- Child-Safety Regulations Support Gaming Shift: Policies such as Australia’s under-16 social media restrictions, enforcement of the EU Digital Services Act, and increased U.S. COPPA scrutiny are limiting children’s access to social media, and shifting engagement toward mobile gaming and child-safe apps, supporting Kidoz’s audience base.

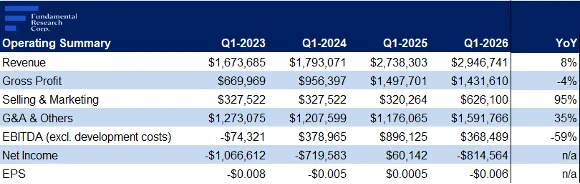

- Revenue Growth In Line with Expectations: Q1 revenue rose 8% YoY to $3M, in line with our estimate. However, in a departure from the usual trend of beating larger digital advertising platforms, growth lagged YouTube (NASDAQ: GOOGL) and Meta (NASDAQ: META), which reported ad revenue growth of 11% and 33%, respectively, over the same period.

- Elevated Spending to Support Future Growth: Operating expenses rose 48% YoY, approximately 13% above our estimate, driven by higher staffing costs, infrastructure investments, and AI-related R&D spending to support future growth. EPS turned negative, versus our expectation for a modest profit, primarily due to higher-than-expected operating expenses.

- Strong Balance Sheet Position: The company has no outstanding debt, and we do not anticipate any need for equity financing, limiting the risk of share dilution.

- Valuation Discount Creates Upside Potential: We continue to expect record revenue and EPS in 2026. Kidoz trades at 0.87x forward EV/revenue vs the sector average of 2.82x (69% discount), highlighting significant valuation upside potential.

Price and Volume (1-year)

| |

YTD |

12M |

| KDOZ |

-41% |

-23% |

| TSXV |

1% |

43% |

* Kidoz Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures are in US$, except share price, fair value, and MCAP data, which are in C$.

Company Overview

Source: Company / FRC

Two offerings on the same underlying platform, serving different audience segments across the full demographic spectrum

KIDOZ is a child-safe network that delivers ads through a platform integrated into mobile games, and apps

Launched in 2023, Prado adapts Kidoz’s core technology, and extends it to serve a broader, non-child mobile audience

Reaches 500M+ gamers every month across 40k+ games

Used by major brands such as Disney (NYSE: DIS), Lego, Mattel (NASDAQ: MAT), McDonald’s (NYSE: MCD), and others, reflecting trust from leading global advertisers

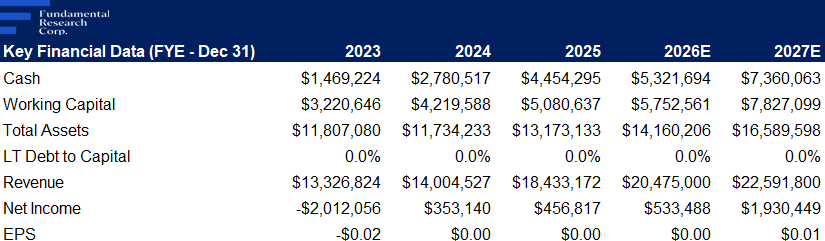

Three straight years of revenue growth; turned profitable in 2024

Source: FRC

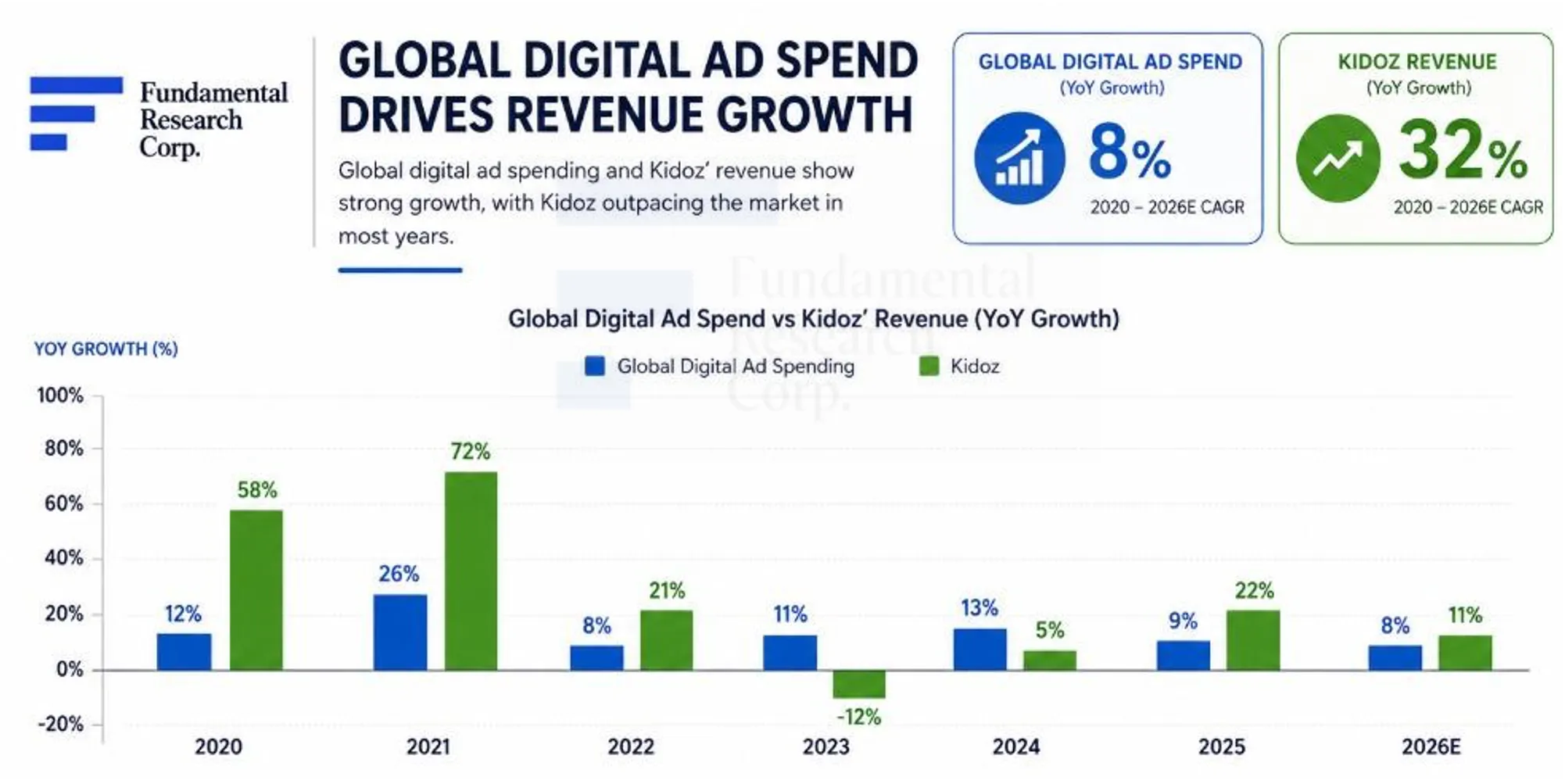

Kidoz is positioned at the intersection of privacy-first advertising, mobile gaming growth, and accelerating in-app ad demand

Source: FRC / Various

Historically, we estimate that KDOZ's revenue growth outpaced global digital ad spending growth by 2.1x on average

Financials

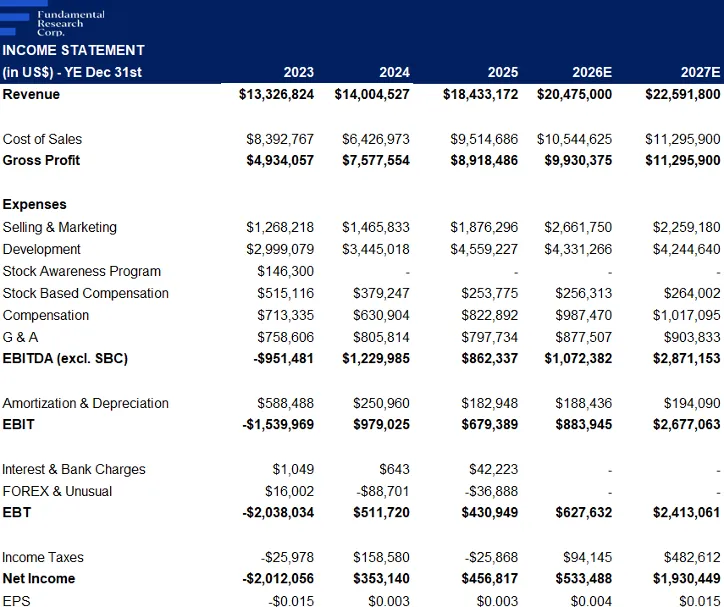

Q1 revenue was up 8% YoY to a record high of $2.94M, in line with our estimate

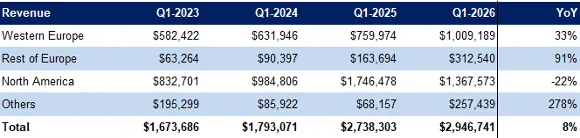

Growth was driven by organic international expansion, and a weaker US$, partly offset by softer North American (NA) revenue

Source: FRC / Company

Management attributed NA softness to a weak January; activity rebounded later in the quarter

We do not see signs of a broader slowdown in North American activity

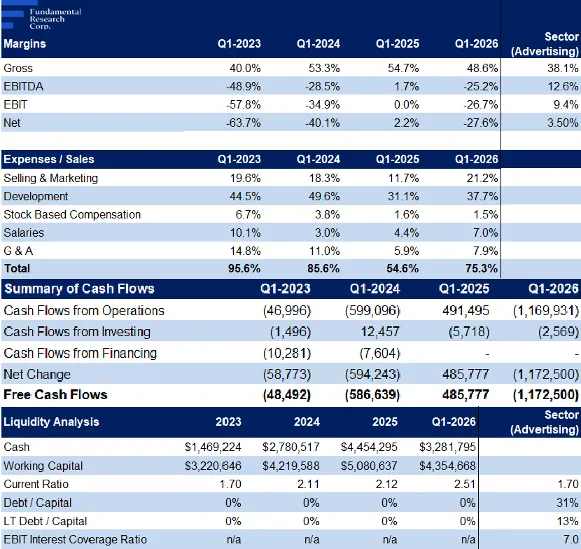

Gross margins fell 6 pp YoY to 49%, 1.5 pp below our forecast, due to a shift toward higher-volume, lower-margin revenue. We are lowering our near and long-term margin forecasts accordingly. For context, the advertising industry’s average gross margin is ~38%, versus ~40–60% for digital ad companies, keeping Kidoz within the broader industry range.

Gross margins compressed 6 pp YoY

Operating expenses rose 48% YoY, 13% above our estimate, mainly due to higher staffing and infrastructure costs to support growth and increased AI-related R&D spending

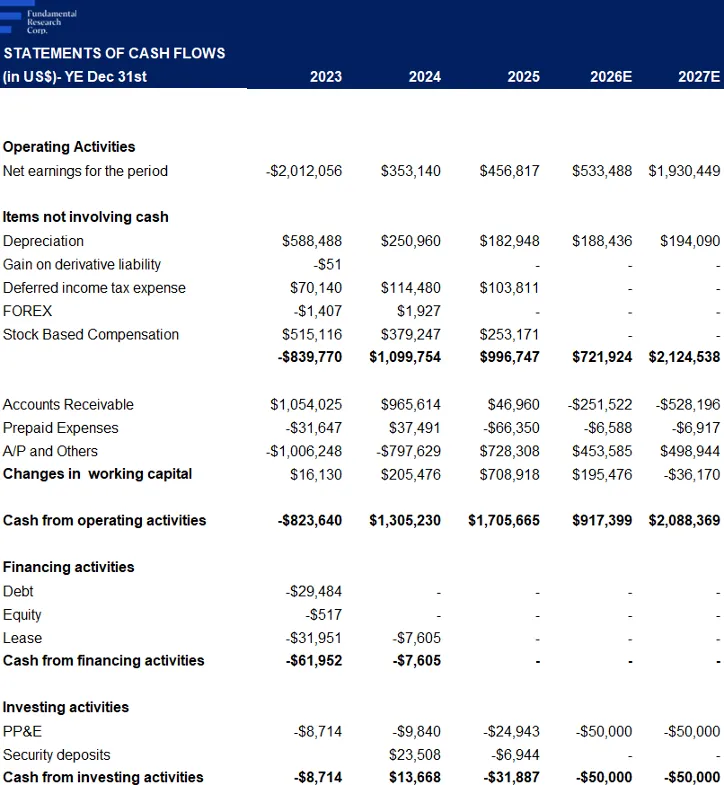

Higher revenue was more than offset by higher costs, driving a shift from profits to losses, while free cash flow also turned negative

EPS declined YoY from $0.0005 to ($0.006), vs our $0.001 forecast

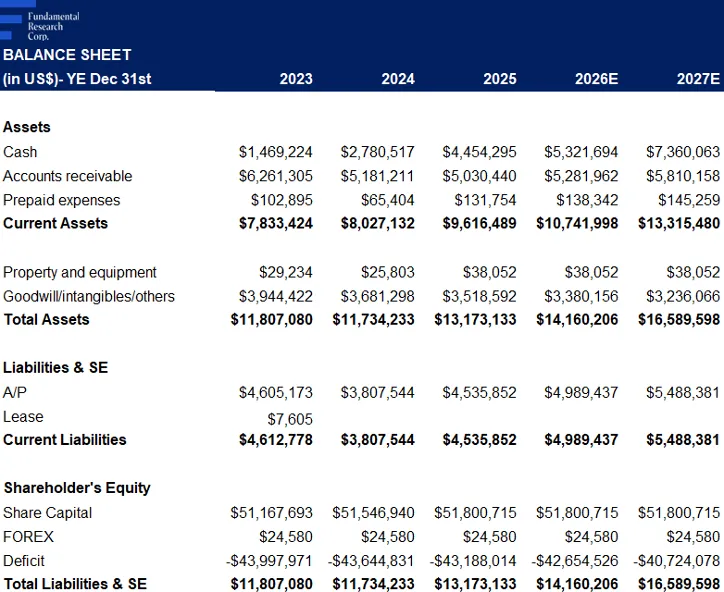

The balance sheet remains healthy with zero debt, and we see no need for financing or potential share dilution

Source: FRC / Company

FRC Projections and Valuation

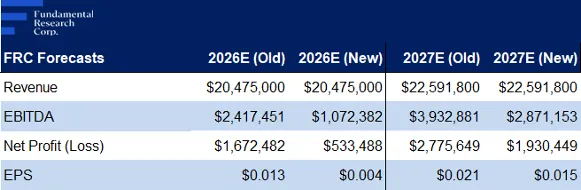

We are maintaining our revenue forecasts, but lowering our EPS forecasts, due to higher-than-expected operating expenses

Source: FRC

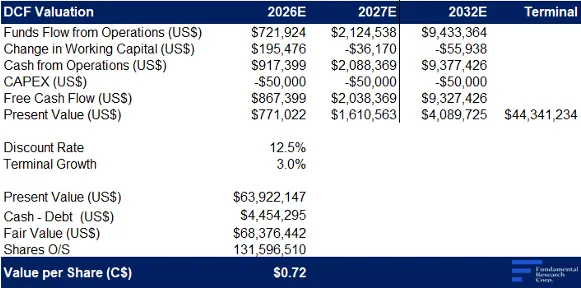

As a result, our DCF valuation declined from $0.84 to $0.72/share

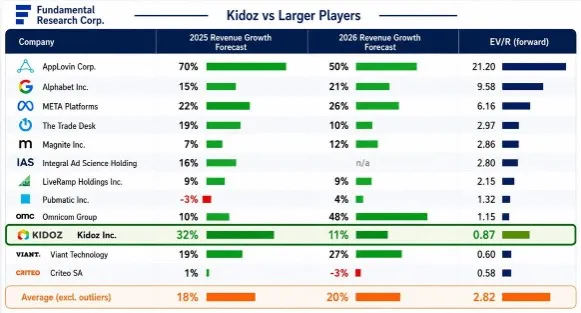

Digital AdTech Companies

Source: S&P Capital IQ / FRC

KDOZ is trading at 0.87x forward EV/Revenue (previously 1.20x), well below the sector average of 2.82x (previously 2.81x), a 69% discount

Our comparables valuation increased modestly to $0.65/share (from $0.64), driven by a higher sector multiple; revenue forecasts unchanged

We are reiterating our BUY rating, and lowering our fair value estimate from $0.74 to $0.68/share (the average of our DCF and comparables valuations). While elevated spending pressured near-term profitability, we believe supportive sector trends. and a favorable macro backdrop. continue to support revenue growth, and a positive outlook. With a debt-free balance sheet, and the shares trading at a significant discount to peers, we continue to see attractive upside potential.

Risks

We believe the company is exposed to the following key risks:

- Operates in a highly competitive space

- Unfavorable changes in regulations

- Ability to attract publishers and brands will be key to long-term growth

- FOREX

- Reliance on digital ad spending trends

- Changes in U.S. or global tariff policies that could affect client budgets

- Data privacy or security breaches could impact advertiser trust and platform reputation

Maintaining our risk rating of 4 (Speculative)

APPENDIX