Disclosure: Doubleview Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

Price and Volume (1-year)

*QP: Erik Ostensoe, P.Geo., Consulting Geologist of Doubleview Gold Corp. Doubleview Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

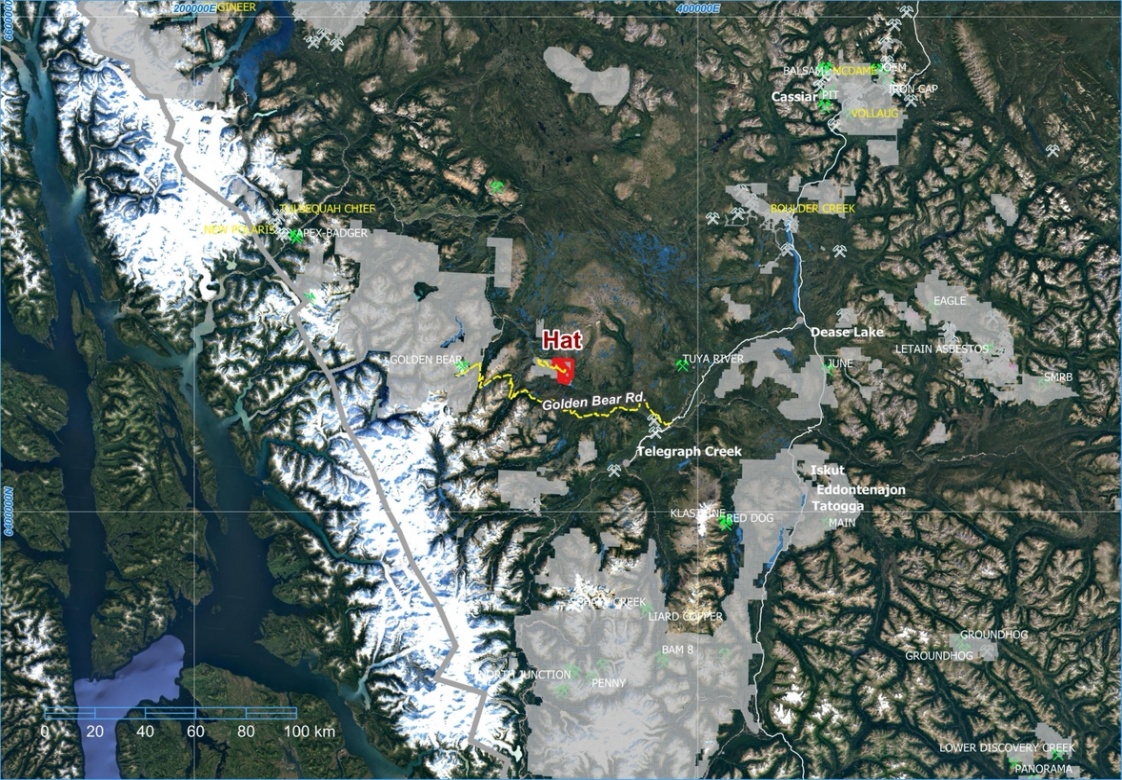

The Hat projected, located in B.C.’s Golden Triangle, one of the world’s most mineralized regions, hosts polymetallic porphyry mineralization containing copper, gold, silver, cobalt, and scandium

Hat Polymetallic Project, B.C. (100% interest)

Project Location

Strategically situated near renowned production and development projects such as Red Chris, Galore Creek, and Schaft Creek

Source: Company

Located in northwestern B.C., 95 km southwest of Dease Lake, and 190 km south of Atlin, the project benefits from access to power, water, and a skilled local workforce

Although the property is remote, future road access may be supported through restoration of a historic access route should the project advance to production. Regional infrastructure prospects strengthened in 2024, when the B.C. government, and the Tahltan Central Government announced a joint $195 M investment to upgrade regional highway infrastructure.

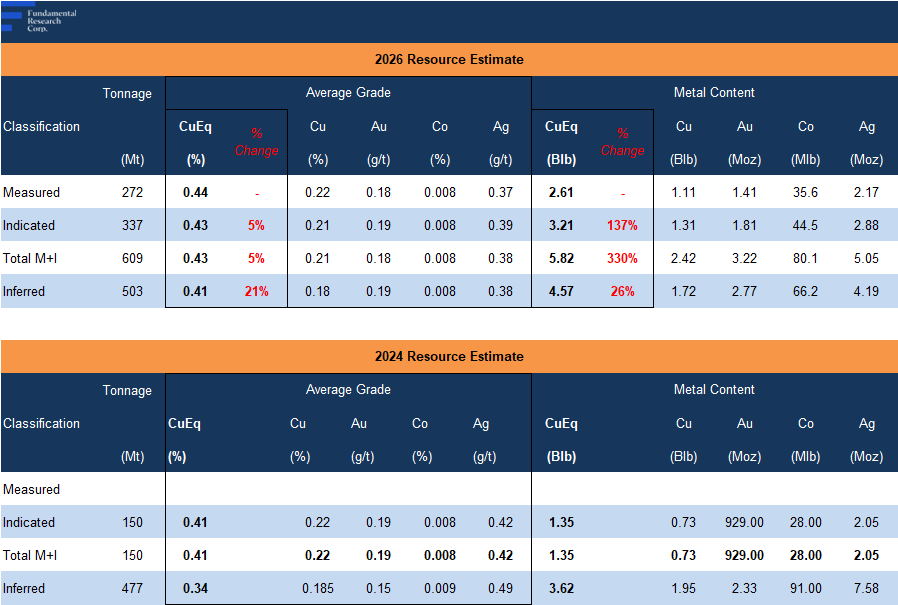

Updated Resource Estimate

The latest resource estimate incorporates drilling completed since the 2024 estimate , and is based on 97 drill holes totaling 49,548 m, up from 71 holes totaling 30,000 m in the prior estimate.

M&I resources (higher-confidence category) increased 330% to 6 Blbs CuEq

Inferred resources up 26% to 5 Blbs CuEq

M&I now accounts for 56% of resources vs 27% previously, reflecting higher confidence

Grade increased 17% to 0.42% CuEq, supporting potential higher production at lower costs

Source: Company / FRC

While grades are consistent with similar-style deposits (known as porphyry projects, typically large with relatively low grades), we note that the resource size is notable, exceeding the usual range of 2–6 Blbs CuEq, implying potential for a longer mine life, and superior economics

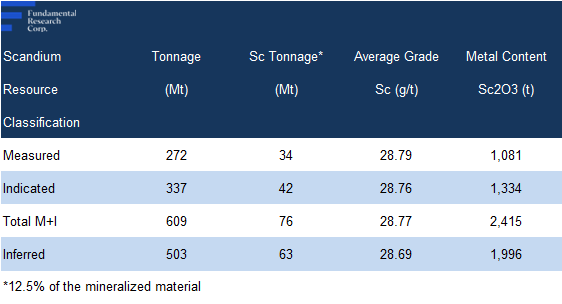

Scandium, a critical mineral, is a rare earth element primarily used in super-alloys, and ceramic fuel cells. The presence of significant scandium is a key advantage, distinguishing HAT from typical porphyry projects . Notably, the U.S. currently imports all of its scandium from countries such as Japan, China, Germany, and the Philippines, underscoring the need for domestic production in North America.

Another major positive is the inclusion of a maiden scandium resource, which we note is a high-tonnage, low-grade deposit, compared with most global scandium projects

Source: Company / FRC

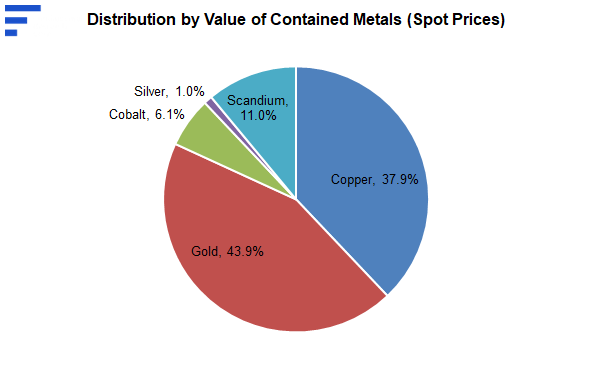

Based on spot prices, we note that gold accounts for 44% of resources, followed by copper (38%), scandium (11%), cobalt (6%), and silver (1%)

Preliminary Economic Assessment

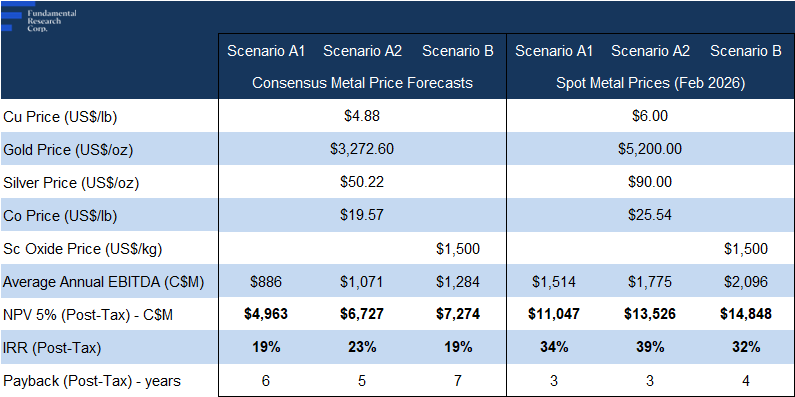

The study evaluated three processing options: A1 used recovery rates from past test results; A2 assumed potential higher recoveries through optimization; and B added a new circuit to potentially recover scandium. While option B showed the best results (higher NPV and IRR), the study showed that the project is attractive even without scandium.

The study returned an AT-NPV5% of $7B, with an IRR of 19%, using consensus metal prices

Source: Company / FRC

Using Feb 2026 spot prices, AT-NPV5% rises to $14B, with an IRR of 39%, well above the 15% IRR considered attractive for mining projects

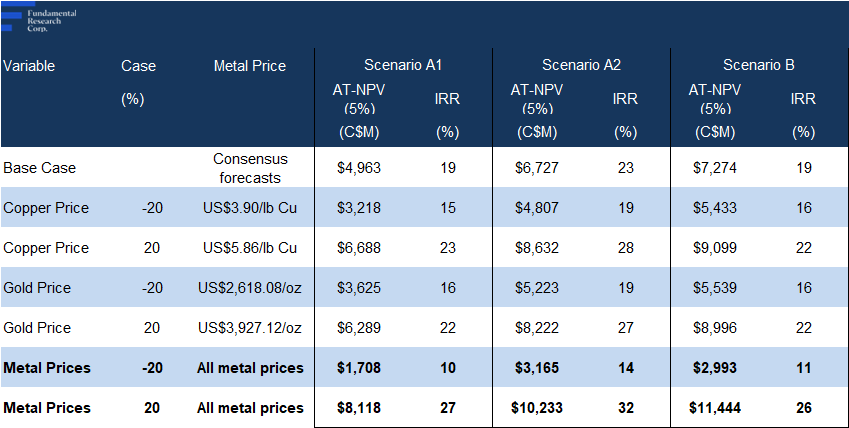

Sensitivity to Metal Prices

NPV varies from $3–$10 B with ±20% changes in metal prices, highlighting the significant impact of metal price assumptions on project value

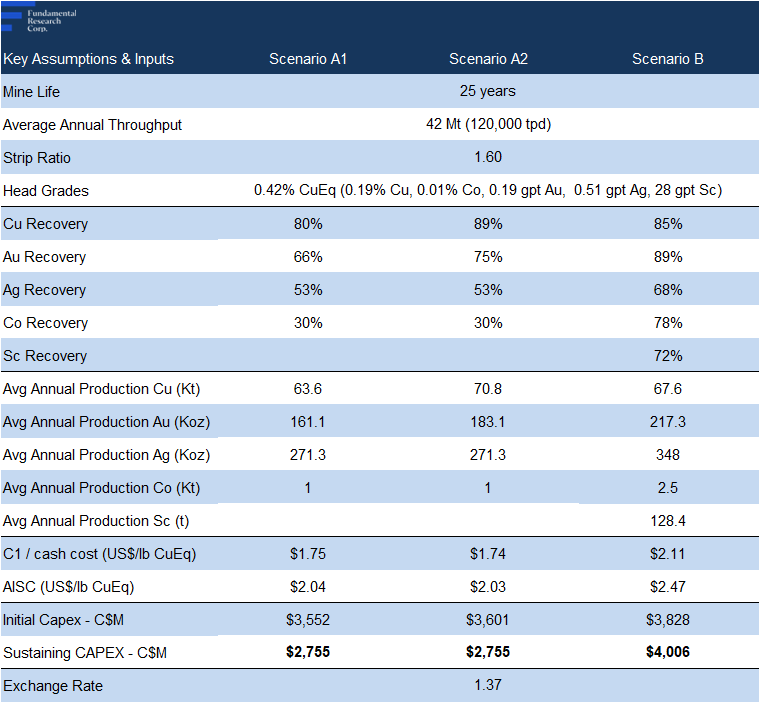

Large-scale open-pit operation with a 25-year mine life

Production is higher in the first 10 years due to focus on higher-grade zones, generating stronger early cash flows, and enhancing project economics

Source: Company / FRC

The operation involves crushing, grinding, and flotation to extract copper, gold, silver, and cobalt, plus hydrometallurgical methods to recover cobalt and scandium, making it a conventional, straightforward process

Initial Capex of $3.6B is high, but typical for large porphyry projects ($2–$10B)

We note that cash costs sit at the low end of the industry range, driven by significant by-product credits

Next Steps

Management Timelines

Source: Company

Next steps: resource upgrade and expansion, metallurgical tests, and project optimization

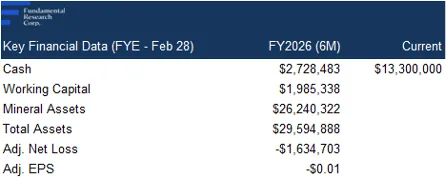

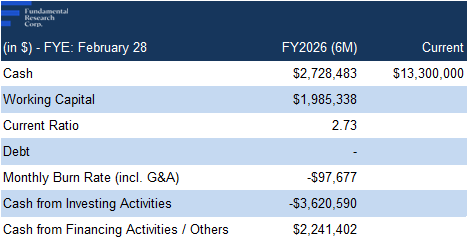

Financials

Strong balance sheet

Subsequent to FY2026 (6M), DBG closed a $7.18M equity financing

The company is currently pursuing a $2M financing, with $0.73M raised to date

Source: FRC / Company

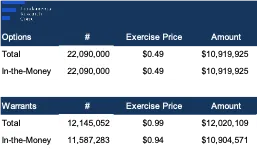

In-the-money options and warrants can bring in $22M

FRC Valuation and Rating

Source: FRC / S&P Capital IQ / Various

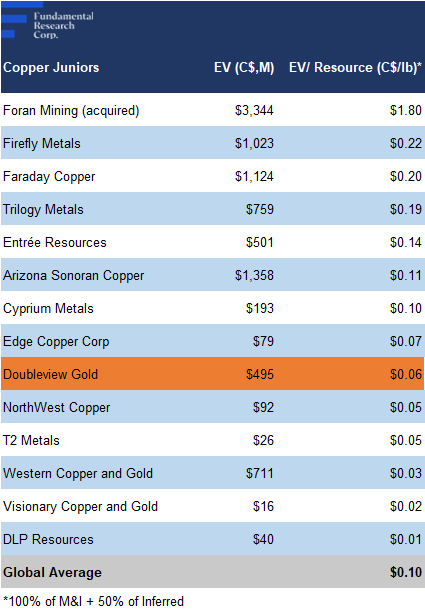

Relative to copper juniors, DBG is trading at $0.06/lb (previously $0.03/lb) vs the comparables average of $0.10/lb (previously $0.05/lb), a 36% discount

Applying the comparables’ average to DBG’s updated resource, we arrive at a fair value estimate of $3.12/share (previously $1.13/share)

Source: FRC / S&P Capital IQ / Various

Relative to gold juniors, DBG is trading at $57/oz (previously $20/oz) vs the comparables average of $74/oz (previously $46/oz), a 23% discount

Applying the comparables’ average to DBG’s updated resource, we arrive at a fair value estimate of $2.61/share (previously $1.64/share)

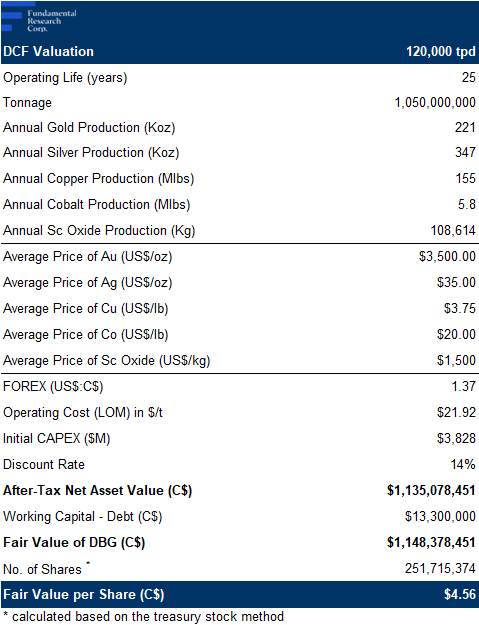

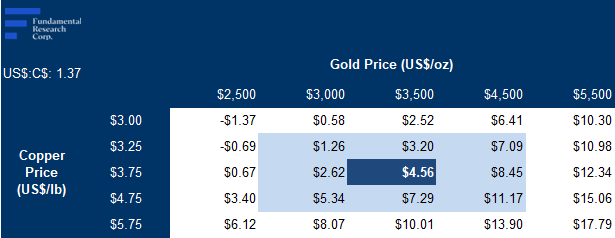

Our DCF valuation, which we are introducing in this report, is $4.56/share

OPEX, CAPEX, and production inputs are similar to the PEA

However, we use our long-term metal price forecasts, which are 11% lower on average than the PEA, and a higher 14% discount rate, which we believe, better reflects the risks of a development-stage project versus the 5% used in the PEA

Source: FRC

We are reiterating our BUY rating, and raising our fair value e stimate from $1.39 to $3.43/share (the average of our three valuation models). DBG’s strong stock performance reflects its significant resource growth, and robust PEA results. The presence of critical minerals like scandium and cobalt, along with low cash costs and high by-product credits, makes the project highly attractive. Trading well below NPV, and backed by a favorable metals outlook, we believe DBG offers significant upside potential.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining a risk rating of 5 (Highly Speculative)

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?