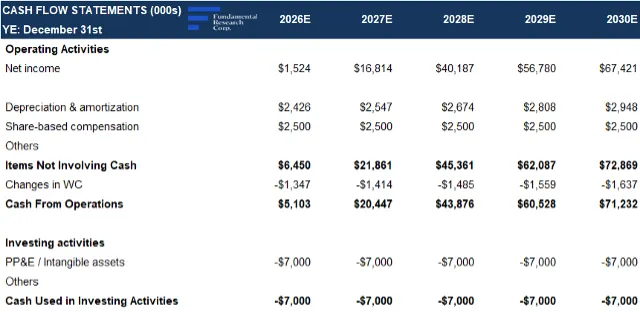

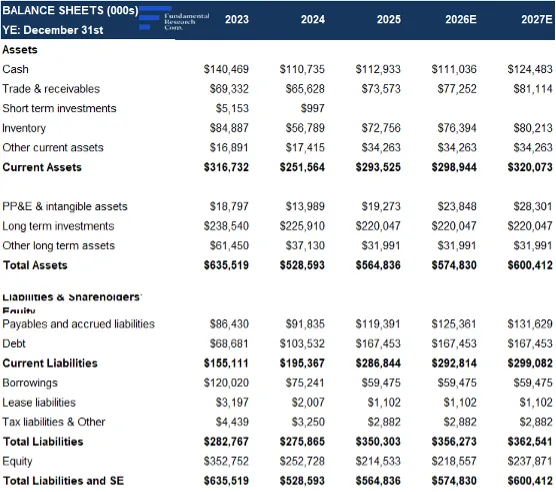

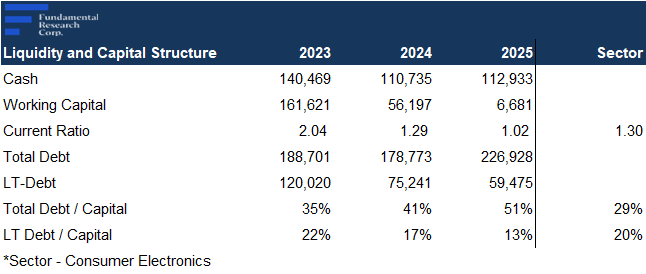

Working capital, and investments, net of long-term debt was $167M, or $12/share

FRC Projections and Valuation

Per consensus forecasts, global smartwatch shipments, which fell 7% in 2024, rebounded 4% in 2025 and are expected to grow 7 –10% in 2026, driven by product upgrades, rising health awareness, AI integration, and broader wearables adoption.

Market Share and Growth

Source: FRC / Various

Zepp products accounted for 1.9% of global smartwatch shipments in 2025, up from 1.5% in 2024

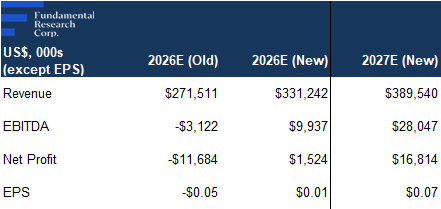

Given the recent product launches and upbeat guidance for Q1, we are raising our revenue and EPS forecasts

We now forecast EPS to turn positive this year, ending a five-year streak of losses, instead of in 2027

Source: FRC

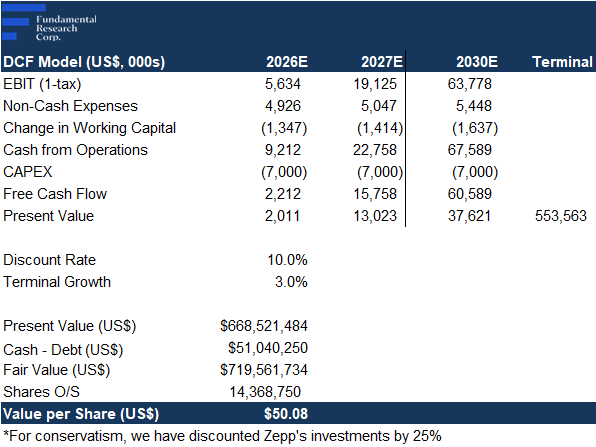

As a result, our DCF valuation increased from $47 to $50/share

Source: FRC/S&P Capital IQ

Sector EV/forward revenue is down 24% since our previous report in November 2025

ZEPP remains undervalued, trading at just 0.45x forward revenue (previously 1.71x), well below the sector average of 3.27x (previously 4.31x)

Applying 3.27x to our 2026 revenue forecast for Zepp, we arrived at a comparables valuation of $62/share (previously $82/share)

We reiterate our BUY rating, and adjust our fair value estimate from $ 64.37 to $56.28/share, based on the average of our DCF and comparables valuations. The valuation decline reflects lower sector valuations, partially offset by our higher DCF valuation. Zepp delivered strong 2025 performance, with unit shipment growth significantly outpacing the broader smartwatch market, supported by new product launches, and increased marketing spend. Although EPS missed our estimate due to one-off costs, underlying fundamentals continue to strengthen, with rising market share and a clearer path to profitability in 2026.

Risks We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining our risk rating of 3 (Average)

APPENDIX