Disclosure: Delivra Health Brands Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Delivra Health has paid FRC a fee for research coverage and distribution of reports. All figures in C$ unless otherwise specified. See last page for other important disclosures, rating, and risk definitions.

Overview

Products

DHB’s product portfolio consists of sleep aid/anxiety relief formulations, and pain relief products

Follows an asset-light model by outsourcing manufacturing and packaging to established entities in North America

Two Primary Brands: Dream Water (sold in the U.S./Canada/the Middle East), and LivRelief (sold in Canada)

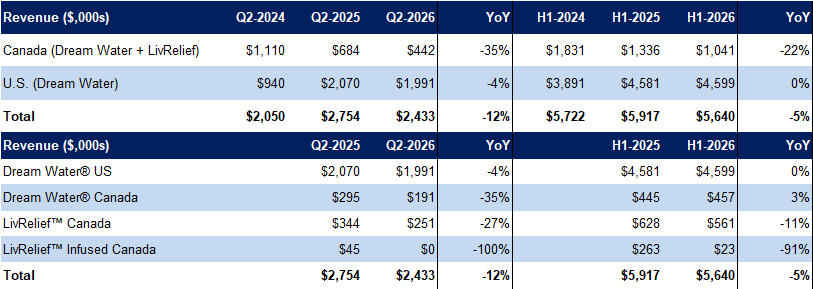

Dream Water drove ~90% of revenue this quarter, vs 84% a year ago

Extensive Distribution

Source: Company

Available at 30k+ outlets in the U.S., and Canada, including major retailers, airports, and pharmacy chains

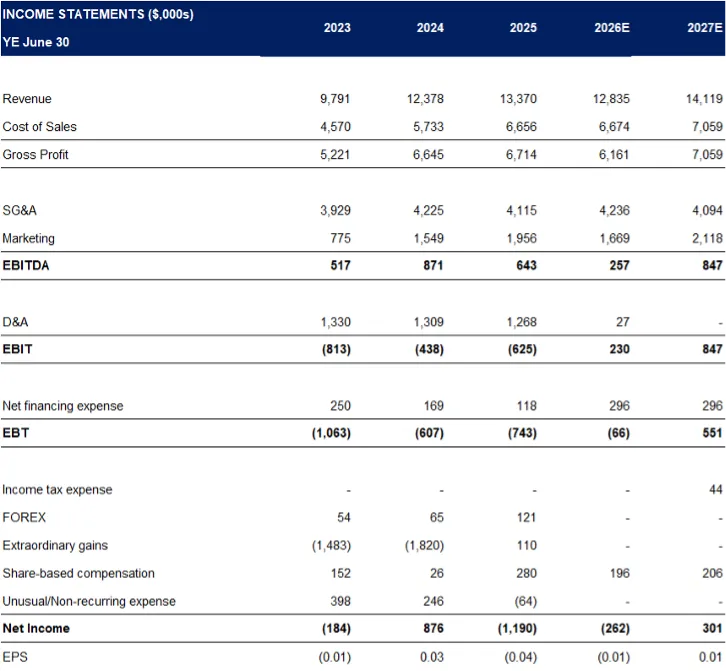

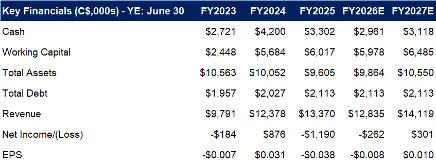

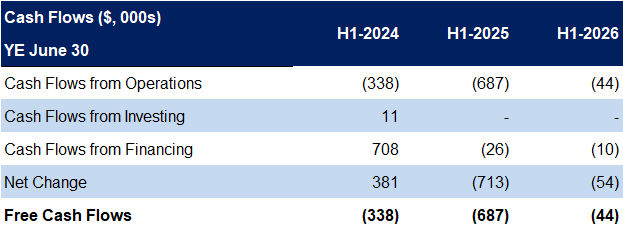

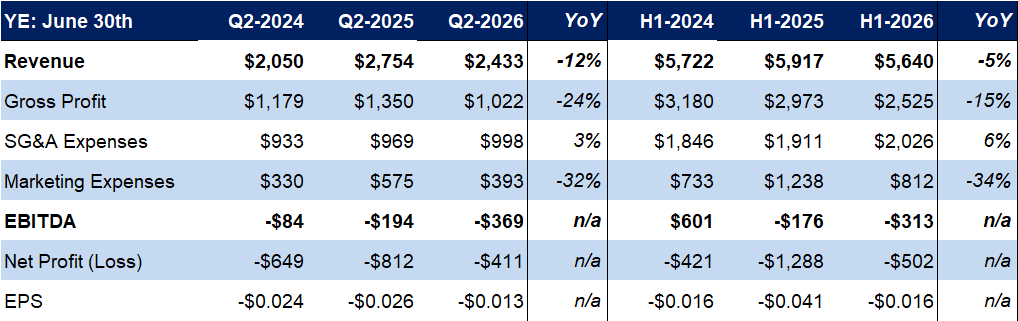

Financials (Year-End: June 30th)

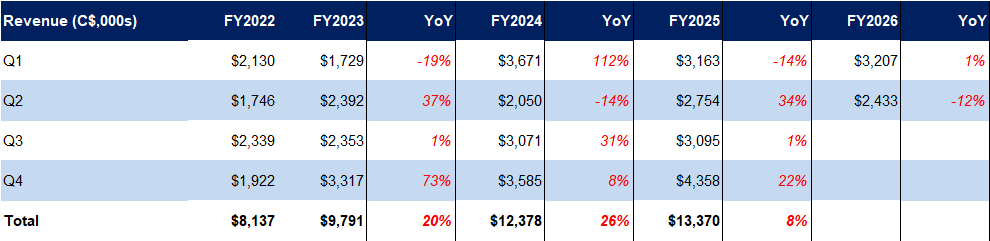

Q2 revenue fell 12% YoY, 14% below our estimate, mainly due to weaker Canadian sales, which management attributes to the timing of large customer orders

YTD direct-to-consumer e-commerce sales rose 27% YoY, indicating strong engagement and repeat purchasing

* Historically, quarterly revenue has been volatile due to the timing of orders from large customers

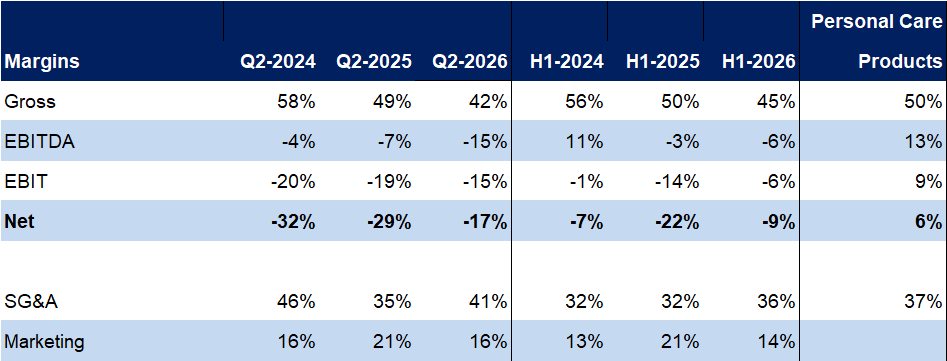

Gross margins declined 7 pp YoY, missing our estimate by 2 pp, mainly due to lower revenue; management noted that vendor pricing, customer mix, and product mix also affected margins, though details were undisclosed

SG&A expenses rose 3% YoY, but came in 2% below our estimate, a positive sign of cost control

Source: Company Filings, FRC

Marketing expenses fell 5 pp YoY to 16% of revenue, following last year’s unusually high spend on a major marketing program; for context, industry peers spend 10–20% of revenue

EBITDA declined due to lower revenue, and gross margins

Although EPS improved YoY, from ($0.03) to ($0.01), due to lower depreciation expenses, it still fell short of our forecasted modest profit of $0.001/ shar

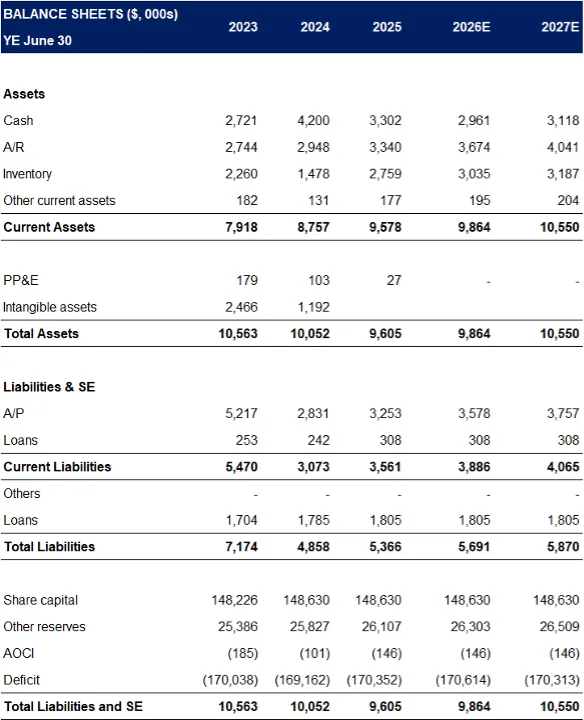

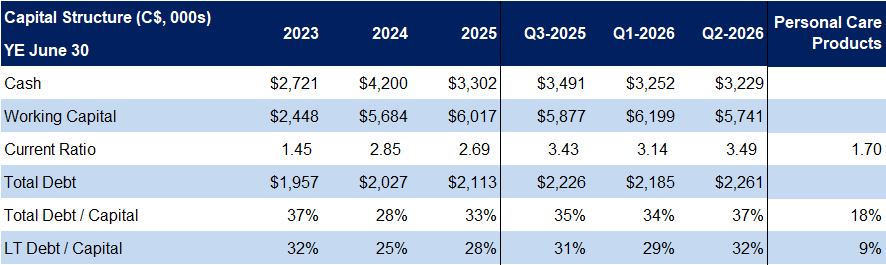

Balance sheet remains healthy

Source: Company Filings, FRC

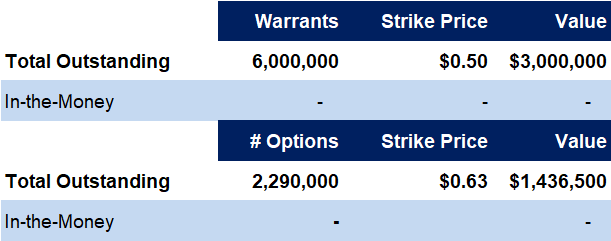

No outstanding options/warrants are in-the-money

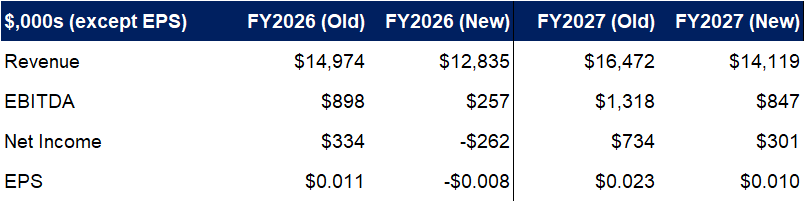

FRC Projections and Valuation

Source: Company Filings, FRC

Following weaker-than-expected Q2 results, we are revising down our revenue and EPS forecasts, and now expect EPS to turn positive next year instead of this year

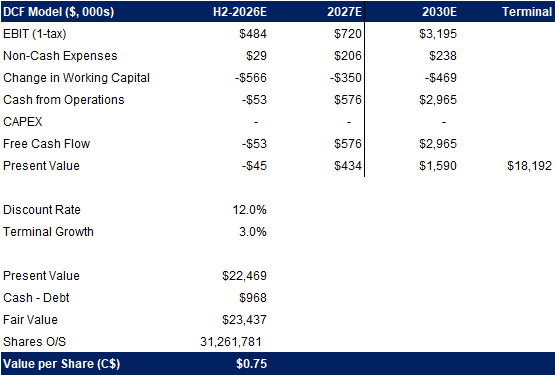

DCF Valuation

Source: FRC

As a result, our DCF valuation declined from $0.86 to $0.75/share

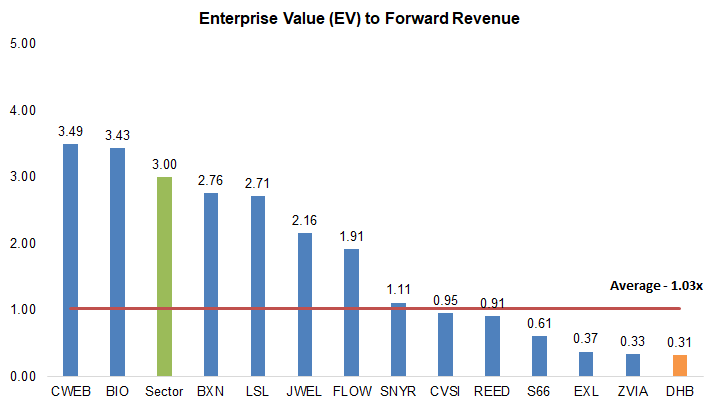

Comparables Valuation

Source: FRC/S&P Capital IQ

DHB is the most undervalued stock on our list within the Personal Care Products sector

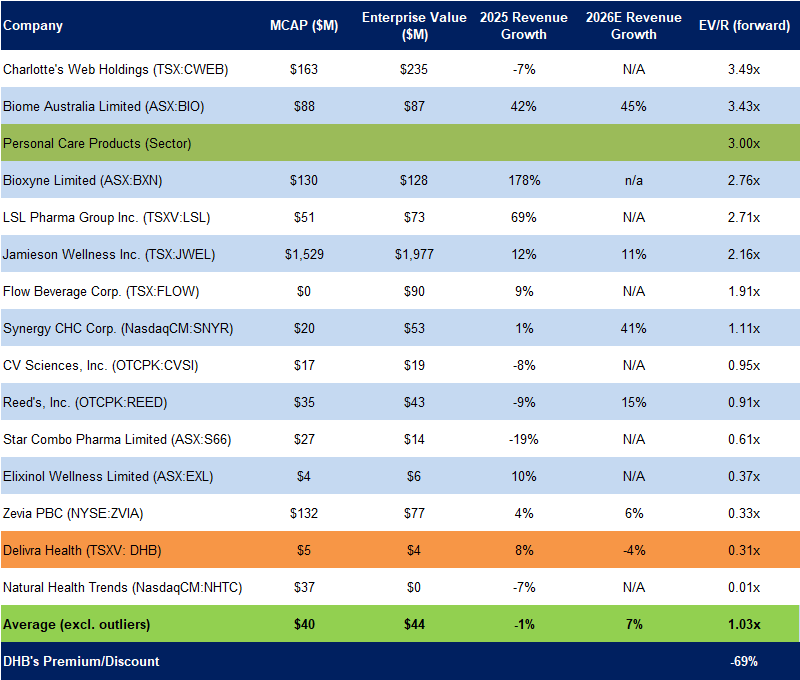

Comparables Valuation

Source: FRC/S&P Capital IQ

The average sector forward EV/Revenue is down 11% since our previous report in November 2025

DHB is trading at a 69% discount to comparables (previously 54%)

Using the average sector EV/Revenue, we arrived at a comparables valuation of $0.45/share (previously $0.59/share)

We are reiterating our BUY rating, while adjusting our fair value estimate from $0.73 to $0.60/share (the average of our DCF and comparables valuations). Despite Q2 revenue weakness and margin pressure, we believe DHB’s strong e-commerce growth, near-term profitability, and undervalued balance sheet highlight significant upside potential.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining our risk rating of 3 (Average)

APPENDIX