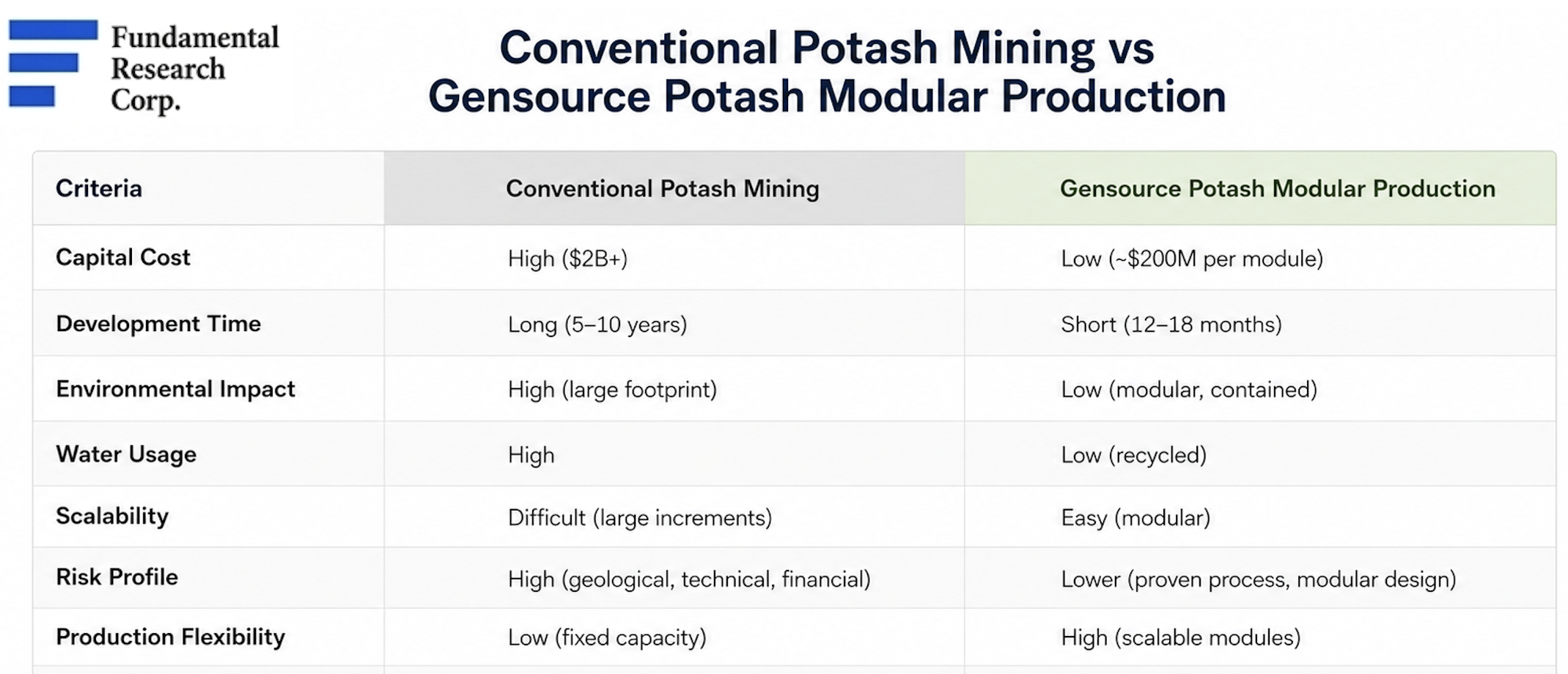

- Modular Mining Could Be a Game Changer: GSP is advancing a modular potash mining model with significantly lower initial CAPEX (~$350M vs. multi-billion-dollar conventional mines), enabling faster, phased development, and potentially reducing financing risk. While the underlying technology and process are proven, the modular production model has yet to be demonstrated at commercial scale and remains subject to execution risk.

- Compelling Economics and Significant Upside: A 2021 bankable feasibility study generated an after-tax NPV8% of $454M for a single 250,000 tonne per annum (250 Ktpa) module. We believe the current resource could support 30+ modules, while management is conservatively targeting 12 modules (3 Mtpa). Applying the economics of a single module to 12 modules implies a potential after-tax NPV8% of $5.5B, versus GSP's current MCAP of just $57M, highlighting a significant valuation disconnect.

- Strategically Positioned for U.S. Supply Security: The U.S. imports >90% of its potash, with Canada supplying ~80%. Since adding potash to its Critical Minerals List, the U.S. has funded strategic potash projects including one in Africa, highlighting the importance of secure supply. We believe GSP's proximity to the U.S., direct rail access, and an offtake agreement with Helm Fertilizers, a leading North American fertilizer distributor, strengthens its strategic position.

- Potentially Transformational ASEAN Partnership: GSP has signed an agreement with a large undisclosed ASEAN conglomerate to evaluate a two-module (500 Ktpa) project, including long-term product offtake and potential full project funding, which could limit future shareholder dilution. A definitive agreement would represent a major validation of GSP's modular strategy.

- Multiple Near-Term Catalysts: GSP is up 28% YoY, outperforming both the TSXV (+17%) and the S&P Fertilizers & Agricultural Chemicals Index (+8%). Key catalysts include an updated resource estimate and feasibility study, and a definitive agreement with the ASEAN partner, potentially including full project funding.

Risks

- Potash price volatility

- Permitting and construction delays

- Financing and strategic partner risk

- Unproven modular mining model

- Potential shareholder dilution

Price and Volume (1-year)

| |

YTD |

12M |

| GSP |

64% |

28% |

| TSXV |

-9% |

17% |

| INDEX* |

25% |

8% |

*Much of the working capital deficit relates to project partners and may be renegotiated. Discussions with the ASEAN partner could unlock significant project funding. Qualified Person: Mike Ferguson, P.Eng., President & CEO of Gensource Potash. Gensource Potash has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ except for commodity prices, which are in US$.

Source: FRC

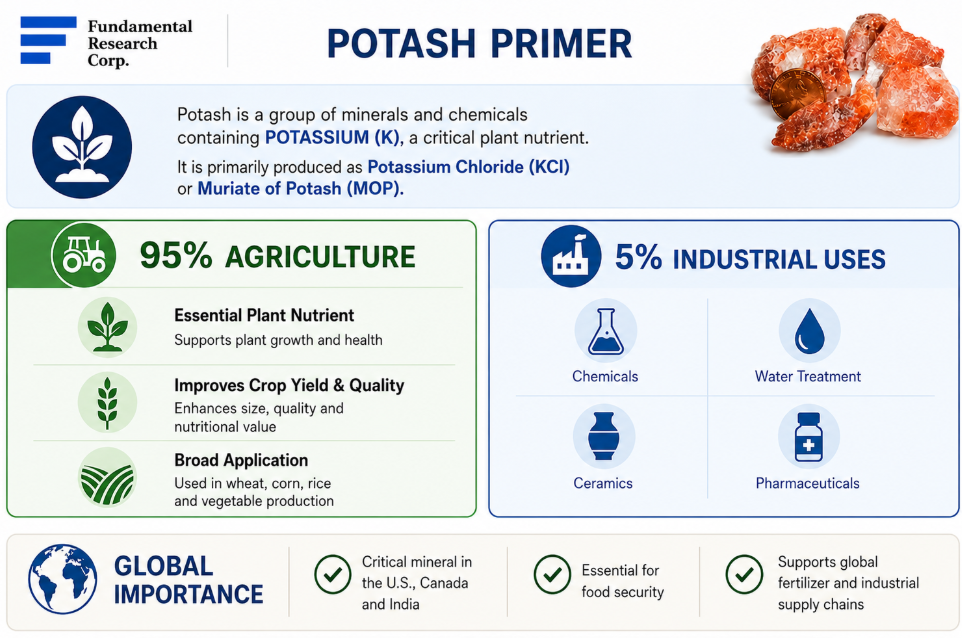

Potash is mainly used in fertilizers

Potash accounts for 21% of global fertilizer use; nitrogen 58%, phosphorus 21%

Demand is driven by global food security, population growth, and limited arable land

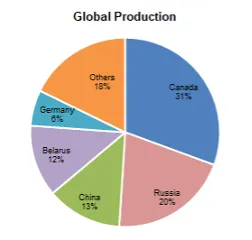

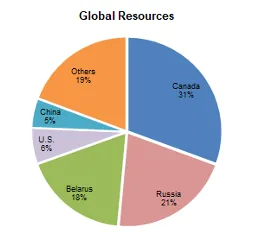

2025 Global Production vs Resources

Source: USGS / Statista / FRC

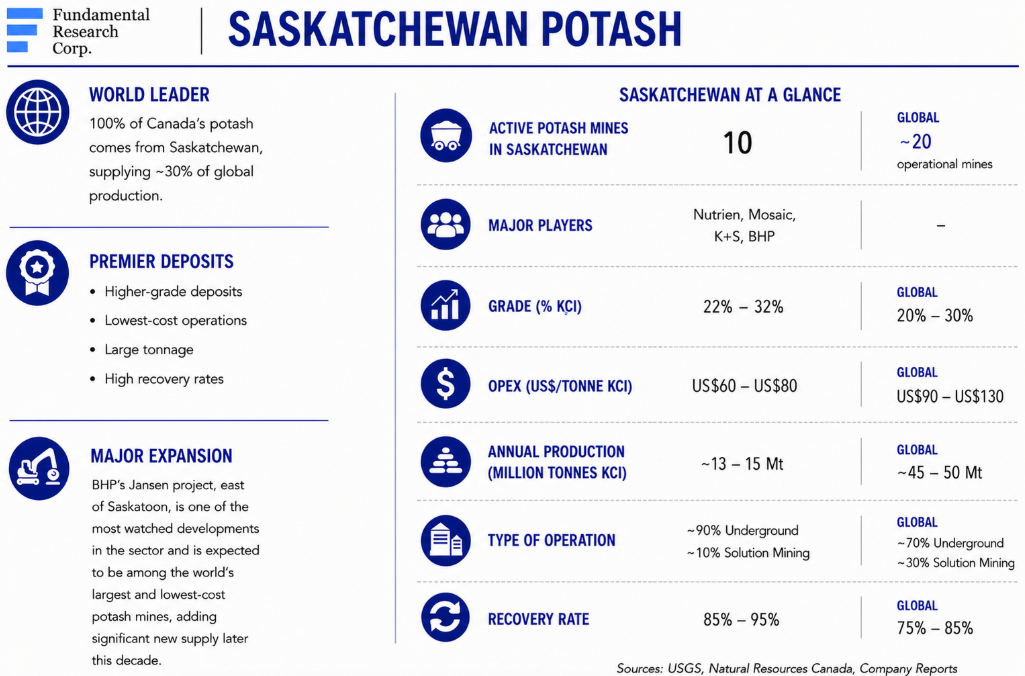

Canada is the world's largest potash producer (31%) and resource holder (31%), well ahead of Russia, Belarus, and other major potash-producing nations

Source: Precedence Research

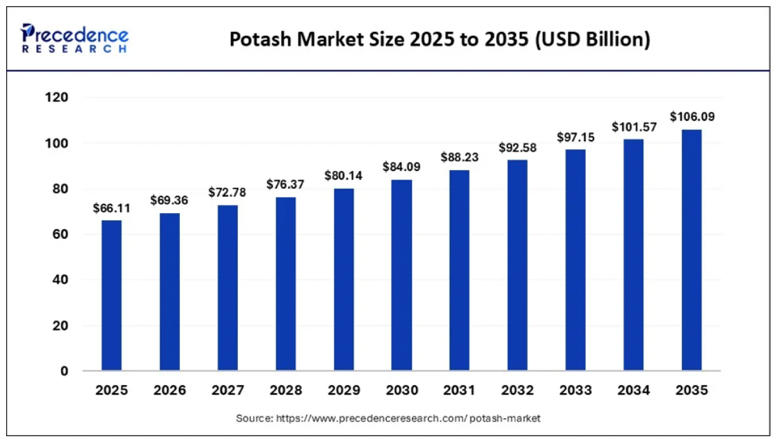

Global potash demand is projected to grow from $66B in 2025, to $106B by 2035 (4.8% CAGR)

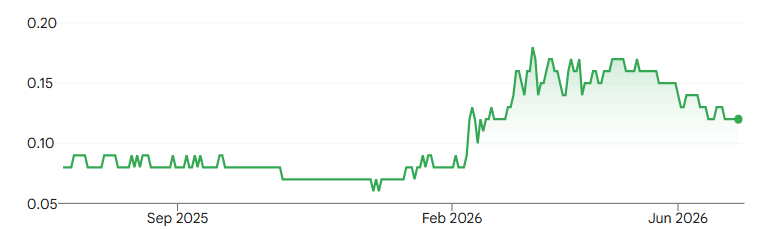

U.S. Retail Potash Prices

Source: DTN Progressive Farmer

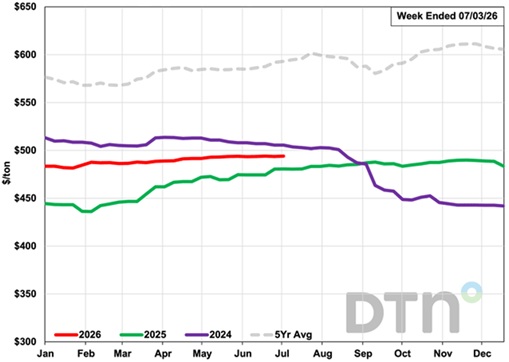

Global potash prices are up 12% YoY to $405/t (World Bank benchmark) vs the 10-year average of $380/t, driven by robust demand and a vulnerable global supply chain

U.S. retail potash prices (chart) are higher at $545/t primarily due to import-related transportation costs

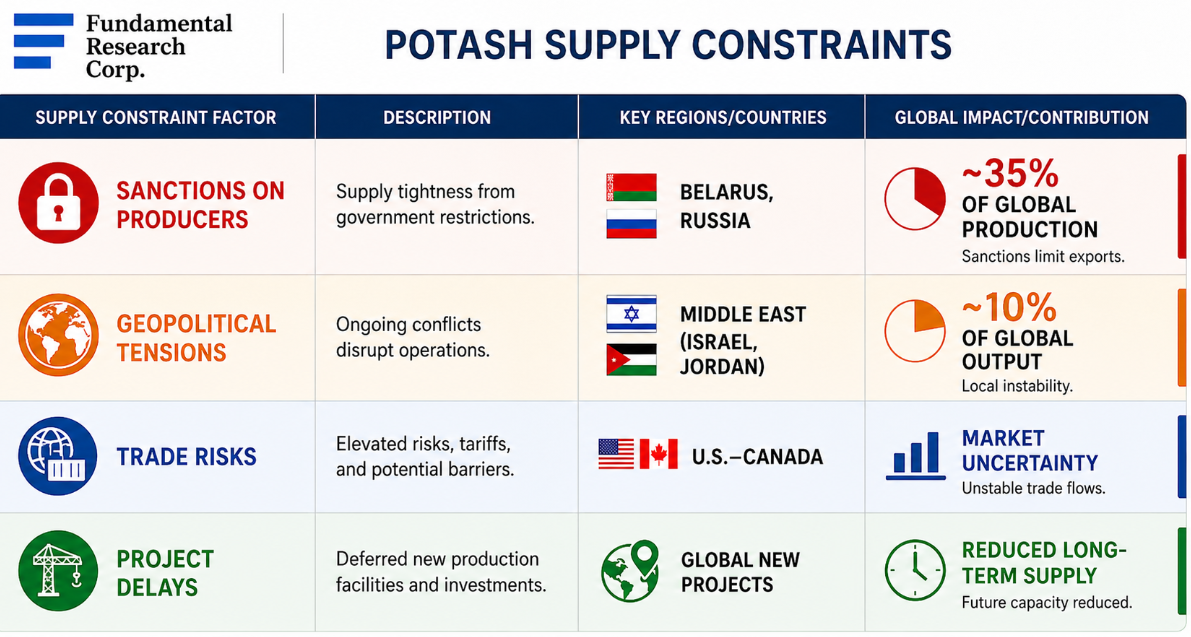

Geopolitical tensions and trade risks across key producing regions have created a highly vulnerable supply chain, which we believe will continue to support potash prices

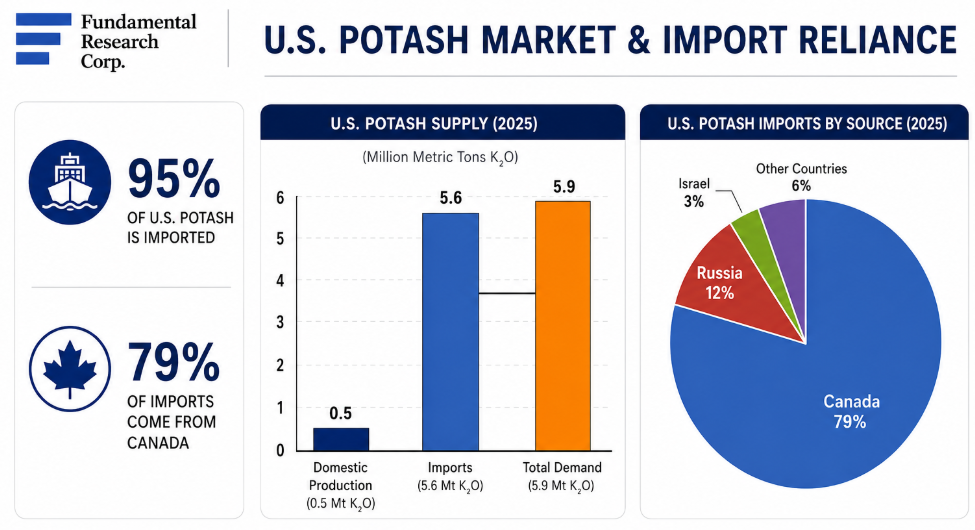

The U.S. imports >90% of its potash, with Canada supplying ~80%

The U.S. government allocated ~$26B in funding to 33 publicly listed critical mineral companies between 2023 and 2026. While most funding targeted U.S. projects, companies in Canada, Australia, Greenland, and Africa also received support. Notably, the U.S. International Development Finance Corporation (DFC) provided $4M to advance a potash project in Gabon, demonstrating its willingness to support strategic supply chains beyond U.S. borders. Given GSP's proximity to the U.S. border , and direct rail access, we believe the company is strategically positioned within this supportive policy environment.

Recognizing its import dependence, the U.S. added potash to its Critical Minerals List in 2025, and has since funded projects in the U.S. and Africa, underscoring the value of a secure North American potash supply

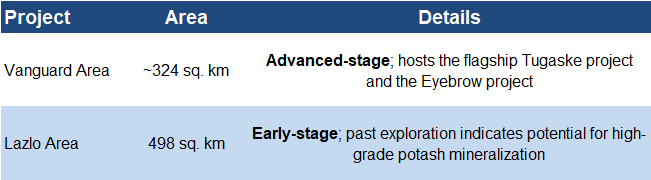

Portfolio Summary

GSP controls two potash areas in Saskatchewan

Source: FRC / Company / Various

Saskatchewan accounts for over 30% of global potash production and offers a rare combination of scale, high-grade deposits, and low-cost operations

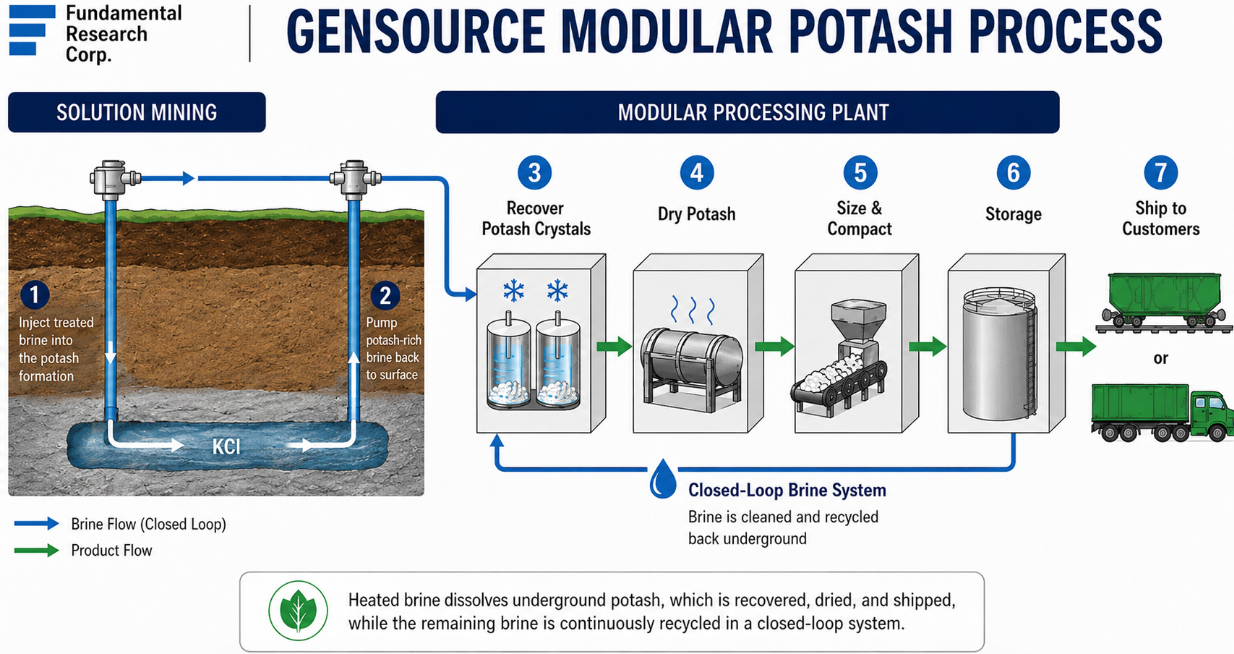

A Modular Approach to Potash Mining

GSP is utilizing a modular potash production model that we believe could potentially revolutionize the industry. Unlike conventional potash mines, which are built as large, multi-billion-dollar operations, GSP's model consists of smaller production modules that require significantly lower CAPEX and can be developed faster.

Source: FRC

GSP's modular model replaces traditional large-scale potash mining with smaller, lower-CAPEX operations

While this results in some loss of economies of scale, we believe it is more than offset by lower capital requirements, reduced execution risk, and greater scalability

Conventional potash projects are highly capital-intensive, relying on costly shafts, tunnels, and large processing plants. GSP aims to replace this traditional model with compact, modular production units instead of one large, centralized mine.

Source: FRC

GSP combines conventional solution mining with proprietary selective extraction and modular processing technologies

While the production process is largely similar to conventional operations, GSP differentiates itself through a compact, modular processing plant

Unlike conventional solution mining, which dissolves both potash and salt, GSP's process primarily dissolves potash while leaving most of the salt underground. This reduces processing requirements, lowers CAPEX and OPEX, and minimizes the environmental footprint by eliminating salt tailings and brine ponds. Production can be expanded incrementally by adding modular processing units as demand grows, reducing upfront capital requirements.

The modular production model has the potential to be replicated across other potash deposits with similar geology

Although the underlying technology and process are proven, GSP's modular production model has yet to be demonstrated at commercial scale. Therefore, the successful commissioning and operation of the first module will be an important milestone.

While GSP incorporates certain proprietary technologies, we believe its competitive advantage lies in its ability to execute a modular production model built on proven industry technologies, rather than in intellectual property that could be licensed to other producers.

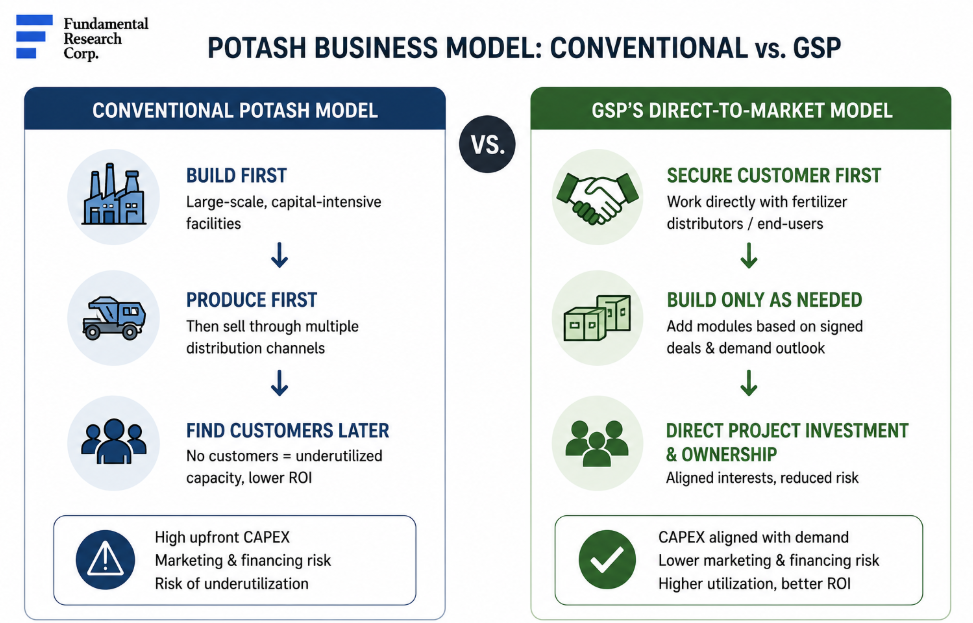

Direct-to-Market Strategy

Unlike conventional potash producers that build large, capital-intensive mines, and then market production through distribution channels, GSP follows a direct-to-market, build-to-suit strategy. The Company plans to work directly with fertilizer distributors and end-users, encouraging direct project investment , while adding production modules only as customer demand is secured. We believe this strategy aligns CAPEX with customer demand, reducing the financing, marketing, and underutilization risks common to conventional projects.

Source: FRC

Bypasses producer-controlled supply chains, allowing for direct project investment

GSP has already signed an exclusivity agreement with a large, undisclosed ASEAN conglomerate for a proposed two-module (500 Ktpa) project. We believe a definitive agreement would be transformational, potentially securing project funding, significantly de-risking the project, and accelerating its path to construction and production.

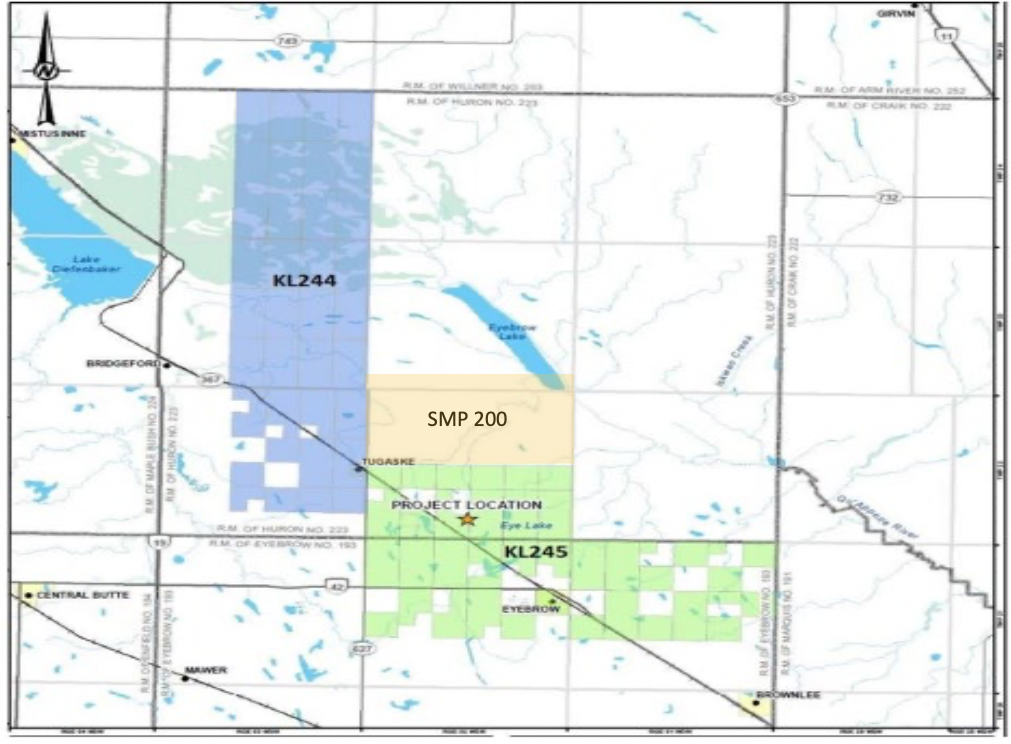

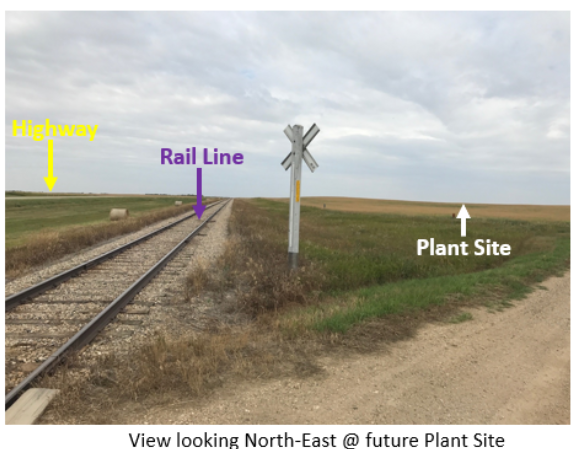

Tugaske Potash Project

Tugaske is GSP's flagship project, and the focus of this report. Located within the company's ~324 sq. km Vanguard property in south-central Saskatchewan, Tugaske ( ~35 sq. km) is fully permitted, having secured all required environmental, mining, and municipal approvals for a production facility. The remaining Vanguard land , and the c ompany's package in the Lazlo area , are at earlier stages of development.

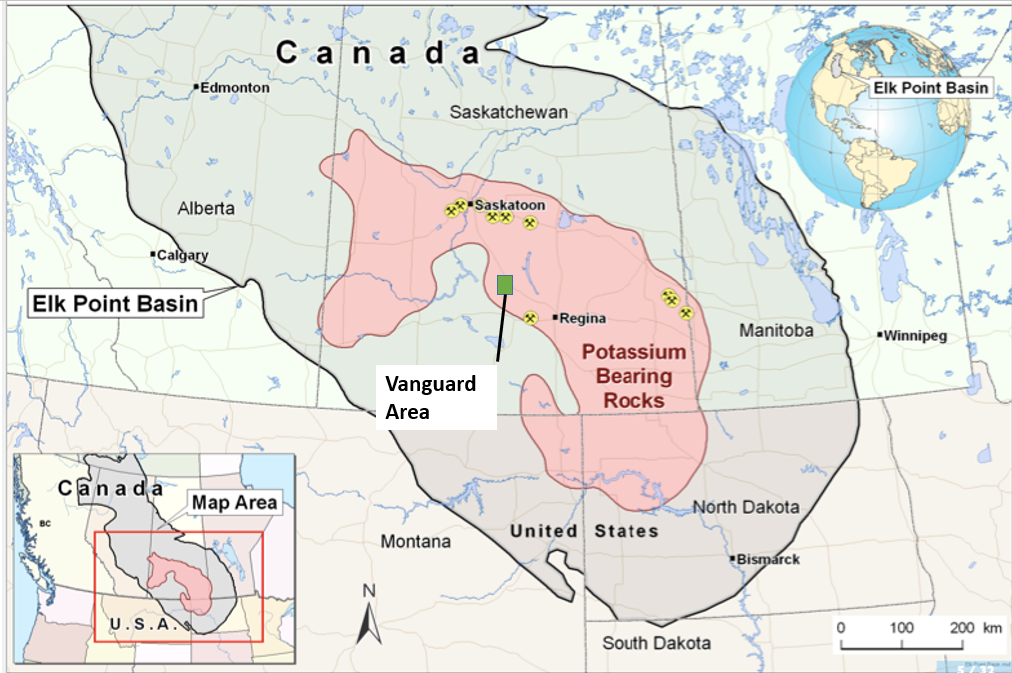

Project Location

Strategically Located: 360 km from the U.S. border, 170 km from Saskatoon, and 150 km from Regina, enhancing logistics and market access

Developed Infrastructure: Direct access to highways, rail, natural gas, water, and grid power, lowering capital requirements and development risk

Source: Company

Favorable Geology: Similar to major potash deposits in Saskatchewan, increasing confidence in exploration potential

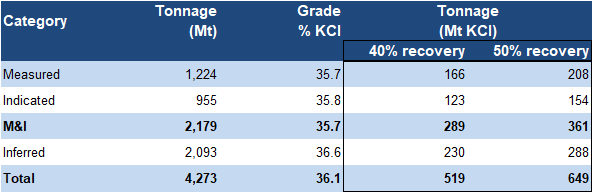

2021 Resource Estimate

The project hosts a high-grade resource, even by Saskatchewan standards, capable of supporting decades of production

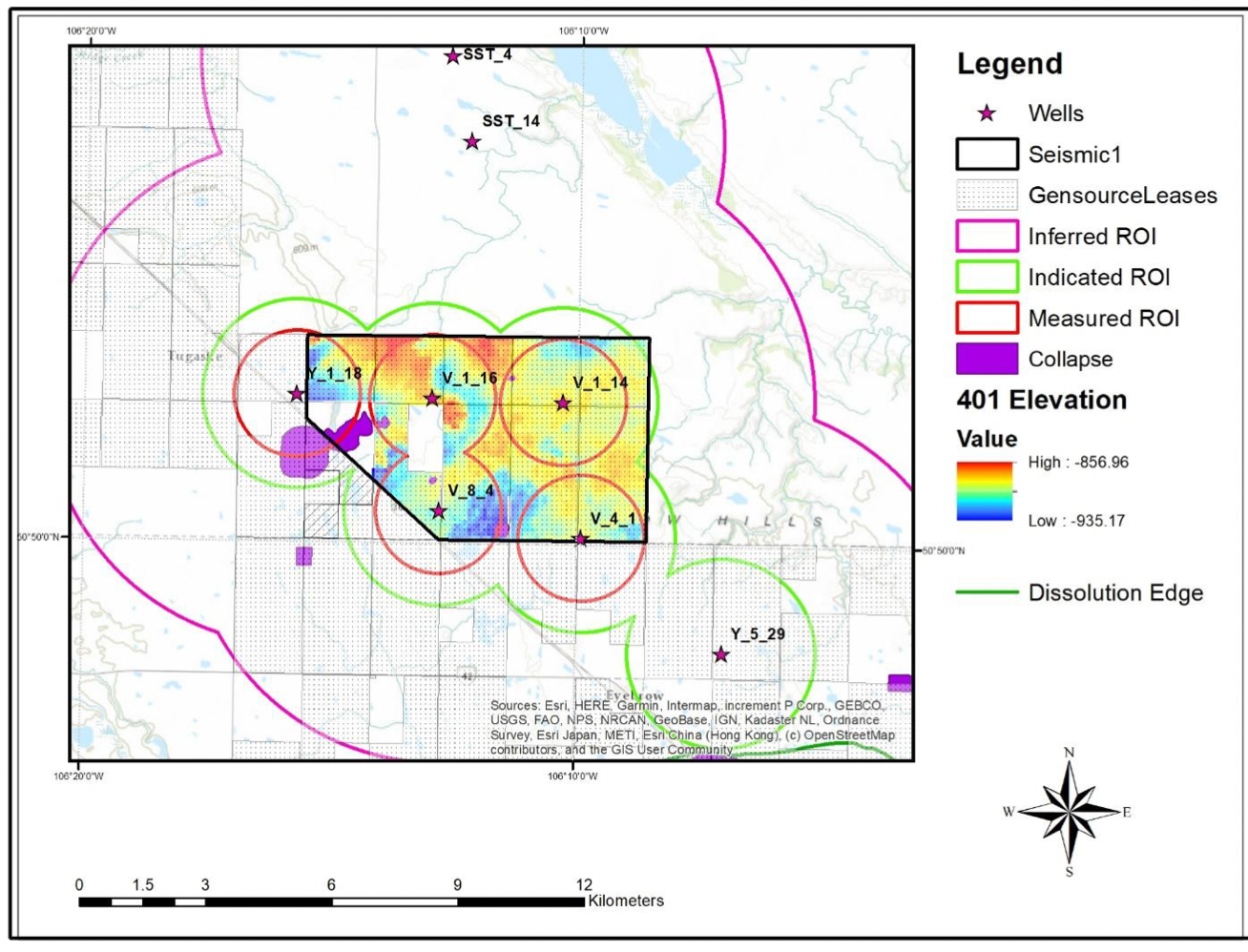

Resource Area

Source: Company

Only 10% of the 324 sq. km property has been included in the resource, leaving substantial exploration upside

The feasibility study is even more conservative, utilizing just 1% of the total KCl resources (14 Mt vs 1.5 Bt)

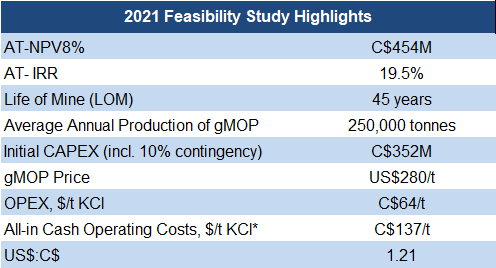

Following the resource estimate, GSP completed a feasibility study (an advanced independent evaluation) for a single 250 Ktpa modular operation. The project is designed to produce granular muriate of potash (gMOP), a premium form of MOP, the most widely used potash fertilizer.

A single 250 Ktpa module (45-year mine life) returned an after-tax NPV8% of $454M using a long-term gMOP price of $280/t (spot: $545/t)

*Including OPEX, Sustaining CAPEX and royalties

Source: 2021 Technical Report

Low costs (OPEX: $64/t; all-in cash costs: $137/t) suggest robust margins

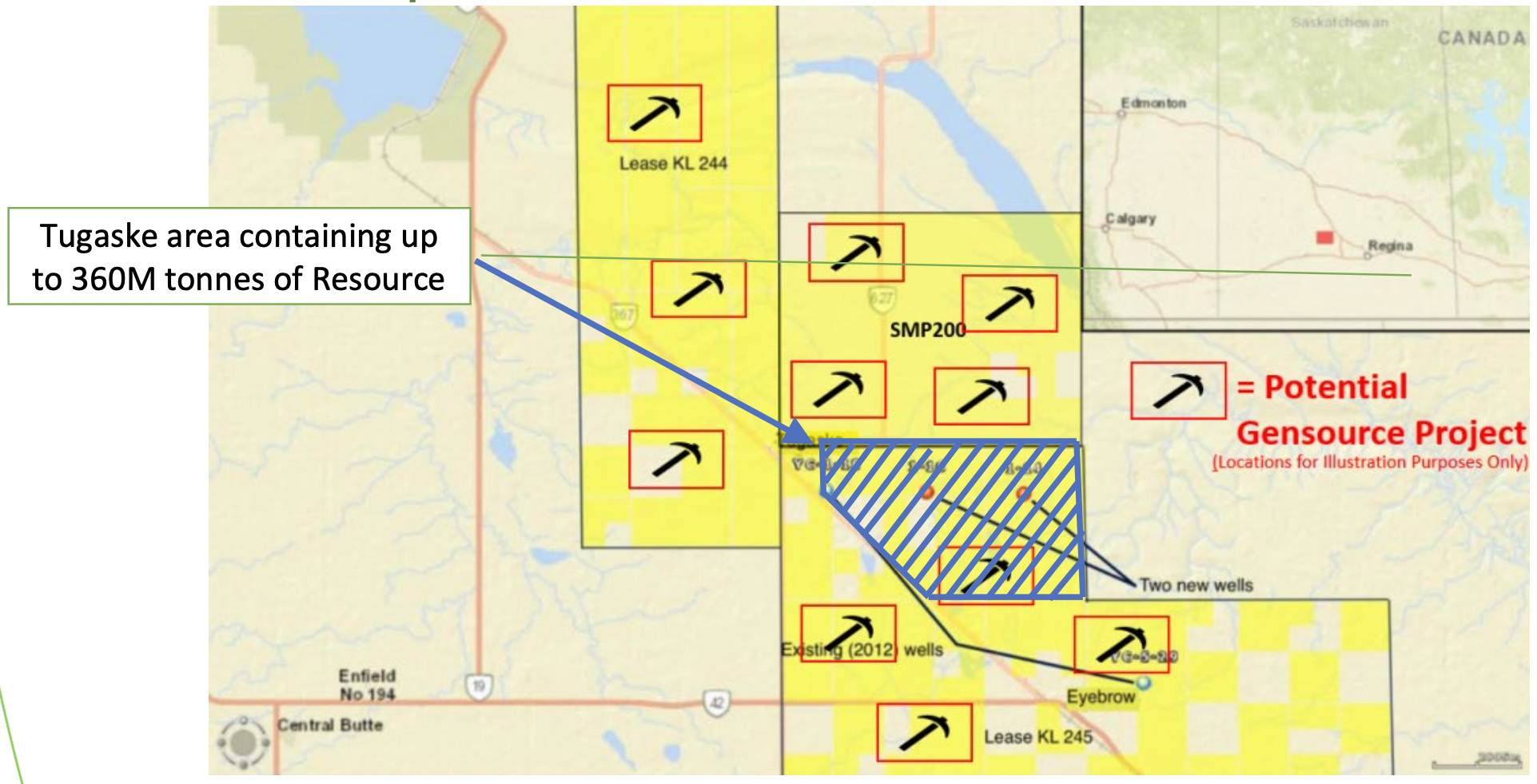

We believe the current resource can support 30+ modules; management is conservatively targeting 12, implying 3 Mtpa, already comparable to a large Saskatchewan potash mine

Production Expansion Potential

Source: Company

Applying the economics of a single module to 12 modules implies a potential after-tax NPV8% of $5.5B, vs GSP's current MCAP of just $57M, highlighting substantial upside potential

Development Plans

Shortly after completing the Feasibility Study, GSP signed a 250,000 tpa offtake agreement with Helm Fertilizers, a leading North American fertilizer distributor, validating the project's commercial potential.

In early 2026, GSP signed an agreement with a large, undisclosed ASEAN conglomerate, for a proposed two-module (500 Ktpa ) development. The proposed transaction includes long-term product offtake and potential full project funding, subject to definitive agreements and a final investment decision.

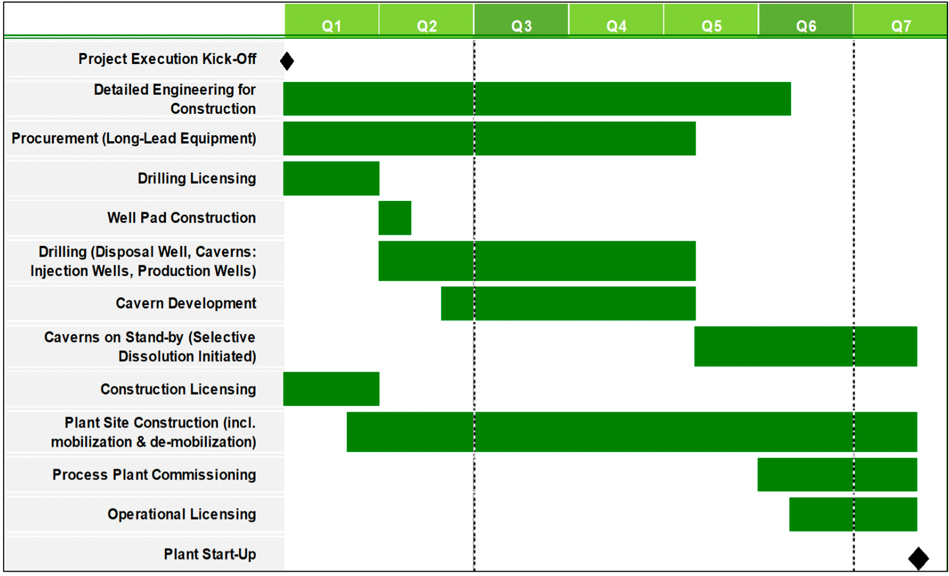

Project Implementation Schedule

The company aims to complete a technical update for a 500 Ktpa operation by Q4-2026, followed by a Financial Investment Decision (FID) by year-end

Source: Company

Subject to FID, GSP targets commercial production within two years

The partner has already advanced $0.85M to fund the technical update, providing an early indication of its commitment

Securing a definitive agreement would be a major validation of GSP's modular business model

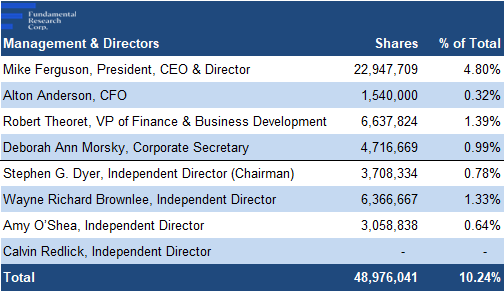

Management and Board

Source: S&P Capital IQ / FRC

CEO Mike Ferguson is GSP's largest shareholder (5% ownership)

Management and directors collectively own 10%, aligning their interests with shareholders

Brief biographies of the management team and board members follow:

Mike Ferguson, P.Eng. – President, CEO & Director: 25+ years of potash mining and project development experience in Saskatchewan. Led the development of Potash One's Legacy Project from exploration through feasibility and permitting, culminating in its acquisition by K+S Group. Brings rare, hands-on experience developing Saskatchewan's first greenfield potash project in over 40 years.

Three of four directors are independent

Alton Anderson, CPA, CA – CFO: 30+ years in the fertilizer industry, including 22 years at PotashCorp (now Nutrien ). Led global transformation initiatives across 16 operating sites spanning finance, supply chain, procurement, operations, and logistics. Recipient of multiple operational excellence awards.

Rob Theoret, B.Comm., CIM – VP, Corporate Finance & Business Development: 20+ years of capital markets experience. Co-founded NEXXT Potash, Gensource's predecessor, and has financed multiple junior resource companies. Extensive expertise in project financing, business valuation, and resource company development.

Led by a seasoned team with proven expertise in potash development, fertilizer operations, and capital markets

Deborah Morsky – VP, Corporate Services: 40+ years of executive leadership in corporate governance, finance, and restructuring. Extensive experience reorganizing public and private companies while overseeing corporate finance, operations, and governance.

Stephen Dyer – Board Chair (Independent): Former CFO and Senior Vice President of Agrium with 30+ years in agriculture. Led major corporate transactions, including Agrium's $1.8B acquisition of Viterra's retail assets, and managed a global retail business generating US$12B in revenue and US$1.1B in EBITDA.

Senior leadership experience at majors such as Nutrien and K+S provides GSP with significant operational and strategic credibility

Wayne Brownlee – Independent Director: Former Executive Vice President and CFO of PotashCorp and Nutrien . Played a key role in PotashCorp's privatization and growth into a global fertilizer leader, overseeing major acquisitions and a US$6B asset divestiture.

Amy O'Shea – Independent Director: CEO of Invaio Sciences and CEO Partner at Flagship Pioneering, with over 27 years in the agricultural sector. Former Vice President and Business Director, North America Agricultural Solutions at FMC Corporation.

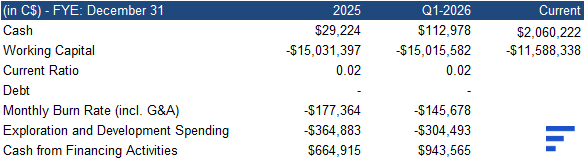

Financials

Post-Q1, GSP raised $2.5M in equity, and reduced debt by $1.5M through share issuances, improving its working capital deficit from ($15M) to ($11M)

While much of the working capital deficit relates to project partners and may be renegotiated, the next six months will be critical as the outcome of discussions with the ASEAN partner could unlock significant project funding

Source: FRC / Company

FRC Valuation & Rating

Source: FRC

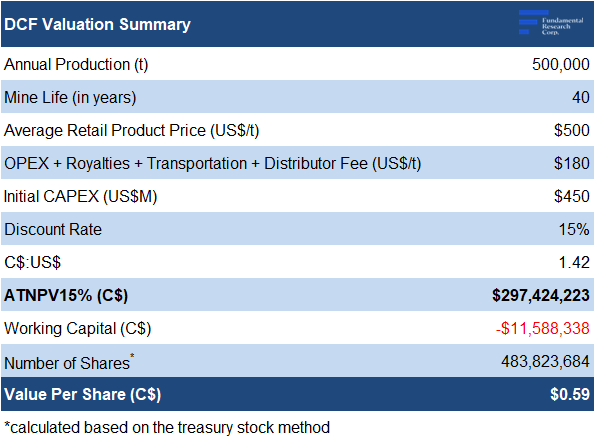

Our DCF valuation, based on a 500,000 tpy operation, yields a fair value estimate of $0.59/share

Our model adopts a conservative long-term potash price ($500/t vs $545/t spot) and CAPEX/OPEX estimates above the 2021 feasibility study to account for sector-wide cost inflation

We use a 15% discount rate (vs. our typical 12%) to reflect development and financing risks. A definitive partnership agreement could lower this risk , and increase our valuation.

Source: FRC

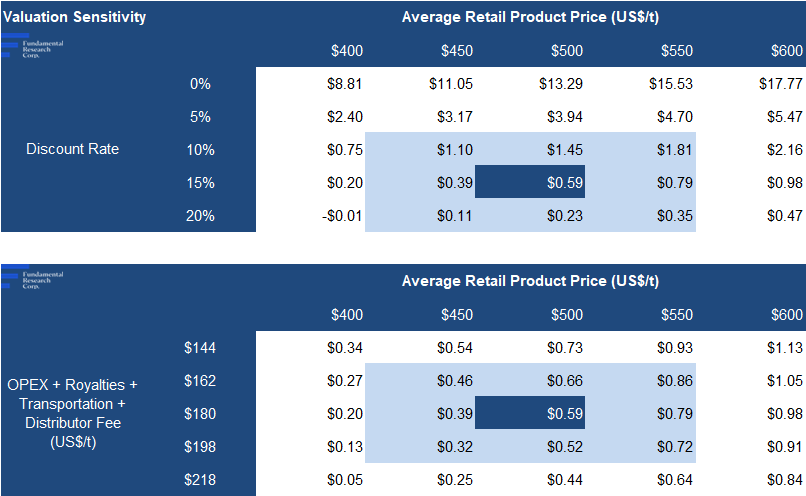

As with any mining project, our valuation is highly sensitive to changes in key inputs

We rely solely on our DCF valuation, as there are no comparable modular potash operations

We are initiating coverage with a BUY rating, and a fair value estimate of $0.59/share. We believe GSP's key strengths are its high-grade asset, differentiated modular business model, experienced management team, and the potential to bring production online faster and with significantly lower upfront CAPEX than conventional potash projects. While execution and financing remain key risks, a definitive agreement with the ASEAN partner could be a game-changing catalyst.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- The value of the company is dependent on potash prices

- Securing project financing and strategic partners

- Potential for delays in permitting, financing, and construction

- Modular production model yet to be proven at commercial scale

- Future equity financings could dilute existing shareholders.

- Failure to secure or maintain long-term offtake agreements

We are assigning a risk rating of 5 (Highly Speculative)