- Stronger Energy Storage Tailwinds: Geopolitical tensions, including in the Middle East, are reinforcing demand for diversified and resilient energy systems, boosting energy storage adoption. The market outlook remains strong, supported by rising electricity demand, grid reliability needs, and growth from AI data centers and renewable integration.

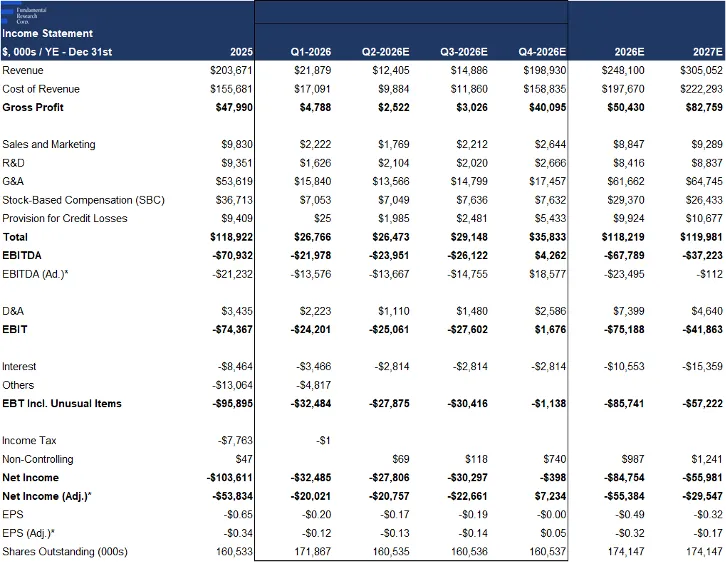

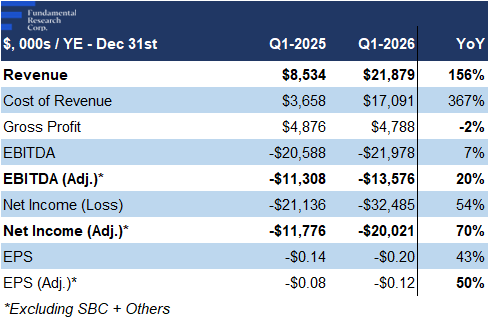

- Revenue Beat, Modest EPS Miss: Q1 revenue, primarily driven by third-party deployments, increased 156% YoY, beating our estimate by 47%. Adjusted EPS declined YoY, from ($0.08) to ($0.12), below our estimate of ($0.10). Quarterly revenue remains difficult to forecast due to variability in project completion timing. Management reaffirmed 2026 revenue guidance of $225–$300M (~30% YoY), and we maintain our $248M forecast.

- Significant Valuation Discount: NRGV trades at 13x forward EBITDA vs the sector average of 17x, a 23% discount.

Price and Volume (1-year)

| |

YTD |

12M |

| NRGV |

-15% |

446% |

| NYSE |

4% |

19% |

| ZAP* |

13% |

32% |

* Global X U.S. Electrification ETF

* Energy Vault Holdings has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in US$ unless otherwise specified.

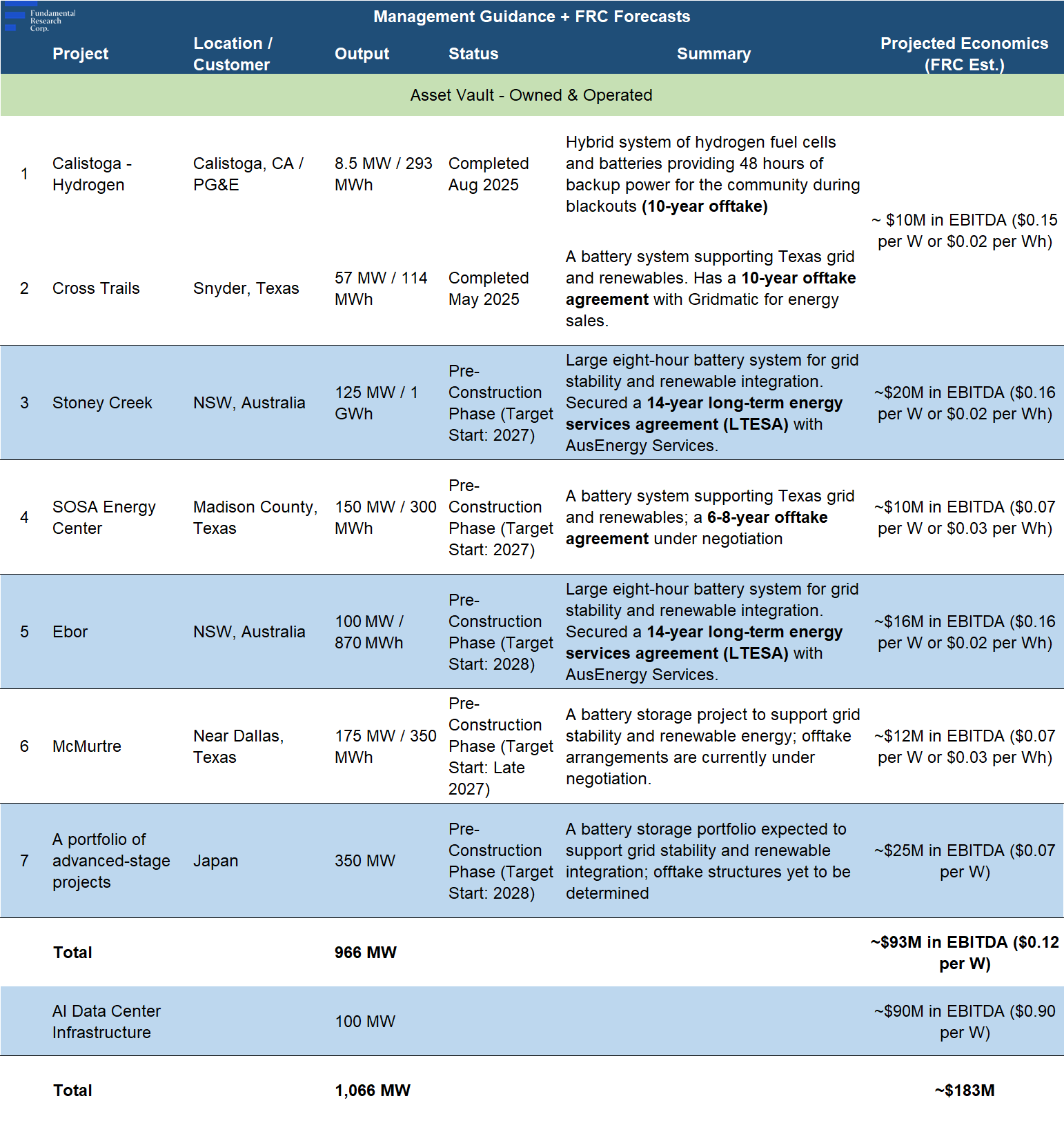

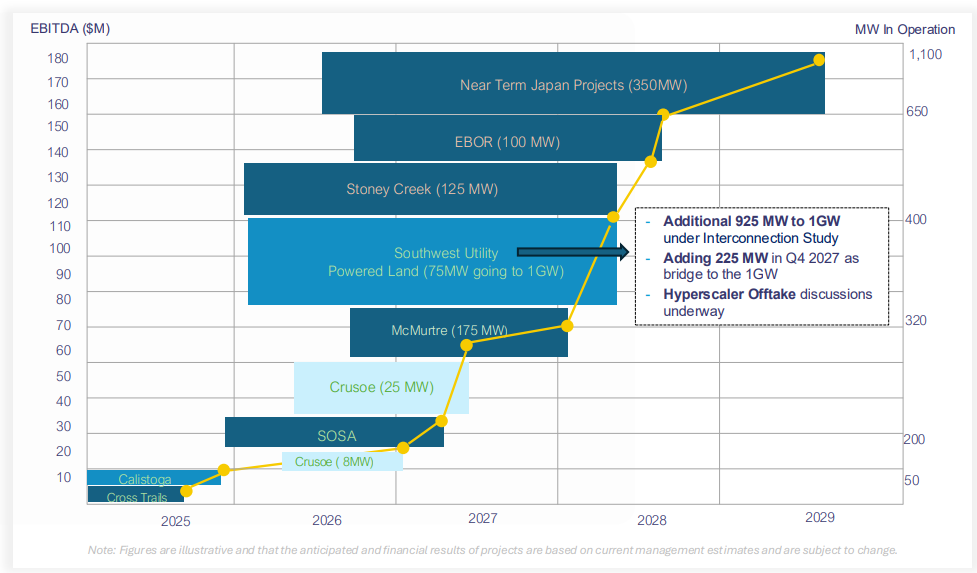

In Q1-2026, the company expanded its portfolio with a 175 MW project in Texas, and a 350 MW portfolio in Japan

Both projects are designed to support grid stability, and renewable integration, with completion expected in 2027–2028

NRGV now manages 1,066 MW of assets, up 461% YoY, with 66 MW operational, and the remainder expected online within two to three years

Asset Vault Portfolio

* Project economics depend on storage duration; duration refers to how long a system can supply power; longer-duration projects earn more EBITDA per MW (e.g., Sosa: two-hour → $0.07/W, Stoney Creek: eight-hour → $0.16/W)

* CAPEX to build a system is ~$0.30/Wh in the U.S., and ~$0.20/Wh outside the U.S.

Source: Company / FRC

Management projects ~$180M in annual EBITDA at full operation, with a long-term target of $1.8B+ from a ~4 GW portfolio by 2030

Projected Timelines

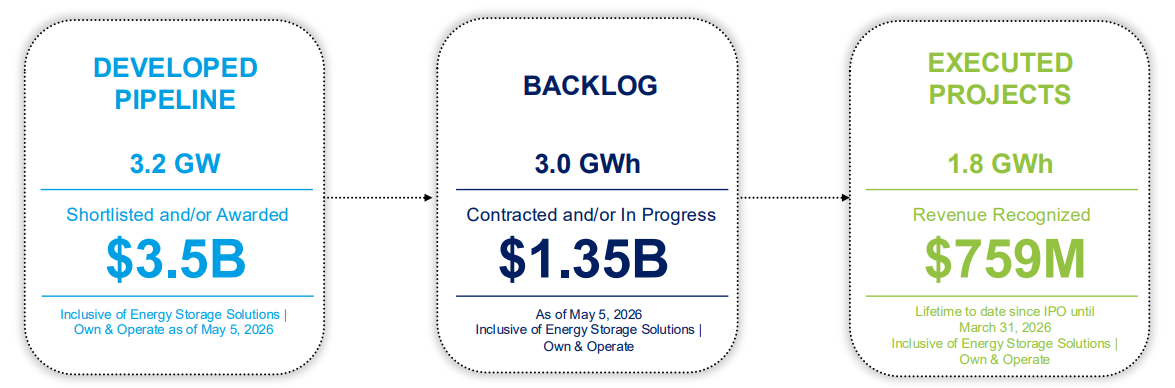

By the end of Q1-2026, NRGV had $1.35B in contracted backlog (Q4: $1.30B), and a $3.50B pipeline (Q4: $3.00B), with ~80% from its own projects, and the remainder from third-party deployments

Project Pipeline

Source: FRC

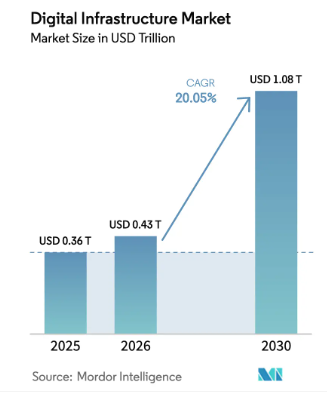

Expanding into Digital Infrastructure

The current portfolio includes a new 100 MW AI data center infrastructure project. While the rest of the portfolio consists of energy storage assets, this project integrates energy generation , and storage to power AI data centers.

Higher-margin expansion beyond core energy storage assets

This marks the company’s entry into the digital infrastructure space , which includes the energy and computing backbone for AI, cloud computing, and data centers. It is one of the fastest-growing , and most in-demand infrastructure segments, driven by accelerating AI adoption, rising cloud workloads, and increasing power intensity requirements.

Forecast to grow at a CAGR of 21% from 20226 to 2030

Given its broader scope, such projects carry significantly higher margins (~$1/W in EBITDA vs ~$0.10/W for standalone storage). The company is increasingly focused on scaling this segment alongside its storage business. We believe this new business line is strategically important, driven by rising demand for AI-driven digital infrastructure, materially higher margins, and stronger market sentiment, with higher EBITDA multiples than traditional storage assets.

Financials

Source: FRC / Company

Q1 revenue, dominated by third-party deployments, was up 156% YoY, beating our estimate by 47%

Quarterly revenue remains difficult to forecast due to variability in project completion timing

We are maintaining our full-year forecast; similar to last year, we expect revenue to remain heavily weighted toward Q4

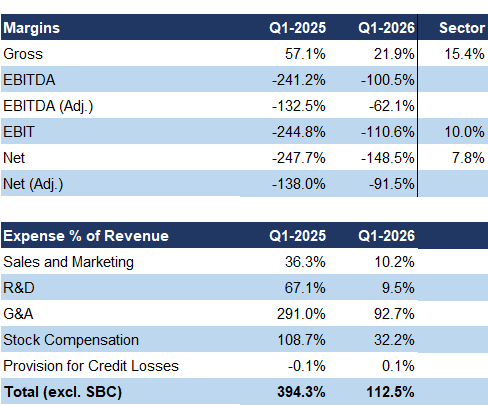

Gross margins declined significantly YoY, normalizing to levels consistent with third-party deployments. Q1-2025 was abnormally elevated due to certain non-recurring IP licensing revenue with 100% gross margins

Operating expenses increased 22% YoY, and were 4% higher than expected

Despite higher revenue, elevated operating expenses led to a decline in adjusted EPS from ($0.08) to ($0.12), missing our estimate of ($0.10)

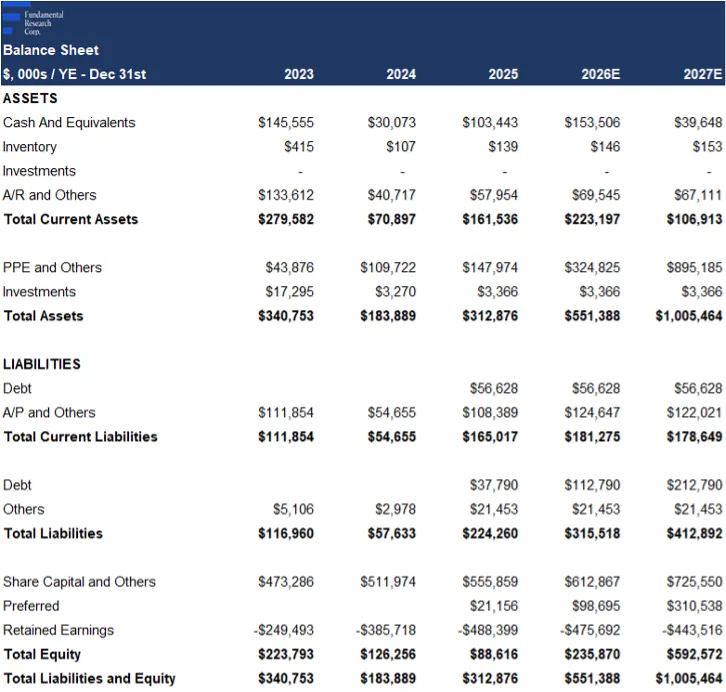

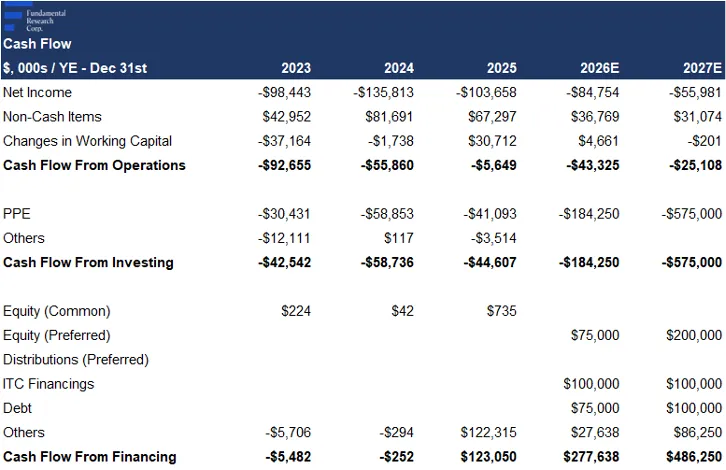

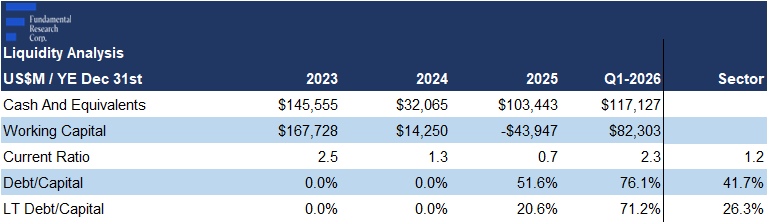

At the end of Q1, the company held $117M in cash, up 13% QoQ

Source: FRC / Company

Debt-to-capital is elevated due to a relatively low book value of equity following several years of losses

FRC Valuation and Rating

Source: FRC

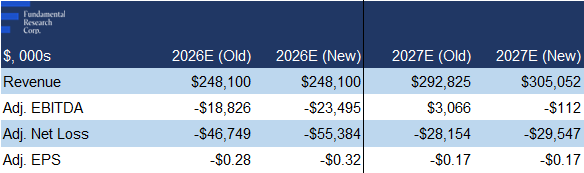

We are lowering our 2026 EPS forecast due to higher-than-expected operating and deprecation expenses, while raising our long-term (2028+) revenue and EPS forecasts following the recent project acquisitions, and entry into the digital infrastructure space

We now expect project acquisitions to scale total capacity to ~1.6 GW by 2029 (previously ~1.5 GW), and to ~4 GW by 2034 (previously ~2.4 GW)

To account for execution risk, we are raising our discount rate from 10% to 15%

Source: FRC

As a result of the above changes, our DCF valuation increased from $6.53 to $8.09/share

*We use the present value of our 2029 EBITDA estimate on NRGV in this calculation.

Source: FRC / S&P Capital IQ

Given the company’s entry into the digital infrastructure space, we have expanded our comparables set to include digital infrastructure companies

The average forward EV/EBITDA of comparables increased from 13x to 17x, driven by the inclusion of digital infrastructure companies, which generally trade at higher multiples, and a rise in multiples across existing energy storage and technology comparables

NRGV is currently trading at 13x, a 23% discount

Applying the sector multiple implies a comparable valuation of $8.23/share (previously $5.57/share)

We are reiterating our BUY rating, and adjusting our fair value estimate from $6.05 to $8.15/share (the average of our DCF and comparables valuations). NRGV delivered a quarter of strong top-line growth, and continued pipeline expansion. We believe the company’s accelerating global buildout, entry into digital infrastructure, and discounted valuation s position the stock favourably for those seeking exposure to high-growth energy and AI infrastructure markets.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- Tariffs: U.S. tariffs on Chinese lithium-ion imports may raise costs

- Policy: Changes in green energy incentives could reduce demand

- Credit: Most large utilities and IPPs are low-risk counterparties, while smaller industrial clients and new partners carry higher default risk

- Compliance: Projects must meet all regulations and permits

- Financing: High upfront costs require funding

- Sales Cycle: Long nine-to-18-month installation delays revenue

- FOREX

While the company operates in a relatively low-risk market with potential for long-term steady cash flow, we believe its early-stage deployment of energy storage projects warrants a risk rating of 4 (Speculative)

APPENDIX