Disclosure: MetalQuest Mining Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Qualified Persons: Adou Katche, P.Geo., Troy Gallik, P.Geo., Alexandr Beloborodov, P.Geo., Consultants to MetalQuest Mining / MetalQuest Mining has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise indicated.

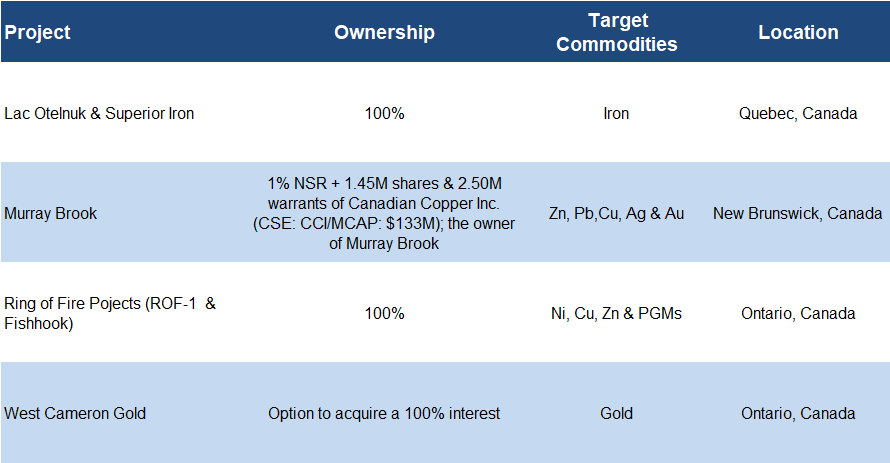

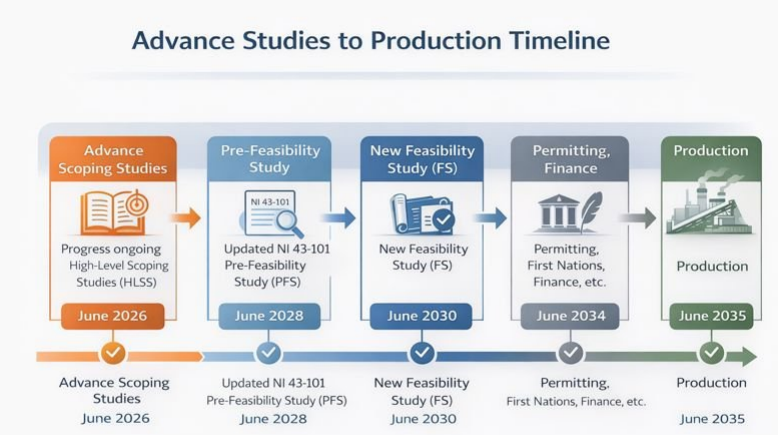

Diversifying assets: The company has strengthened its portfolio with an early-stage iron project in Quebec, two polymetallic projects in Ontario, and an option on a gold project in Ontario MQM’s flagship and most advanced project In January 2026, the company lowered the outstanding royalty on the project from 2.5% to 1.5% by issuing 0.50M shares Located 155 km northwest of Schefferville, near active iron ore mines operated by majors, including Rio Tinto (NYSE: RIO), Tata Steel, and ArcelorMittal (NYSE: MT)MQM aims to complete an updated feasibility study (a detailed, independent economic study) by 2028, with the long-term objective of moving into production within 10 years

Portfolio Overview

Source: FRC / Company

The following section s summarize the recent acquisitions, and provide a quick update on its flagship project.

MQM’s flagship and most advanced project

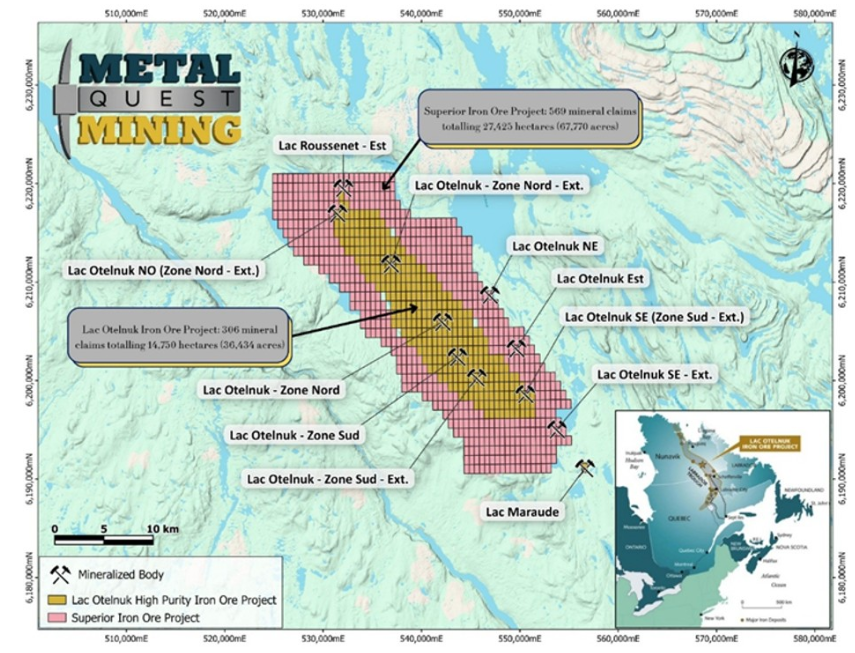

Lac Otelnuk Iron Ore Project, Quebec

In January 2026, the company lowered the outstanding royalty on the project from 2.5% to 1.5% by issuing 0.50M shares

Located 155 km northwest of Schefferville, near active iron ore mines operated by majors, including Rio Tinto (NYSE: RIO), Tata Steel, and ArcelorMittal (NYSE: MT)

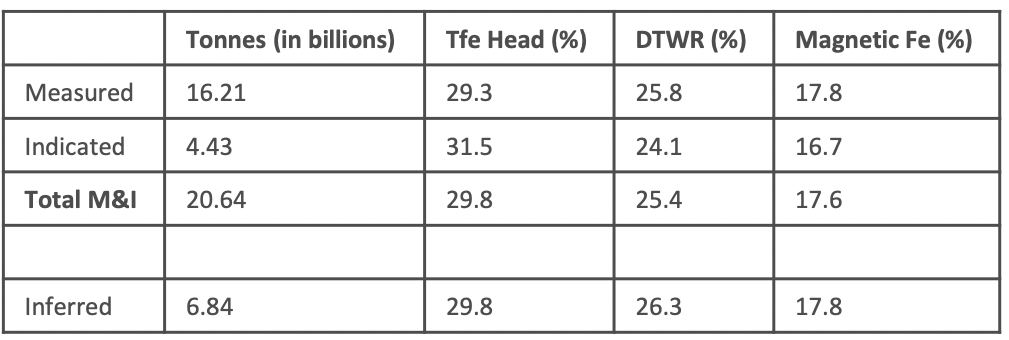

2013 Resource (Historic)

MQM aims to complete an updated feasibility study (a detailed, independent economic study) by 2028, with the long-term objective of moving into production within 10 years

2015 Reserves

QP: Adou Katche, P.Geo ., Consultant to MQM

Source: Company

The project hosts a large, near-surface iron deposit

Tests show it can produce high-quality iron (68% Fe), potentially commanding premium prices

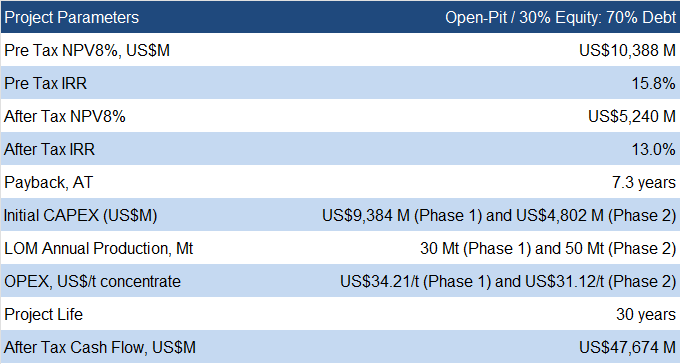

2015 FS Highlights

Source: Technical Report/FRC

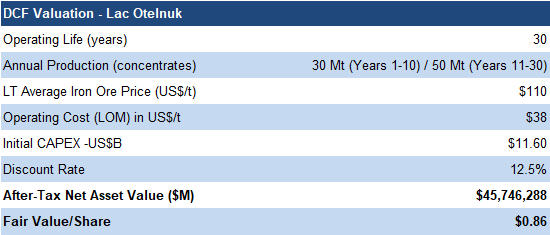

The previous feasibility study (2015) reported an after-tax NPV8% of US$5.24B, based on an iron ore price of US$105/t (vs. the current spot price of US$100/t)

However, MQM’s MCAP is just $14M, suggesting the market is largely overlooking the project

A recent technical study (gap analysis) , led by AtkinsRéalis , the firm behind the 2015 feasibility study , showed a clear plan to move the project forward. This includes checking old data, improving the mine plan and processing methods, planning infrastructure, preparing for ESG requirements, and updating the financial models. MQM is looking for a partner to help develop the project, share costs, bring expertise, and speed up the path to production.

Superior Iron Project, Quebec

Source: Company

MQM staked this asset in November 2025, meaning the mineral rights were acquired directly from the provincial government, keeping acquisition costs minimal

Directly adjoins the Lac Otelnuk project

MQM is planning geophysical and environmental studies

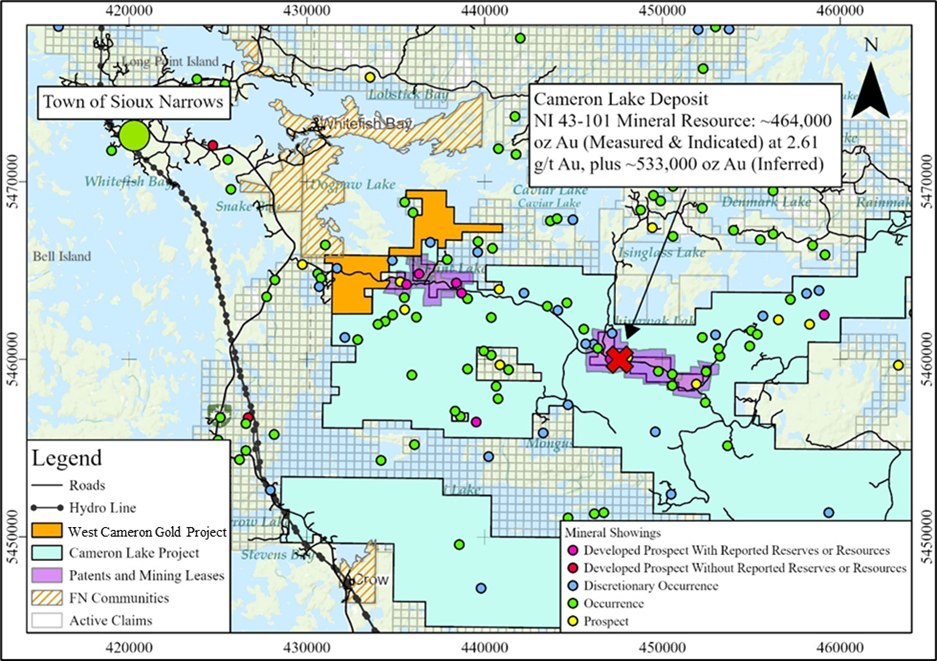

West Cameron Gold Project, Northwestern Ontario

This 1,700-hectare project in the Kenora Mining District is just 12 km from First Mining Gold’s (TSX: FF) Cameron g old p roject, which hosts 1 Moz of gold. First Mining recently agreed to sell the project for $27M to a company backed by renowned mining entrepreneur Frank Giustra’s Fiore Group.

First step into gold exploration

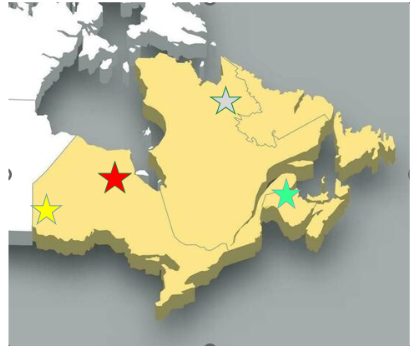

Location of the West Cameron and Cameron Gold Projects

Source: Company

MQM can acquire 100% of the project for $75k cash, and $75k shares over three years

In mining, proximity to advanced-stage projects offers key advantages:

a) Successful exploration increases the likelihood of becoming a strong acquisition target

b) Higher probability of discovering similar deposits nearby

c) Location and infrastructure are favorable for mining operations

The Kenora Mining District is an underexplored , but increasingly active gold region. It offers established mining infrastructure, highway access, proximity to power, and a relatively favorable permitting environment. Recent high-profile activity in northwestern Ontario , such as Coeur Mining’s (NYSE: CDE) US$7B acquisition of New Gold , which includes the Rainy River Mine (produced 290 Koz of gold in 2025), and the a bove-mentioned Cameron project deal , we believe underscores the region’s strategic potential.

MQM’s West Cameron project is still in its early stages. Samples from the property have returned exceptionally high gold grades , up to 9.18 g/t, compared with the 1–3 g/t typical of most gold mines globally. The most notable aspect of the project is that a big fault, called the Cameron Lake Fault, runs through the area, making it a promising spot for finding gold. The property has been explored sporadically by several companies, but has never been systematically studied.

Overall, we believe the project appears promising due to its proximity to a known gold deposit, significant geological features, and lack of comprehensive exploration. The modest acquisition terms limit financial risk while offering potential upside. MQM plans to advance permitting and engage with local stakeholders and First Nations to support upcoming fieldwork and drilling.

Shared Office with New Age Metals in Kenora

Source: Company

MQM shares a field office and core facility in Kenora with New Age Metals (TSXV: NAM; same management team) to support its Ontario properties

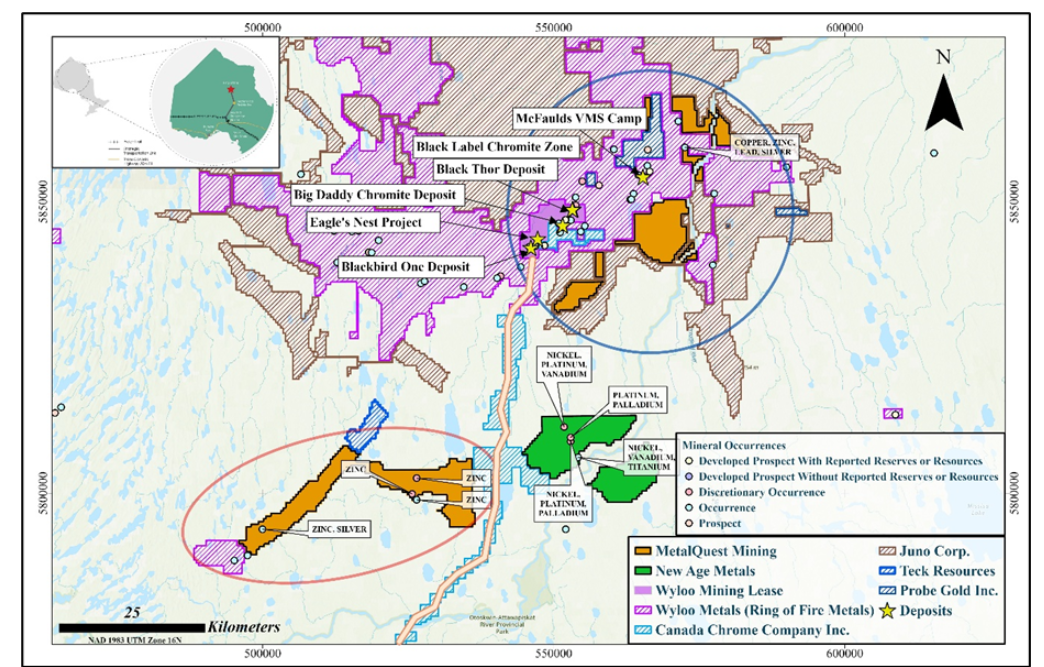

Ring of Fire Projects in Ontario

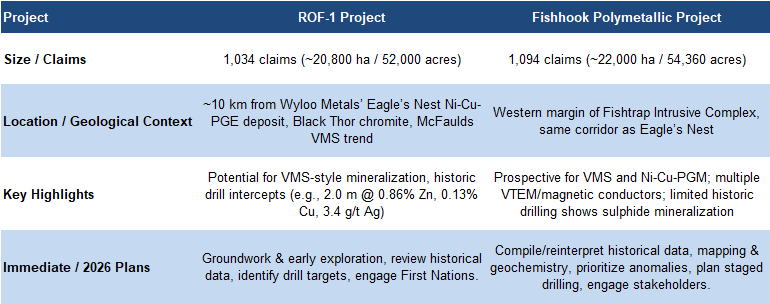

The Ring of Fire is one of Canada’s largest undeveloped mineral districts , rich in critical minerals such as nickel, copper, and platinum-group metals (PGMs). MQM has staked two projects in the regio n : the ROF-1 p roject (~20,800 ha) , and the Fishhook p olymetallic p roject (~22,000 ha). Based on limited historical work, ROF-1 is prospective for nickel, copper, and PGMs, while the Fishhook is prospective for copper-zinc, nickel, and PGMs.

Source: Company / FRC

A major positive for these critical mineral projects is their proximity to the advanced-stage Eagle’s Nest nickel-copper-PGE deposit owned by Wyloo Metals

ROF-1 and Fishhook Polymetallic Projects

*ROF-1 (northeast) and Fishhook (southwest) are circled on the map

Source: Company

The Ontario and federal governments have agreed to build an all season access road to the Ring of Fire, with construction starting this year, which would reduce logistical barriers and accelerate mining activity in the region

MQM’s land packages have not been fully explored, with only limited drilling done in the past

We believe these acquisitions offer MQM a low-cost entry into a district experiencing renewed exploration activity , and increased government interest due to its potential for critical minerals. The company is planning early-stage programs including data compilation, mapping, geochemistry, and drilling. Like West Cameron, these properties are at an early stage, with no defined resource, so their value depends entirely on the success of future exploration.

Murray Brook (Equity Investment and NSR)

MQM holds 1. 45 M shares , and 2.50M warrants (exercise price $0.12; current share price $0.69), in Canadian Copper Inc. (MCAP: $133M), representing a current market value of $ 2.50M.

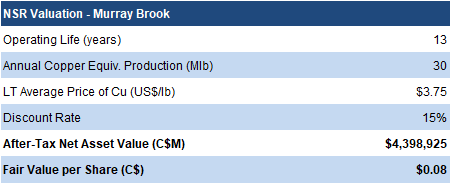

MQM also retains a 1% NSR royalty on CCI’s Murray Brook Project , located in the Bathurst Mining District, New Brunswick. The project hosts a large, low-grade open-pit polymetallic deposit. CCI can buy 0.17% of the royalty for $1 M , and must pay MQM $1 M once the project starts producing. A recent independent study ( Preliminary Economic Assessment) outlined an after-tax NPV7% of $171 M, and an IRR of 36%, based on US$4.25/lb Cu (spot price: US$6.04/lb) , with a relatively low initial CAPEX of $64 M . CCI plans more drilling this year to expand the deposit, which could increase the project’s value if successful.

Exposure to an advanced-stage copper project through equity and royalty interests

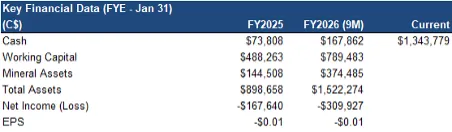

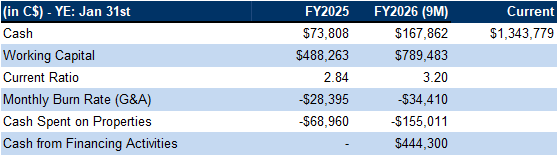

Financials

MQM raised $2M in January 2026, and now has ~$1.3M in the treasury

Source: FRC / Company

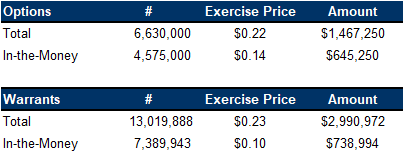

Can raise up to $1.38M from in-the-money options

FRC Projections and Valuation

Source: FRC / S&P Capital IQ / Various

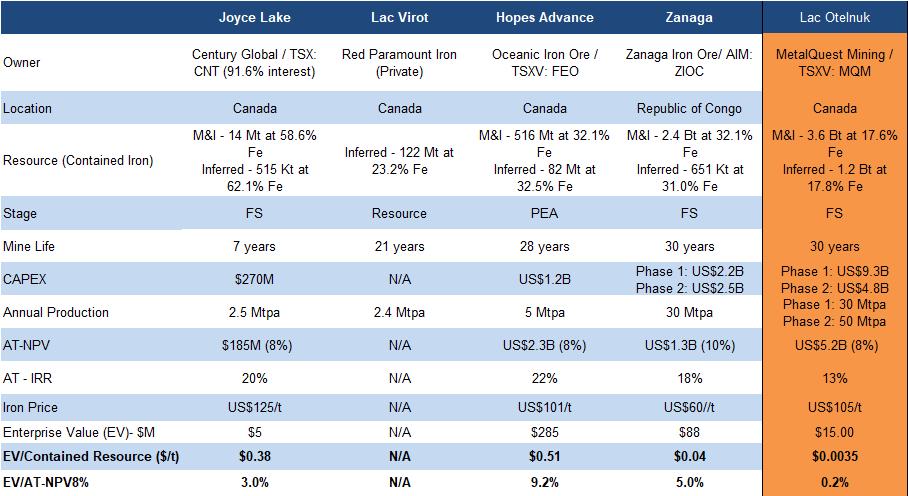

MQM’s EV/Resource and EV/AT-NPV remain materially lower than those of comparable iron ore juniors, indicating the market has yet to recognize the intrinsic value of the Lac Otelnuk project

With the reduction of the outstanding royalty, we have adjusted our DCF valuation on Lac Otelnuk from $0.80 to $0.86/share

Source: FRC

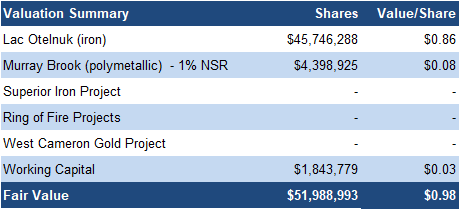

Using a sum-of-parts valuation, we arrive at a fair value of $0.98/share (previously $0.92/share)

Given their early-stage nature, we are not currently assigning a value to the company’s other projects

We are reiterating our BUY rating, and adjusting our fair value estimate from $0.92 to $0.98/share. MQM has strengthened and diversified its portfolio, reduced project royalties, and advanced technical studies on its flagship Lac Otelnuk project. With early-stage acquisitions, strategic locations, strong management ownership, and upcoming catalysts, the company offers exposure to iron, gold, and critical minerals in high-potential districts.

Risks

We believe the company is subject to the following risks:

We are maintaining our risk rating of 5 (Highly Speculative)