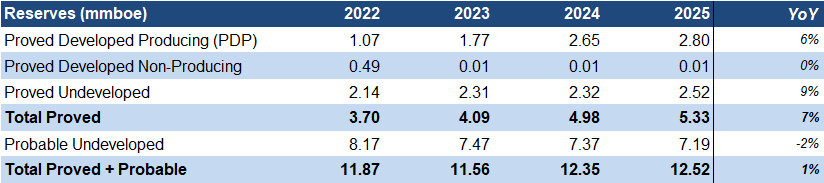

- Large Undeveloped Resource Base: BRK has produced 3.7 mmboe since 2021, and holds 12.52 mmboe of remaining reserves (as of Dec 31, 2025), supporting 19 future drilling locations. We expect cash from operations to fund development, limiting financing risk, and share dilution.

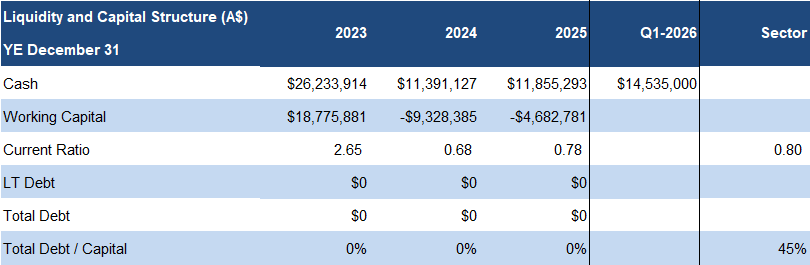

- Strong Balance Sheet & Liquidity: Cash rose 23% QoQ to $15M, and the company maintains a debt-free balance sheet with a $35M undrawn credit facility, providing strong financial flexibility.

- Low-Cost Structure Supports Resilience: Elevated oil prices driven by geopolitical tensions have strengthened sector sentiment. BRK’s low production costs ($5–$10/boe vs. ~$104/bbl spot) support resilient profitability, when prices normalize as Middle East tensions ease.

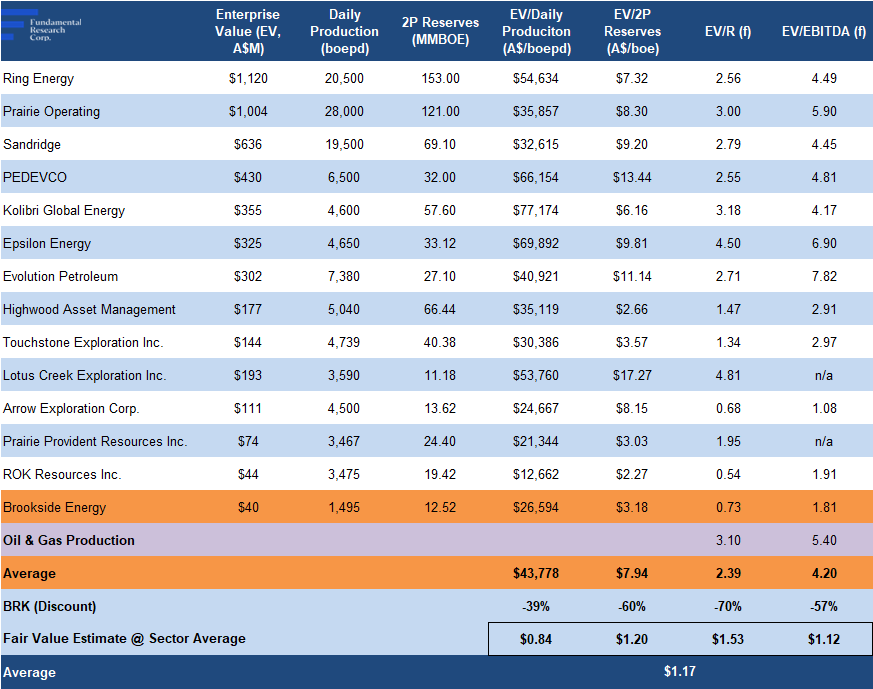

- Compelling Valuation Discount: BRK trades at a 56% discount to peers across key metrics, including EV/Forward Revenue (0.73x vs. 2.39x), EV/Forward EBITDA (1.81x vs. 4.20x), EV/daily production ($27k vs. $44k), and EV/2P reserves ($3.18x vs. $7.94x).

- Multiple Near-Term Catalysts: Key catalysts include the upcoming two-well drilling program, and a potential NYSE American ADR listing (targeted for H1-2026), which could broaden the investor base, and improve liquidity. We also anticipate record revenue this year, driven by higher production and supportive oil prices.

Price and Volume (1-year)

| |

YTD |

12M |

| BRK |

19% |

50% |

| ASX |

0% |

7% |

| Sector* |

40% |

59% |

* Brookside Energy has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in A$ except commodity prices, which are in US$.

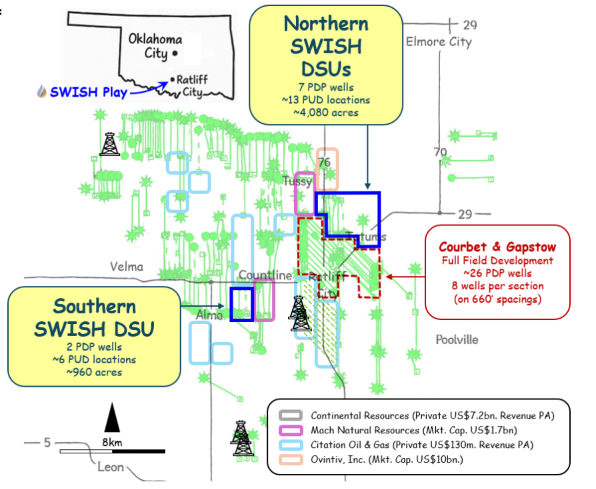

BRK’s portfolio sits within the Anadarko Basin, which covers ~58,000 sq miles (150,200km²)

Portfolio Overview

Key Targets in the Anadarko Basin , Oklahoma

A mature basin revived by horizontal drilling and fracking

Horizontal drilling + fracking has transformed oil production by boosting output, improving recovery, and unlocking shale resources previously uneconomic

Per various sources, the basin is estimated to host tens of billions of boe in recoverable resources, supporting multiple decades of remaining drilling potential

Source: Company

BRK operates nine producing wells (PDP), and 19 proved undeveloped locations (PUDs/planned for future development), across 5,000+ acres

BRK has a 100% success rate, with all nine wells successfully drilled on first attempt

Reserves & Expansion Potential

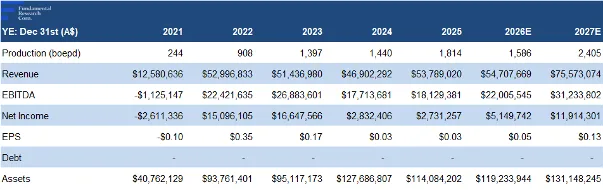

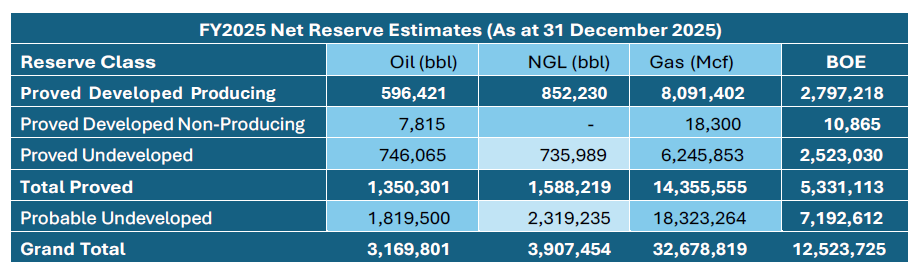

BRK has produced over 3.7 mmboe since 2021

As of December 2025, the portfolio had 12.52 mmboe in reserves, including 2.80 mmboe from the currently producing nine wells, and 19 future drilling locations

The existing wells are expected to remain productive for ~20 years

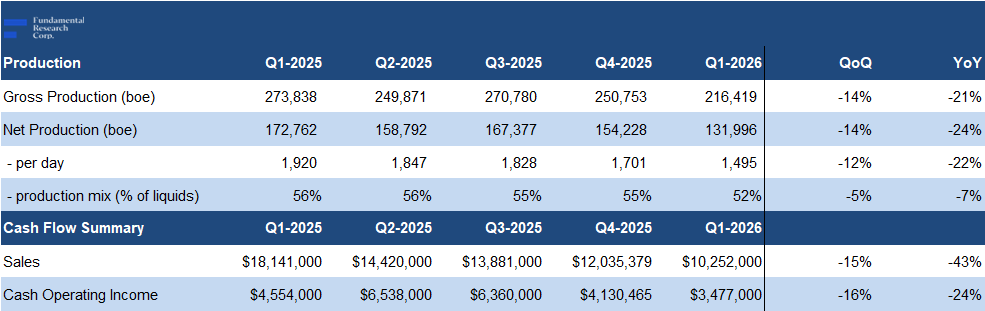

Q1 production fell 14% QoQ due to natural decline rates, 9% lower than our estimate

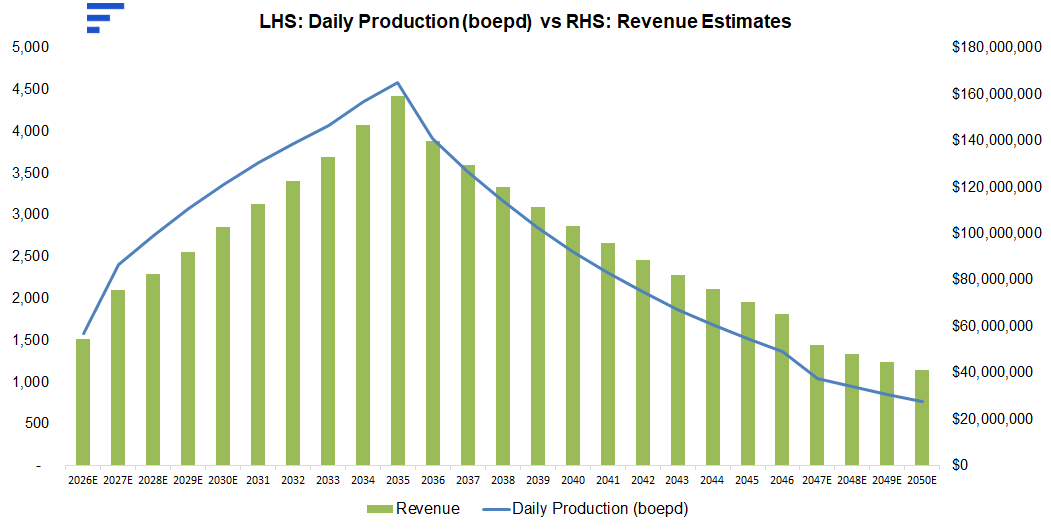

Production Data and Key Metrics

Sales declined 15% QoQ, and cash operating income fell 16% QoQ; both were ~9% below our estimates

Note that decline rates are typically steeper in the initial years, and then flatten to ~10% annually

Source: FRC / Company

RK ended Q1 with $15M in cash (up 23% QoQ), and access to an undrawn $35M credit facility, providing $50M in available funding

Near-Term Plans & Catalysts

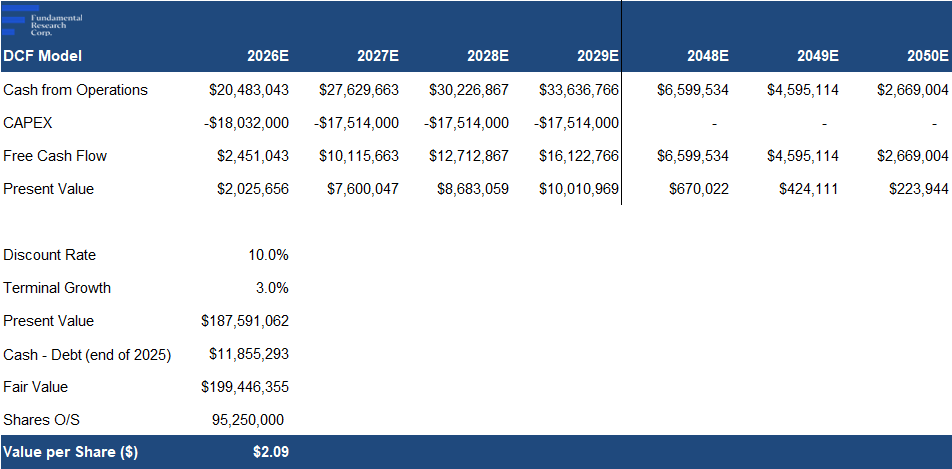

- BRK is currently pursuing the first two of the remaining 19 potential wells (projected CAPEX of $ 18M net for BRK, to be funded through cash from operations), which are expected to come online in H2 - 2026.

Multiple near-term catalysts with potential to drive production and reserve growth

- The company is advancing the Riverbend AOI in the Anadarko Basin, a ~24 sq. mile position identified in late 2025 , and located on trend with third-party prolific wells in the region; initial technical work indicates significant oil-in-place potential, and BRK is actively leasing acreage to support future development.

- BRK is also evaluating additional stacked pay potential (meaning multiple oil- and gas-bearing rock layers stacked on top of each other that can be developed separately) across its acreage , beyond the Sycamore and Woodford formations (~7,000–10,000 ft). This includes the Caney Shale (~5,000–7,000 ft), and the deeper Simpson Group (>9,000–12,000+ ft), both of which are not included in current reserves but could provide meaningful upside.

Oil Price Outlook

Source: FRC / GLJ / Sproule

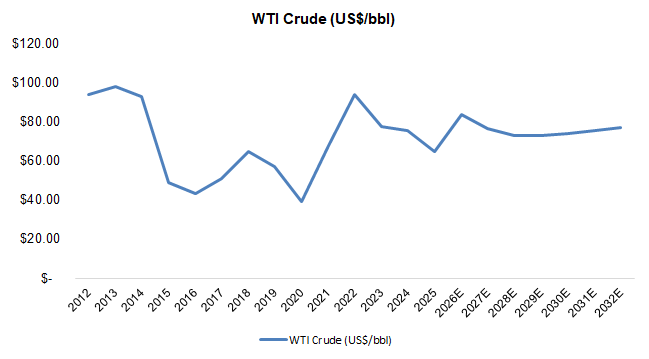

Consensus near and long-term price forecasts remain well above the 10-year average of $64/bbl, suggesting a supportive pricing backdrop for stronger netbacks, and improved economics

BRK vs Junior Oil and Gas Producers

Source: FRC / S&P Capital IQ

BRK trades at an average discount of 56% to comparables across key metrics

Sector multiples are up 12% since our last report

Applying sector multiples, we arrive at a comparable valuation of $1.17/share (previously $1.12/share), driven by higher sector multiples, partially offset by our lower revenue and EBITDA estimates

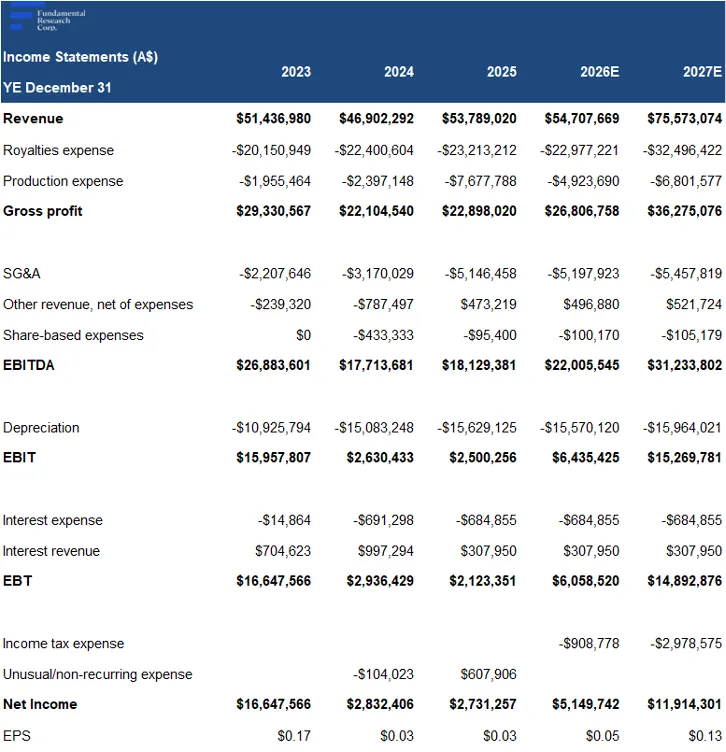

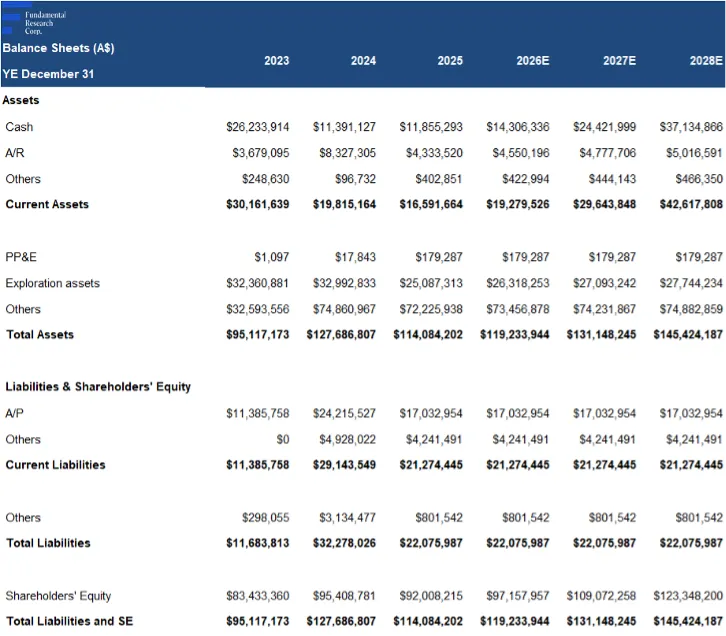

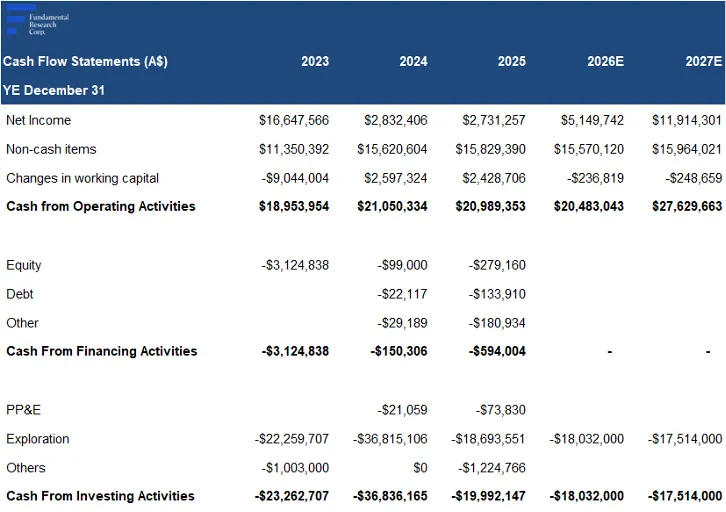

FRC Projections and Valuation

Source: FRC

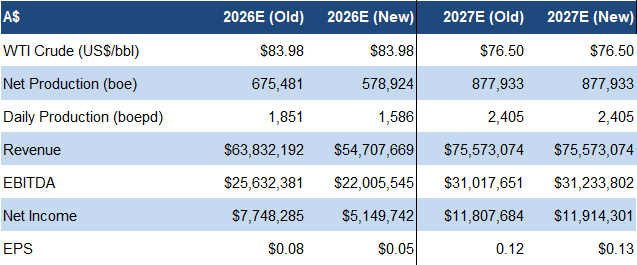

In light of softer-than-expected Q1 production, we are revising down our 2026 revenue and EPS estimates, while leaving our long-term forecasts largely unchanged

As a result, our DCF valuation declined from $2.12 to $2.09/share

We assume two new wells per year, reaching 28 total wells by 2034

Source: FRC

For conservatism, we assign no value to upside from further development of the Simpson and Caney Shale formations within the existing land position, or from broader regional exploration and development opportunities

We reiterate our BUY rating, and maintain our fair value estimate of $1.62/share (the average of our DCF and comparables valuations). BRK trades at a material discount to peers, presenting an attractive opportunity. Q1 softness reflects natural decline dynamics, rather than structural weakness, while underlying fundamentals remain strong. With a deep resource base, and a robust balance sheet, we believe BRK is well positioned for production growth.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- Production and projections are highly dependent on oil prices

- Oil prices are volatile, and influenced by macroeconomic and geopolitical factors

- Exploration and drilling success is uncertain

- High upfront costs associated with drilling and completing new wells

- Regulatory, environmental, and permitting requirements may affect operations

- Access to financing may be sensitive to commodity price cycles

We are maintainingour risk rating of 3 (Average)

APPENDIX