Disclosure: Olympia Financial Group Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Olympia Financial Group has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

The leading Canadian custodian/ administrator of alternative investments

OLY’s platform supports a broad range of investments typically not offered by banks or traditional trading platforms

Primary Services

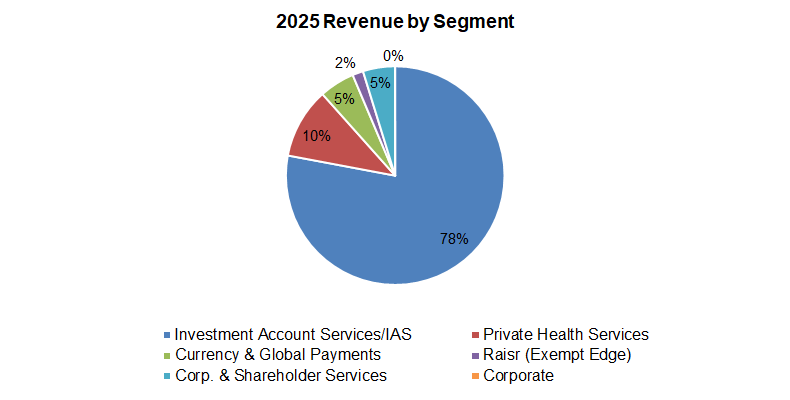

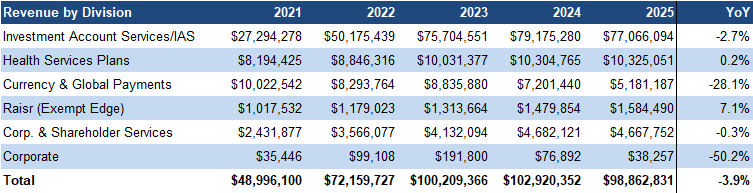

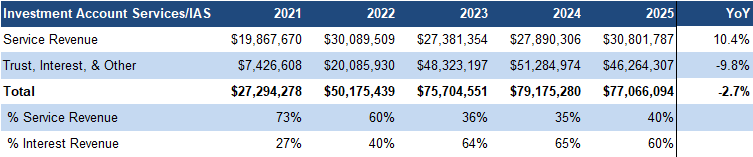

In 2025, revenue mix remained stable: 78% from IAS (77% in 2024), 10% from private health services (unchanged), and 12% (13% in 2024) from other services

Source: Company / FRC

In 2025, client assets rose 10% YoY to $13.21B, 0.3% above our forecast

We are raising our 2026 year-end estimate by 0.2% to $13.96B

Financials (Year-End: Dec 31st)

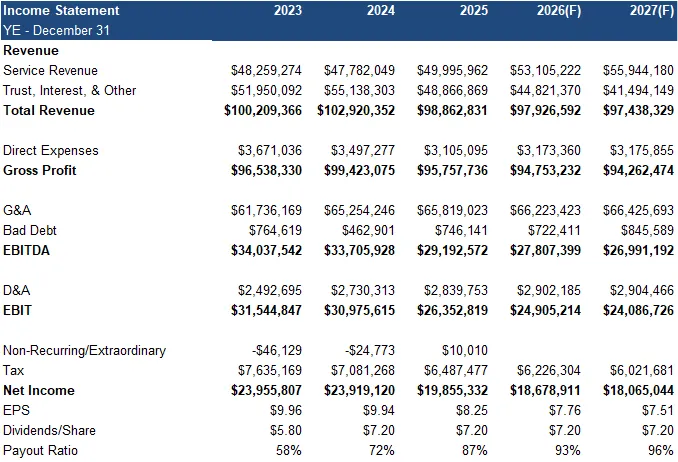

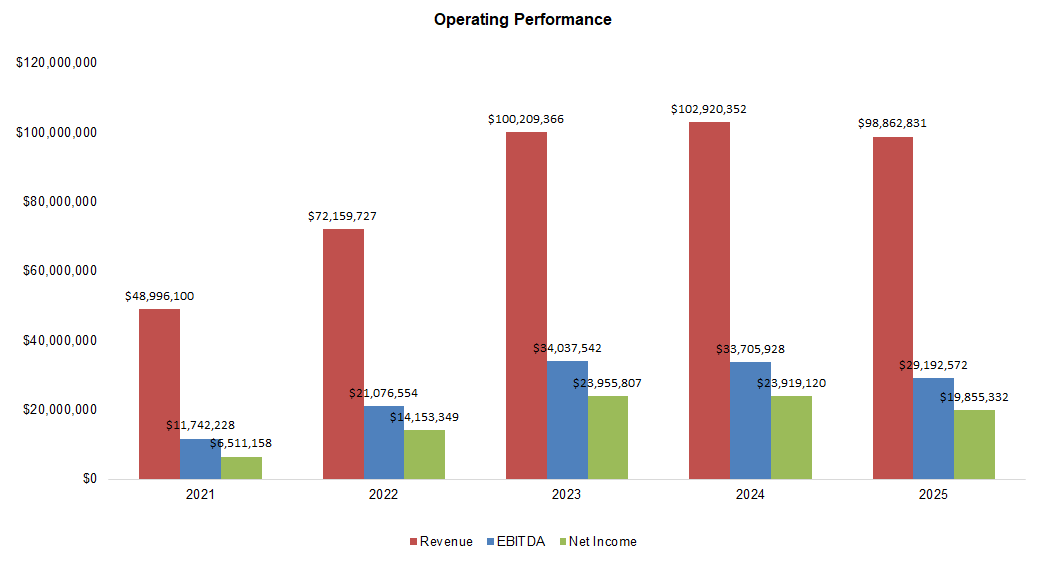

Revenue declined 3.9% YoY, but exceeded our forecast by 0.6%, driven by lower interest on unallocated client capital

Importantly, services revenue from core divisions (IAS and Private Health Services) was up 9% YoY, driven by higher transaction volumes

*The primary source of revenue in the “Trust, Interest, & Other” category is the interest earned on placing undeployed client capital in cash accounts at major Canadian banks.

*Service revenue includes annual and transaction fees

*‘Trust, interest, and other’ primarily includes interest revenue

G&A expenses rose 1% YoY, coming in 0.3% below our forecast

Source: FRC / Company

EPS declined 17% YoY, primarily due to weaker revenue, but exceeded our forecast by 1.6%

Source: Company/FRC

Dividends held steady at $7.20/year, aligning with our estimate

The payout ratio was 87% in 2025 vs the historic average of 72%

Source: Company/FRC

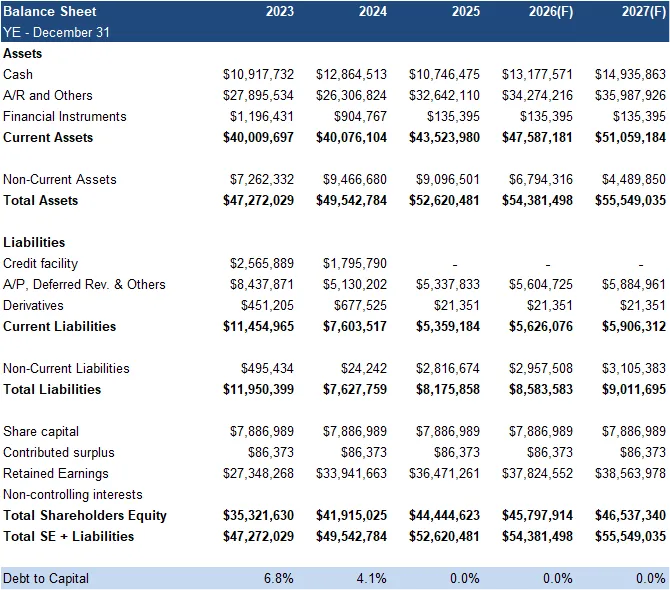

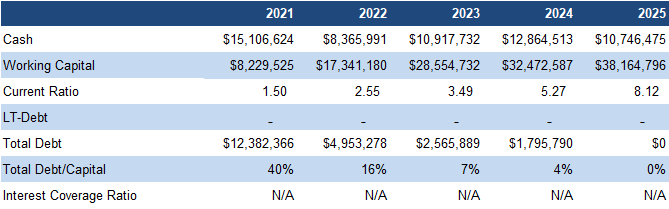

Strong balance sheet

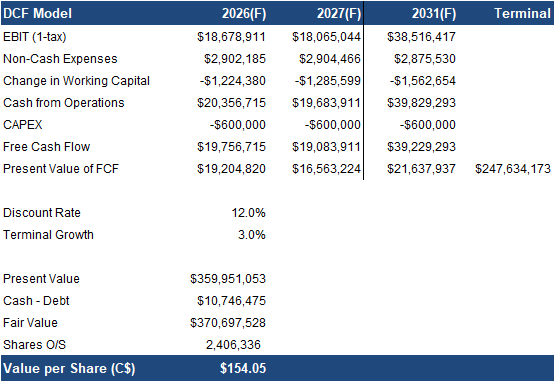

FRC Projections and Valuation

With client assets growing ahead of expectations, we are raising our 2026 revenue and EPS forecasts accordingly

Source: FRC

As a result, our DCF valuation increased from $147 to $154/share

Source: FRC/S&P Capital IQ

With sector multiples down 3% since our November 2025 report, our comparables valuation fell from $186 to $181/share

We are reiterating our BUY rating, and adjusting our fair value estimate from $166.83 to $167.49/share (the average of our DCF and comparables valuations), implying a potential return of 43% (including dividends) in the next 12 months. OLY delivered resilient results with strong client asset growth and services revenue, while interest revenue may stabilize as rates level off. Trading at a 19% discount to the sector average , and with a 5.88% yield, we believe OLY offers attractive income , and potential upside from expansion in Ontario, Canada’s largest province.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

Maintaining our risk rating of 3 (Average)

APPENDIX