Disclosure: Focus Graphite Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Sprott Critical Materials ETF

* Qualified Person: Réjean Girard, P.Geo. (QC), President of IOS Geosciences Inc., a consultant to Focus Graphite. Focus Graphite Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$; commodity prices in US$.

Aims to supply graphite anodes for lithium-ion batteries in North America

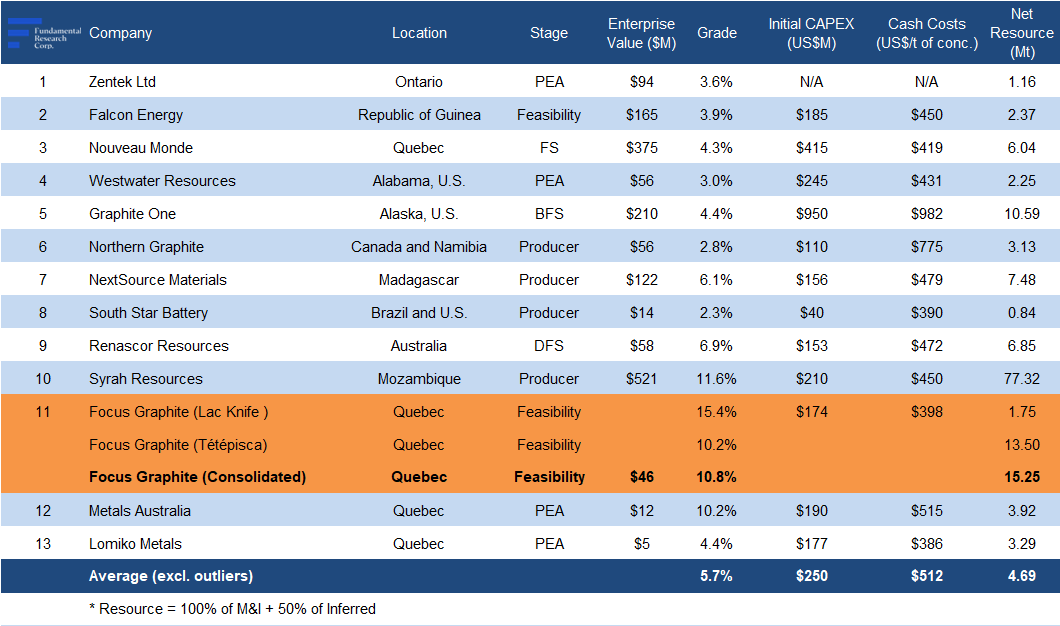

Portfolio Summary

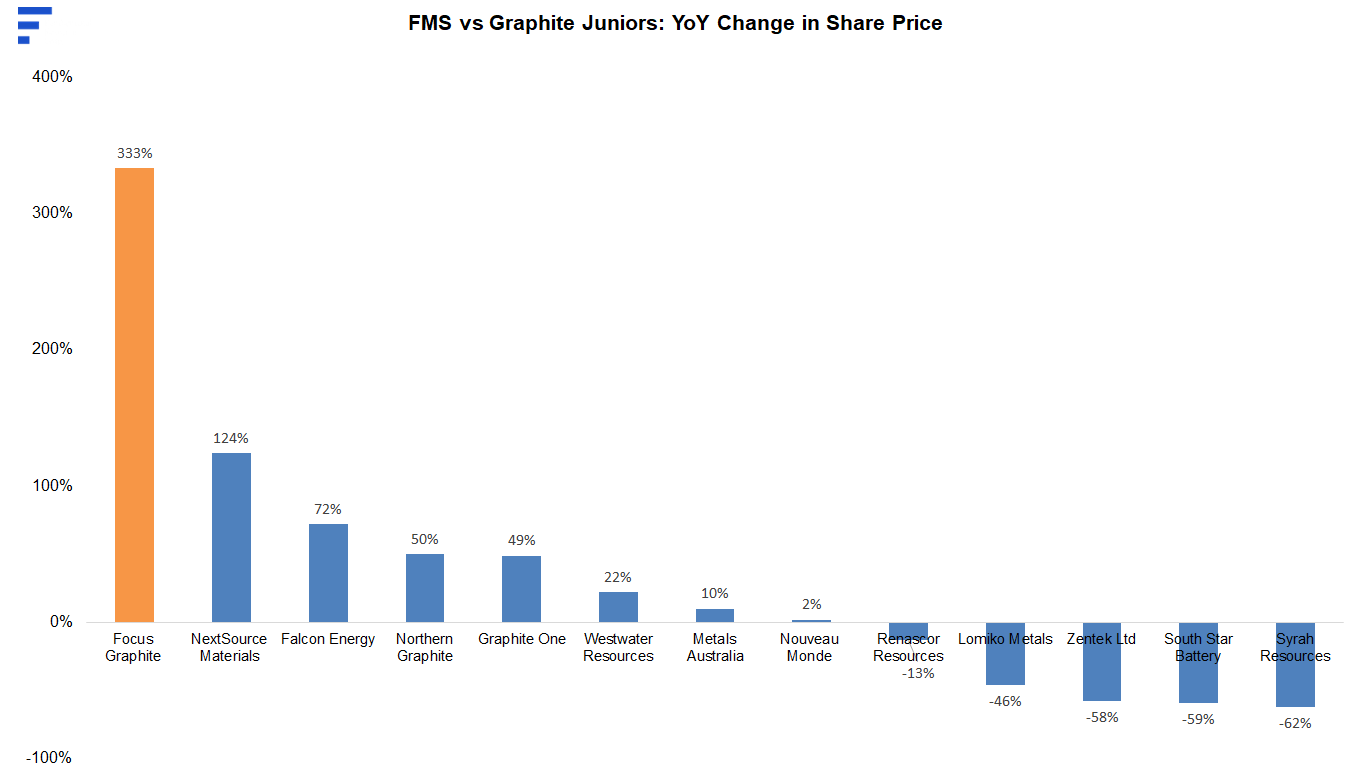

FMS vs Graphite Juniors

Source: S&P Capital IQ / Various / FRC

In December 2025, FMS received $14M in non-repayable government funding to build a high-purity graphite plant for military, defence, aerospace, and advanced technology applications

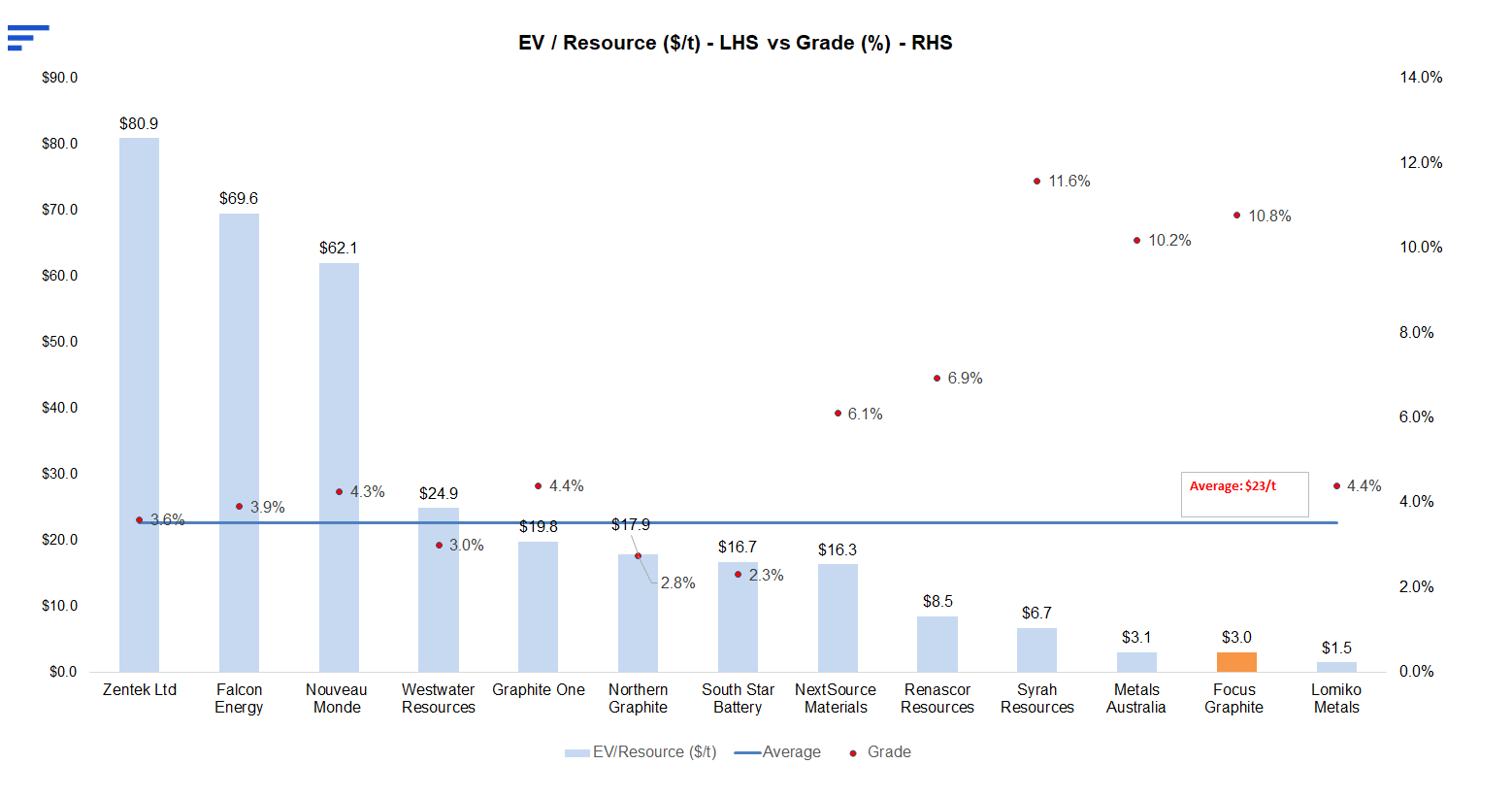

FMS stands out among comparable projects for its superior resource scale and grade, combined with below-average projected CAPEX and OPEX

Source: FRC

FMS is up 333% YoY, significantly outperforming the comparables average gain of 33%

Tétépisca Graphite Project (100% owned)

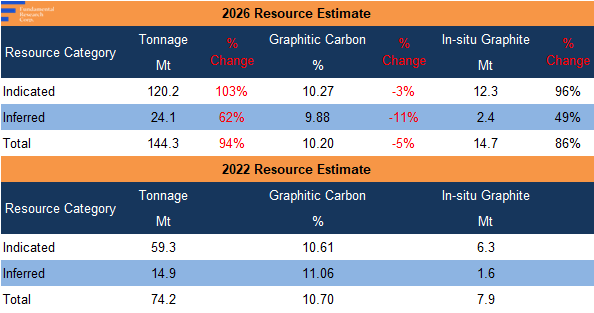

The updated resource estimate incorporates drilling since 2022, expanding the database to 150 holes (26,095 m) from 106 holes (16,467 m).

Source: Company / FRC

We believe this upgrade is transformational, positioning Tétépisca among the world’s largest and highest-grade graphite projects

Indicated resources (higher-confidence category) increased 96%; Inferred resources (lower-confidence) increased 49%

Indicated resources now account for 84% of total resources (previously 80%), reflecting higher confidence

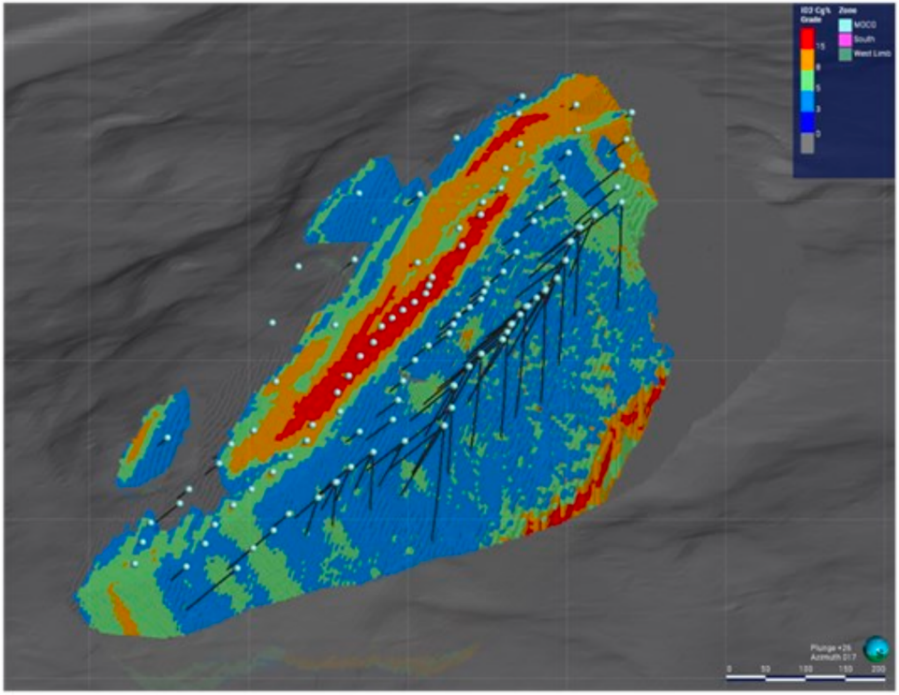

Block Model

* Red shows high-grade areas, while orange/yellow and green represent mid-to-high and moderate grades

Source: Company

Grades declined by 0.5 pp to 10.2%, but remain well above the typical 3–8% range for graphite projects

High-grade deposits are preferred due to their potential for stronger economics and lower operating costs

Next steps: FMS plans to conduct metallurgical testing to determine recovery rates, which will support an independent economic study (PEA) evaluating the project’s economic viability.

Lac Knife Graphite Project (100% owned)

FMS is also simultaneously advancing its flagship Lac Knife graphite project, a more advanced-stage asset. Next steps include product testing with potential buyers, securing supply agreements, completing the environmental assessment (now in its final stages), permitting, and project financing.

With a 25+ year mine life, the project offers potential for long-term, stable graphite supply for prospective buyers

Recent Developments

Source: FRC

If successful, these programs could support future partnerships, customer engagement, funding opportunities, and commercialization efforts

Project Development Stages

Permitting underway; production expected by 2028-2029

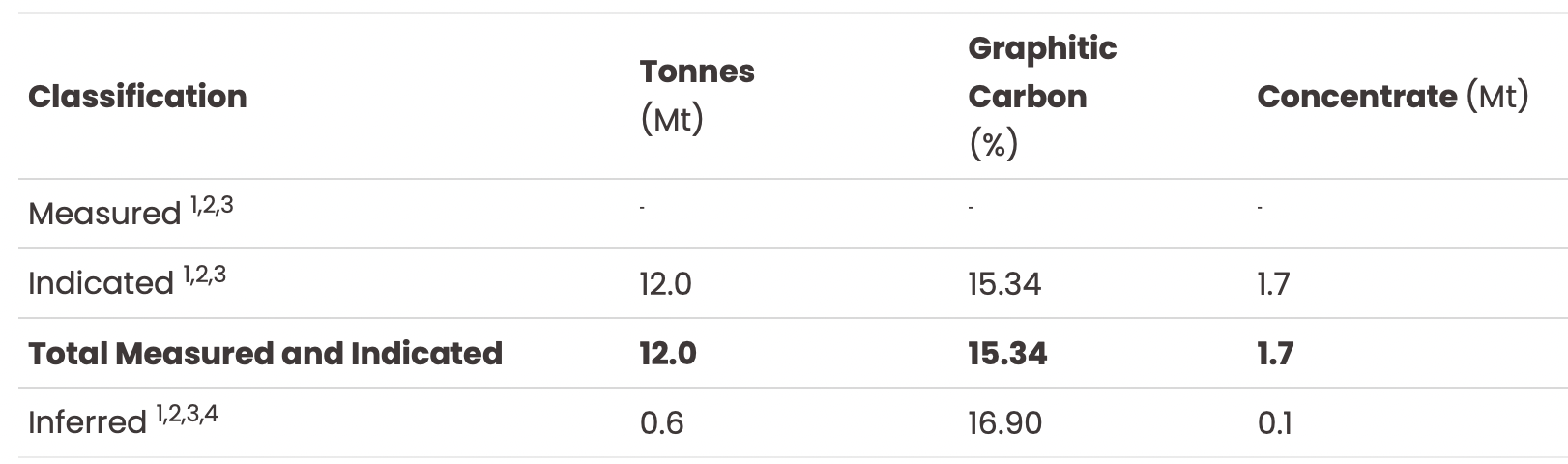

2023 Resource Estimate (4.0% Cg cut-off)

Source: Company

Ideal for open-pit mining, with one of the world’s highest graphite grades at 15% Cg

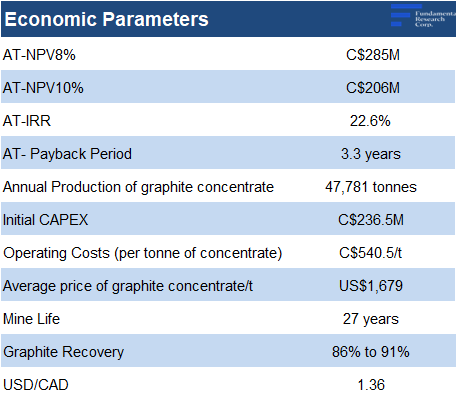

2023 Feasibility Study Highlights

Source: Company / FRC

After-tax NPV8% of $286M, and IRR of 23%; we view an IRR above 20% as very attractive

FMS’s MCAP is only $42M, suggesting the market is undervaluing Lac Knife, and assigning no value to Tétépisca

The study used a weighted average product price of $1,679/t vs the current spot price of $1,000-$1,500/t

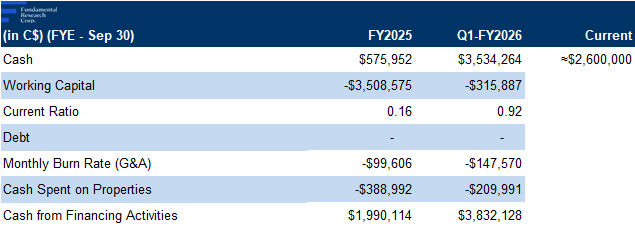

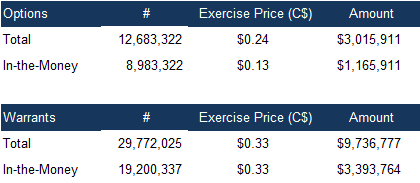

Financials

Healthy balance sheet, with in-the-money options and warrants that could add up to $5M

Source: FRC / Company

FRC Comparables Valuation

Source: S&P Capital IQ / Various / FRC

Despite attractive project metrics (large tonnage, high grade, and low costs), FMS is trading at just $3/t (previously $4/t), compared with the sector average of $23/t (previously $21/t)

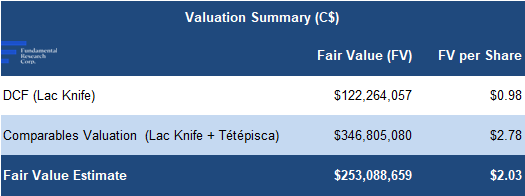

Applying the sector average to FMS’s resources, we arrived at a comparables valuation of $2.78/share (previously $1.53/share)

Source: FRC

The average of our DCF and comparables valuation is $2.03/share (previously $1.27/share)

We reiterate our BUY rating, and raise our fair value estimate from $1.27 to $2.03/share, reflecting the significant resource growth at Tétépisca. FMS is advancing two large-scale, high-grade graphite projects in Quebec, highlighted by a transformational resource expansion at Tétépisca, and continued progress at the flagship Lac Knife project. Despite the scale and quality of its assets, the company trades at a significant discount to its comparables.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining our risk rating of 5 (Highly Speculative)