Disclosure: Noram Lithium Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

The analyst’s rating and fair value are one click away. Free FRC account, no credit card.

Already have an account?

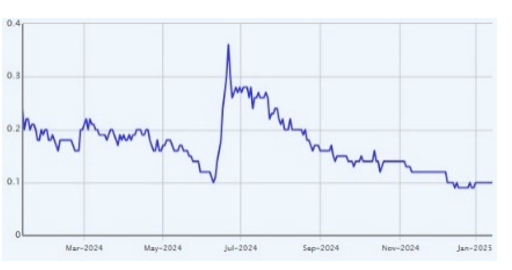

Price Performance (1-year)

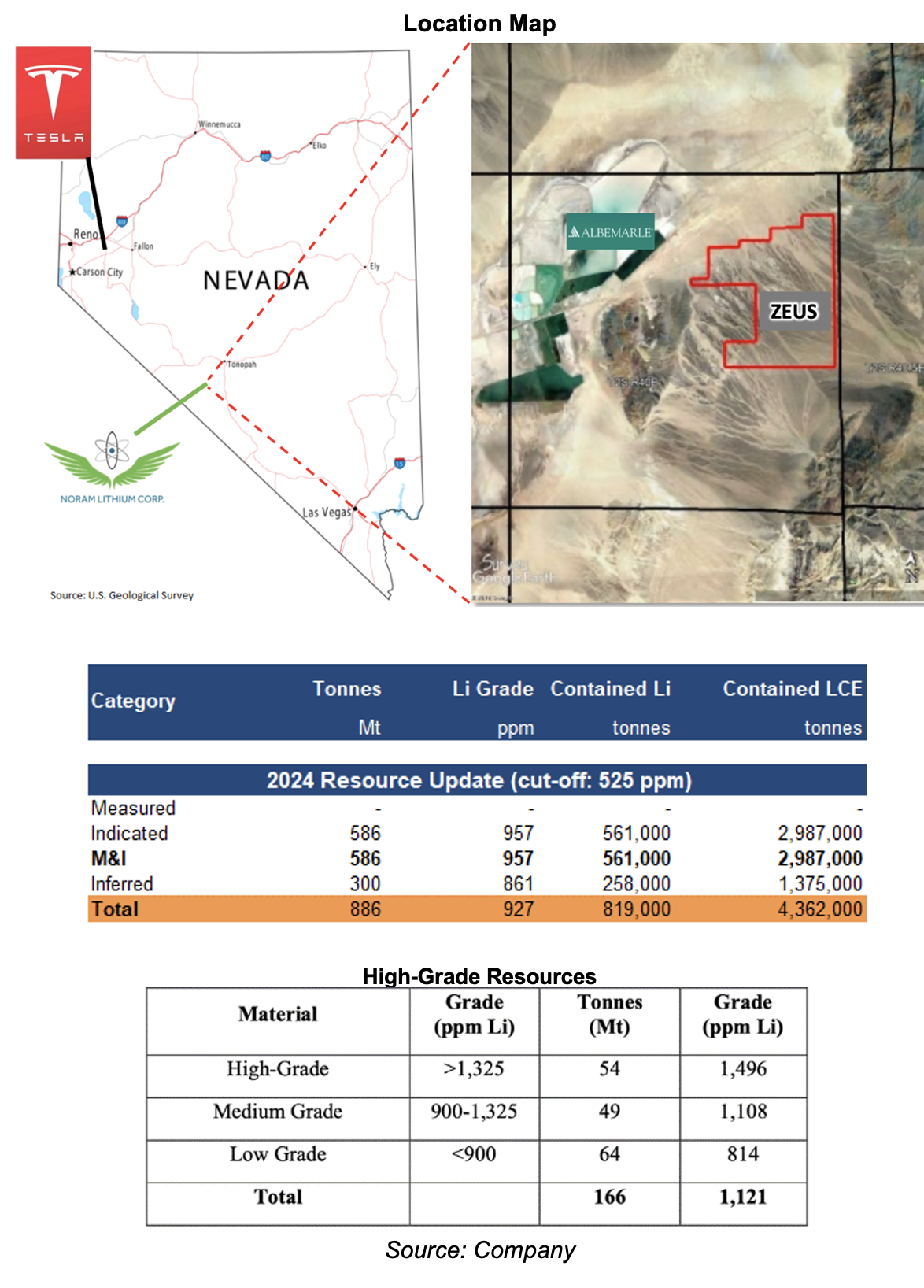

Located 220 miles southeast of Reno, Nevada. Lies in the Clayton Valley, adjacent to Albemarle’s Silver Peak lithium brine operations. Excellent infrastructure in place, including power and paved road access

4.4 Mt in resources at 927 ppm. Majority of resources occur near surface, implying potential for lower OPEX. This resource has a high-grade component totaling 1 Mt at 1,121 ppm

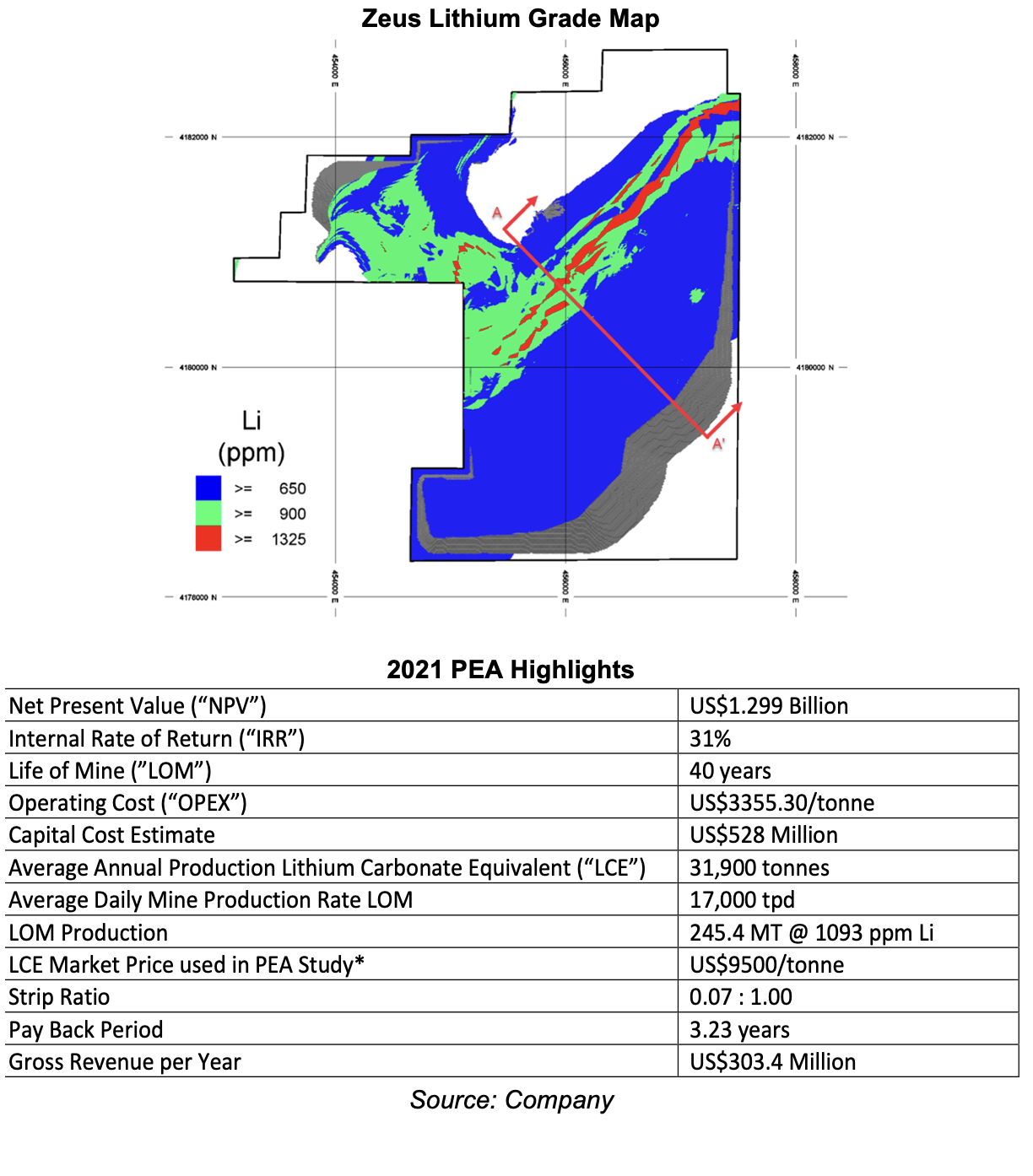

The high-grade portion alone has the potential for a mine life of over 40 years. A 2021 PEA had returned an AT-NPV8% of US$1.30B, and a high AT-IRR of 31%, using US$9.5k/t LCE vs a spot price of US$10 k/

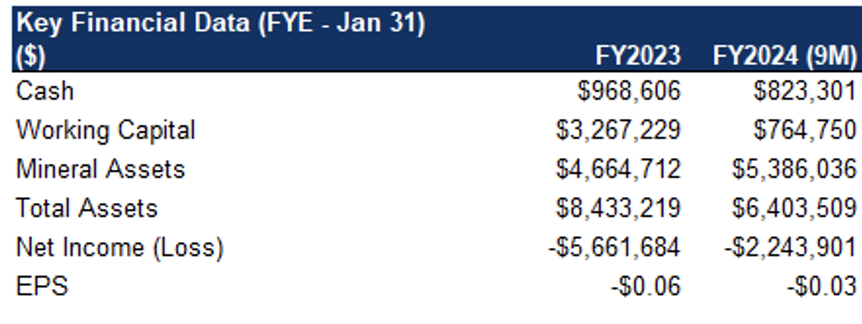

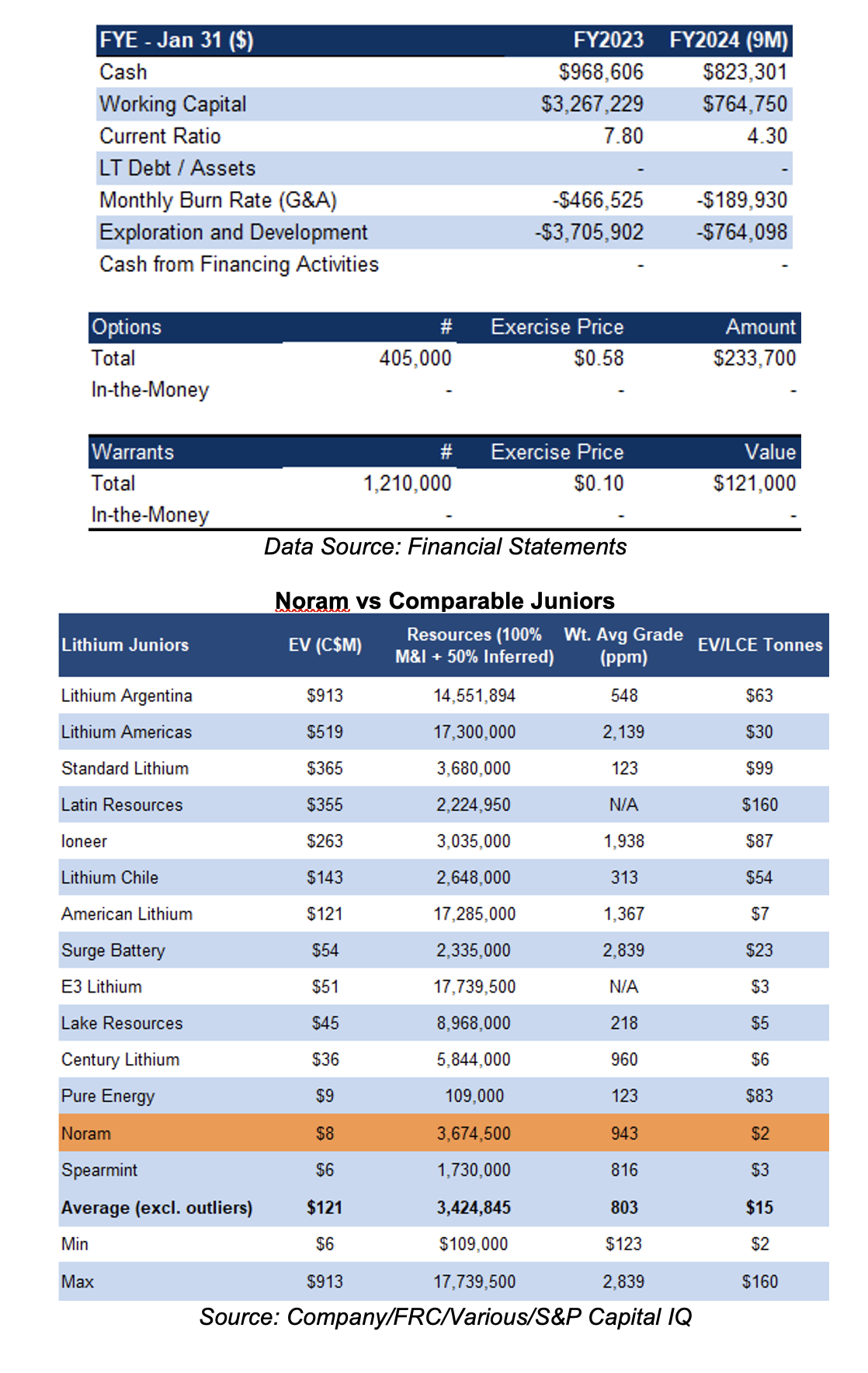

Financials

Healthy balance sheet, with no debt. We note that Zeus’ resources and grades are comparable to other well-known advanced projects

NRM is the most undervalued lithium junior on our list. NRM is trading at $2/t LCE vs the sector average of $15/t, an 85% discount. Applying $15/t to NRM’s resources, we arrived at a comparables valuation of $0.56/share

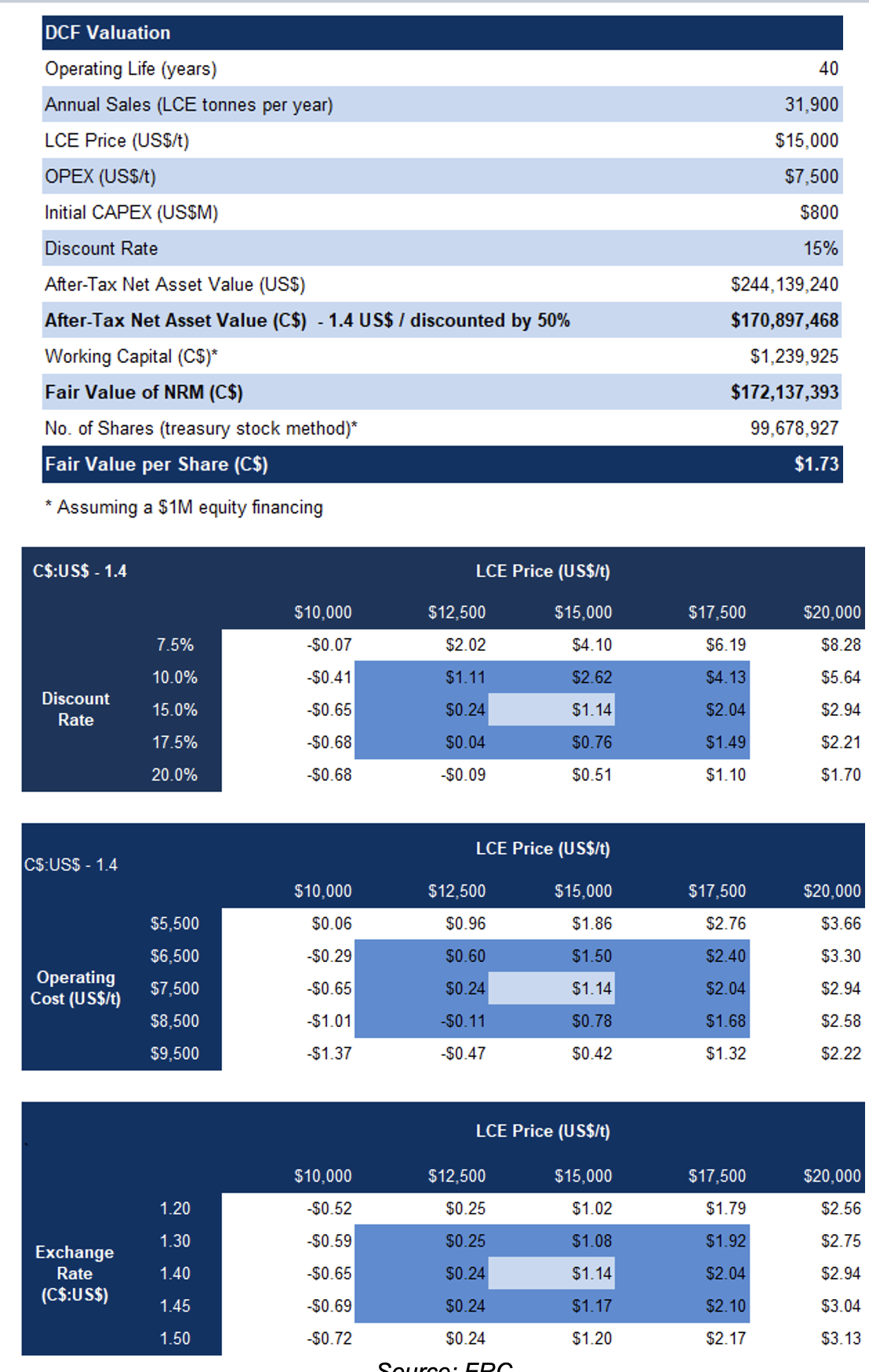

Our DCF valuation is $1.73/share. The average of our DCF and comparables valuation is $1.14/share. Our valuation is highly sensitive to lithium prices

We are assigning a BUY rating, with a fair value estimate of $1.14/share. We expect the lithium market to rebound, creating opportunities for undervalued juniors like NRM to gain investor attention. NRM is the most undervalued lithium junior on our list, trading at a steep discount to Zeus’ NPV, highlighting its strong upside potential. Located in a strategic region near major lithium projects, NRM is well-positioned for potential M&A or consolidation, further enhancing its appeal.

Risks

We are assigning a risk rating of 5

We believe the company is exposed to the following key risks (not exhaustive):