Disclosure: Klondike Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Risks

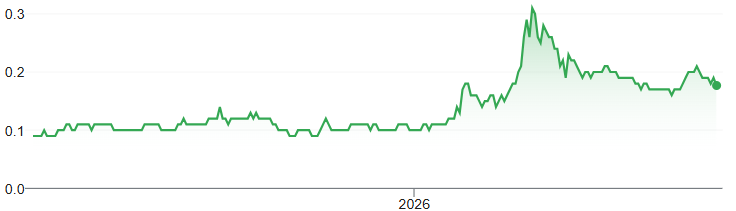

Price and Volume (1-year)

*QP: Peter Tallman, P.Geo., President of Klondike Gold Corp. Klondike Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ except for metals prices, which are in US$.

Developing the 729 sq km Klondike district project in the Yukon’s Klondike Goldfields, a prolific gold district with limited modern exploration below shallow depths

Portfolio Overview

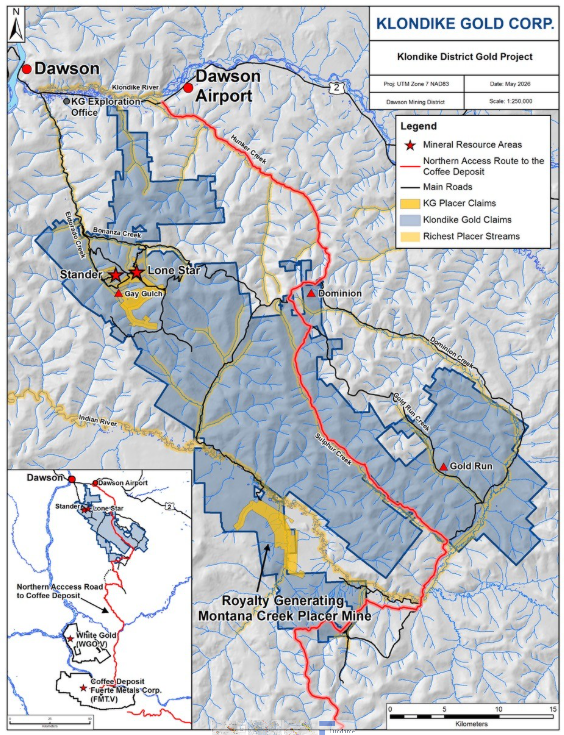

Project Locations

Source: Company

Royalty interest in the producing Montana Creek placer mine, located along the southern edge of the Klondike property, with ~$9M in expected royalty revenue over the next five years

Klondike District Gold Project (100% interest)

Overview

Located in the Yukon's historic Klondike Goldfields, the 729 sq. km project covers the 1896 Klondike Gold Rush district, one of the most significant gold discoveries in North American history.

The Yukon hosts several producing mines and advanced gold projects

The district has produced 20+ Moz of placer gold (gold recovered from riverbeds and surface gravels), but has never hosted a large-scale gold mine.

Infrastructure

Source: Company

Located 20 km south of Dawson City, a mining hub in the Yukon

We believe year-round road access, hydro power, water resources, and proximity to Dawson City, support project development

History, Mineralization and Resources

After consolidating the district in 2014, KG completed extensive exploration and drilling programs, culminating in the project's first independently verified (NI 43-101 compliant) resource estimate in 2022. The resource is based on hard-rock gold mineralization, the source of the district's historic placer gold production.

Prospective for orogenic gold systems, which can host large, high-grade gold deposits

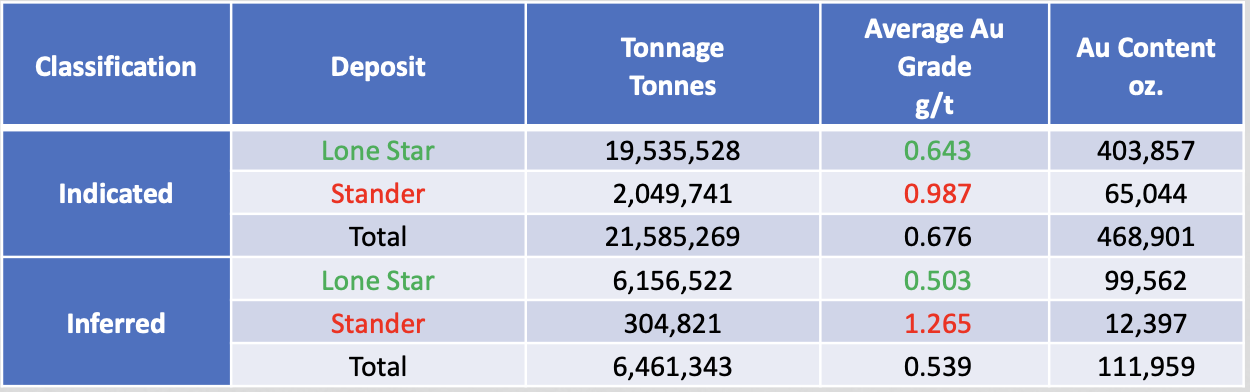

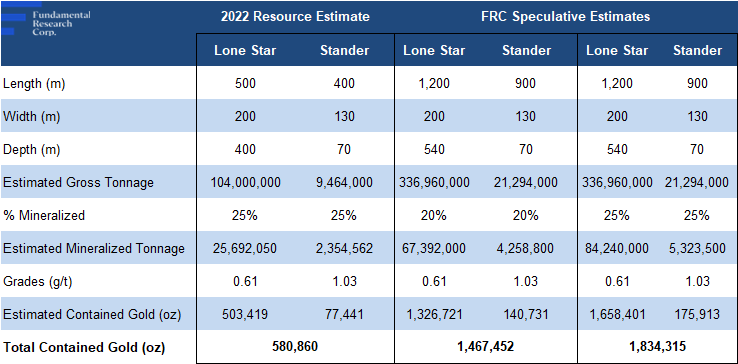

2022 Resource Estimate

Source: Company

The maiden resource estimate defined 581 Koz of gold across two targets - Lone Star and Stander

While this provides a promising initial resource base, we believe further resource growth is needed to support the economics of a future mine

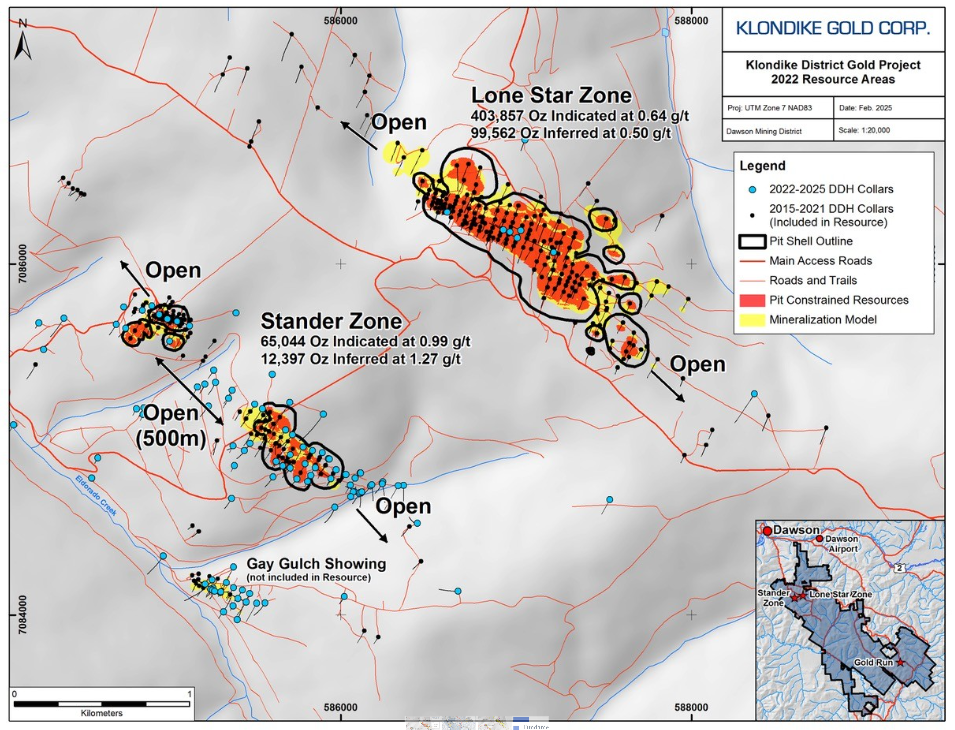

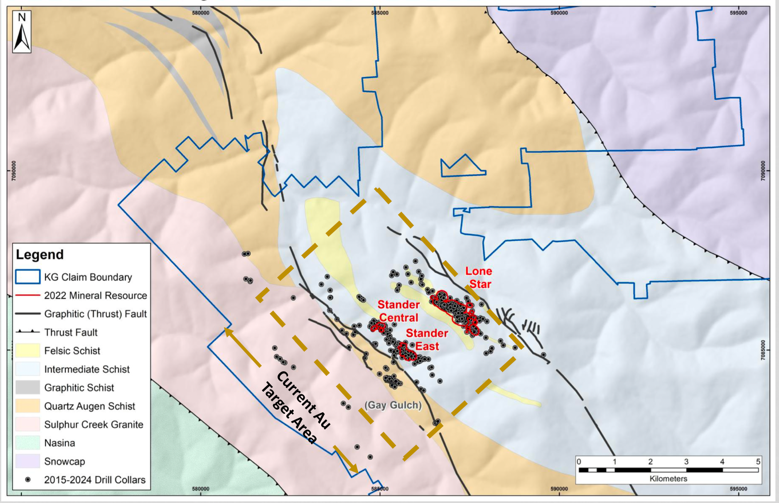

Two Defined Targets

* Red represents the high-grades areas within the planned open pits, while yellow shows the broader mineralized zones.

Source: Company

Lone Star and Stander are located ~0.5 km apart, and could potentially be developed as an open-pit operation, a generally lower-cost mining method

Lone Star hosts 92% of the resource, while Stander has significantly higher gold grades (1.03 vs 0.62 gpt gold)

The weighted average grade of 0.65 g/t is within the typical range for open-pit gold mines

Resource Expansion Potential

Extensive Drill Programs

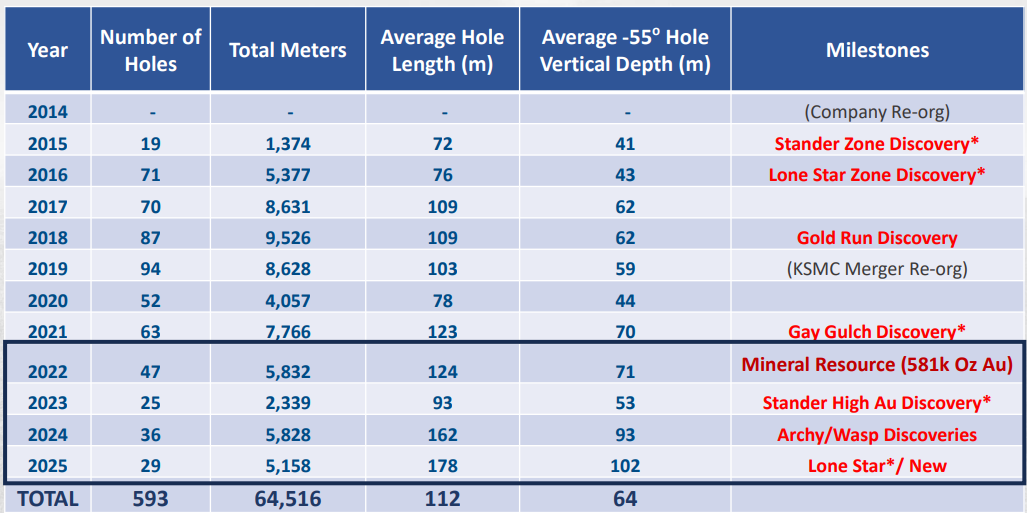

Since the 2022 resource, KG has completed 137 drill holes (19,157 m)

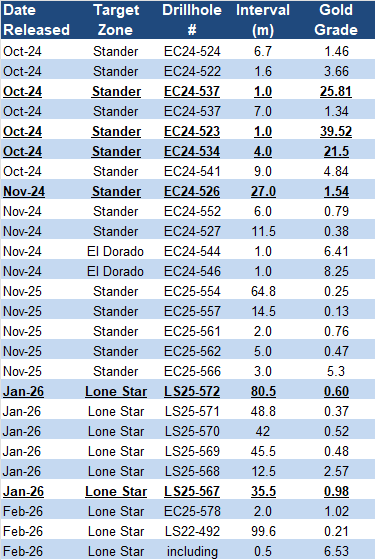

Post-Resource Drill Highlights

Source: Company/FRC

2022-2025 drilling extended known mineralized zones, and closed a 0.5 km gap between the two pits at Strander, potentially supporting future resource growth

FRC Preliminary/Speculative Estimates

Based on recent drilling and current mineralized zone dimensions, we believe Lone Star and Stander could host 1.5–1.8 Moz Au, 150–215% above the 2022 resource estimate

Source: FRC

Assumes 20–25% mineralization vs ~25% in the 2022 resource model

Resource Expansion Potential

Source: Company

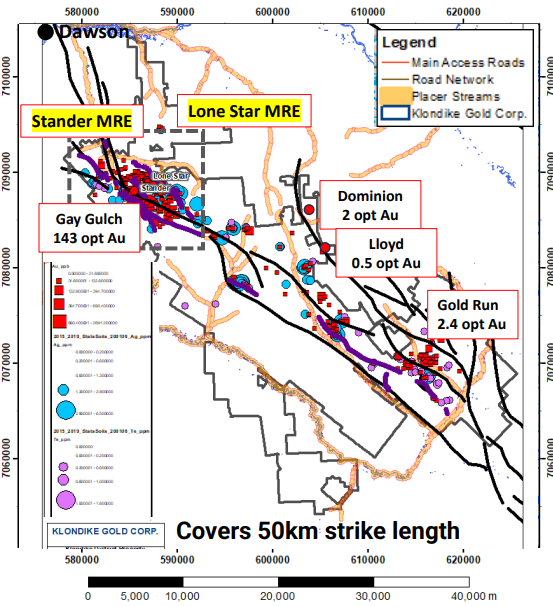

Beyond Lone Star and Stander, additional targets such as Gay Gulch, Dominion Zone, and Gold Run, offer potential exploration upside, although they remain largely untested

Surface sampling returned high-grade gold values of up to 4,064 g/t across these targets

Lone Star and Stander cover less than 5% of the project's 50 km prospective strike length

2026 Drill Targets

* Gold dashed box = 2026 drill target area

Source: Company

Management is targeting 2 Moz of gold across the property, a goal we view as a reasonable exploration estimate

KG has launched its largest drill program to date (8,000–10,000 m), focused on expanding the Lone Star and Stander targets ahead of a resource update expected in early 2027

Update to include 19,157 m of drilling completed since the end of 2021, plus results from the current campaign

Royalty Income – Montana Creek

Located at the southern end of the Klondike District land package, Montana Creek is a producing placer gold property. In 2025, Armstrong Mining (a privately owned gold pro du cer) optioned the property from KG, and can acquire a 100% interest for $9.5M over six years.

KG has received $0.55M to date, and retains a 10% production royalty, with royalty payments credited toward the purchase price. Management forecasts royalty income of $1.5M in 2026, and $2.5M in 2027.

Up to $9M in payments over six years could support exploration activities and offset the need for future capital raises

Klondike vs. Coffee

A prominent advanced-stage gold project in the region is the Coffee Project, located ~130 km south of Klondike . Both projects are prospective for orogenic gold systems. Talamore Mining acquired the project from Newmont (TSX: NGT) in 2025 , in a deal valued at up to $210M.

Coffee hosts a larger, higher-grade resource, and is at a more advanced stage, but its remote location requires substantially higher CAPEX

Source: FRC / Various

TALA recently completed an independent economic study (PEA), which outlined an after-tax NPV5% of $5.2B at $5,000/oz gold, highlighting strong regional economics

Coffee trades at $327/oz based on TALA's enterprise value of $1.10B, vs $97/oz for KG's current resource, and $31/oz based on our resource estimate, highlighting a significant valuation gap

Regional Infrastructure Tailwinds: TALA ’s investment in regional infrastructure, including a new 214 km all-season access road, could indirectly benefit Klondike Gold through improved access, stronger contractor availability, and increased attention on the district. We believe continued exploration success could position KG as a potential acquisition target.

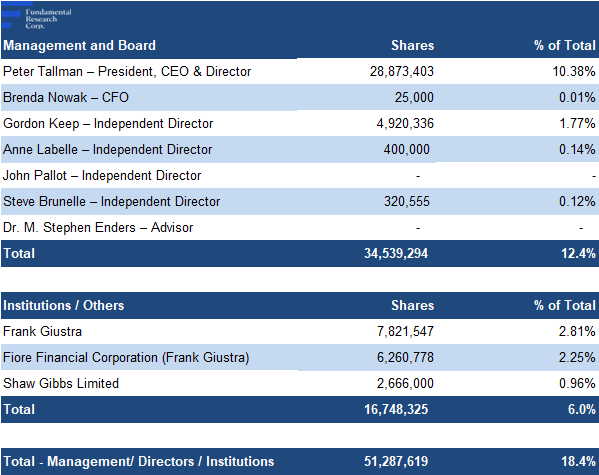

Management and Board

Led by an experienced mining and capital markets team

CEO Peter Tallman is the company's largest shareholder, owning ~10% of the shares outstanding

Source: S&P Capital IQ/FRC

Charitable foundations associated with Frank Giustra and Eric Sprott hold ~15% of the company, which we view as a strong endorsement

Four out of five directors are independent

Brief biographies of management and board members follow.

Peter Tallman – President, CEO & Director: 35+ years in mining and exploration; discovered/delineated three mineral deposits, two of which became producing mines; former Director of Fiore Gold , acquired by Calibre Mining for US$151M.

Brenda Nowak – CFO: 30+ years in securities law and corporate finance; serves as CFO, Corporate Secretary, and senior finance executive across multiple public resource companies.

Gordon Keep – Independent Director: Veteran investment banker and mining financier; CEO of Fiore Management & Advisory with extensive experience building and financing public resource companies.

Anne Labelle – Independent Director: Geologist, lawyer, and corporate director with 25+ years in mining; former mining executive and founder of Sterling Green Law Corporation.

John Pallot – Independent Director: 32+ years of executive and board experience; former CEO and President of resource companies and public company director since 1993. Steve Brunelle – Independent Director: 30+ years in exploration and mine development; involved in major discoveries and project advancements in Mexico and Canada.

Dr. M. Stephen Enders – Advisor: 45+ years in mining and exploration; former senior executive at Phelps Dodge, Newmont, EMX Royalty, and Colorado School of Mines.

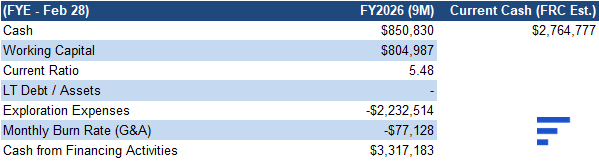

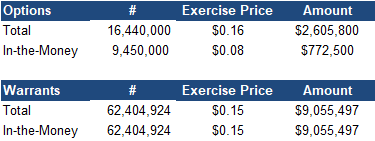

Financials

Strong balance sheet, with ~$2M in cash, and up to ~$10M from in-the-money options and warrants

Source: FRC / Company

No equity financing expected over the next 12–18 months, reducing dilution risk

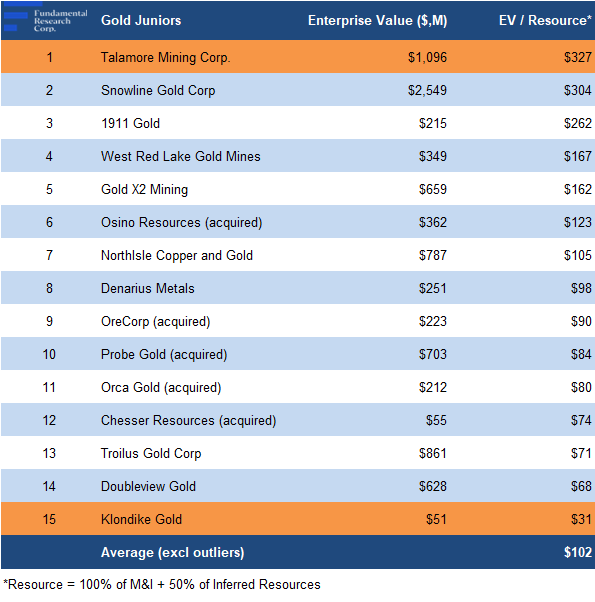

FRC Valuation & Rating

We value KG using the average EV/resource multiple of gold juniors

Source: FRC / S&P Capital IQ / Various

Based on the midpoint of our speculative estimate (1.65 Moz), KG is trading at $31/oz vs a comparables average of $102/oz, a 70% discount

Applying the comparables average implies a fair value estimate of $0.58/share

As shown in the table, KG trades at the lowest EV/resource multiple among peers, while its closest comparable, Talamore, commands the highest, highlighting a significant valuation gap

Our valuation also includes an estimated NPV of $5M ($0.02/share) from potential Montana Creek royalties

We initiate coverage with a BUY rating, and a fair value estimate of $0.59/share. We believe the current share price does not reflect KG's exploration upside, with the stock trading at a 70% discount to the sector EV/resource multiples. With the largest drill program in the company's history underway, a strong balance sheet, and multiple catalysts ahead, we believe the shares could move toward our fair value i f results from further exploration support our preliminary 1.5–1.8 Moz estimate.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are assigning a risk rating of 5 (Highly Speculative)