- Project Focus: Althea is focused on delineating a maiden resource estimate on its Mink Narrows copper-polymetallic project in Manitoba, located in the Flin Flon–Snow Lake mining district, a prolific mining area dominated by Hudbay. The project is near several well-known deposits. We were among the first analysts to cover Foran Mining (TSX: FOM) in 2017, when its MCAP was $40M. In February 2026, Eldorado Gold (TSX: ELD) announced plans to acquire Foran for $3.8B, highlighting one of the region’s most notable success stories. Another regional copper junior we covered, Rockcliff Metals, was acquired by Hudbay in 2023.

- Mineralization Potential: Mink Narrows is prospective for multiple mineralization types, including copper-zinc, gold, and nickel-copper. The primary target is the Copper Reef VMS copper-zinc zone, which hosts a non-compliant high-grade historic resource. VMS deposits often occur in clusters (1–20 Mt), and can collectively form major mining districts. We believe there is significant upside potential beyond the historic resource, as mineralization remains open in multiple directions, and several geophysical anomalies are untested.

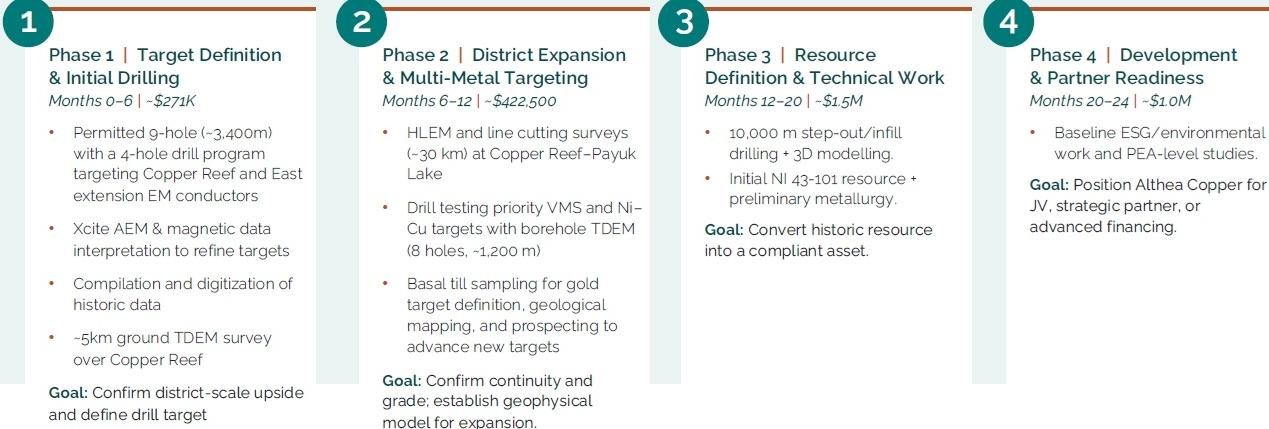

- Upcoming Drill Program: Management is planning a four-hole drill program across high-priority targets (permits in place for up to nine holes), aiming to complete a maiden resource estimate by Q4 2026.

- Copper Market Outlook: Copper prices have retreated from historic highs, but are still up 12% YoY, and remain at unprecedented levels. We maintain a positive outlook, anticipating US$ weakness, slow production growth, and recent supply disruptions. The market is expected to shift from a surplus in 2025, to a deficit in 2026.

- Valuation: At the IPO price of $0.30/share, we estimate Althea’s historic resources are valued at $0.11/lb vs. the sector average of $0.17/lb for high-grade copper juniors, a 34% discount.

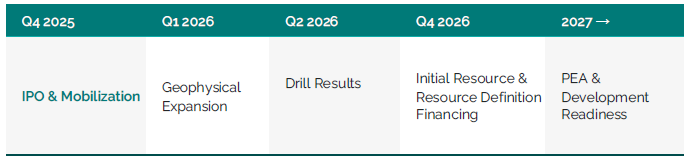

- Catalysts: Upcoming catalysts include closing the IPO, completion of a geophysical survey, and the start of drilling.

* Qualified Person: Ty Magee, M.Sc., P.Geo., Axiom Exploration

* Althea Copper has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

| |

YTD |

12M |

| Althea |

N/A |

N/A |

| CSE |

1% |

39% |

Mink Narrows Polymetallic Project , Manitoba - Option to earn a 100% interest

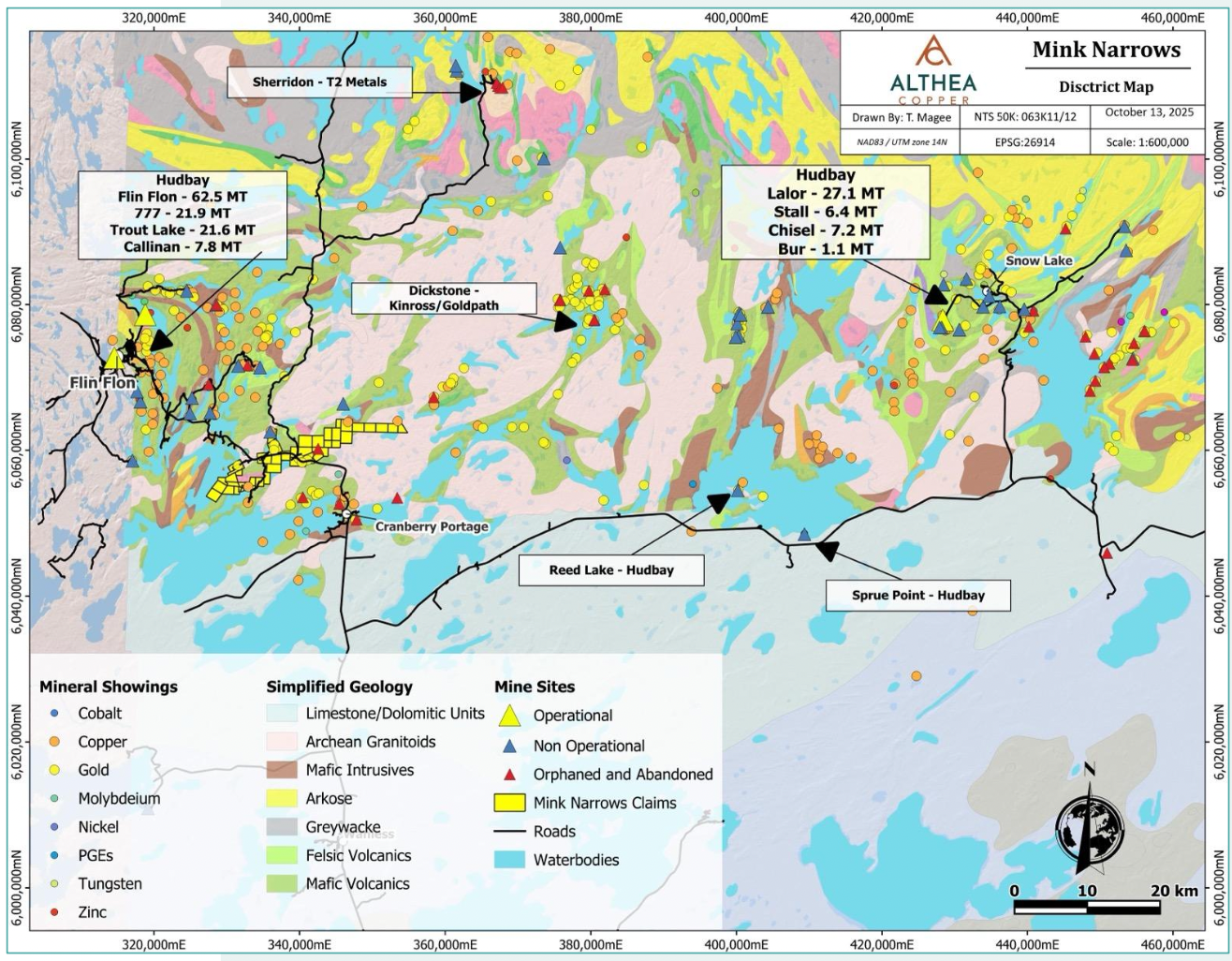

Althea’s flagship 6,984-hectare project is located in the Flin Flon–Snow Lake mining district, a prolific greenstone belt in Canada.

The Flin Flon–Snow Lake mining district, spanning Manitoba and Saskatchewan, is historically a major producer of copper and zinc, with mining dating back to the early 1900s. Beyond base-metals, the district also has significant gold exploration potential. Sources indicate the region has produced over 12 Bls of copper, 14 Blbs of zinc, and 14 Moz of gold from 29 mines .

Project Location Map

Source: Company

District-scale land package

Located 24 km southeast of Flin Flon, Manitoba, near several well-known projects held by majors

~150 Mt mined from 30+ deposits in Flin Flon–Snow Lake, with 100+ deposits identified

Hudbay dominates the region

Excellent infrastructure in place, including access to roads, rail, water, power, and a skilled workforce

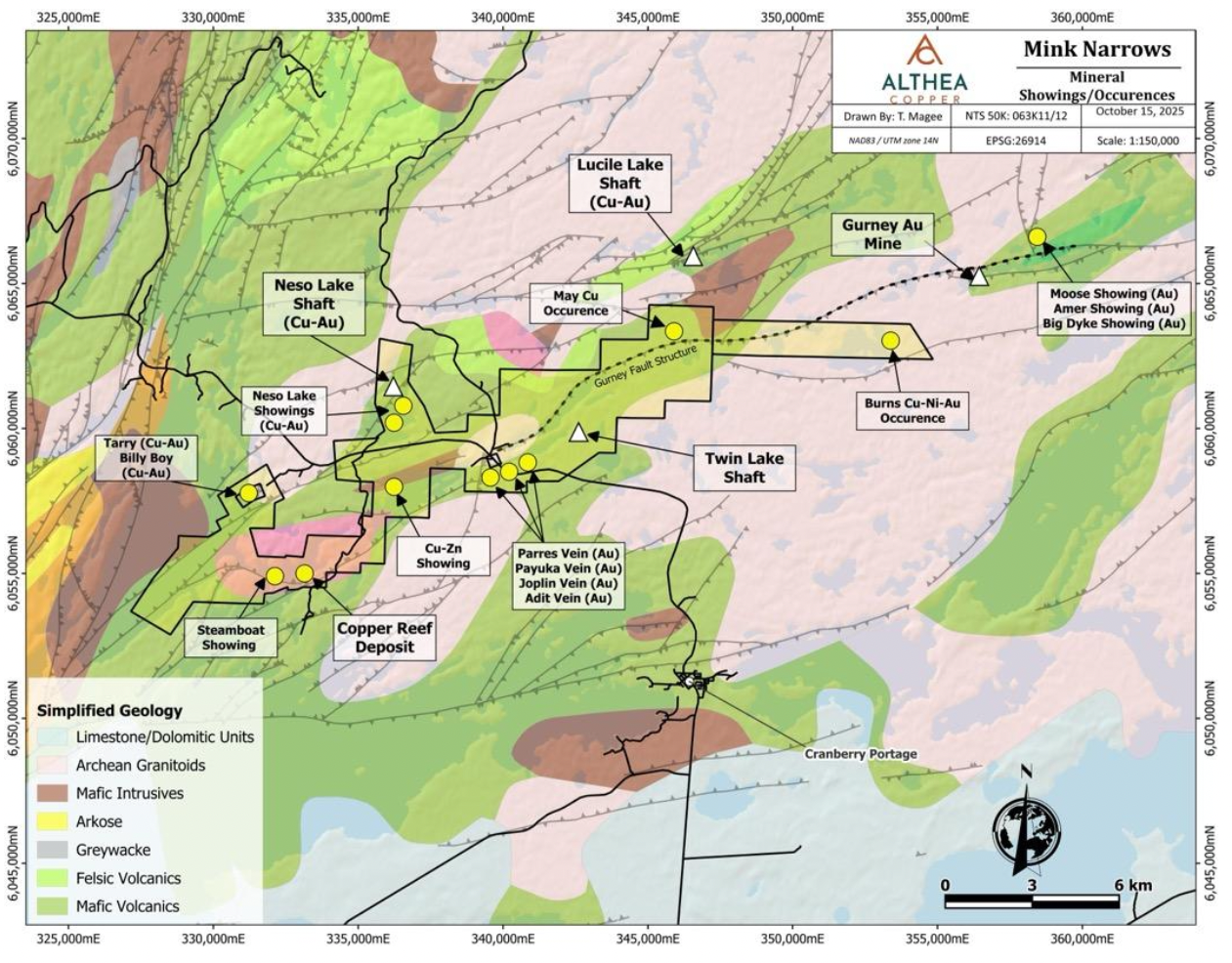

History, Mineralization and Historic Resource

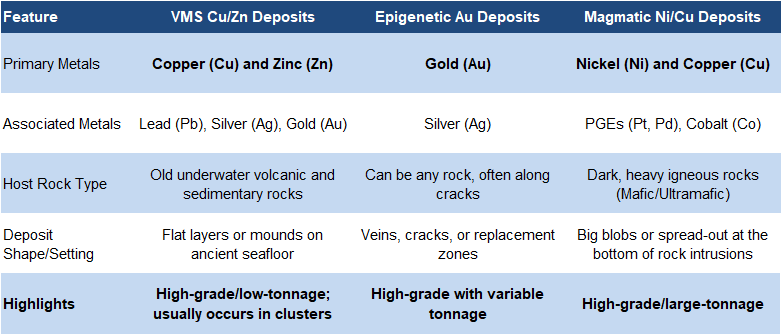

With exploration dating back to the 1920s, Mink Narrows hosts multiple mineralization types : VMS copper-zinc, epigenetic gold, and magmatic nickel-copper.

Deposit Types

Source: FRC / Various

Althea is primarily focused on the Copper Reef VMS target

A brief overview of VMS deposits: Copper sulfides form in the hotter, central parts of VMS systems, while zinc sulfides occur farther out. VMS deposits often occur in clusters (1–20 Mt), and can collectively form major mining districts or camps. Canada hosts three major VMS camps: Flin Flon–Snow Lake (Saskatchewan–Manitoba), Bathurst (New Brunswick ), and Noranda (Quebec). Smaller deposits (<4 Mt) are usually found from surface to ~300 m depths, whereas larger deposits (>10 Mt) commonly extend to depths of 1,000–2,000 m.

VMS deposits often cluster, forming mining camps

Targets

Source:Company

The flagship Copper Reef target accounts for 5-10% of the project area

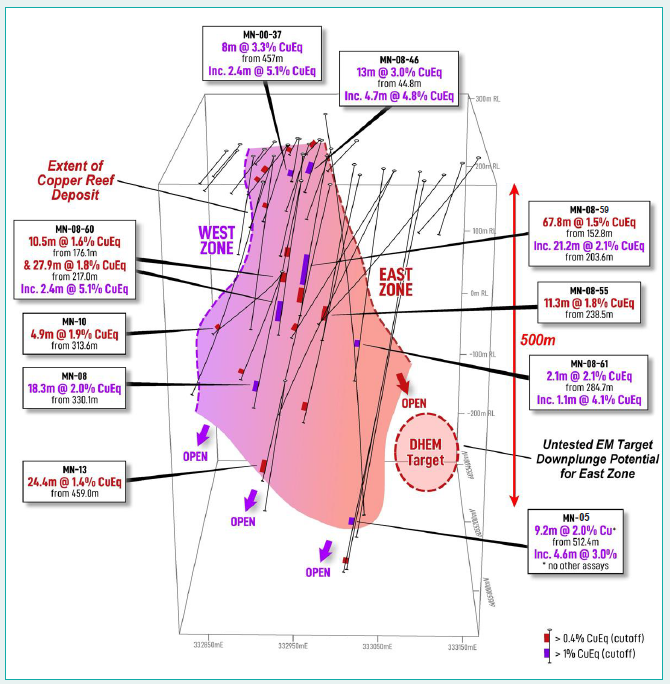

Copper Reef: Historic Resources (1969)

Source: Company

A 1969 study delineated a high-grade, small-tonnage VMS deposit, containing 16.5 Mlbs of copper, and 5.5 Mlbs of zinc (18.5 Mlbs CuEq)

Post-2000 drill programs reported large bulk-tonnage style intercepts, including up to 67.8 m grading 1.5% CuEq, and several high-grade intercepts such as: 4.0 m at 4.95% Cu, 19.7 g/t Ag, 0.32 g/t Au, and 3.1 m at 13.9 g/t Au, 1.7% Cu, 2.0% Zn.

For context, grades of copper mines globally typically range between 0.4% and 1.0%

Copper Reef Resource Upside

Source: Company

The Copper Reef target hosts multiple high-grade VMS-style shoots

Mineralization has been traced to over 500 m in depth, and remains open in several directions

The historic 1969 resource only included copper and zinc. However, later drilling has demonstrated the presence of significant gold and silver, which is typical of VMS deposits. Althea plans to include these metals in future resource estimates. In comparable deposits, gold and silver can contribute around 30% of total metal value, meaning the historic resource of 18.5 Mlbs CuEq could potentially increase to approximately 26 Mlbs CuEq, when these credits are included.

Gold & silver potential

Copper Reef Resource Upside

Source: Company

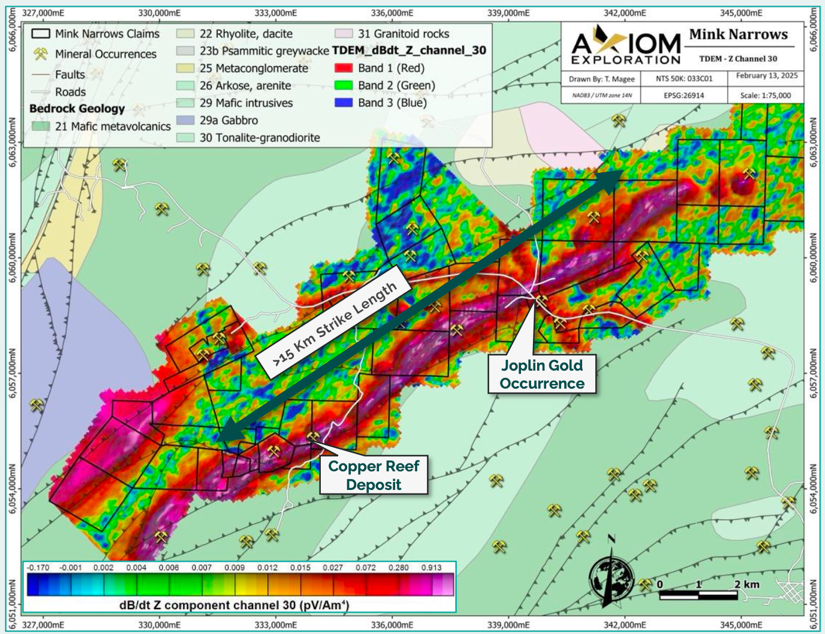

We believe there is significant expansion potential beyond the historic resource, as mineralization is open along multiple directions, and several geophysical anomalies remain untested

Last year, Althea completed a property-wide geophysical survey, delineating a major conductive body over 15 km long and open at depth, along with several new targets.

Geophysical Anomalies

Source: Company

Four drill-ready targets along a >15 km trend

Exploration Strategy

According to the property’s technical report completed earlier this year, approximately 25 drill holes (4,129 m) have been completed since the historical resource estimate, confirming and expanding the non-compliant historical resource.

Copper Reef Exploration Strategy

Source: Company

Total budget over 24 months: $3.20M

Althea is focused on confirming the Copper Reef mineralization, and exploring opportunities to expand the existing mineralized envelope. Upcoming work will include further geophysical surveys, and an initial four-hole drill program (permits in place for up to nine holes) at high-priority targets along the Copper Reef trend.

Management Projected Timelines

Source: Company

Management aims to complete a maiden NI 43-101 compliant resource estimate by Q4-2026

Management and Board

Brief biographies of the management team, as provided by the company, follow:

Lowell Kamin, CEO, Chairman & Founder

- Founded Althea Copper Corp in 2022

- 30+ years of capital markets experience (Scotia Capital, BofA Merrill Lynch)

- Worked with Kinross, Hudbay; supported Kinross–Red Back Mining transaction

Management, Board members, and advisors hold more than 70% of the shares, maintaining a tightly held structure

Randene Seeman, President & Director

- 25+ years in land, regulatory, compliance, and project execution

- Formerly with Shell Canada and other industry leaders

- Deep expertise in government relations, vendor management, cost optimization

Leo Horn, Technical Advisor

- 25+ years global exploration & mining experience in precious, base and critical metals as well as uranium and diamonds

- Led high-grade uranium discoveries in Athabasca Basin

- Also Technical Director at Lodestar Metals (TSX-V) and Cosmos Exploration (ASX) and technical advisor for several other companies

The IPO will broaden the public float

Doug Engdahl, Advisor

- President & CEO of Axiom Exploration

- Professional Geologist with applied geostatistics background

The team brings experience from major companies including Hudbay, Kinross, and Shell

Richard Masson, Advisor

- 20+ years across Manitoba/Saskatchewan

- President & CEO of Boreal Gold

- Formerly with M’Ore Exploration and Voyageur Minerals

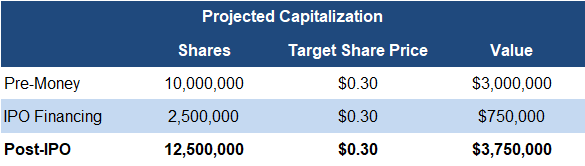

Capital Structure

Source: Company/FRC

Althea intends to raise $0.75M through the IPO, with a subsequent larger raise of $3–$5M later in the year

The IPO is priced at $0.30/unit, with each unit including one common share, and one-half warrant, exercisable at $0.30 for 18 months. We believe the warrant is a valuable bonus, as its exercise price equals the unit price; unlike most offerings, where exercise prices are typically 30–50% higher than the stock price.

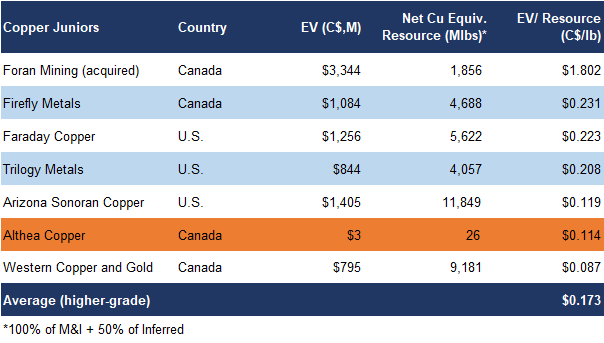

Comparables Valuation

Source: FRC / S&P Capital IQ / Various

At the IPO financing price of $0.30/share, Althea’s historic resources are valued at $0.11/lb, compared with a sector average of $0.17/lb for high-grade copper juniors, a 34% discount

Applying the sector average, we estimate a pre-IPO valuation of $0.46/share, and a post-IPO valuation of $0.43/share

This valuation is based solely on Althea’s historic resources and excludes any potential upside

Conclusion

We believe Althea Copper is interesting as an early-stage, high-grade project in a region dominated by Hudbay, which has a strong track record of acquiring promising juniors. Based on our comparable valuation, we believe the IPO is priced at a discount. Multiple catalysts lie ahead, including the IPO, geophysical surveys, and a maiden drill program.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- Commodity prices

- Access to capital and potential share dilution

- Exploration and development

- No NI 43-101 compliant resource

- Permitting

We are assigning a risk rating of 5 (Highly Speculative)