Disclosure: Rocket Doctor AI Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

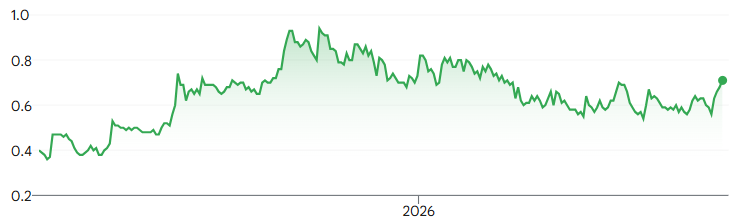

Price and Volume (1-year)

* Rocket Doctor AI has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

Company Overview

B2C: Physician-Funded Model (Primary Revenue Driver)

B2B: Institutions license AI tools for training and care

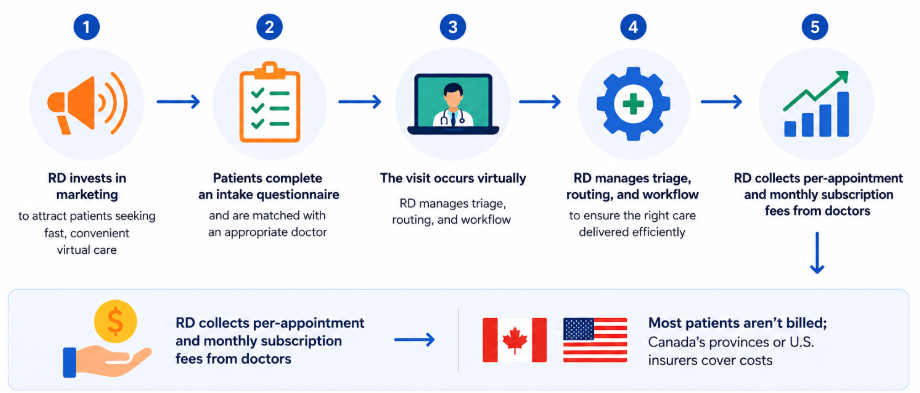

The Rocket Doctor Process

Source: FRC

Offers a streamlined virtual care experience from patient intake to payment

Generates revenue from doctors through monthly subscriptions and per-appointment platform fees

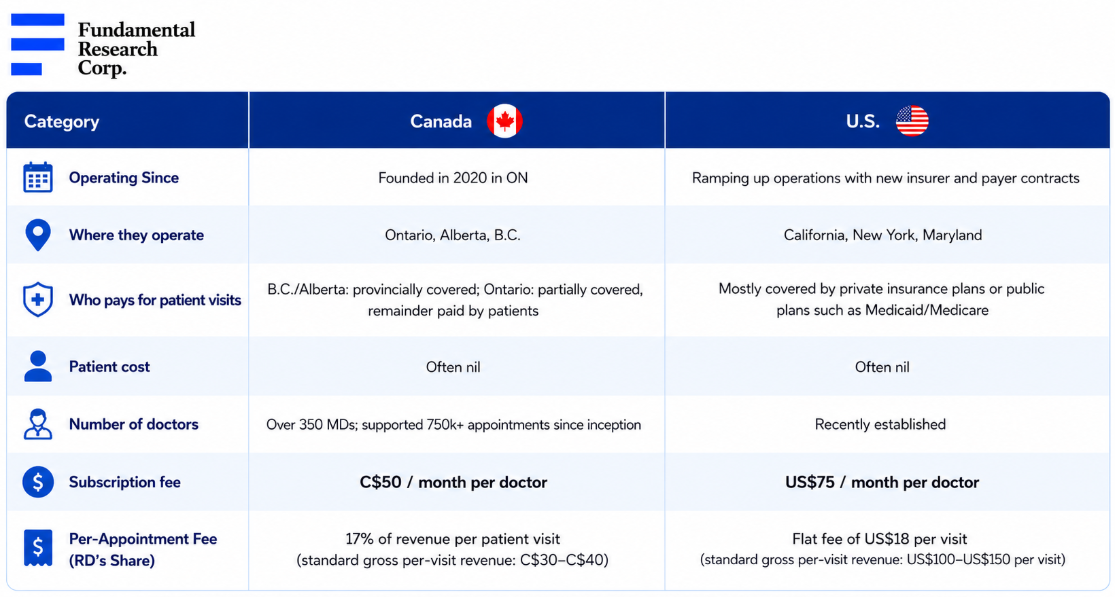

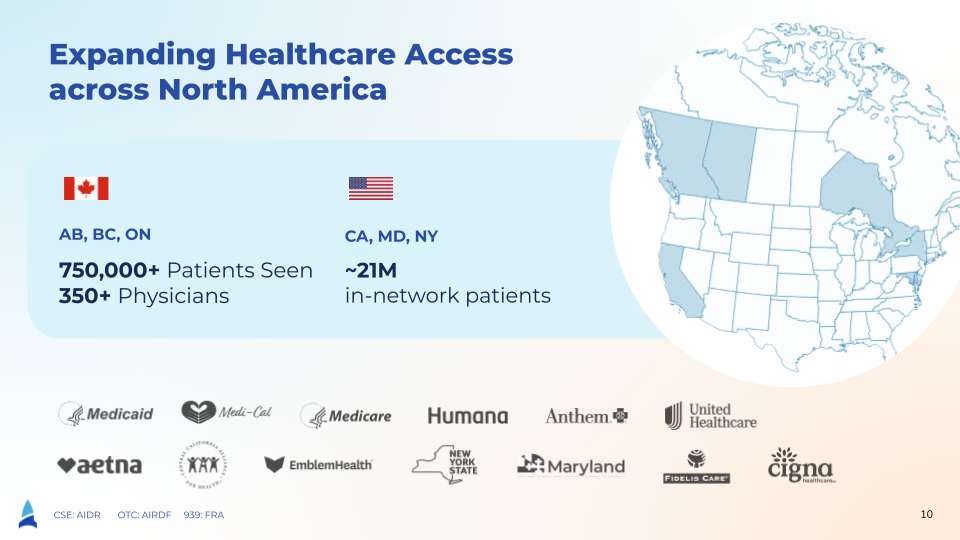

Target Markets

Source: FRC / Company

Operating in Canada since 2020; currently focused on U.S. expansion

RD’s current target pool includes ~46M people across its target regions in the U.S. and Canada

Source: Company

Primarily targets patients using government-funded health insurance (provincial in Canada and Medicaid / Medicare in the U.S.)

Partnerships with ~20 insurers in the U.S.

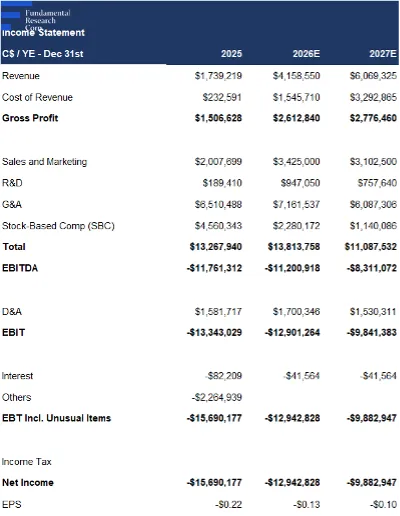

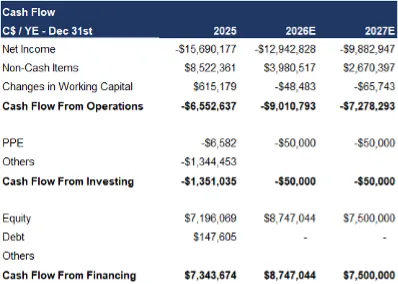

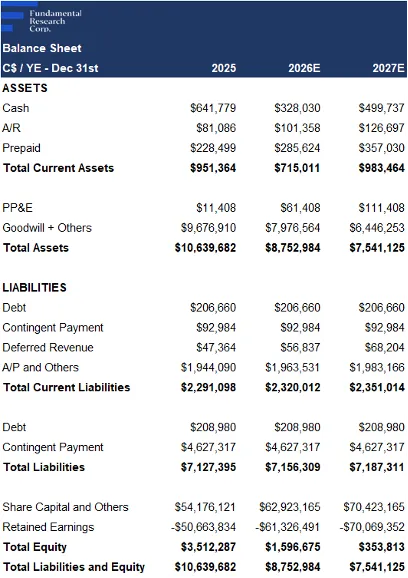

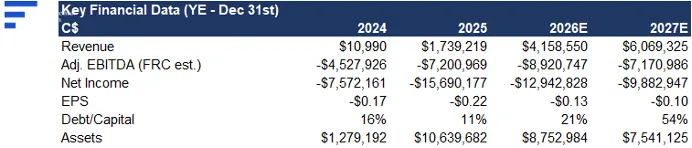

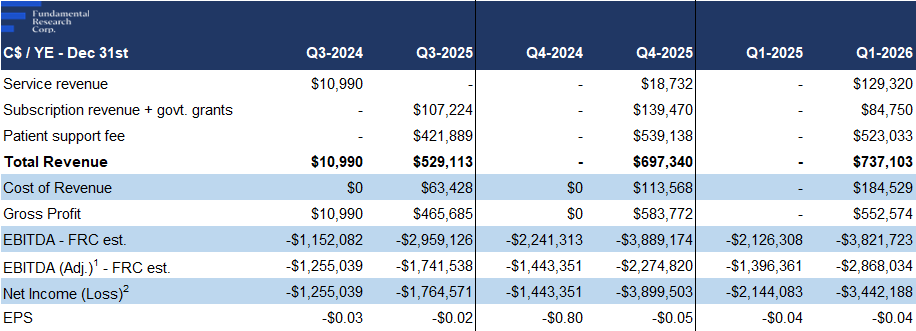

Financials

Q1- 2025 and Q1-2026 results are not comparable, as material revenue commenced only after the Rocket Doctor acquisition in April 2025.

1.Excluding stock-based compensation (SBC) / 2.Excluding unusual items + SBC

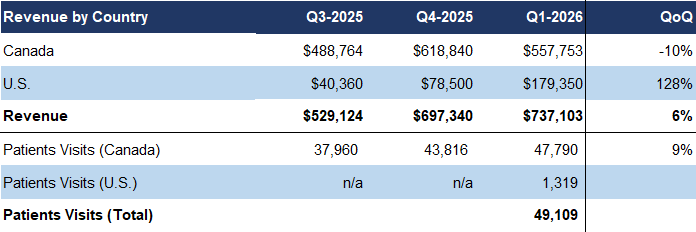

Q1 revenue of $0.74M (+6% QoQ), continuing sequential growth; 14% below our estimate

Growth driven by higher patient volumes; Canadian visits up 9% QoQ and 24% YoY to ~48k

U.S. visits were ~1.3k vs negligible activity in Q4-2025

Strong Q2 momentum: April U.S. visits of ~1.1k, up 160% from the Q1 monthly average (~0.4k)

The above table shows a QoQ decline in Canadian revenue in Q1-2026. However, Q4-2025 benefited from unusually high government grant revenue. Excluding grants, management indicated that Canadian revenue would have continued to grow sequentially.

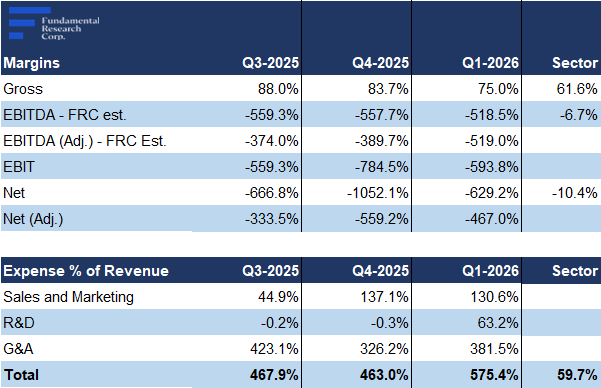

Gross margins declined QoQ to 75% from 84%, primarily due to the growing contribution of U.S. operations rather than any structural change in the business model. In the U.S., the company records the full revenue per patient visit as revenue, and physician fees as direct costs, resulting in gross margins of approximately 15–20%. In Canada, revenue is reported net of physician payments, resulting in gross margins of 85–90%.

The difference in reporting stems from the payment flow: in the U.S., insurers pay RD directly, which then compensates physicians, while in Canada, physicians receive reimbursements directly from provincial healthcare plans , and pay RD service fee.

Operating expenses were 34% above our estimate, reflecting our underestimation of costs associated with integrating and scaling Rocket Doctor

Adjusted EBITDA weakened QoQ on higher OPEX, while EPS improved on lower depreciation expenses; both remained negative

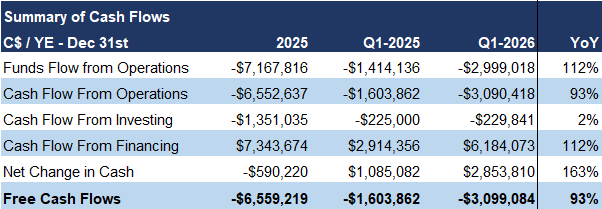

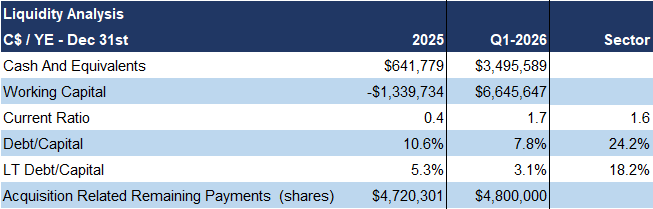

Ended Q1 with $3.50M cash, and minimal debt

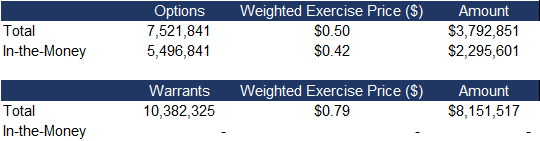

We estimate the company will require ~$2.5M in additional funding this year; however, in-the-money options could generate up to $2.3M in proceeds, likely eliminating the need for a significant equity financing

Source: FRC / Company

FRC Valuation and Rating

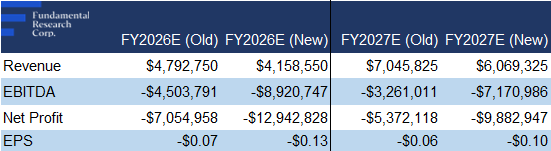

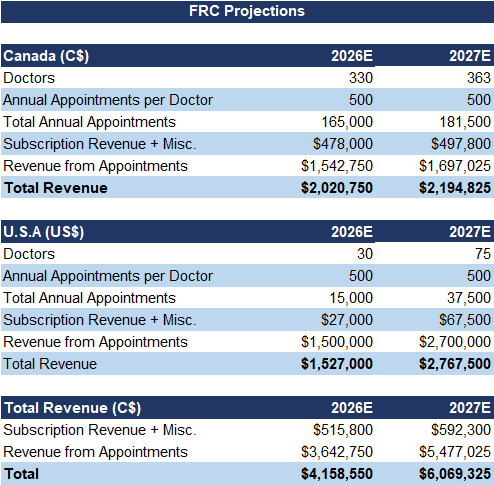

Given higher-than-expected Q1 expenses, we are lowering our 2026 and 2027 EPS forecasts; we are lowering our revenue estimates as well

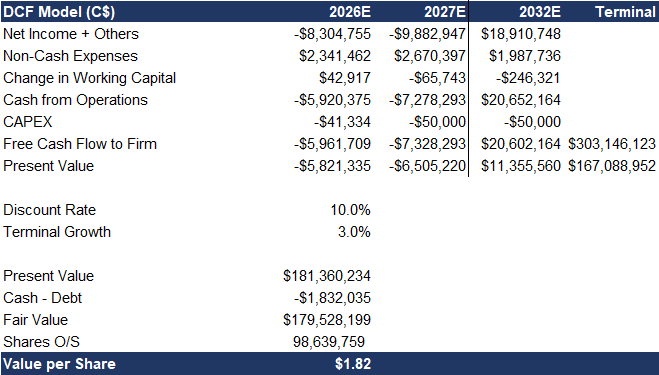

As a result, our DCF model returned a fair value estimate of $1.82/share (previously $1.96/share)

Source: FRC

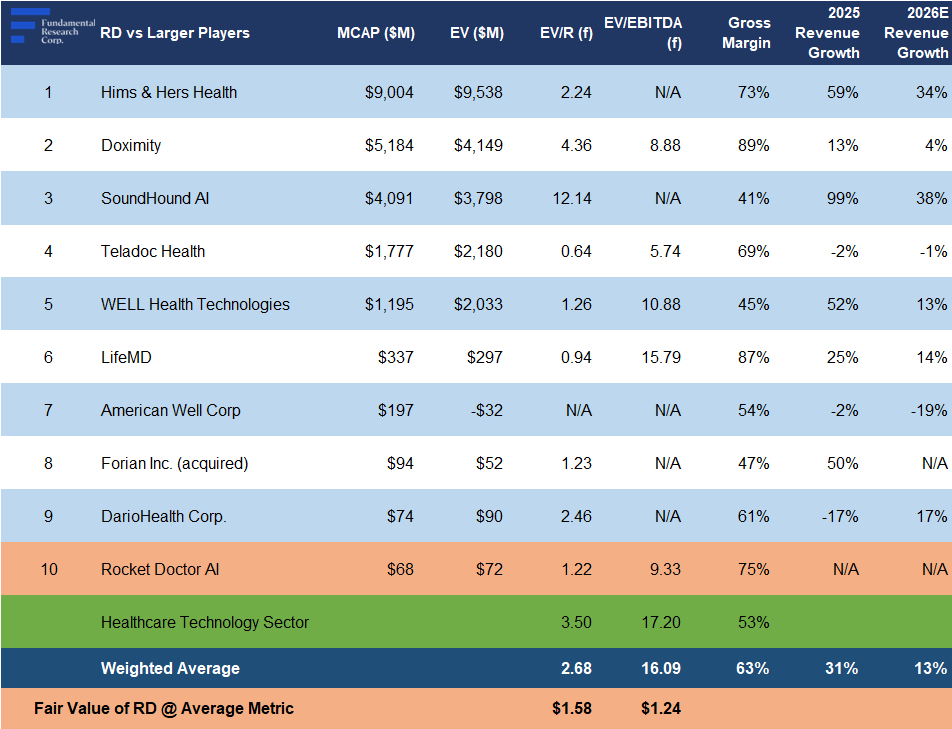

Comparables Valuation

*We use the present value of our 20 30 EBITDA estimate for RD in this calculation.

Source: FRC / S&P Capital IQ

RD is trading at 1x forward revenue vs the sector average of 3x, a 54% discount

RD is trading at 9x forward EBITDA vs the sector average of 16x, a 42% discount

Our comparables valuation declined to $1.41/share from $1.75/share, primarily due to our lower revenue and EBITDA forecasts

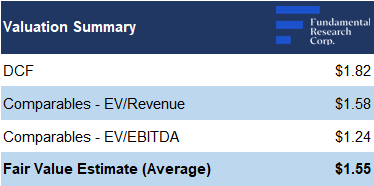

We reiterate our BUY rating, and adjust our fair value estimate from $1.86 to $1.55/share (the average of our DCF and comparables valuations). While Q1 results were impacted by higher costs and lower-than-expected patient volumes, we believe underlying growth trends remain intact. Supported by U.S. expansion, rising patient volumes, and sufficient liquidity, we expect meaningful operational and financial improvement over the coming quarters. The current valuation discount to peers does not, in our view, fully reflect its growth potential.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining a risk rating of 4 (Speculative)

APPENDIX