Millennial Potash Corp.

Leveraging Gabon's Strategic Location and Infrastructure Advancements

Published: 12/10/2024

Author: FRC Analysts

Sector: Basic Materials | Industry: Other Industrial Metals & Mining

| Metrics | Value |

|---|---|

| Current Price | CAD $0.29 |

| Fair Value | CAD $1.38 |

| Risk | 5 |

| 52 Week Range | CAD $0.17-0.36 |

| Shares O/S (M) | 77 |

| Market Cap. (M) | CAD $23 |

| Current Yield (%) | N/A |

| P/E (forward) | N/A |

| P/B | 2.0 |

Already a subscriber?

Want to know the fair value of the stock?

Subscribe for free to get exclusive insights and data.

Report Highlights

- Since our last report in May 2024, the Banio potash project area has seen considerable infrastructure development. Ongoing construction of a deep-port facility, and a power plant, is expected to greatly reduce operational risks for the project.

- MLP has raised $1.7M as part of an ongoing $3.8M equity financing (increased from the original $3.4M due to strong investor appetite), including $3M from an insider, to fund drilling and initiate environmental studies.

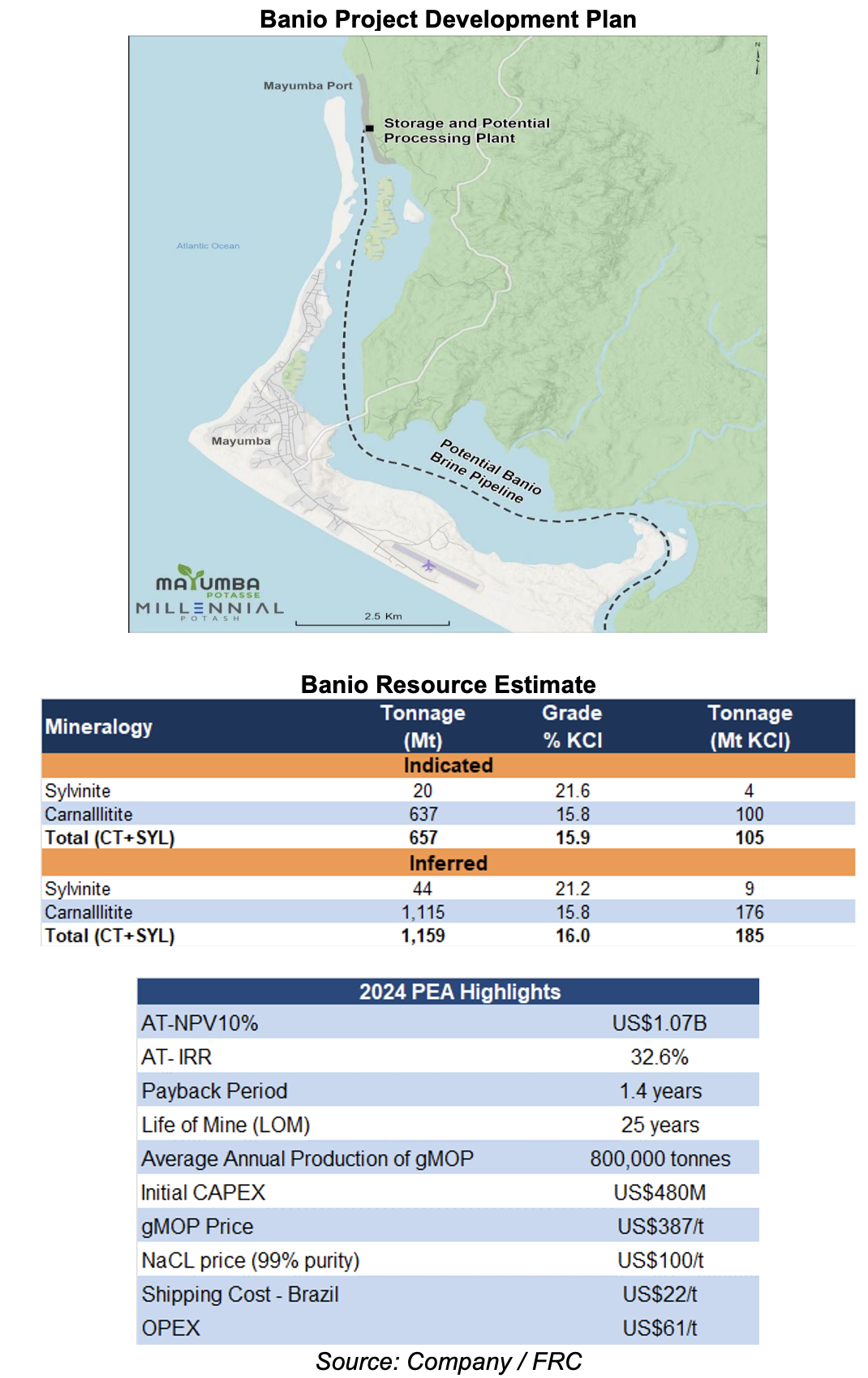

- The Banio project hosts a large-tonnage/low-grade potash resource. We believe there is significant resource expansion potential, as the deposit remains open in multiple directions, with the current estimate covering only 1.5% of the project area. MLP is targeting a resource update in Q1-2025.

- A Preliminary Economic Assessment (PEA) conducted earlier this year reported robust economics, with an AT-NPV10% of US$1.1B, and a high AT-IRR of 33%, using a long-term average price of US$387/t granular Muriate of Potash (gMOP). At the current spot price of US$278/t, the PEA would yield an AT-NPV10% of US$663M, and an after-tax IRR of 26%. MLP is trading at just 2% of the AT-NPV10% based on the spot price.

- The project can be advanced to production within three to four years. We believe Banio stands out among undeveloped potash projects with its comparatively low initial CAPEX of US$480M, and OPEX of US$61/t, attributed to its amenability to solution mining.

- The target markets for Banio’s potash are Brazil and Africa, both of which import most of their potash consumption. Gabon’s proximity to Brazil implies that MLP should have lower transportation costs than other potash suppliers.

- Potash prices are down 16% YoY, to US$278/t vs the 15-year average of US$302/t. Last month, the Belarusian President proposed consulting with Russia to reduce their combined production by 10% in an effort to boost prices. As Russia and Belarus account for approximately 35% of global potash supply, we believe the potash market is highly susceptible to supply chain disruptions.

- Upcoming catalysts include drilling, and an updated resource update

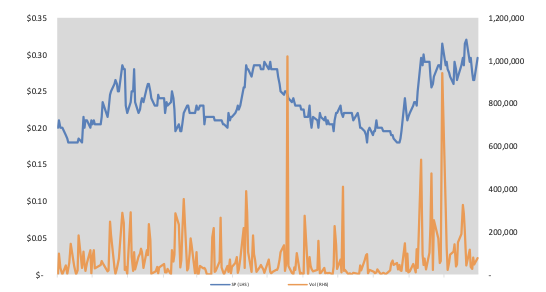

Price and Volume

Banio Potash Project

We believe that both the port and power plant will significantly reduce operational and transportation risks associated with the Banio potash project.

- The Gabonese government, in partnership with private investors, has initiated construction and development of the Mengali port in Mayumba. Phase one of this project is expected to be completed by 2025.

- Additionally, a new thermal power plant in southern Mayumba is under construction. This project is a joint venture between the Gabonese government, Gabon Power Company, and Perenco Oil & Gas Gabon. Phase one of the power plant is scheduled for completion in July 2025.

Gabon hosts several majors such as Fortescue (ASX: FMG), Eramet (ENXTPA: ERA), Total (NYSE:TTE), and Shell (NYSE: SHEL)

Located in the potash-rich Congo Evaporite basin in Gabon, which hosts several large potash deposits

MLP plans to transport the enriched brine extracted through solution mining via pipelines to a processing plant in Mayumba, located 50 km north of the Banio project. The processing plant will transform brine into granular fertilizer through evaporation, crystallization, drying, and compaction.

The company plans to ship the final product to its target markets via the Mengali port. Gabon’s proximity to Brazil gives MLP a transportation cost advantage over other global suppliers

Banio hosts a large-tonnage/low-grade potash deposit

At the current spot price of US$278/t, the PEA would yield an AT-NPV10% of US$663M, and an after-tax IRR of 26%. We note that OPEX/CAPEX are relatively low as the deposit is amenable to solution mining

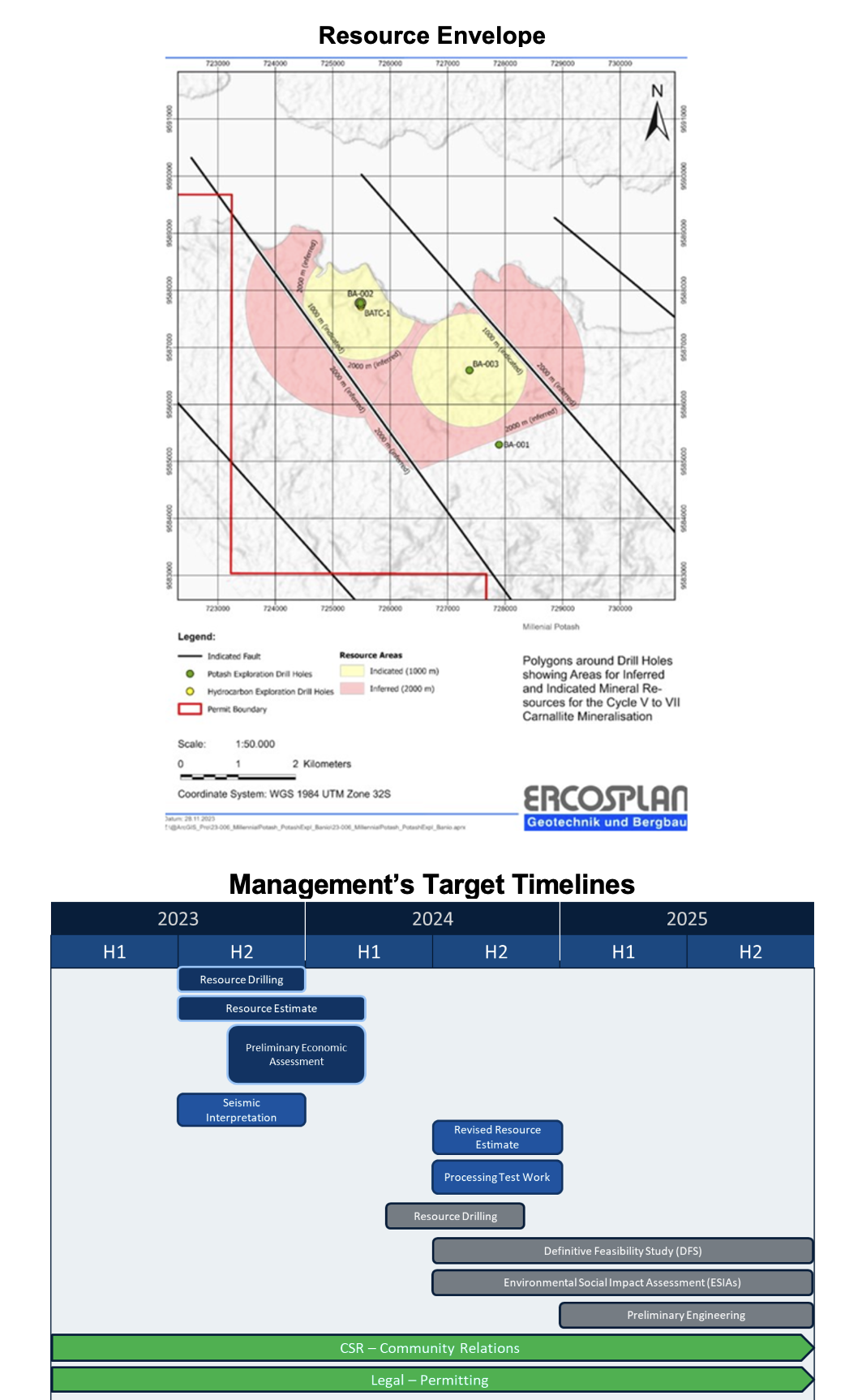

The resource envelope measures 5 km (length) x 3 km (width) x 0.2 km (thickness)

Mineralization has been identified at depths ranging between 230 m and 520 m below surface; we note that Banio’s potash beds are shallow compared to projects in Saskatechwan (800-1,500 m deep)

We believe there is potential for resource expansion, as the deposit remains open in multiple directions, and the current resource represents only 1.5% of the project area

Management aims to complete a resource update by Q1-2025, followed by engineering studies for a feasibility study

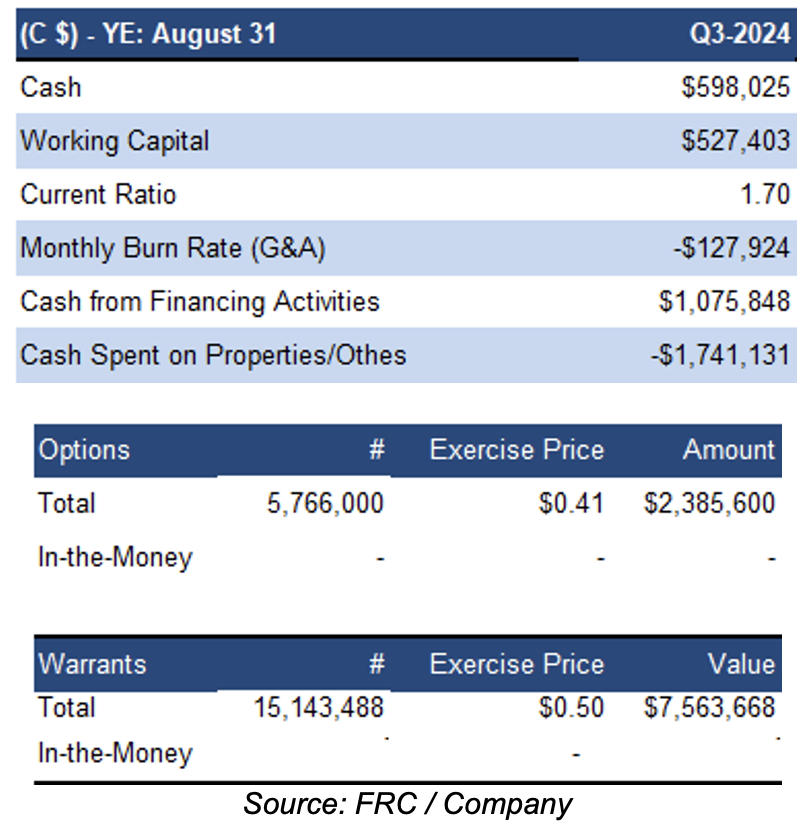

Financials

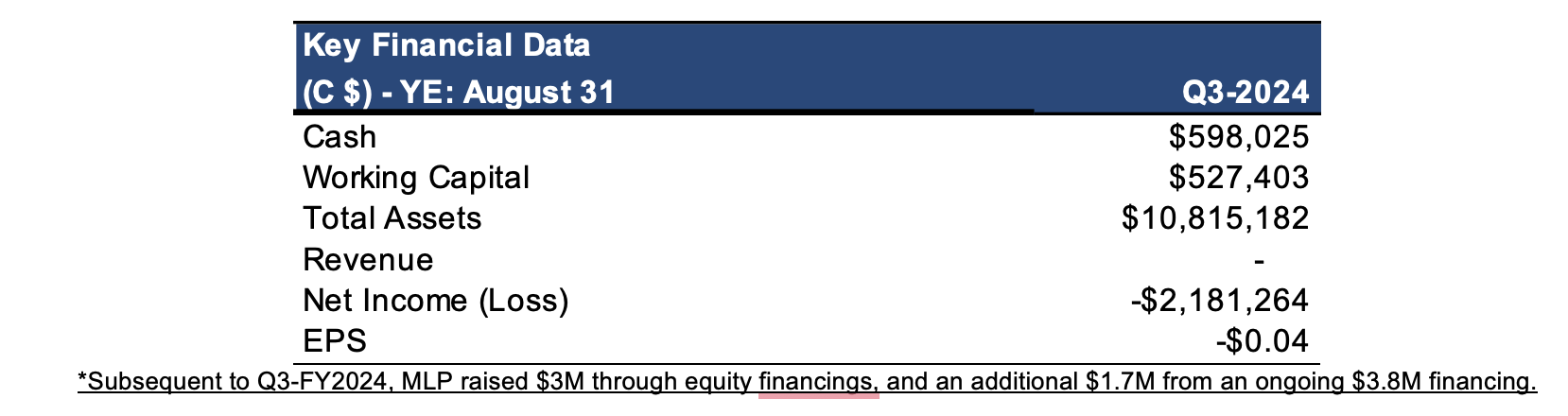

Subsequent to Q3-FY2024, MLP raised $3M through equity financings, and an additional $1.7M through an ongoing $3.8M financing

Upon completing the current financing, MLP will have $5M in the treasury

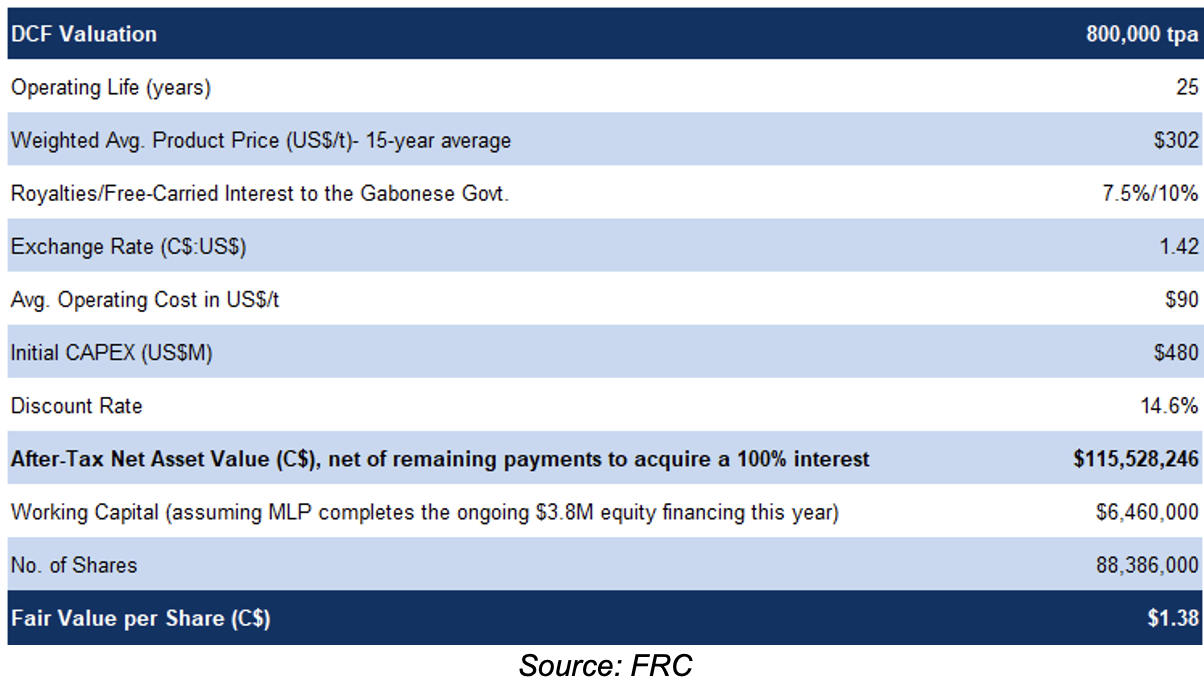

FRC Valuation

As a result of the recent equity financings, our DCF valuation dropped form $1.52 to $1.38/share

We are not making any other material changes to our models

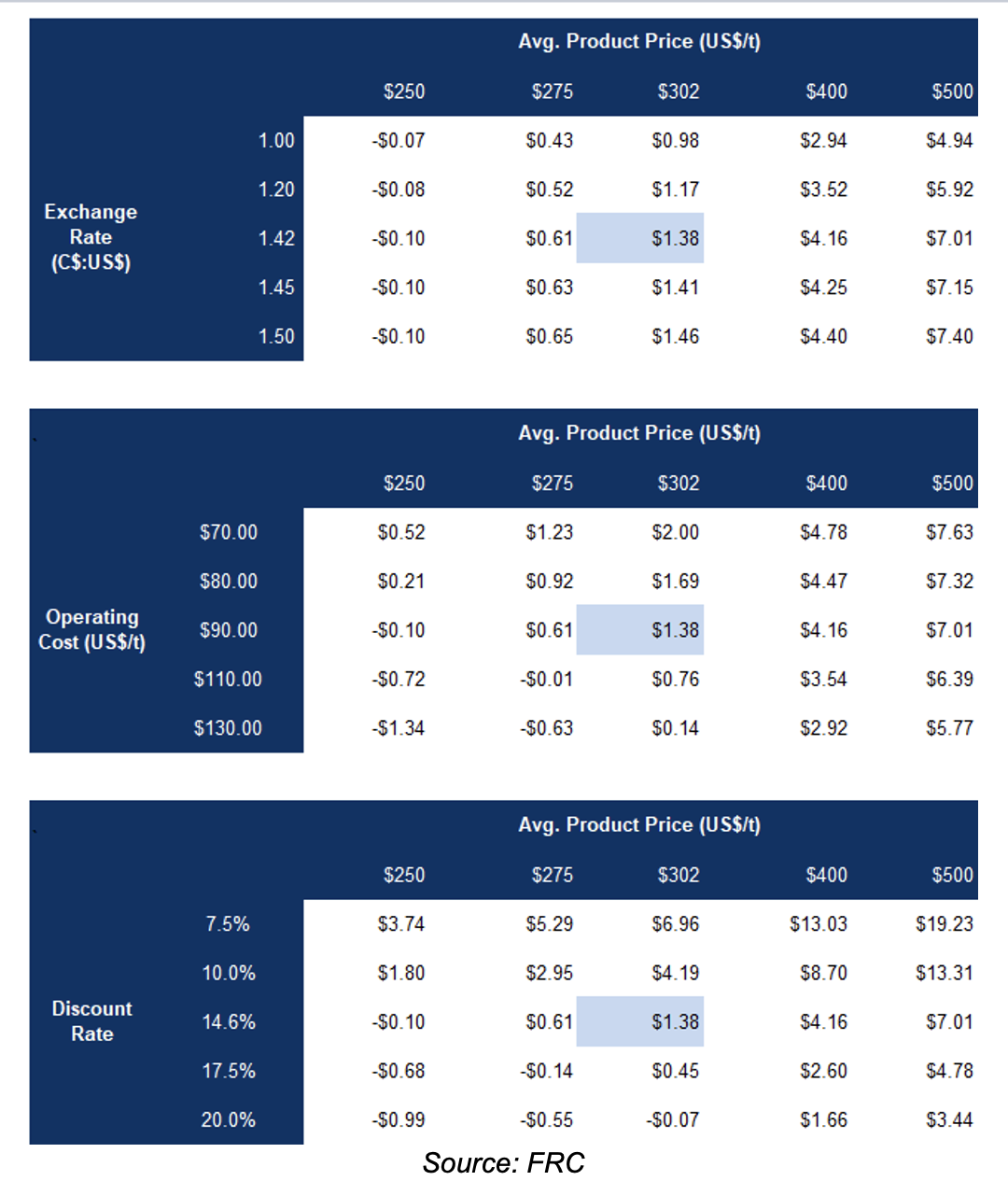

Our valuation is highly sensitive to key inputs

We are reiterating our BUY rating, and adjusting our fair value estimate from $1.52 to $1.38/share. The Banio project continues to advance, with significant infrastructure development underway. We believe the project's robust economics, low-cost production profile, and strategic location make it a compelling opportunity. While current potash prices are lower than historical averages, potential supply disruptions, and increasing global demand, could drive prices higher.

Risks

We believe the company is subject to the following key risks:

- The value of the company is dependent on potash prices

- Exploration and development

- FOREX and geopolitical

- Access to capital and potential for share dilution