Disclosure: Graphite One Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

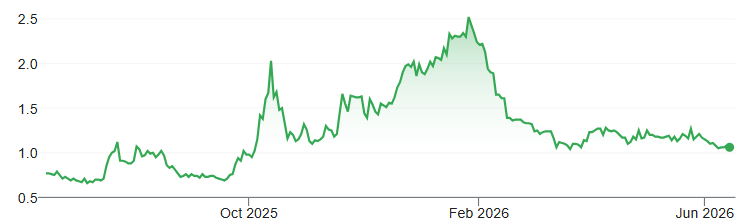

Price and Volume (1-year)

*Sprott Critical Materials ETF

* Qualified Person: Robert M. Retherford, P.Geo., an Independent Consultant of Graphite One Inc. (GPH). Graphite One Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in US$ except share price, MCAP, and fair value.

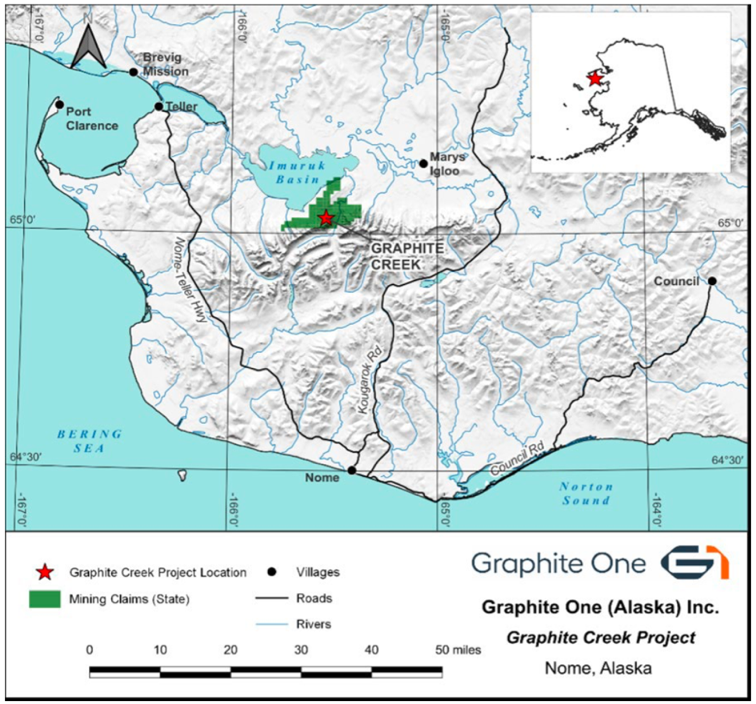

Graphite Creek is located 60 km north of Nome, Alaska; seasonal port access

Project Location

A remote site with no current road or grid power access

Access planned via a new road connecting to the Nome–Teller highway

to support future mining operations

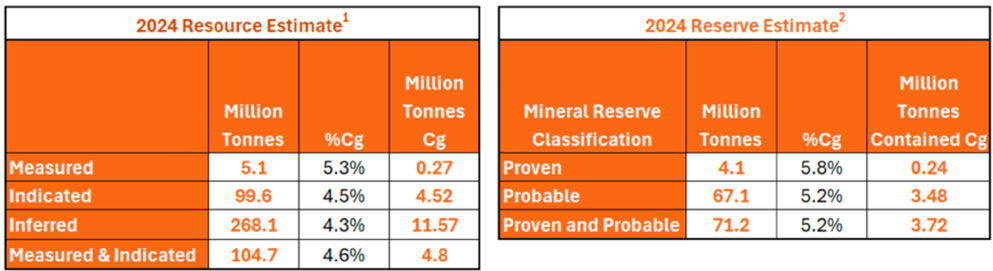

2024 Resource Estimate

Power to be supplied by diesel generation; water sourced from nearby rivers and streams

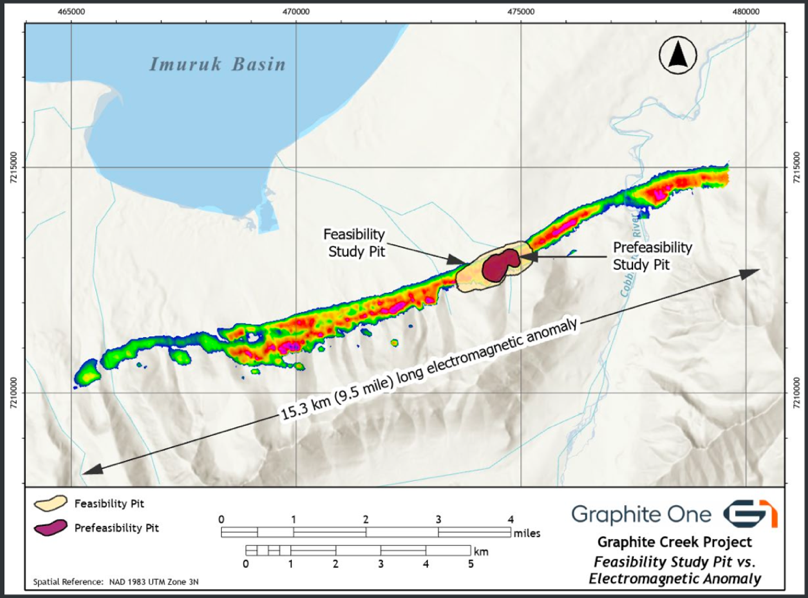

Proposed Pit Overlaying Electromagnetic (EM) Anomaly

Source: Company

Graphite Creek is the largest known graphite deposit in the Americas; only 12% of a 15.3 km mineralized zone has been fully tested, leaving significant room for resource growth

Source: FRC

A mine-to-market supply chain linking Graphite Creek with a planned Ohio facility producing Active Anode Material (AAM)

2025 BFS Highlights

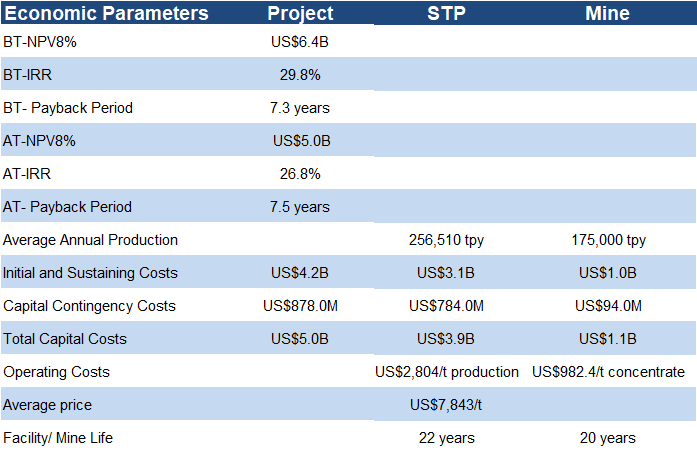

A 2025 Bankable Feasibility Study, based on a 20 year mine life, returned an after tax NPV8% of $5B

Source: Company / FRC

GPH's $152M enterprise value implies its shares trade at just 3% of the project's independent valuation

Like most large-scale mining projects, development is capital intensive, with initial CAPEX estimated at $4B, including $1B for the mine, and $3B for the Ohio STP

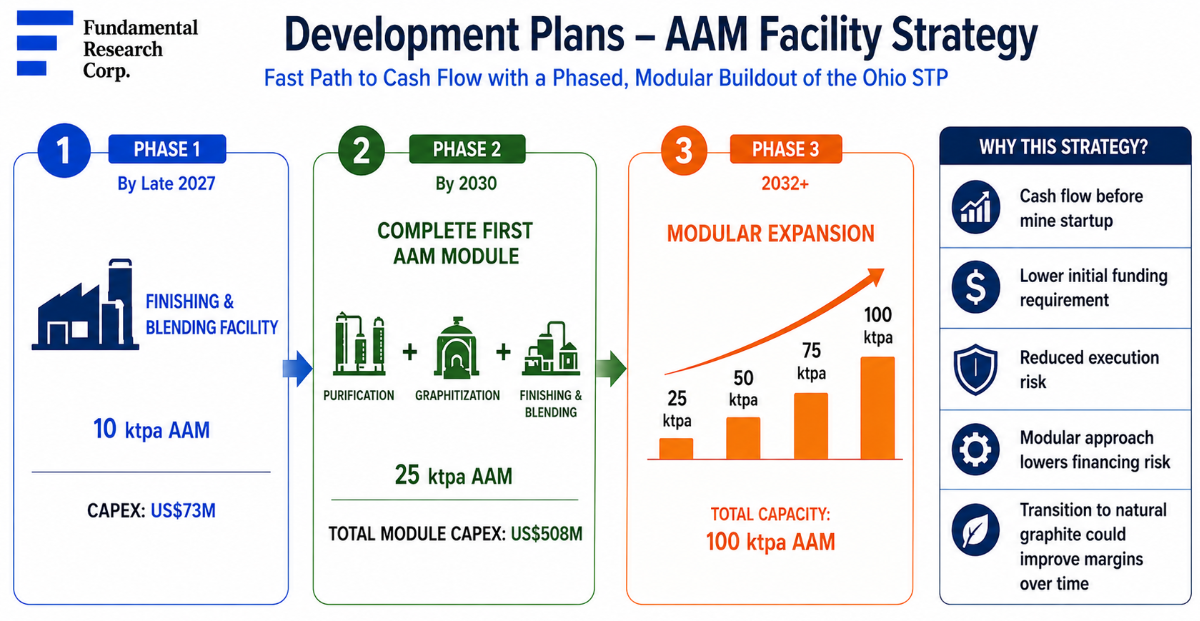

Phased Development Strategy to Accelerate Cash Flow

Given the significant capital required to develop the fully integrated Graphite Creek project, management is pursuing a phased strategy to accelerate cash flow, and reduce financing risk. While advancing Graphite Creek toward potential production by 2030, GPH plans to prioritize the construction of its Ohio STP, initially sourcing graphite from external suppliers before transitioning to feedstock from Graphite Creek once the mine enters production.

Source: FRC

We believe the modular approach enables gradual production growth while significantly limiting upfront CAPEX ($73M vs $4B)

GPH plans a modular buildout, with each module capable of producing 25 ktpy of AAM. An AAM module includes three key processes: Purification, Graphitization, and Finishing & Blending. Rather than building the full module upfront, GPH intends to start with a 10,000 tpy Finishing & Blending facility requiring just $73M in CAPEX, and targeted for completion by late 2027. The remaining processes would be added over time, creating a lower-risk pathway to full-scale production.

Funding Agreements & Endorsements

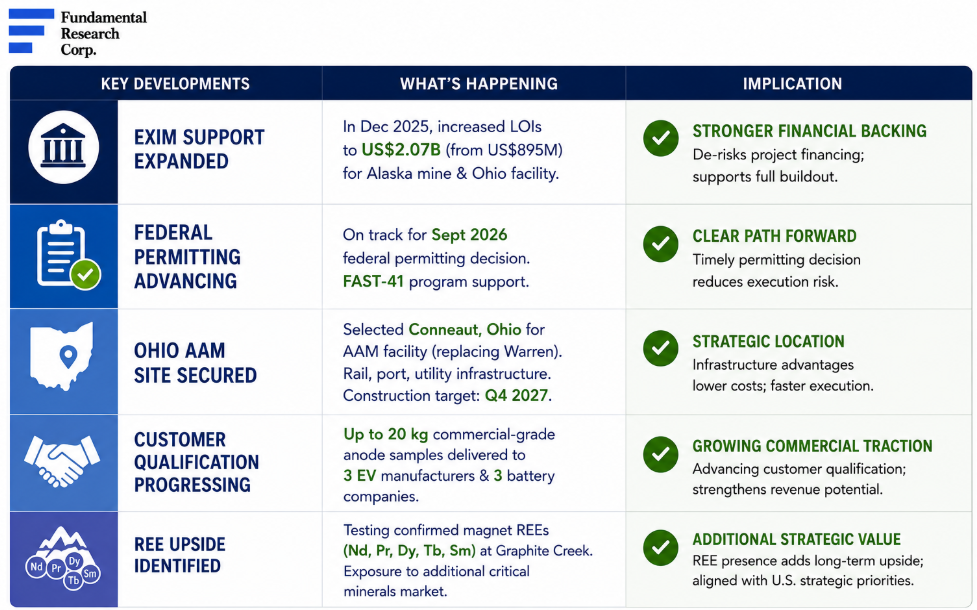

While the company’s strategy involves multiple stages and execution milestones, including permitting, it continues to receive strong support from industry and government entities, providing validation of the business plan and confidence in its execution.

Source: FRC

GPH has secured a mix of strategic agreements, grants, and investments from industry partners, government bodies, and native corporations

To date, three of the 12 local native groups have invested in GPH, underscoring strong community support

Recent Developments

Source: FRC

Since our October 2025 report, GPH has strengthened financing support, selected a site for its Ohio facility, and identified rare earth element mineralization at Graphite Creek, though exploration remains at an early stage

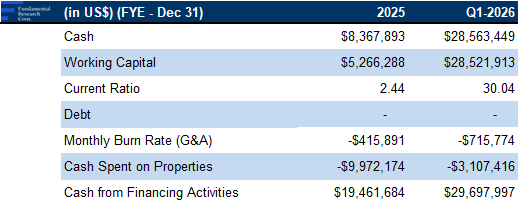

Financials

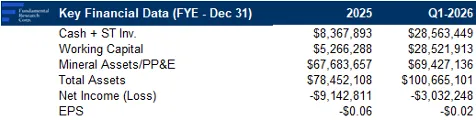

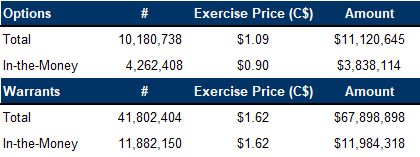

Strong cash position, with $29M in cash, and up to $11M from in-the-money options and warrants

Ohio facility construction is targeted for Q1-2027, with EXIM funding up to 70% of CAPEX, and the balance potentially via equity or lease financing

Source: FRC / Company

FRC Valuation & Rating (all figures in C$)

Source: S&P Capital IQ / Various / FRC

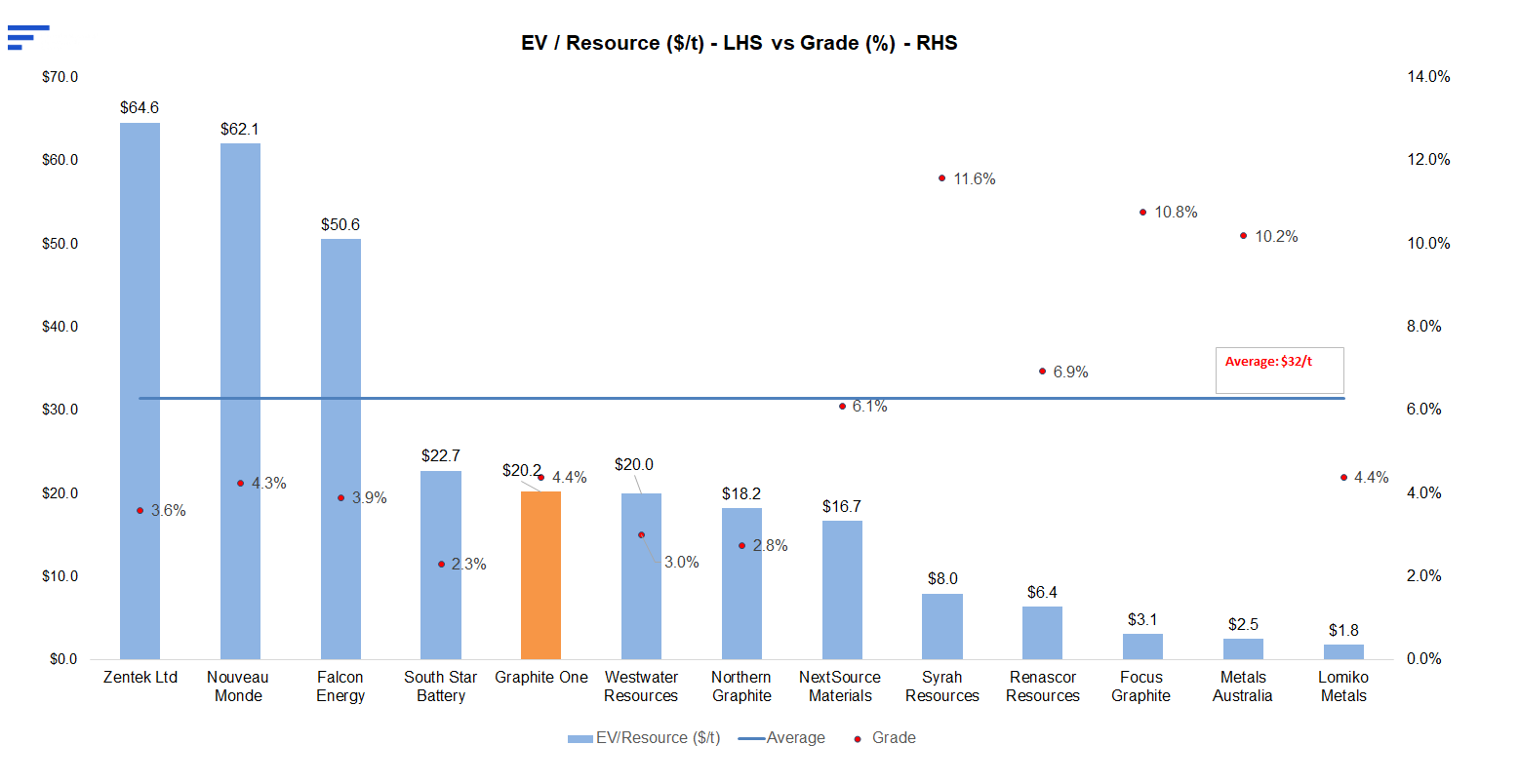

GPH is trading at $20/t (previously $28/t), compared with the sector average of $32/t (previously $40/t), a 36% discount

Applying the sector average yields a comparables valuation of $1.61/share (previously $2.20/share), reflecting lower sector multiples and share dilution since our previous report

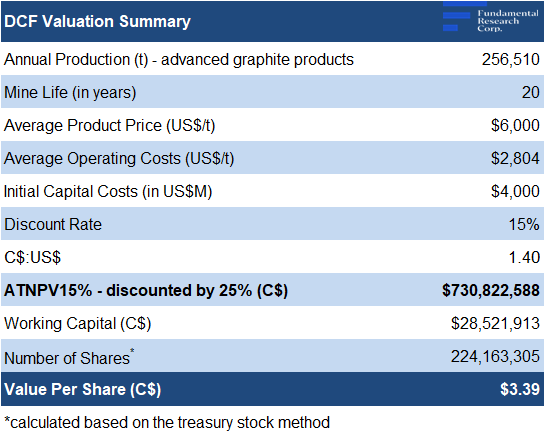

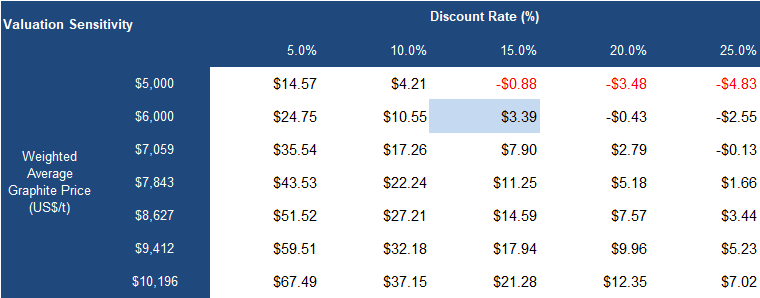

Our DCF valuation declined to $3.39/share from $3.50/share, primarily due to share dilution

Source: FRC

We reiterate our BUY rating, and adjust our fair value estimate from $ 2.85 to $2.50 /share. We believe GPH is well positioned to become a U.S. supplier of graphite and battery materials, supported by strong government backing. Despite this progress, its shares continue to trade at a significant discount to comparables and project NPV.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining our risk rating of 5 (Highly Speculative)