SPC Nickel Corp.

Delineates a Large Open-Pittable Nickel Resource

Published: 1/31/2024

Author: Sid Rajeev, B.Tech, CFA, MBA

Sector: Basic Materials | Industry: Other Industrial Metals & Mining

| Metrics | Value |

|---|---|

| Current Price | US $0.04 |

| Fair Value | US $0.33 |

| Risk | 5 |

| 52 Week Range | US $0.045 |

| Shares O/S (M) | 0.135 |

| Market Cap. (M) | US $7 |

| Current Yield (%) | n/a |

| P/E (forward) | n/a |

| P/B | 4.9x |

Already a subscriber?

Want to know the fair value of the stock?

Subscribe for free to get exclusive insights and data.

Report Highlights

Highlights

SPC has completed a maiden resource estimate for its West Graham Deposit (WGD) within the Lockerby East project in Sudbury, Ontario.

SPC has confirmed and expanded historic resources, with contained NiEq increasing by 31% (329 Mlbs to 430 Mlbs), and the average grade rising by 28% (0.54% to 0.70%).

91% of resources are open-pittable, implying potential for relatively low OPEX/CAPEX. We view WGD as a large-tonnage deposit, with attractive grades for potential open-pit operations.

We see potential for resource expansion as the WGD remains open in multiple directions. Additionally, the current estimate excludes the high-grade LKE deposit, located 200 m from the WGD.

SPC is currently updating the historical resource of its LKE deposit, which we believe will likely be followed by a PEA encompassing both WGD and LKE.

BHP (ASX: BHP), First Quantum Minerals (TSX: FM), and Wyloo Metals, are temporarily suspending production at some of their nickel mines in Australia due to a 46% YoY decline in prices, driven by slower global GDP growth, and rising supply. LME inventories are up 40% YoY. We foresee these production shutdowns exerting upward pressure on prices. We are anticipating nickel to average US$8.75/lb this year vs the current spot price of US$7.30/lb.

We maintain a positive outlook on juniors focused on EV metals. Battery/EV manufacturers/miners are actively seeking stable/long-term supply sources of EV metals. Earlier this month, Sumitomo Metal Mining (TSE: 5713) acquired a 10% interest in nickel junior FPX Nickel Corp. (TSXV: FPX) for $14M, or $0.48/share, reflecting a 45% premium over FPX’s last closing price.

SPC is trading at $0.02/lb vs the sector average of $0.13/lb, an 89% discount.

Upcoming catalysts include a resource update, PEA, and positive sentiment on EV-metal juniors.

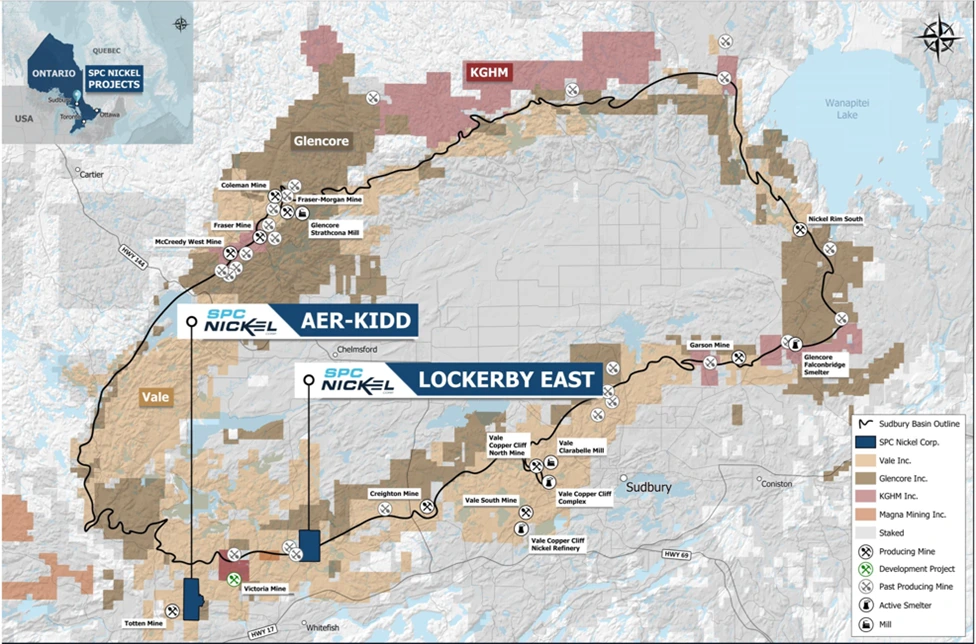

Maiden Resources for the WGD, Lockerby East Project

The Lockerby East project encompasses the West Graham Deposit (WGD), and the LKE deposit.

Project Location

Located adjacent to past-producing mines in the Sudbury camp, one of the richest mining districts in the world

We believe the proximity to active mills allows SPC to potentially expedite projects to production quickly with a relatively low CAPEX

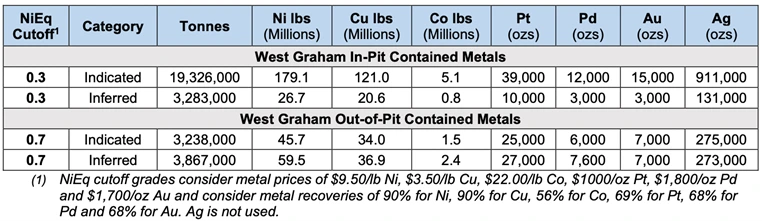

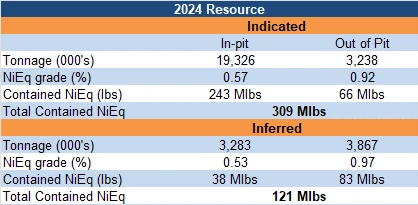

West Graham Resource Estimate

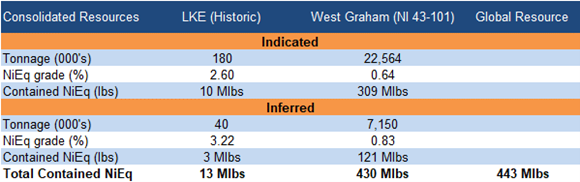

The maiden NI 43-101 compliant resource estimate, which was based on 67-holes/14,180 m, has confirmed and expanded historic resources

Source: Company/FRC

A large-tonnage deposit with indicated resources totaling 309 NiEq (0.64%), and inferred resources totaling 121 Mlbs (0.83%)

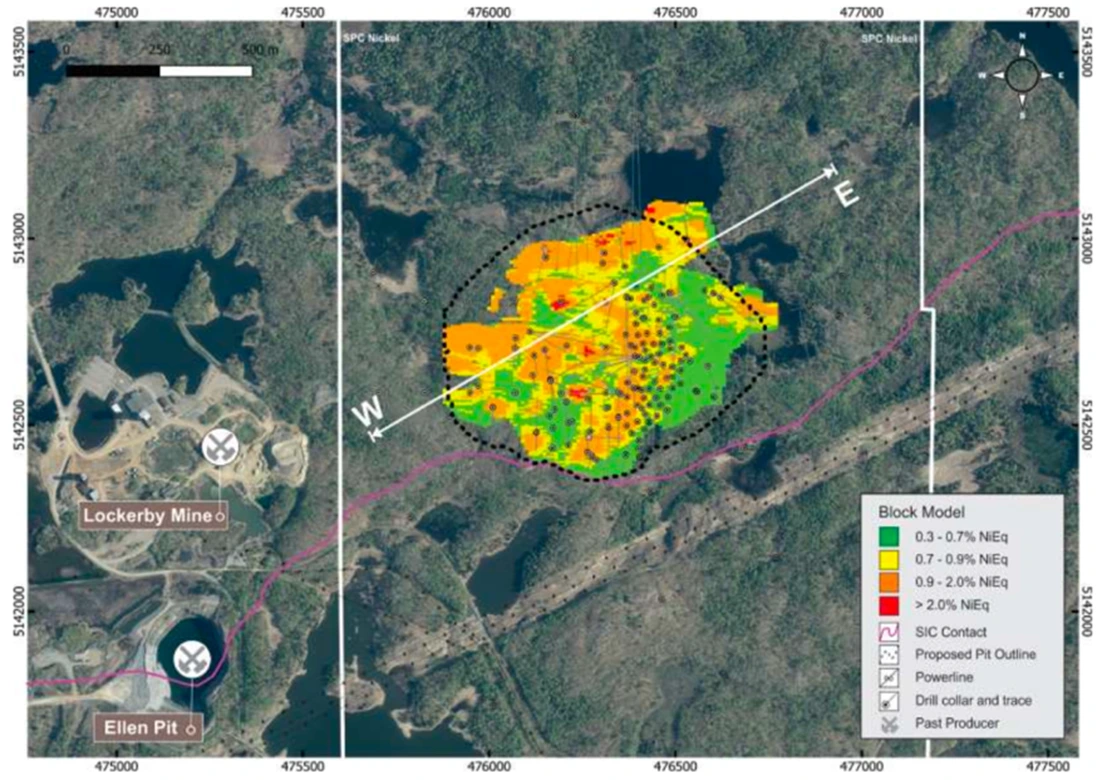

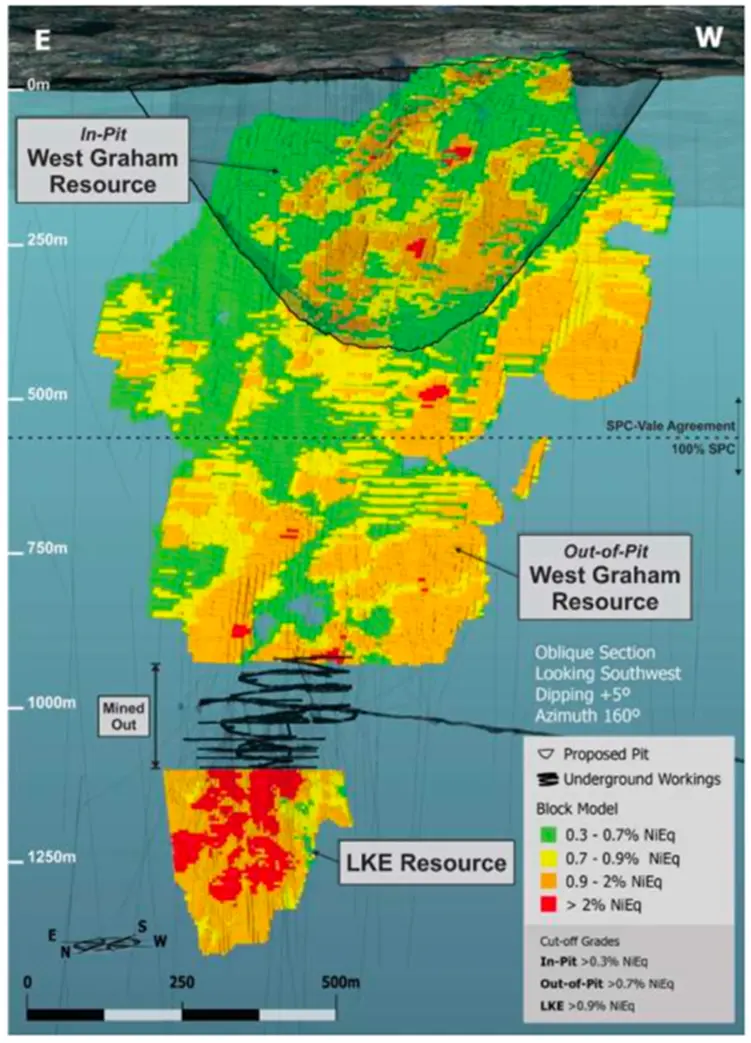

Resource Envelope

The resource envelope measures 900 m (length) x 3-60 m (width) x 1,000 m (depth)

Source: Company

91% of resources are open-pittable, implying potential for relatively low OPEX/CAPEX

Attractive grades for open-pit operations

We believe there is potential for resource expansion as the WGD remains open in multiple directions

In addition, the current estimate does not include the high-grade LKE deposit, located 200 m down dip of the WGD

Source: FRC/Company

In total, the Lockerby East project hosts 443 Mlbs of NiEq across its two deposits

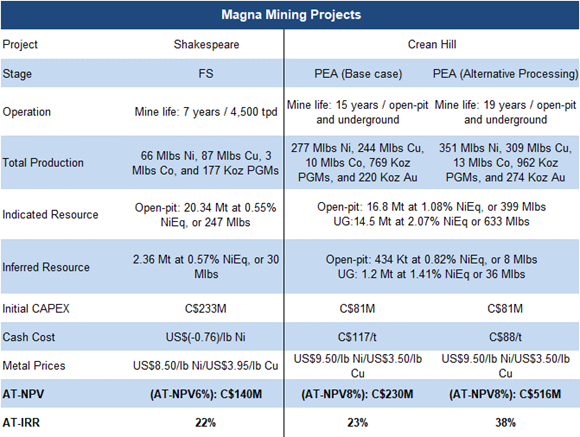

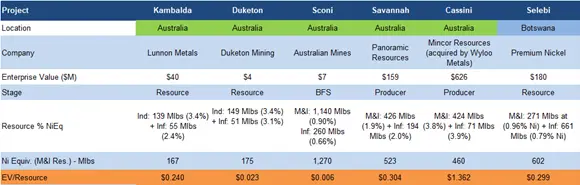

A direct comparable of SPC is Magna Mining (TSXV: NICU/MCAP: $64M). Magna is developing the historic Crean Hill mine, located 40 km southwest of Crean Hill. These projects share similar mineralogy, resources, and grades as SPC's propreties. A recent PEA on Crean Hill returned robust economics.

Source: Magna/FRC

We believe SPC should be able to demonstrate similar economics as its resources are similar to that of Magna

Upcoming Plans

SPC is currently updating the historical resource of its LKE deposit, which we believe will likely be followed by a PEA encompassing both WGD and LKE.

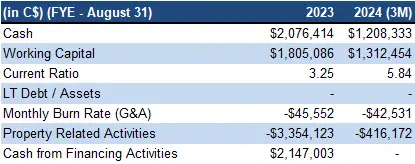

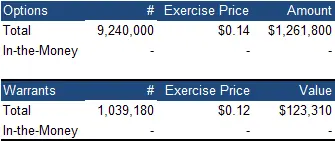

Financials

Source: Company Data/FRC

We believe SPC will likely raise $1-$2M through equity financings in H2-2024

FRC Valuation

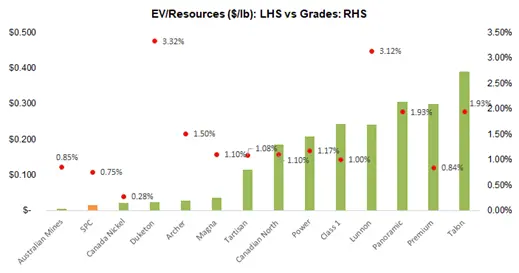

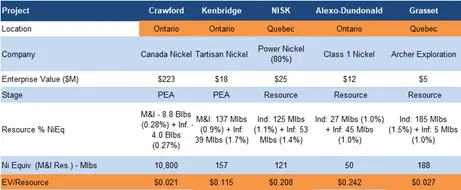

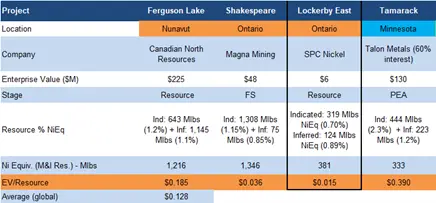

The following section compares SPC to other nickel juniors.

Source: FRC/ S&P Capital IQ/ Various

SPC is one of the most undervalued nickel juniors on this list

Juniors with higher grades generally exhibit a higher EV/lb

SPC is trading at $0.02/lb NiEq (previously $0.09/lb) vs the sector average of $0.13/lb (previously $0.29/lb), an 89% discount

Applying $0.13/lb to SPC’s resources, we arrived at a fair value estimate of $0.33/share (previously $0.28/share)

Source: FRC/ S&P Capital IQ/ Various

Valuation increased due to higher resources, partially offset by lower sector EV/lb

We are reiterating our BUY rating, and adjusting our fair value estimate from $0.28 to $0.33/share. Upcoming catalysts include a resource update, PEA, and positive sentiment towards juniors focused on EV metals. Despite the promising maiden resource estimate, SPC is down 25% since the announcement, reflecting broader weakness in the junior resource sector. We anticipate a rebound in small-cap stocks when the Fed starts cutting rates, possibly in Q2-2024.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- Sensitive to nickel prices

- Exploration and development

- Access to capital and potential for share dilution

- No guarantee that the company will be able to advance all of its projects simultaneously

- No economic studies