Atrium Mortgage Investment Corporation

Reports Record Revenue and EPS Despite a Spike in Loan Loss Provisions

ByFRC Team

.webp&w=1920&q=75)

Disclosure: Atrium Mortgage Investment Corporation has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

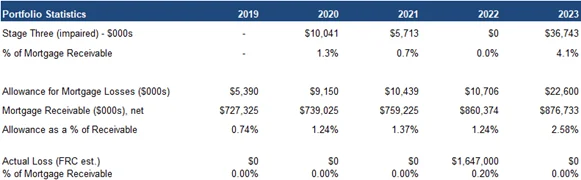

Loan loss provisions were up 521% YoY, and 13% higher than our forecast. Property developers, and landlords, have been hit harder than individual homeowners due to higher borrowing costs, low presales, and dampened real estate activity. As a result, AI’s stage three mortgages (impaired) increased by 62% QoQ to $37M (4% of the portfolio). In the earnings call, AI’s management noted that that in the event of needing to foreclose on collateral assets, there would be ample equity to recover the vast majority of invested capital. We find this realistic, given that AI has first priority on most of its mortgages, with a low portfolio average LTV of 61%.

Despite the recent uptick in inflation, and downtick in unemployment, we anticipate the Bank of Canada will cut rates by June/July 2024, driven by rising financial instability, and mortgage costs. We believe transaction volumes will pick up in H2-2024, driven by lower interest rates.

Our 2024 dividend forecast of $1.10/share (previously $1.07/share), reflects a yield of 9.7%. Anticipating a decline in rates in H2-2024, we find high-yielding funds, such as AI, increasingly appealing.

Portfolio Update

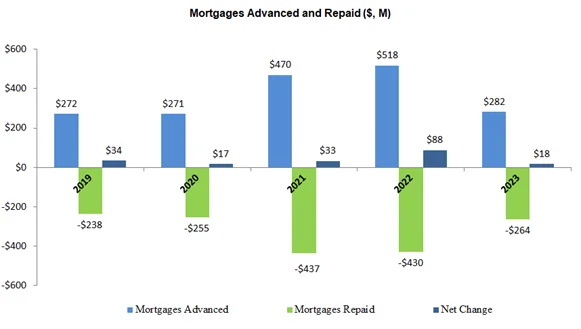

Loan advancements were down 46% YoY; repayments were down 39% YoY

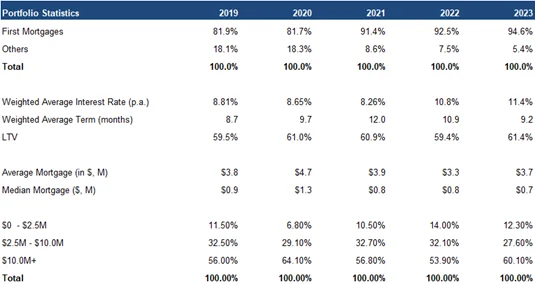

Net mortgages outstanding were up 2% YoY to $877M vs our forecast of $830M

Exposure to first mortgages increased LTV increased as well

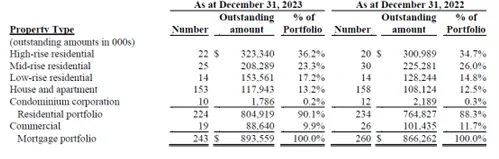

Mortgages By Property Type

Source: Company Data/FRC

No material changes in exposure by property-type

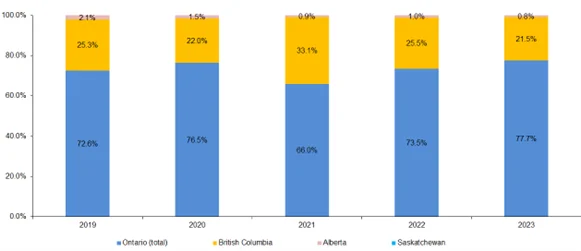

Mortgages by Region

Increased exposure to ON

Source: FRC/Company

No realized losses

However, stage three (impaired) mortgages increased by $14M QoQ, and $37M YoY, to 4.1% of the portfolio

As a result, loan loss allowances increased by 52 bps QoQ, and 133 bp YoY, to 2.6% of the portfolio

Source: FRC

We are raising our forecast for 2024 loan loss provisions from $5M to $15M

In summary, we believe the portfolio’s risk profile has increased due to higher stage three mortgages

Financials

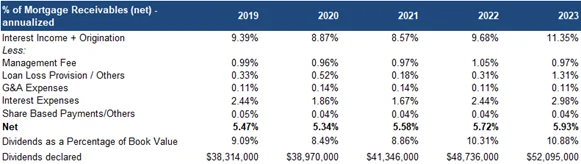

2023 revenue was up 26% YoY, and EPS was up 9% YoY

Revenue was 2% higher than our forecast, while EPS was exactly in line

Dividends increased from $1.13 to $1.19/share vs our forecast of $1.17/share

Debt to capital decreased by 0.6 pp, and remains within historic levels (40%-45%)

FRC Forecasts

Source: FRC

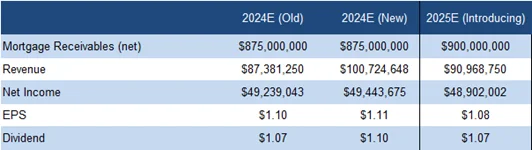

We are raising our 2024 EPS forecast to account for higher lending rates, partially offset by higher loan loss provisions

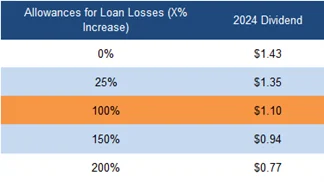

Our estimate for the 2024 dividend varies between $0.77 and $1.43/share, using various YoY increases in loan loss allowances

Source: FRC

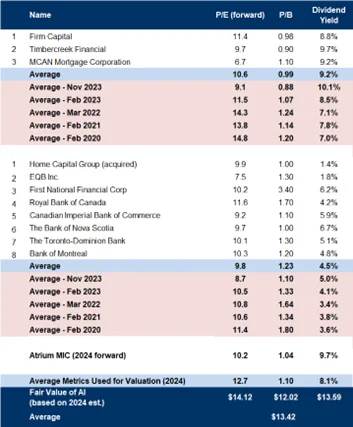

Comparables Analysis and Valuation

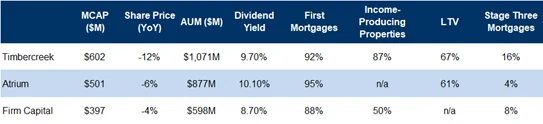

Atrium is the second largest publicly traded MIC, with a higher percentage of first mortgages, lower loan-to-value mortgages, and higher yield

Sector multiples are up 12% since our previous report in November 2023, and 24% below pre-pandemic levels

Our fair value estimate increased from $13.34 to $13.42/share primarily due to higher sector multiples

Source: S&P Capital IQ/FRC

We are reiterating our BUY rating, and adjusting our fair value estimate from $13.34 to $13.42/share, implying a potential return of 28% (including dividends) in the next 12 months. As we expect rates will start declining in H2-2024, we anticipate an increase in appetite for high-yielding stocks, such as AI. Key risks include a softer mortgage origination market, and higher default rates.

Risks

We believe the company is exposed to the following risks:

- Diversification – over 70% of Atrium's mortgages are secured by properties in ON

- Credit

- A downturn in the real estate sector may impact the company’s deal flow

- Timely deployment of capital is critical

- Investments in mortgages are typically affected by macroeconomic conditions, and local real estate markets

- Highly competitive sector

- Like most MICs, the company uses leverage to fund mortgages

- Default rates can rise during recession