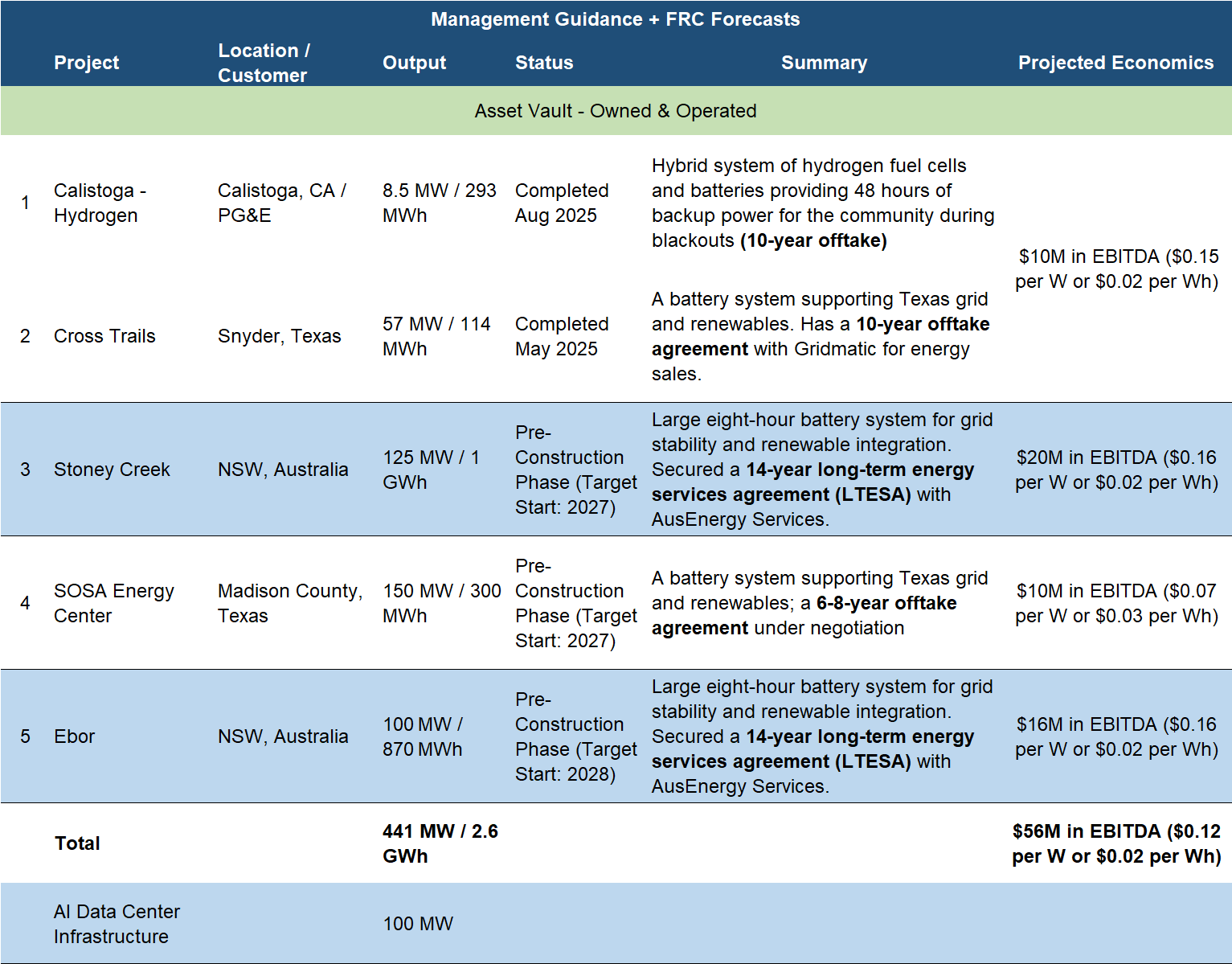

- New Australian Project: In February 2026, NRGV announced a 100 MW / 870 MWh energy storage project in New South Wales, with a long-term government-backed offtake agreement, supporting stable recurring revenue. This marks the fifth Asset Vault project, bringing the portfolio to 441 MW/2.6 GWh, with potential to generate $50-$60M in EBITDA annually. In addition, the company announced initiatives totaling another 100 MW related to AI data centers, highlighting NRGV’s expansion into AI-focused infrastructure.

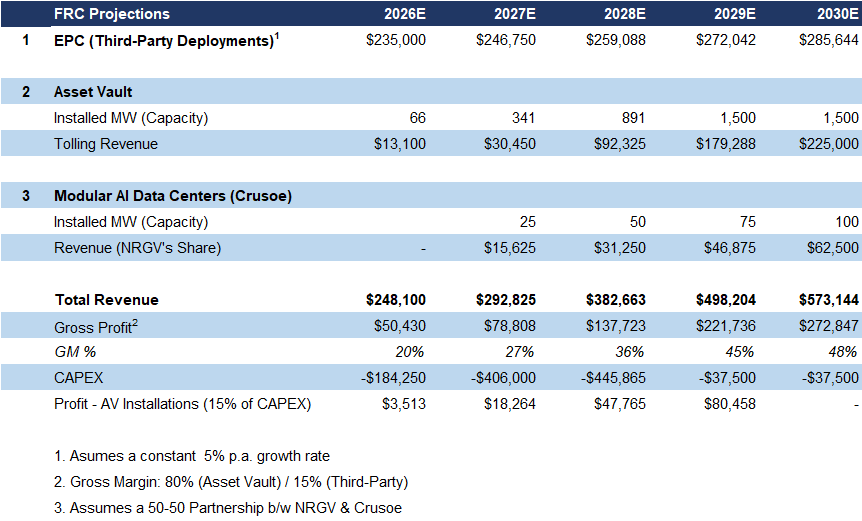

- Asset Vault Scaling: Asset Vault is targeting $100–$150M in annual recurring EBITDA within four years across ~1.5 GW of capacity. Of the five projects currently in the platform, two are operational, with the remaining three expected to come online in 2027–2028.

- Supportive Market Tailwinds: Market outlook remains robust given rising power demand, renewable adoption, and grid reliability needs. Key drivers include AI data centers, and renewable integration. Recent geopolitical tensions in the Middle East, and resulting spikes in oil prices, have further underscored the need for diversified and resilient energy systems, enhancing the attractiveness of energy storage solutions.

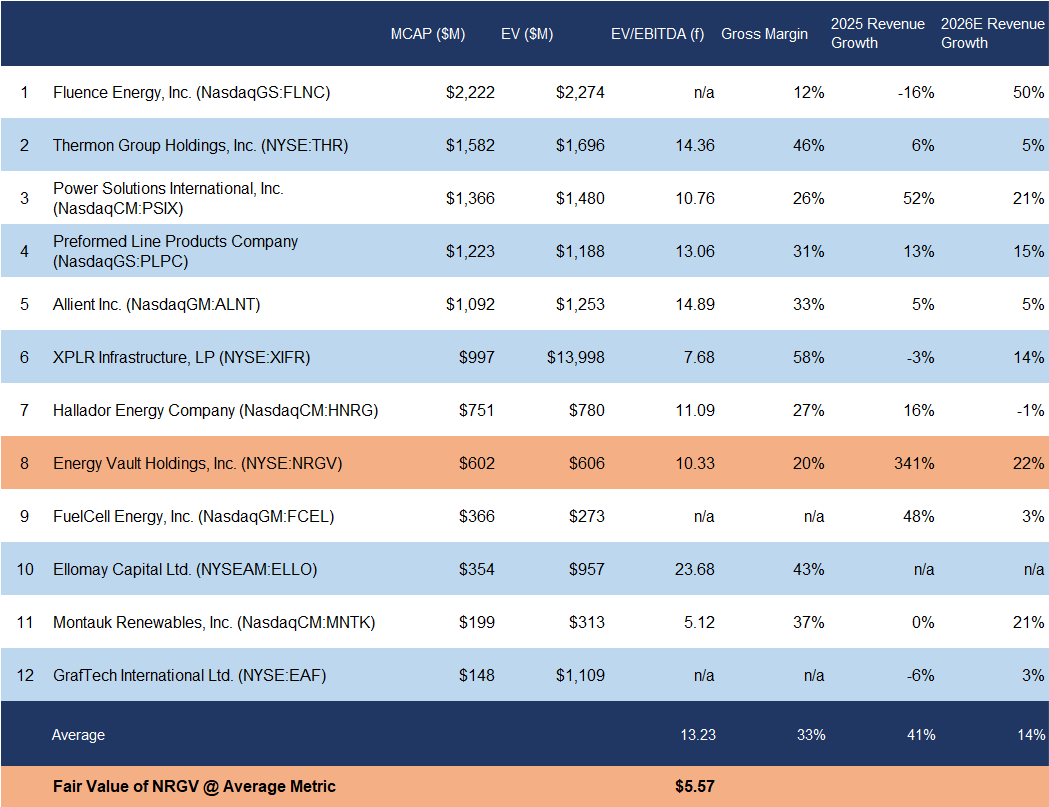

- Valuation Discount: NRGV is trading at 10.3x forward EBITDA vs the sector average of 13.2x, a 22% discount.

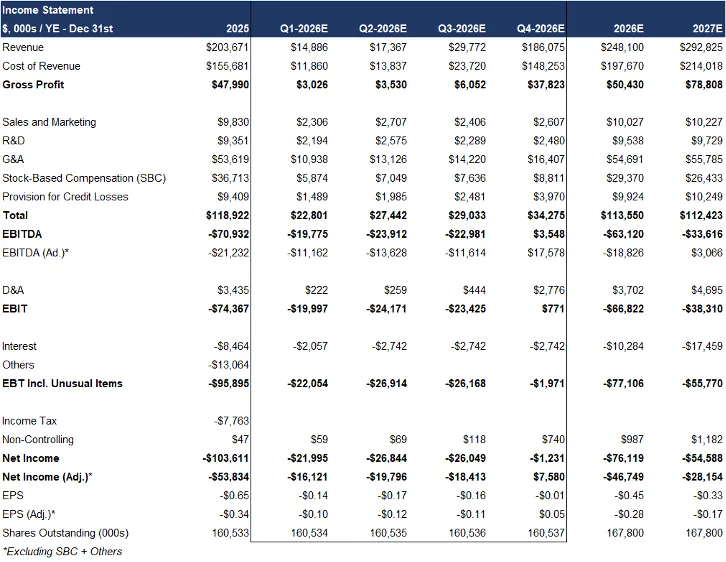

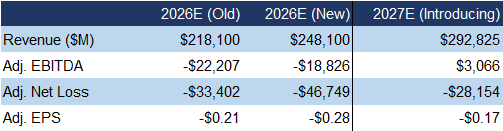

- 2026 Guidance & Outlook: Management guides 2026 revenue of $225–$300M (~30% YoY growth); we raise our estimate by 14% to $248M.

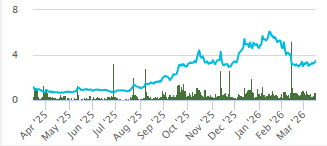

Price and Volume (1-year)

| |

YTD |

12M |

| NRGV |

-27% |

299% |

| NYSE |

-1% |

13% |

* Energy Vault Holdings has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in US$ unless otherwise specified.

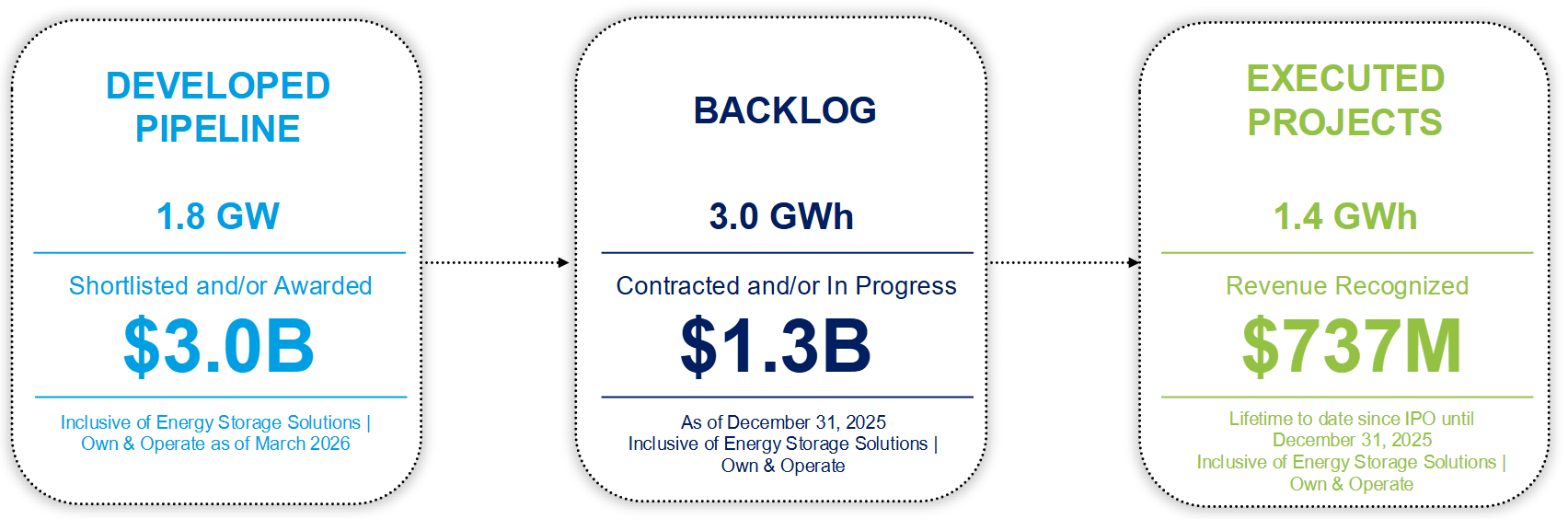

By the end of 2025, NRGV had $1.3B in contracted backlog (Q3: $0.9B), and $3B in its pipeline (Q3: $2.1B), largely driven by tolling revenue from company-owned projects

Project Pipeline

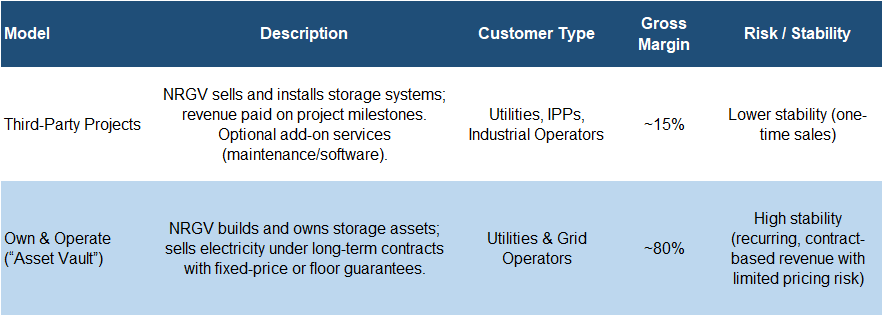

Business Model

Source: Company / FRC

Low-margin third-party vs high-margin recurring Asset Vault revenue

Key Recent Developments:

- In February 2026, NRGV announced plans to construct a 100 MW / 870 MWh energy storage project in New South Wales, Australia. The project has already secured a long-term energy sales agreement with a government-backed counterparty, indicating the potential for stable, recurring revenue. This will be the fifth project in NRGV’s Asset Vault portfolio, bringing the total portfolio to 441 MW/2.6 GWh. We note that construction costs for the new project are estimated at A$310 M (≈$0.25/Wh), broadly in line with other projects in the portfolio.

- In addition, NRGV announced a partnership with a manufacturer of sodium-ion energy storage systems to co-develop a platform targeting AI data centers. Sodium-ion technology offers potential advantages over conventional energy storage for high-intensity, fast-cycling applications typical in AI infrastructure. We believe this partnership underscores NRGV’s expansion into AI-focused infrastructure, and strengthens its technology differentiation versus competitors.

Asset Vault Structure & Economics

*Project economics depend on storage duration; duration refers to how long a system can supply power ; longer-duration projects earn more EBITDA per MW (e.g., Sosa: two-hour → $0.07/W, Stoney Creek: eight-hour → $0.16/W)

*CAPEX to build a system is ~$0.30/Wh in the U.S. , and ~$0.20/ Wh outside the U.S.

Source: Company / FRC

Asset Vault targets $100–$150M in annual recurring EBITDA within four years across 1.5 GW, with the five current projects (441 MW) expected to generate $50-$60M EBITDA (~$0.12/W)

Financials

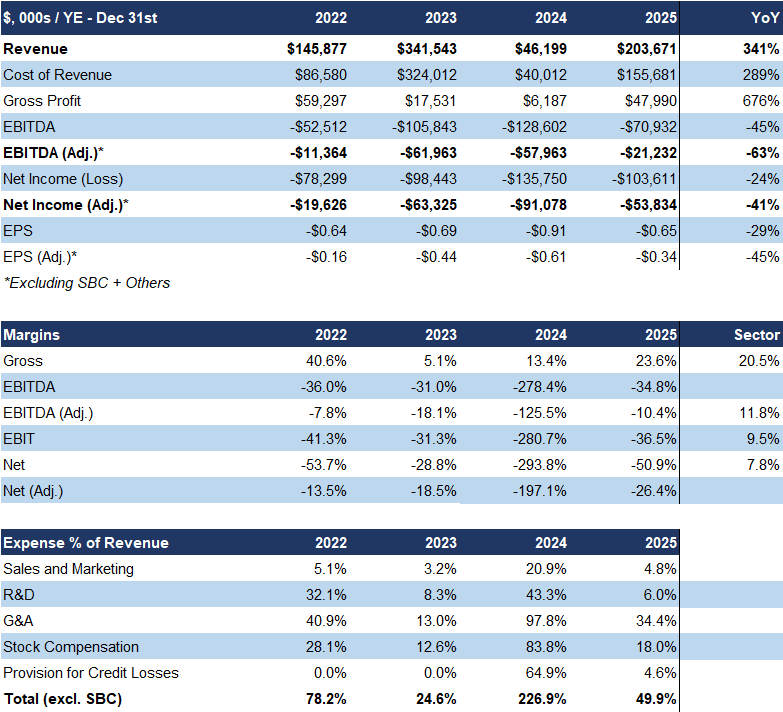

2025 revenue, dominated by third-party deployment projects, up 341%, beating our estimate by 7%

Gross margins improved 10 pp to 24%, exceeding our estimate by 8 pp, due to a higher mix of higher-margin project deployments

Operating expenses were down 12% YoY, and came in 10% above our estimate

Adj. EPS improved from ($0.61) to ($0.34) vs our estimate of ($0.35)

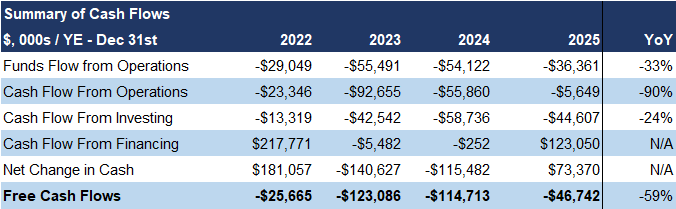

Free cash flows improved as well

Source: FRC / Company

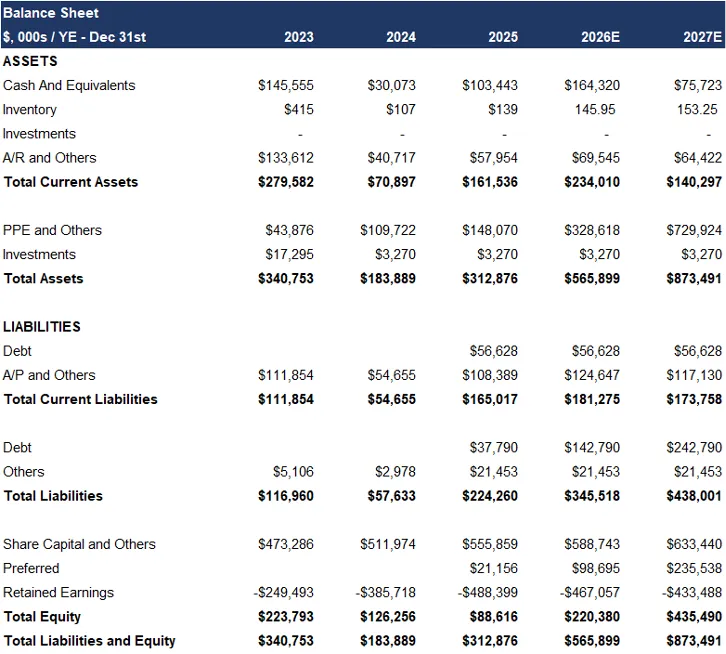

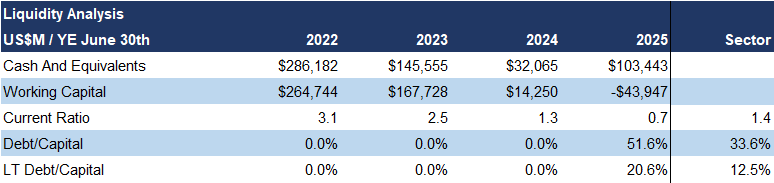

At the end of 2025, the company had $103M in cash

In Q1-2026, the company closed a $150M debt financing, and used part of the proceeds to pay down higher-rate debt, effectively reducing financing costs

FRC Valuation and Rating

Given stronger-than-expected revenue, and management’s upbeat guidance, we are raising our revenue forecast, but lowering our EPS forecast, due to higher-than-expected operating expenses

Source: FRC

We are raising our longer-term revenue forecasts following the company’s recent AI-related data center initiatives

We anticipate ongoing project additions for Asset Vault, growing total capacity to 1.5 GW by 2029 (unchanged)

Source: FRC

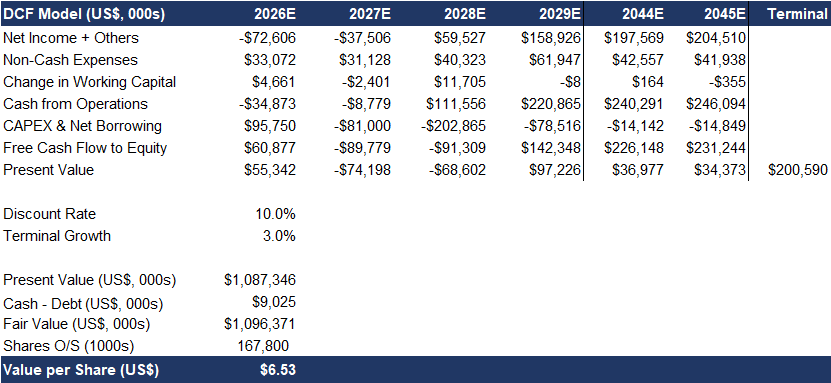

As a result of the above changes, our DCF valuation increased from $4.91 to $6.53/share

*We use the present value of our 2029 EBITDA estimate on NRGV in this calculation.

Source: FRC / S&P Capital IQ

NRGV is trading at 10.3x forward EBITDA (previously 13.2x) vs the sector average of 13.2x (previously 15.2x); applying the sector multiple yields a comparables valuation of $5.57/share (previously $5.47/share)

We are reiterating our BUY rating , and adjusting our fair value estimate from $5.19 to $6.05/share (the average of our DCF and comparables valuations). NRGV delivered a strong 2025, with revenue and EPS beats, a growing backlog, and positive Q4-EBITDA, underscoring momentum across both third-party deployments, and the Asset Vault platform. With the stock trading at a 22% discount to peers , and our increased DCF valuation, we see meaningful upside potential .

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- Tariffs: U.S. tariffs on Chinese lithium-ion imports may raise costs

- Policy: Changes in green energy incentives could reduce demand

- Credit: Most large utilities and IPPs are low-risk counterparties, while smaller industrial clients and new partners carry higher default risk

- Compliance: Projects must meet all regulations and permits

- Financing: High upfront costs require funding

- Sales Cycle: Long nine-to-18-month installation delays revenue

- FOREX

While the company operates in a relatively low-risk market with potential for long-term steady cash flow, we believe its early-stage deployment of energy storage projects warrants a risk rating of 4 (Speculative)

APPENDIX