Disclosure: Millennial Potash Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

Price and Volume (1-year)

* Qualified Person: Peter J. MacLean, Ph.D., P.Geo., Director of MLP. *Millennial Potash Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures are in C$, except for commodity prices, which are in US$ (FOREX rate US$:C$ = 1.37)

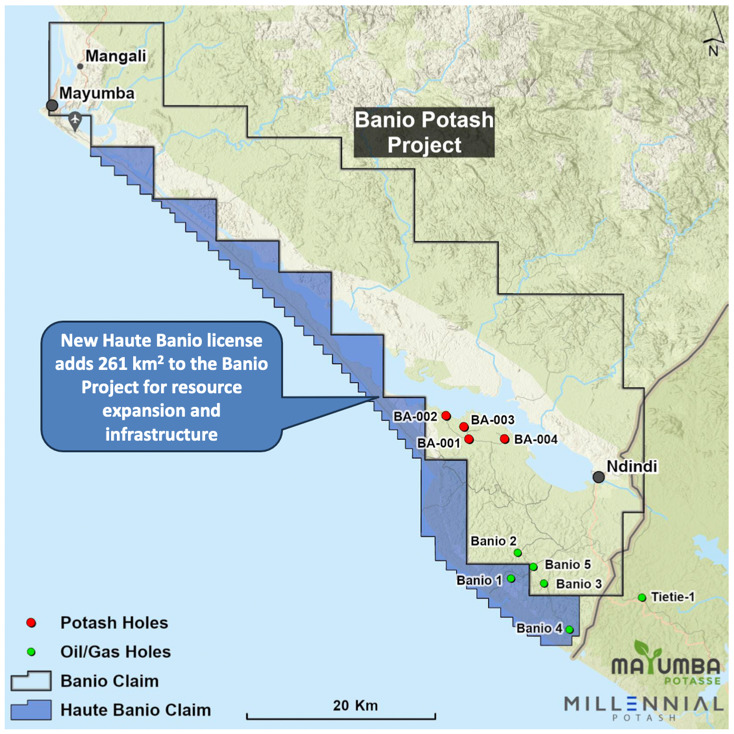

Banio Potash Project, Gabon

MLP has secured a new 261 km² exploration permit next to its main area, expanding the project to 1,500 km². Management plans to start drilling in H2- 2026 to see if the current resource extends into this new permit area.

Gabon has an established mining and oil & gas sector, operated by major international companies such as Fortescue (ASX: FMG), Eramet (ENXTPA: ERA), Total (NYSE: TTE), and Shell (NYSE: SHEL), showing strong foreign investment, and infrastructure capable of supporting large projects

Location Maps

The new permit is strategically important because it includes a coastal road and access to the ocean, providing potential infrastructure routes to support project development

Source: Company/FRC

MLP plans to export its products to the U.S., Brazil, and elsewhere in Africa via the Mangali port

Ongoing construction of a deep-water port, and power plant, funded by a Gabonese government-led group, should meaningfully reduce operational risks

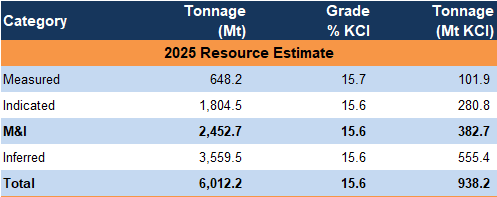

2025 Resource Estimate

(QP: Sebastiaan van der Klauw , EurGeol . Of ERCOSPLAN and Peter J. MacLean, Ph.D., P.Geo , Director of MLP)

Banio hosts a deposit large enough for at least 25 years of production

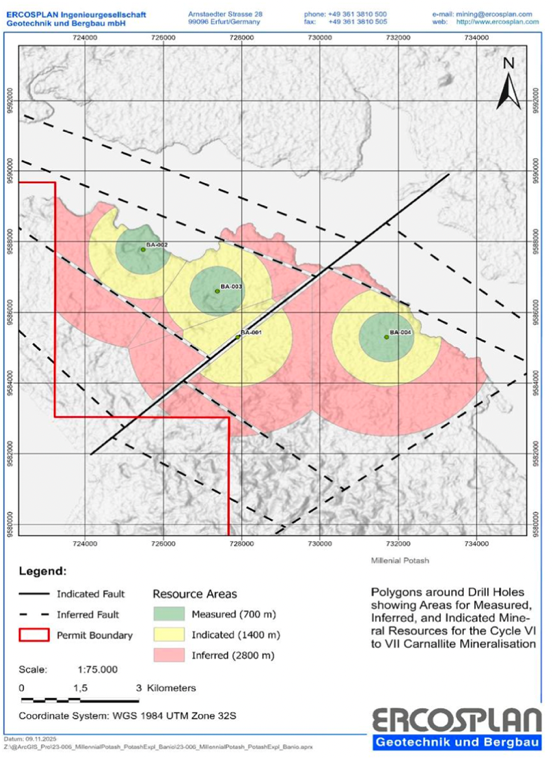

Resource Envelope

Source: Company

We see potential for resource expansion, since the deposit remains open in multiple directions, and the current resource covers just 5% of the project area

(QP: Peter J. MacLean, Ph.D., P.Geo , Director of MLP)

Source: Company /FRC

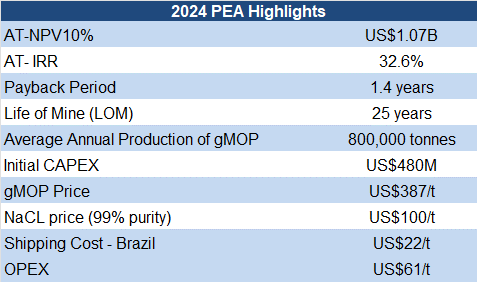

The 2024 PEA returned an AT-NPV10% of $1.47B, and an IRR of 33%, using $387/t gMOP; potassium chloride (spot: $373/t); we view IRRs above 25% as attractive in mining

OPEX and CAPEX are relatively low as the deposit is amenable to solution mining, compared with conventional underground potash mining

Management’s Target Timelines

Source: Company

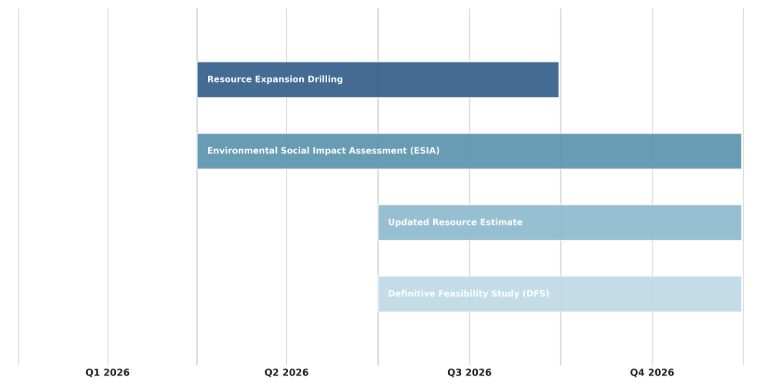

The company aims to finish resource expansion drilling by Q3, followed by a resource update, ESIA, and a feasibility study by year-end

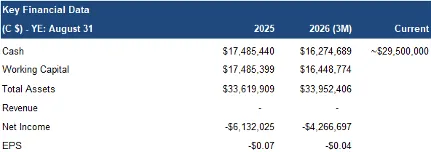

Financials

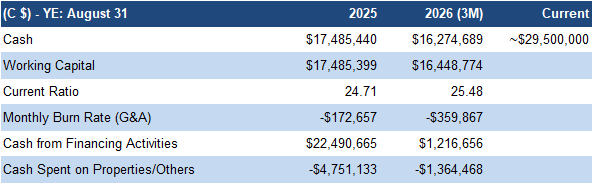

Strong balance sheet

Source: FRC / Company

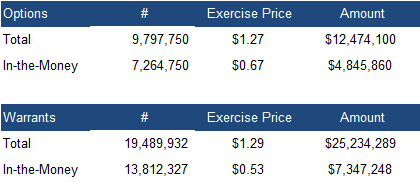

In-the-money options and warrants can bring in $12M

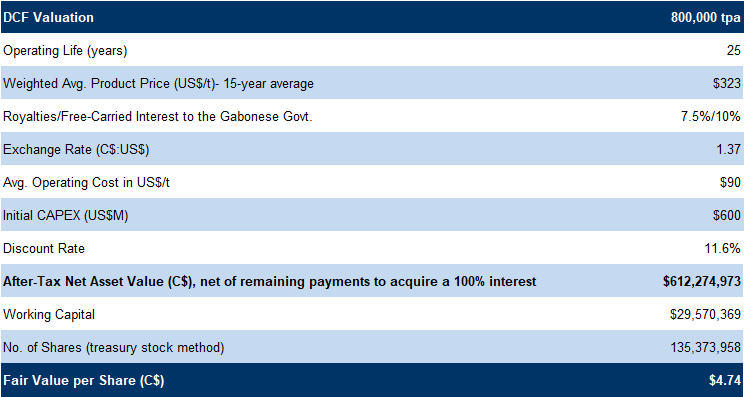

FRC Valuation

We are not making any material changes to our valuation model, aside from adjusting for a 3% appreciation in the US$

As a result, our DCF valuation fell slightly from $4.80 to $4.74/share

Source: FRC

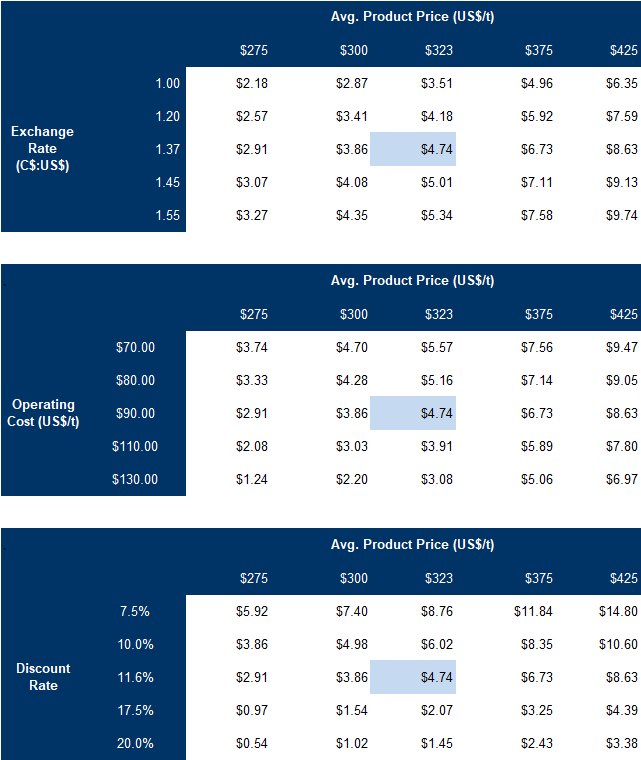

Our valuation is highly sensitive to key inputs

We are reiterating our BUY rating, and adjusting our fair value estimate from $4.80 to $4.74/share. We believe MLP is well- positioned to benefit from potash market tightness, strong institutional backing, and a strategically located project with robust economics. It is trading at a significant discount to NPV. Key catalysts in H2 - 2026, including resource drilling, ESIA, feasibility study completion, and potential M&A.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

We are maintaining our risk rating of 5 (Highly Speculative)