Disclosure: Denarius Metals Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Qualified Person: Scott E. Wilson, CPG, President of RDA, Independent Consultant. Denarius Metals Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures are in US$, except for share price, fair value estimates, and MCAP data.

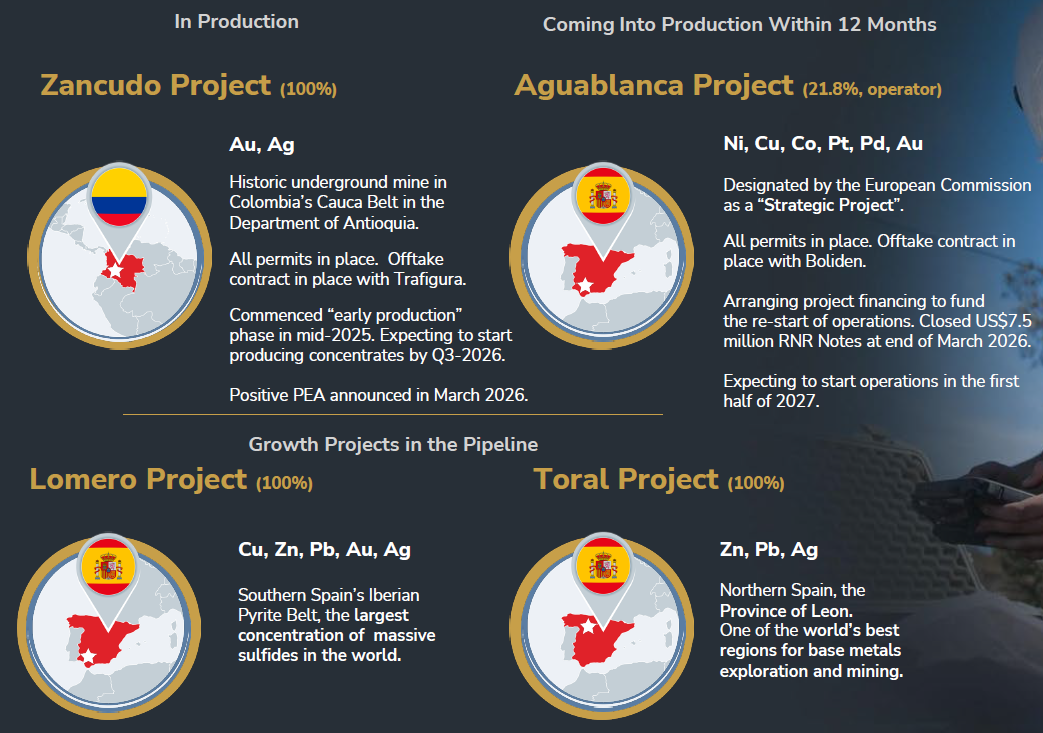

Portfolio of four polymetallic projects, led by Zancudo in early production, with full commercial production expected by Q3-2026, and Aguablanca positioned to begin production in 2027

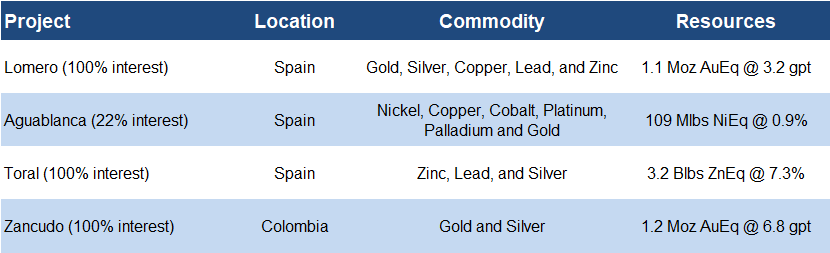

Portfolio Summary

* All equivalent figures were calculated by FRC

Source: Company

Combined resources of 3.44 Moz AuEq (gold equivalent) or 3.21 Blbs CuEq (copper equivalent) across four projects

The following sections provide the latest updates on the two most advanced-stage assets, Zancudo and Aguablanca .

Zancudo Gold-Silver Project, Colombia (100% interest)

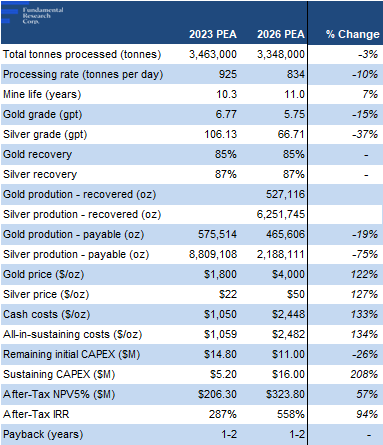

The processing rate and mine life used in the 2026 PEA are largely unchanged from the 2023 PEA

PEA Results (2023 vs 2026)

*Concentrates produced from the processing of mineralized material are sold to Trafigura, a global commodity trading firm, which will pay DMET 86% to 90% of contained gold , and 35% to 45% of contained silver, depending on concentrate grades.

Source: Company / FRC

However, production estimates were lowered due to lower grades, per the latest resource estimate published in late 2025

Annual gold output cut to 40–50 koz, from 50–60 koz

Production value split – gold 94%, silver 6%

The long-term gold price used was 22% higher, but cash costs rose 33% due to lower grades, and higher gold prices

Estimated cash costs of $2,448/oz are high vs peers, but with ~50% of costs, including contractor fees and royalties, tied to gold prices, operating margins (~40%) are expected to remain relatively stable, even if gold prices fluctuate

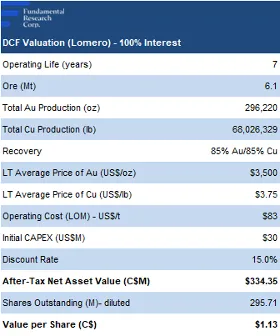

Given all the changes, after-tax NPV increased 57% to $324M

Source: Company / FRC

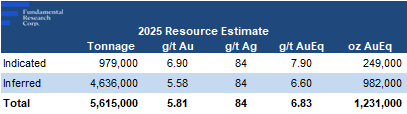

We believe the study was conservative, accounting for just 60% of total resources

The project is in early production, focused on mining and crushing, with processing yet to commence. From June 2025 to December 2025, the company delivered 2,092 tonnes of ore, containing 532 oz of gold, and 15 Koz of silver, generating $1.66M in revenue, and $0.55M in gross profit. DME expects to start producing concentrates, and reach full production by Q3 2026, once its approved 1,000 tpd processing plant is fully built, and operational.

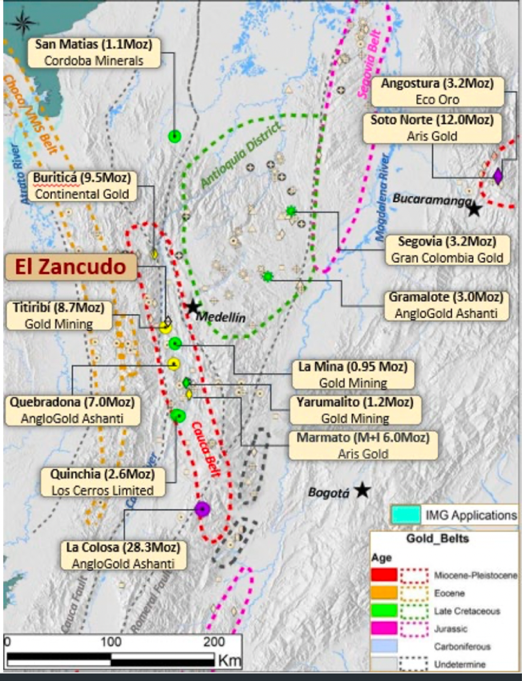

Project Location

Source: Company

30 km southwest of Medellin

The project hosts a high-grade gold-silver system (3.5 km strike length x 0.4 km depth), and the historic Independencia gold mine

Excellent infrastructure, including underground mine access, connection to the national power grid, and water supply

Proposed Processing Plant

Plant commissioning targeted for Q3-2026

We estimate $39M in revenue for 2026, given DMET’s production guidance of 10 koz gold, and 40 koz silver

We estimate stabilized annual revenue of $160M, based on 45 koz gold at $3,500/oz, and 200 koz silver at $35/oz by 2028

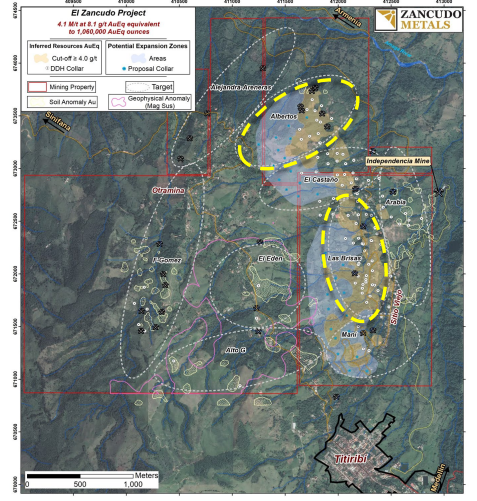

Key Targets

Source: Company

The deposit remains open in all directions, meaning there is potential for further expansion

Commencing a 15,000 m drill program this month

Key Targets

Source: Company

Drilling will focus on Brisas, and El Castaño, to potentially upgrade inferred resources (lower-confidence category), extend gold veins at Independencia, and explore Manto Antiguo and Mani

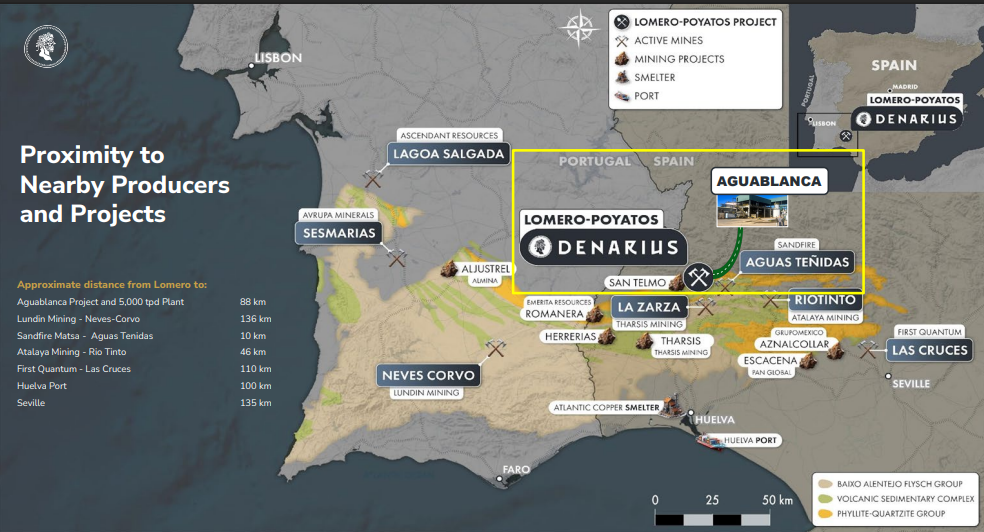

Aguablanca Polymetallic Project (22% interest, operator), Spain

The Aguablanca project, which operated as an open-pit nickel-copper mine from 2005 to 2015, is planned to restart as an underground mine. It benefits from an existing 5,000 tpd processing plant, located 88 km from the company's Lomero project, with the capacity to process material from future Lomero operations.

Project Location

Source: Company

The joint venture that owns the project has so far raised $7M of $30.5M in debt financing needed to restart production by H1-2027

Recognized as a “Strategic project” by the European Commission

This project hosts the only known nickel-copper deposit in Spain

Processing Plant

Fully permitted to re-start operations

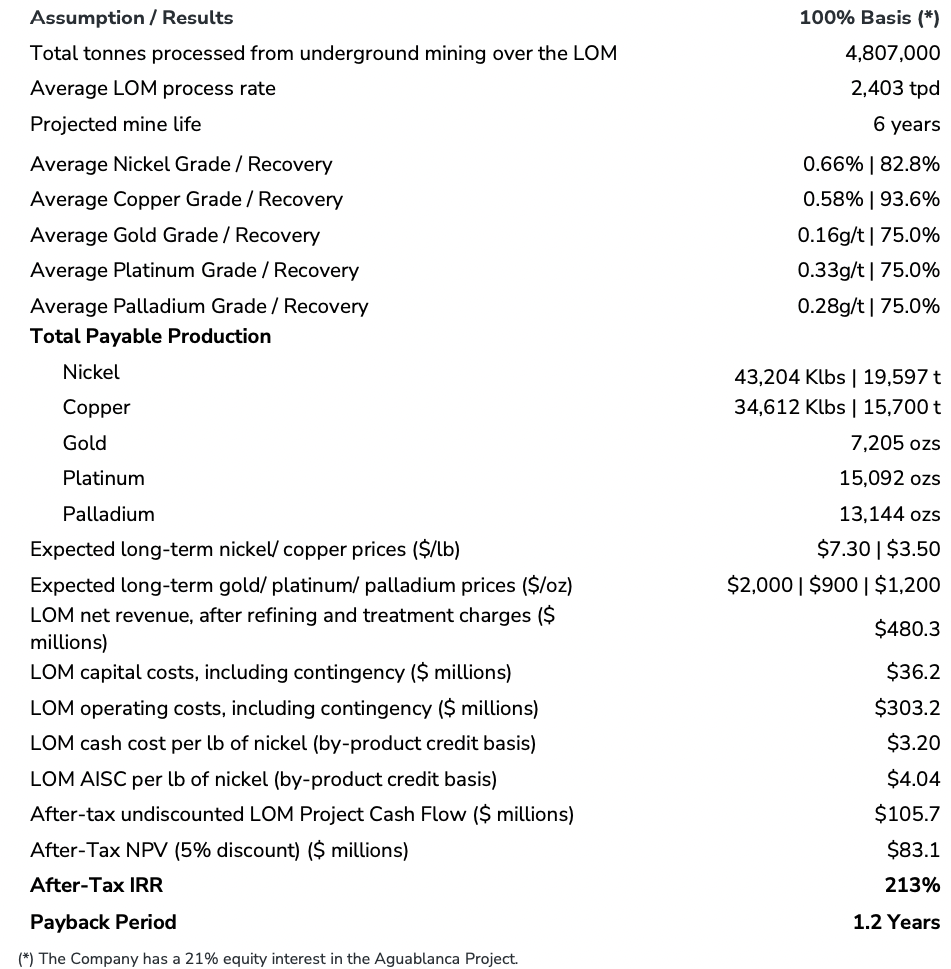

The well-maintained 5,000 tpd processing plant allows production to restart with a relatively low initial CAPEX of $25M

Pre-Feasibility Study

Source: Company

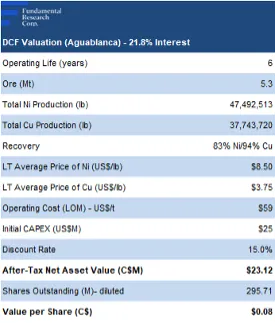

A PFS completed in 2024 assumed the project would use 50% of the processing plant’s capacity, reserving the rest for Lomero

AT-NPV5% of $83M, and a very high AT-IRR of 213%, using $7.30/lb Ni (spot: $7.84/lb), and $3.50/lb Cu (spot: $5.56/lb Cu)

Upcoming Catalysts

Advancing all four projects simultaneously

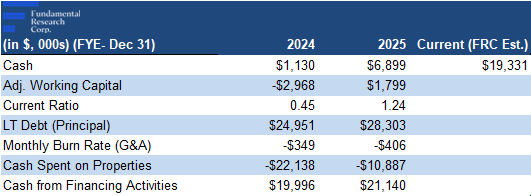

Financials

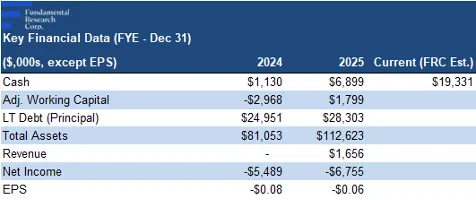

We estimate the company has $19M in cash, with $25M in convertible debentures (principal) outstanding

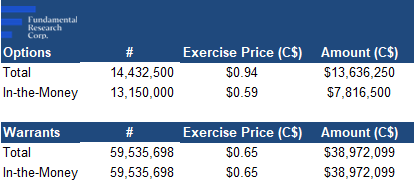

Can raise up to $34M from in-the-money options, and warrants

Source: FRC / Company

We will start presenting our revenue and EPS estimates once commercial production is achieved

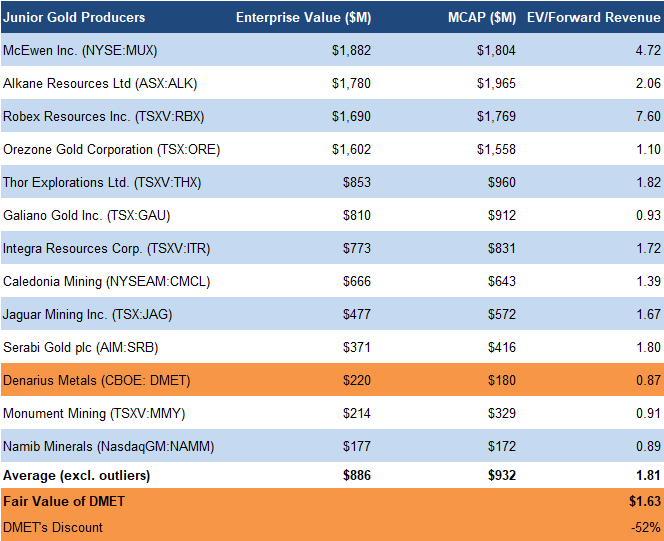

FRC Comparables Valuation

(All figures are in C$, unless otherwise stated)

Source: FRC/S&P Capital IQ/Various

With DMET nearing commercial production, we are beginning to compare it with junior gold producers, instead of exploration and development companies

DMET is trading at 0.87x our stabilized revenue estimate for Zancudo vs the sector average of 1.81x, a 52% discount

Applying the sector average, we arrive at a comparable valuation of $1.63/share vs $1.13/share, when valued as an exploration & development company

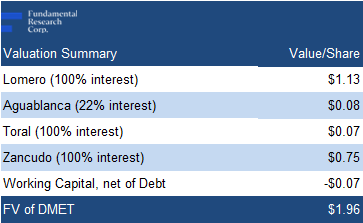

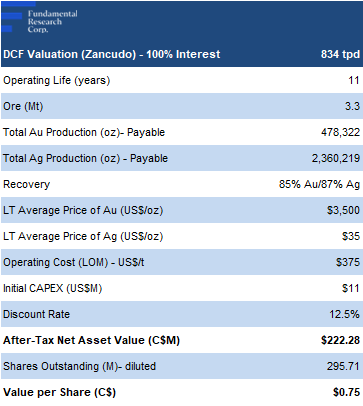

FRC DCF Valuation

Source: FRC

Our DCF (NAV) valuation fell from $2.20/share to $1.96/share, mainly due to share dilution, partly offset by higher metal price forecasts

These tables summarize our valuation on each project

Source: FRC

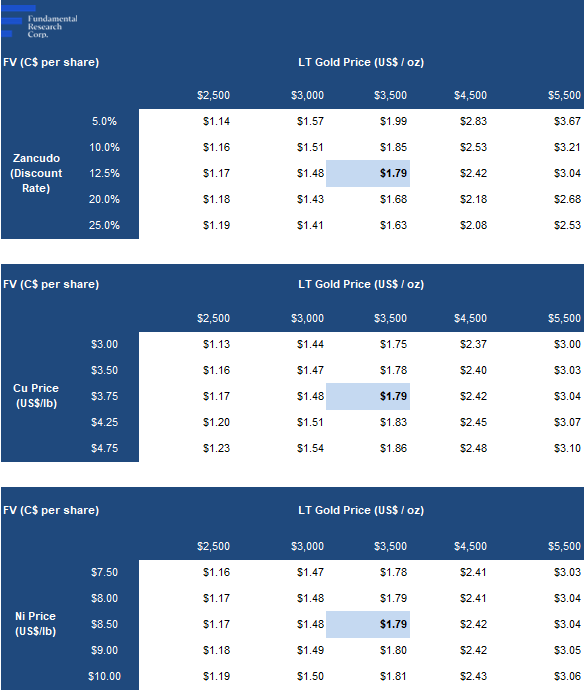

Valuation Sensitivity

Source: FRC

The average of our DCF and comparables valuations is $1.79/share, up from $1.66/share, driven by a higher comparables valuation, partially offset by a lower DCF valuation

Our valuation remains highly sensitive to metal prices

We are reiterating our BUY rating, and raising our fair value estimate from $1.66 to $1.79/share (the average of our DCF and comparables valuations). We believe DMET offers a compelling combination of strong project economics, early production upside, and attractive valuation, trading at a 52% discount to sector peers.

Risks

As the company nears commercial production, we reduce our risk rating from 5 to 4 (Speculative)