Disclosure: Argo Gold Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Risks

Price and Volume (1-year)

* Qualified Person: Michael Guo, PhD, PGeo, MG Geological Consulting Ltd

* Argo Gold Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

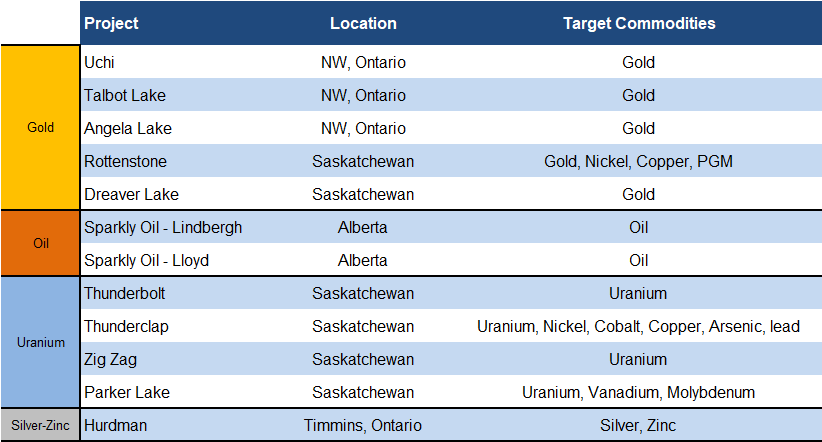

Five gold projects and a silver-zinc project in Ontario and Saskatchewan, oil production in Alberta, and four uranium projects in Saskatchewan

Portfolio Summary

Source: Company / FRC

The following sections summarize ARQ’s flagship projects.

Sparky Oil Project

During 2023–2024, Argo invested $2.6M to develop five oil wells in Alberta, operated by Croverro Energy , a private oil producer in Alberta and Saskatchewan. Four wells are currently producing.

ARQ made its first oil investment in 2023

Project Location

Source: Company

Wells are located in Lloydminster and Lindbergh, producing heavy oil

Heavy oil is denser, more viscous, and lower in API gravity (<22 API), making it harder to refine and generally selling at a discount to light oil, which flows easily and yields more high-value products. Heavy oil wells typically have modest initial production , but can maintain output steadily for 7–10 years, whereas light oil wells often start higher but decline faster.

Oil Type & Production Profile

A standard well in Argo’s target regions, often horizontal or multilateral to maximize reservoir contact, produces roughly 80–120 bpd, with a moderate decline rate of 10–15% per year in the early years. Drilling costs are typically $1–2 M per well, with OPEX around $15/bbl, making them relatively low-CAPEX and low-OPEX projects. This efficiency is because the wells target the Sparky Formation , a shallow layer at 450–650 m, which keeps drilling costs low, combined with high pressure and good permeability, allowing production without expensive injection methods.

Well Design & Economics

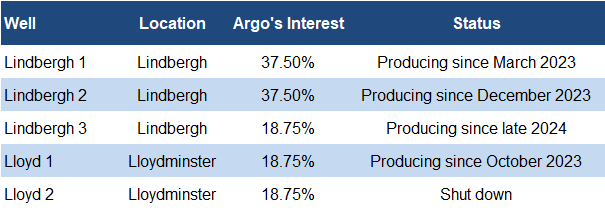

Argo’s Wells

Argo’s ownership (working interest) in the wells ranges between 18.75% and 37.5%

Four wells currently produce 65 bpd

Source: Company / FRC

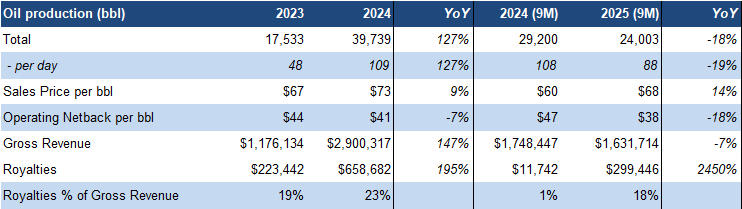

Production rose in 2024 with the addition of new wells, but declined in 2025 due to natural reservoir depletion

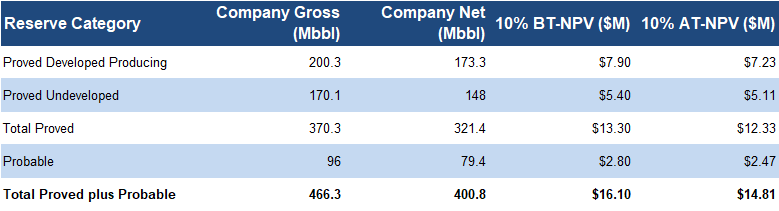

Oil Reserves, 2024

Qualified Person: William Kerr, P.Geo., Consulting Geologist of Argo Gold

Source: Company

Together, these wells generate roughly $1M in operating profit per year, and an independent evaluation values Argo’s interest at $15M

Source: GLJ, Sproule, and FRC

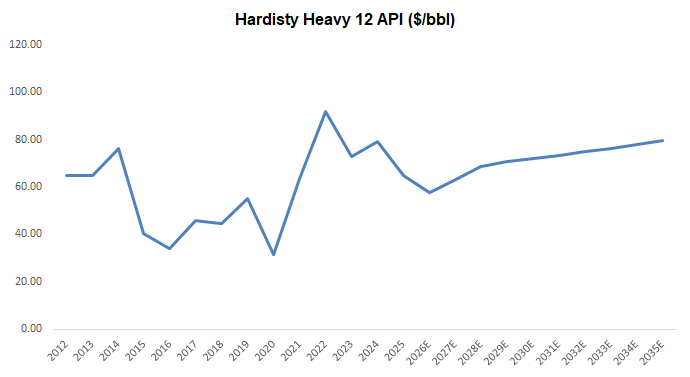

Consensus oil price forecasts (near and long-term) are well above the 10-year average of $58/bbl, suggesting a positive outlook for producers

Argo also has an option to participate in additional 10-15 oil wells. Management plans to use cash flow from oil production to fund exploration of its gold and uranium assets, while minimizing share dilution.

Uchi Gold Project

ARQ gained control of the project in 2018

Ownership and Location

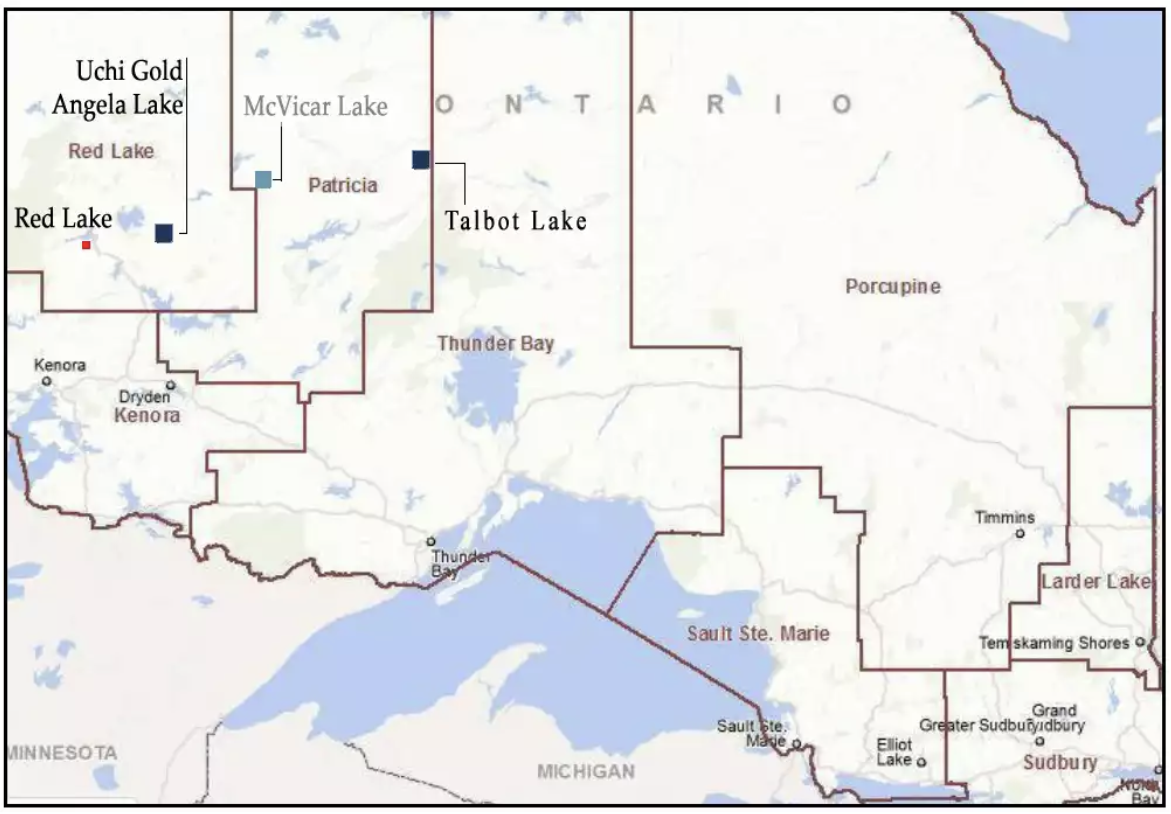

The flagship Uchi project covers 2,176 hectares in northwestern Ontario’s Birch-Uchi Greenstone Belt (BUBG), which hosts the renowned Red Lake gold district. The BUBG is known for three types of gold deposits:

All three types can support long-lasting, lower-cost operations .

Uchi is close to First Mining Gold’s (TSX: FF) Springpole deposit, one of Canada’s largest undeveloped open-pit gold deposits. Proximity to major players is important, as a successful discovery could make the project an attractive acquisition target.

Location Map

Source: Company

Located south of the past-producing Uchi gold mine

The property benefits from existing infrastructure, including roads, hydro power, water, and access to third-party processing facilities

History and Mineralization

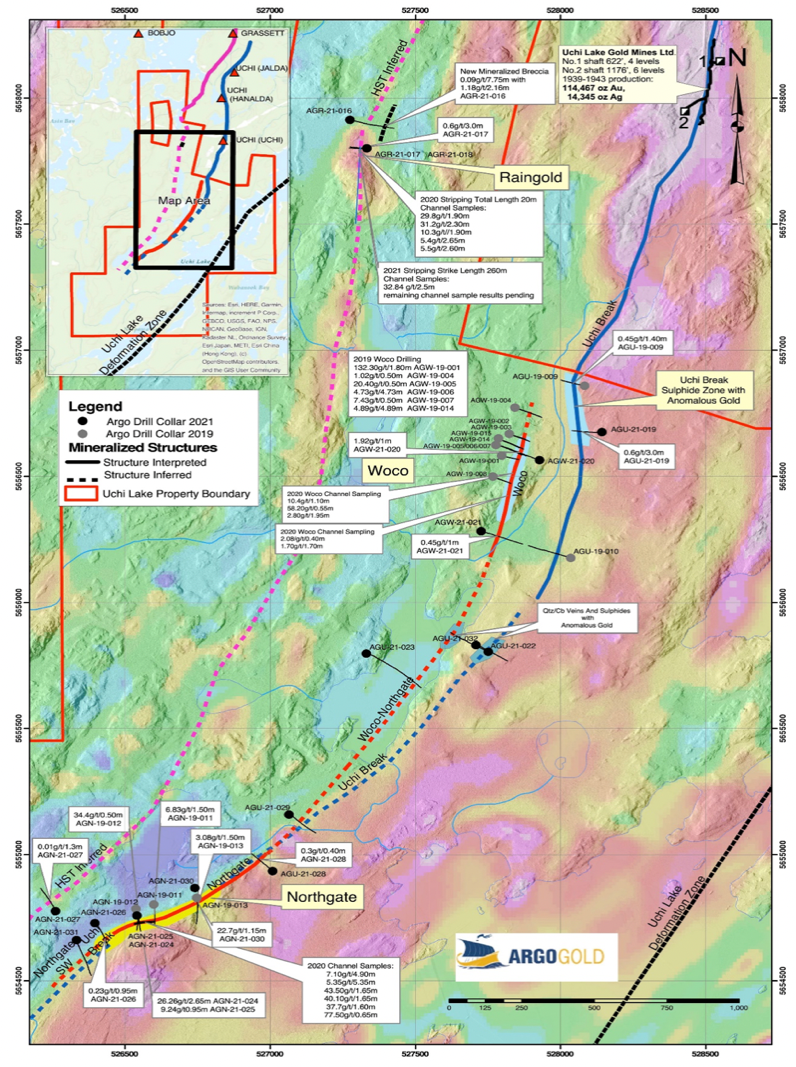

Since the 1930s, six companies have explored the property using sampling, mapping, and drilling. They found high-grade gold veins in three areas: Woco (400 m), Raingold (100 m), and Northgate (500 m). Drilling indicates the property may also contain copper, zinc, and other valuable metals

Exploration has identified key targets

Four Mineralized Zones

Qualified Person: Michael Guo PhD, PGeo, MG Geological Consulting Ltd.

Source: Company

ARQ’s drilling revealed very high-grade gold at multiple veins:

• Woco: 1.8 m at 132 g/t Au

• Northgate: 0.5 m at 34.4 g/t Au and 2.65 m at 26.3 g/t Au

• Raingold: 2.5 m at 32.8 g/t AuFor context, gold deposits with grades above 8 g/t are considered high, and anything over 30 g/t is often called bonanza grade, so these results are highly impressive

Based on exploration so far, management has outlined an exploration target of about 0.4 Moz of gold at an exceptionally high grade of 15 g/t (not independently verified or NI 43-101 compliant). While we consider this a modest resource in size, the unusually high grades make it extremely attractive. This target is based on drilling and surface sampling down to around 200 m. The plan is to drill deeper to see if the high-grade veins at Woco and Northgate continue at depth, and to test whether the metal-rich rocks at the Uchi Break zone could point to a hidden VMS deposit with copper, zinc, and other metals.

Permitting underway, with drilling set to commence shortly afterward

Other Key Projects

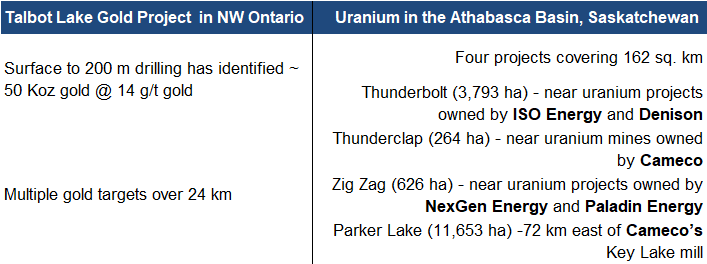

Argo also controls several other early-stage gold and uranium projects, most of which are near well-known projects held by larger companies

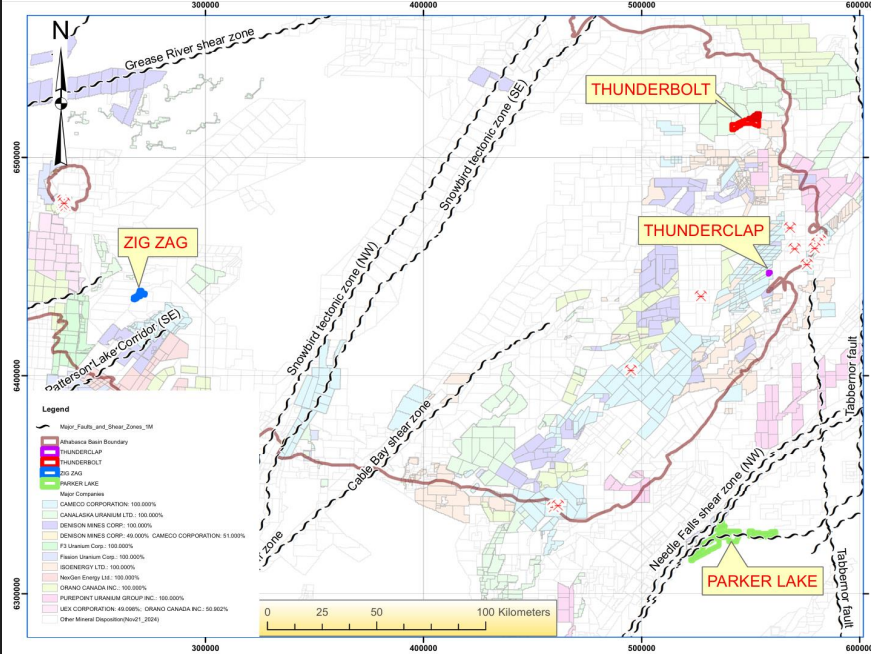

Uranium Projects

Source: Company

One project worth highlighting is the Talbot Lake gold project in Ontario, where the company has outlined an exploration target of about 50 Koz of gold at an exceptionally high grade of 14 g/t (not independently verified or NI 43-101 compliant

Management and Board

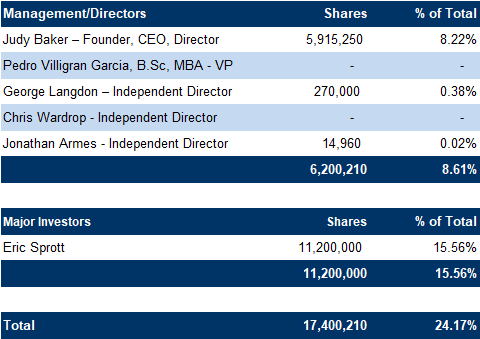

Share Ownership

Source: Sedi/FRC

With 8% ownership and a $1M loan to the company, we believe the CEO demonstrates strong commitment to shareholders

Eric Sprott owns 16% of the company’s equity

Three out of four directors are independent

Brief biographies of the management team and board members, as provided by the company, follow:

Judy Baker – Founder, CEO, Director

Ms. Baker has over 30 years of experience in the mining and mineral exploration sectors. Capital markets experience includes research, equity analysis, IPO’s, valuation, restructuring, sales and fund management. Over the last 15 years, Ms. Baker has founded multiple mineral exploration companies and raised over $30 million for exploration and development. Ms. Baker holds an Honours B.Sc. Geological Engineering in Mineral Resources Exploration from Queen’s University (1990) and an M.B.A. from Ivey Business School (1995).

Pedro Villigran Garcia, B.Sc, MBA - Vice-President

Mr. Villigran Garcia is an Engineer and an MBA that has been involved in the mining industry for two decades. Mr. Villagran Garcia has served as a Director and Officer of several Public Companies listed on the NYSE, NASDAQ and the TSX Venture Exchange. Mr. Villagran Garcia studied Industrial and Systems Engineering at ITESM and obtained an MBA from the University of Texas & ITESM Academic Venture.

George Langdon, B.Sc, M.Sc, PhD (Geology) – Independent Director

George S. Langdon is a petroleum geologist with over 30 years experience in the old and gas industry. He holds a doctorate in Earth Sciences from Memorial University of Newfoundland. In the last 20 years he has been involved as a technical consultant and investor in building several junior public resource exploration companies, and was co-founder and President of Shoal Point Energy Ltd. from 2007 to 2013, as well as a director of Gulf Shores Resources from 2000 to 2016, and Contact Exploration from 2001 to 2008. He currently is also a Director of Relay Medical Corp., a medical diagnostics development company.

Chris Wardrop - Independent Director

Chris Wardrop is a lawyer in Northern Ontario with a practice that focuses on Real Estate, Estate Planning & Estate Administration and Corporate & Commercial Law. Over the past 25 years, he has been involved in several companies owning interests in a number of diverse business activities including the food and beverage industry, real estate, junior resource sector, and private money lending.

Jonathan Armes - Independent Director

Mr. Armes currently serves as Managing Director of Enviromine Inc., a private mineral exploration and development company based in Toronto, Ontario. He previously served as CEO of Ophir Gold from 2016 until 2021 and served as the CEO of ALX Uranium Corp. from 2010 to 2016. Jon has provided corporate development, project management and investor relations services to both public and private mining exploration companies for over 20 years. Jon graduated from the University of Guelph in 1993 with a Bachelor of Applied Science Degree.

Financials

Source: FRC / Company

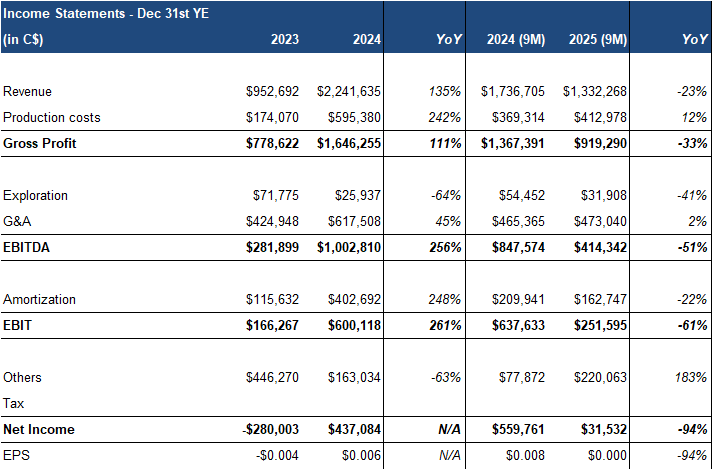

The company has been profitable since commencing oil production in 2024

Revenue and EBITDA peaked in 2024 with new wells, but fell in 2025 due to lower production

All exploration and G&A costs have been fully funded by oil revenue

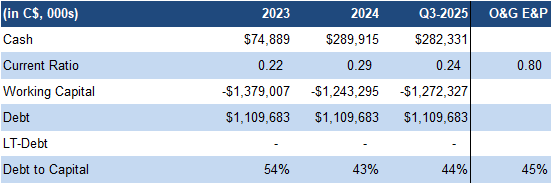

The company has $1.11 M in debt, provided by the CEO

Source: FRC / Company

FRC Projections and Valuation

Source: FRC

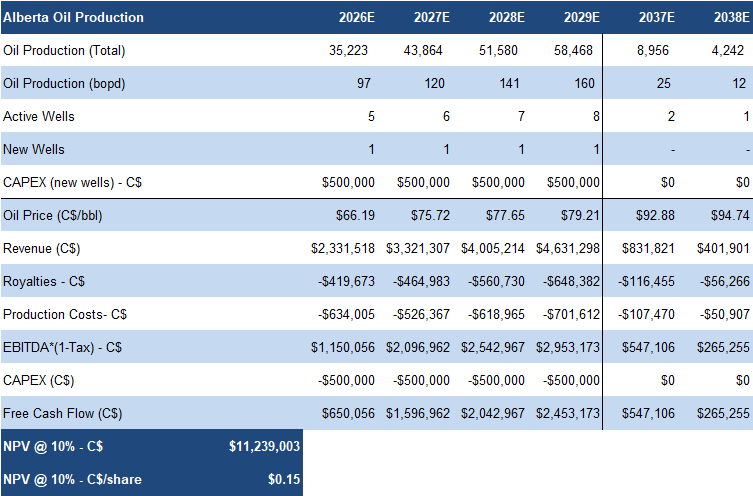

Our fair value estimate on the company’s oil production is $0.15/share, with all key assumptions summarized in the table

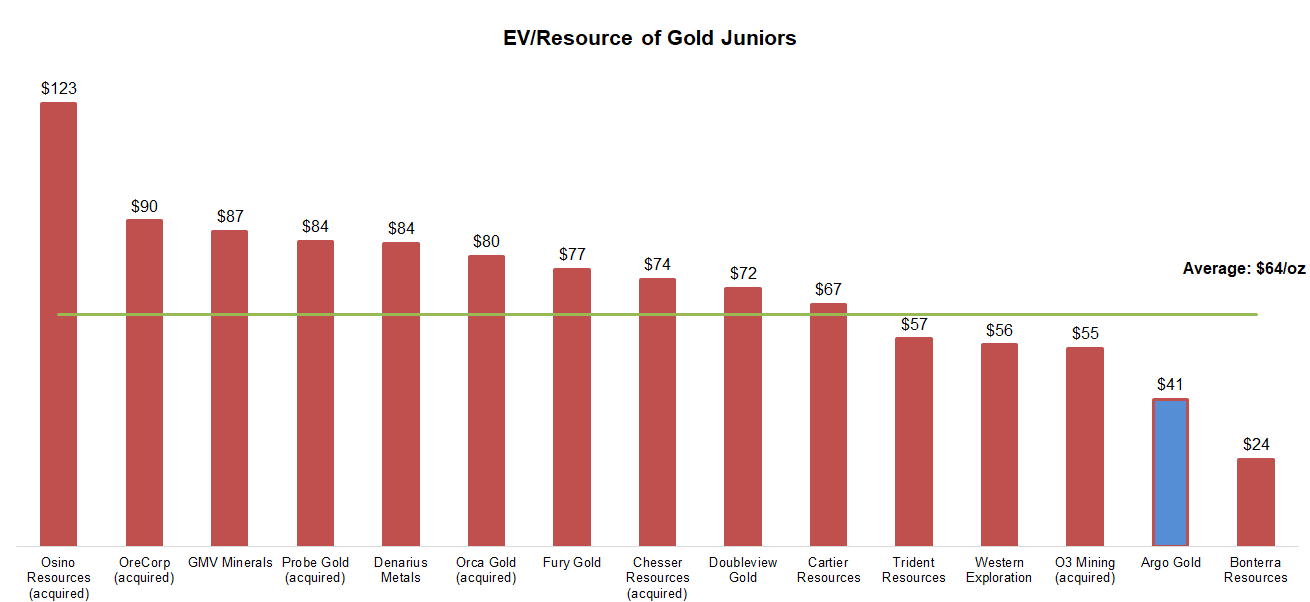

*Resource – 100% of M easured and Indicated + 50% of Inferred Resources. We have discounted ARQ’s potential resources by 50%.

Source: S&P Capital IQ / Various / FRC

ARQ is trading at $41/oz of gold resources identified on two of its properties (not NI 43-101 compliant) vs. the sector average of $64/oz

Applying the sector multiple on ARQ’s potential resources, we arrived at a fair value estimate of $0.20/share

Source: FRC

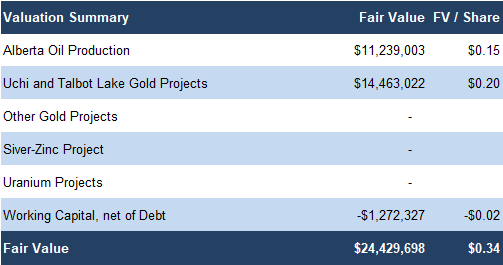

Using a sum-of-parts model, we are arriving at a fair value estimate of $0.34/share

Given their early-stage nature, we are not currently assigning a value to the company’s other projects

We are initiating coverage with a BUY rating, and a fair value estimate of $0.34/share. Argo offers diversified exposure to gold, oil, silver, and uranium, supported by cash flow from profitable oil production that funds exploration without shareholder dilution, a rare model among junior resource companies. With oil assets alone valued above the company’s current MCAP, and multiple near-term catalysts ahead, we believe the market is materially undervaluing Argo’s portfolio .

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are assigning a risk rating of 4 (Speculative)

APPENDIX