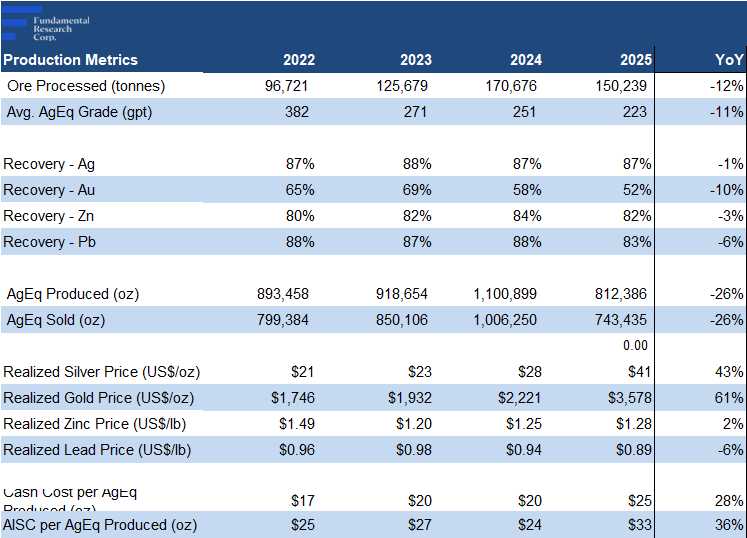

- 2025 production in line: 2025 production fell 26% YoY to 812 koz, driven by lower throughput (processing rate), and grades, nearly in line with our 811 koz estimate. Q1-2026 throughput rose 8% QoQ to 500 tpd, increasing further to 690 tpd by March 2026, supporting a strong 2026 outlook.

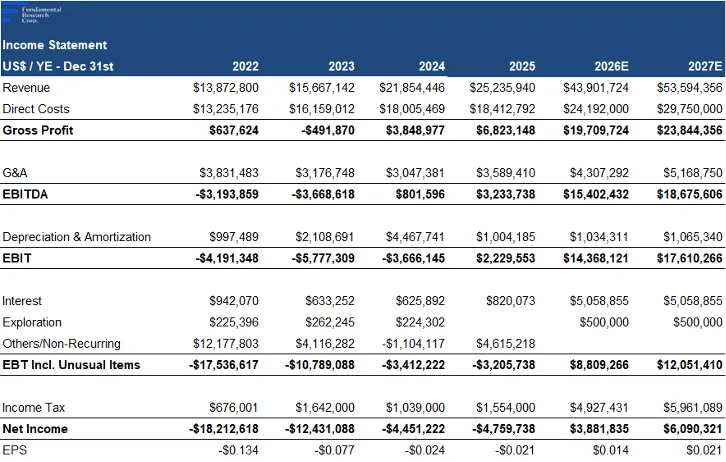

- Earnings inflection: Despite lower production, 2025 revenue rose 15% YoY on higher metal prices, and beat our estimate by 8%. Adjusted EPS improved YoY from ($0.02) to $0.001 vs. ($0.005) forecast, marking a profitability inflection.

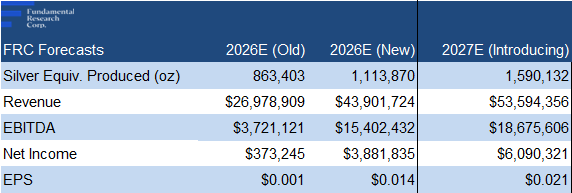

- Production growth outlook: Targeting ~1,000 tpd by Q3-2026, supported by $5M CAPEX. We forecast 37% YoY production growth, to 1.11 Moz AgEq in 2026.

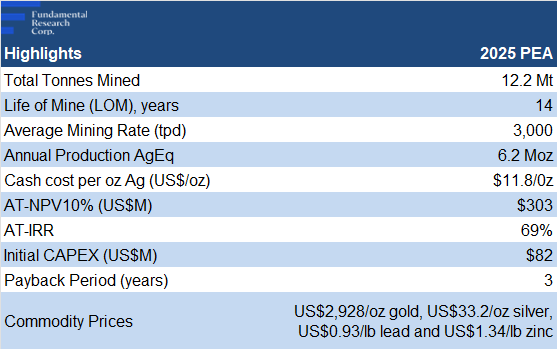

- Long-term growth optionality: 40,000 m resource expansion drill program underway, the largest in the company’s history. An independent economic study (PEA), completed last September, supports potential production of ~6 Moz/year within two to three years.

- Strong silver backdrop: We remain positive on silver, supported by US$ weakness and strong safe-haven demand, amid economic and geopolitical uncertainty. The Silver Institute expects the market to remain in a deficit for a sixth consecutive year in 2026.

- Valuation disconnect: AGX trades at a 50% discount on average to junior silver miners on forward EV/Revenue and EV/EBITDA, suggesting growth is not fully priced in.

Price and Volume (1-year)

| |

YTD |

12M |

| AGX |

-33% |

387% |

| TSXV |

0% |

51% |

| SILJ |

5% |

141% |

* QP: A. David Heyl, C.P.G., Consultant for Silver X Mining. Silver X Mining has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in US$ unless, except for share price, fair value estimates, and MCAP data, which are in C$.

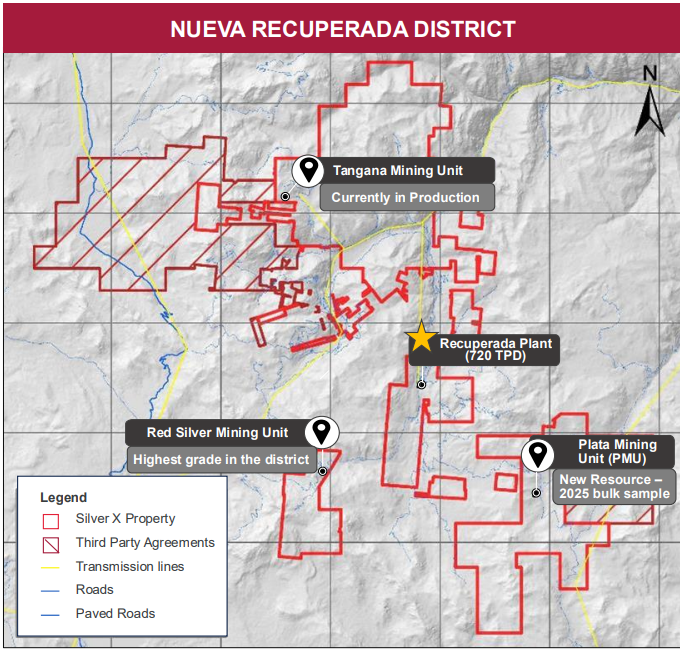

The Nueva Recuperada project includes the producing Tangana mine unit (TMU), with a 720 tpd processing plant, the advanced-stage Plata mining unit (PMU), and four exploration projects

Project Overview

The 2025 PEA highlights the potential to increase annual production from ~1 Moz to 6+ Moz

AGX’s expansion plan involves two milling facilities: a new 1,500 tpd mill at Tangana, and the existing Recuperada mill (15 km south of Tangana), which will be expanded from 720 tpd to 1,500 tpd

(QP: A. David Heyl, C.P.G., Consultant for Silver X Mining)

Source: Company

Recuperada will be dedicated to processing ore from the PMU

The PEA returned an AT-NPV10% of $303M, using $33/oz silver (spot: $73/oz), and $12/oz in cash costs

Source: Company

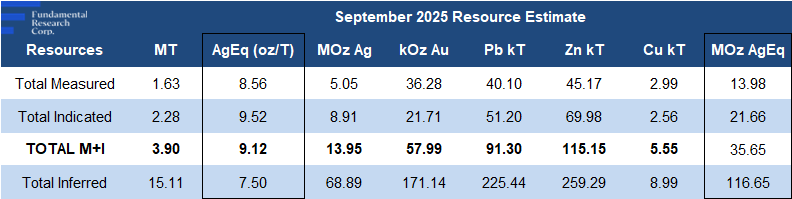

The PEA accounted for just 64% of resources, indicating further upside for NPV and IRR

Production and Key Operating Metrics

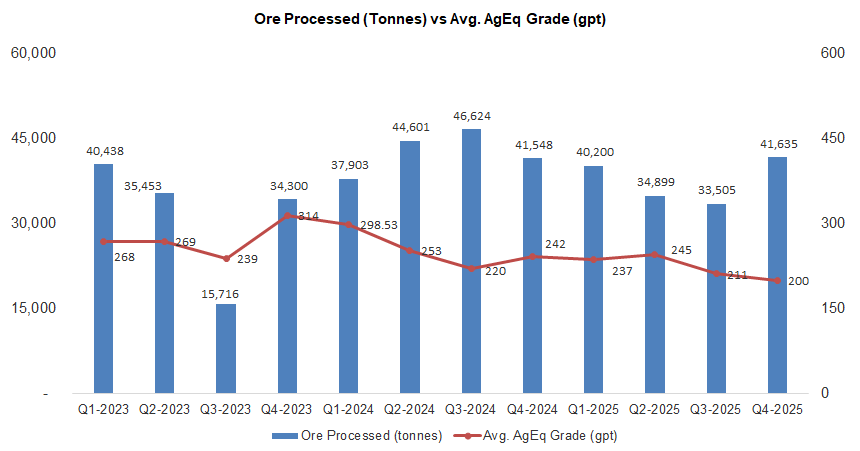

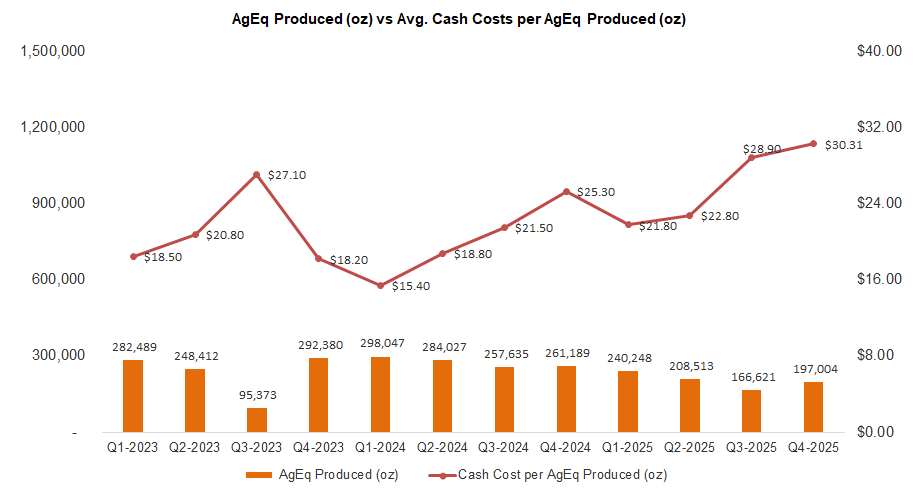

2025 production fell 26% YoY to 812 koz, driven by lower throughput and grades, but was almost exactly in line with our 811 koz estimate

Higher metal prices supported revenue, partially offsetting the impact of lower production

Throughput declined due to temporary contractor-related issues, now resolved

Source: FRC/Company

While silver grades increased YoY, average silver equivalent grades declined due to lower zinc and lead grades, along with a sharp rise in silver prices relative to other metals, impacting the silver equivalent calculation

We expect grades across all metals to improve going forward, as 2025 levels were materially below those in the resource estimate

Source: FRC/Company

In Q1-2026, AGX raised throughput 8% QoQ; March hit 690 tpd vs. 463 tpd in Q4-2025, supporting a strong 2026 production outlook

2025 cash costs rose 28% YoY, but came in 5% below our estimate

Near-term plans include:

- Increase production rate from 500 to 1,000 tpd in 2026

- Advance the PMU to production in 2027 (pushed from 2026)

- Update the Environmental and Social Impact Assessment (ESIA) to support a potential 1,500 tpd operation at Tangana

- Secure permits for a new 1,500 tpd processing facility

- Continue resource expansion drilling.

Financials

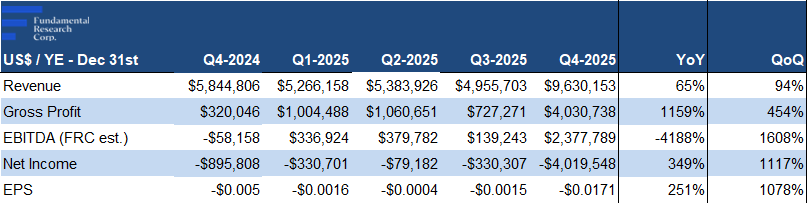

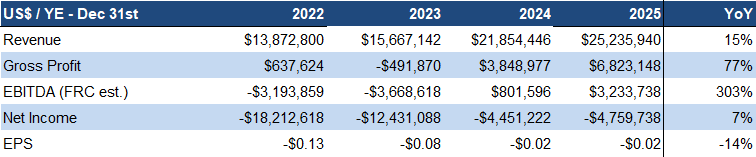

2025 revenue rose 15% YoY on higher metal prices, partly offset by lower production, and beat our estimate by 8%

EBITDA was up 303% YoY

Source: FRC/Company

Adj. EPS improved YoY, from ($0.02) to $0.001 vs. our forecast of ($0.005), marking a key milestone in the shift to profitability

The adjusted 2025 EPS mentioned above does not include a one-time $5M non-cash provision related to historical unpaid fines issued by local regulatory authorities , in connection with infrastructure and environmental matters at the processing plant , under previous ownership. Management indicates that the relevant compliance issues have since been corrected, with final resolution expected shortly. In our models, we assume the full $5M provisioned amount will ultimately be paid.

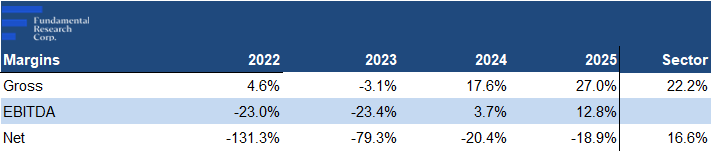

Margins improved across the board on higher metal prices

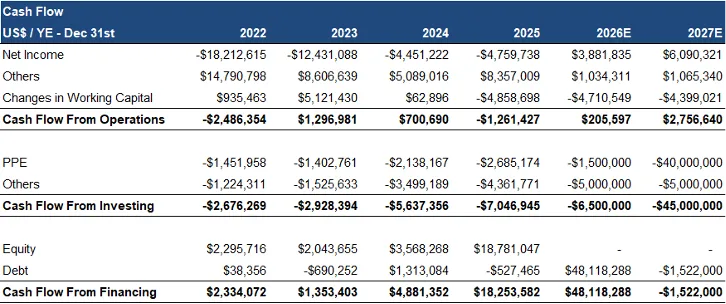

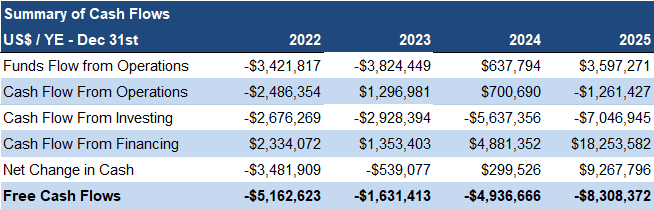

Funds from operations rose 464% YoY, while free cash flow declined, due to higher exploration spend, and increased receivables from December 2025 revenue, collected in early 2026; therefore, the FCF decline is not a concern

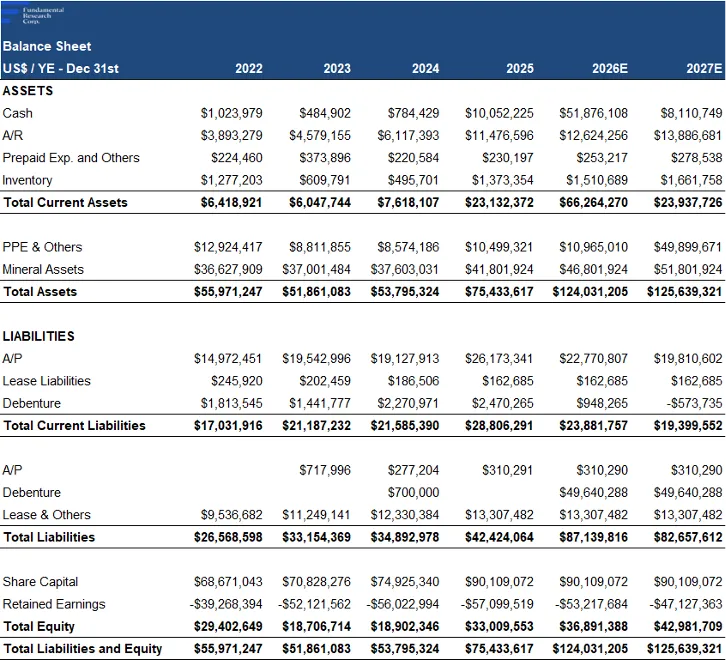

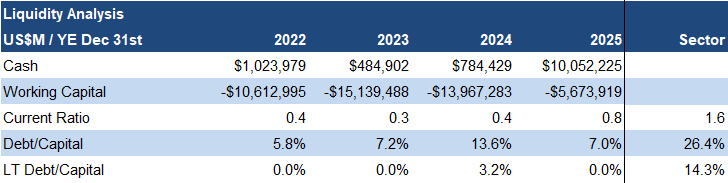

Working capital improved QoQ, from ($15M) to +$6M

In Q1-2026, AGX raised $50M via convertible debentures, and $3M from warrants/options, lifting working capital to $47M, and strengthening the balance sheet

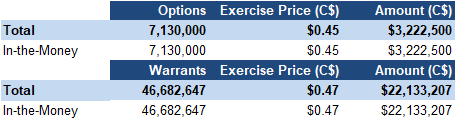

Can raise another $18M from in-the-money options/warrants

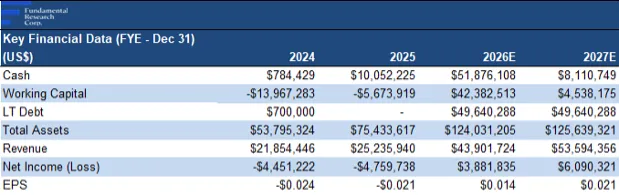

FRC Projections

Source: FRC

Given the potential ramp-up in production this year, and the recent step-up in metal prices, we are raising our 2026 revenue and EPS forecasts

Comparables Valuation

Source: FRC / S&P Capital IQ / Various

AGX’s forward EV/Revenue is 1.57x vs the sector average of 3.64x, a 57% discount

AGX’s forward EV/EBITDA is 3.40x vs the sector average of 6.04x, a 44% discount

Applying the sector averages, we arrived at a comparable valuation of $1.88/share (previously $1.64/share), driven by our higher revenue and EBITDA forecasts

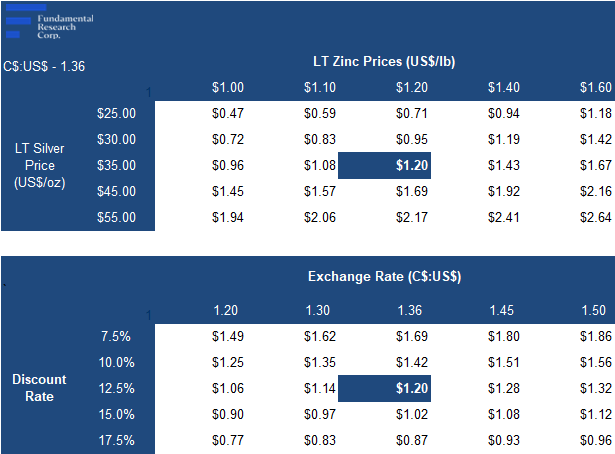

DCF Valuation

Source: FRC

Our DCF valuation rose from $1.04 to $1.20/share

Our valuation remains highly sensitive to metal prices

We are reiterating our BUY rating , and adjusting our fair value estimate from $1.34 to $1.54/share (the average of our DCF and comparables valuations). AGX has delivered strong momentum, with a 387% YoY share price gain, improving profitability, and a significantly strengthened balance sheet following recent financings. Looking ahead, growth is supported by expanding capacity, and a strong silver backdrop, yet AGX trades at a 50% discount to junior silver miners, suggesting its growth potential remains underappreciated.

Risks

We believe the company is exposed to the following key risks:

- Metal prices

- Exploration and development

- FOREX

- Production ramp-up may be slower than expected

- OPEX and recovery rates may underperform assumptions in our models

Maintaining our risk rating of 4 (Speculative)

APPENDIX