Enertopia Corp.

Delineates an Attractive Lithium Resource Near Larger Players

Published: 12/15/2023

Author: Sid Rajeev, B.Tech, CFA, MBA

Sector: Basic Materials | Industry: Other Industrial Metals & Mining

| Metrics | Value |

|---|---|

| Current Price | US $0.02 |

| Fair Value | US $0.11 |

| Risk | 5 |

| 52 Week Range | US $0.01-0.06 |

| Shares O/S (M) | 155 |

| Market Cap. (M) | US $3 |

| Current Yield (%) | n/a |

| P/E (forward) | n/a |

| P/B | 2.1 |

Already a subscriber?

Want to know the fair value of the stock?

Subscribe for free to get exclusive insights and data.

Report Highlights

Highlights

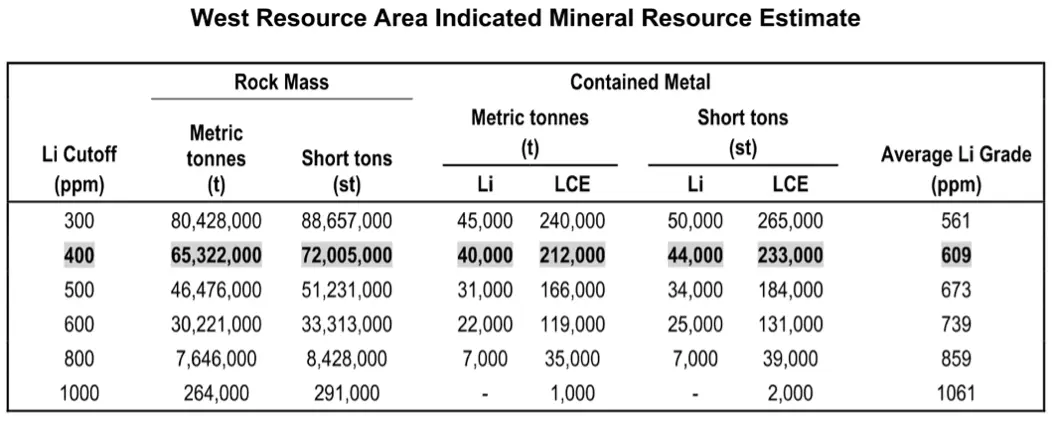

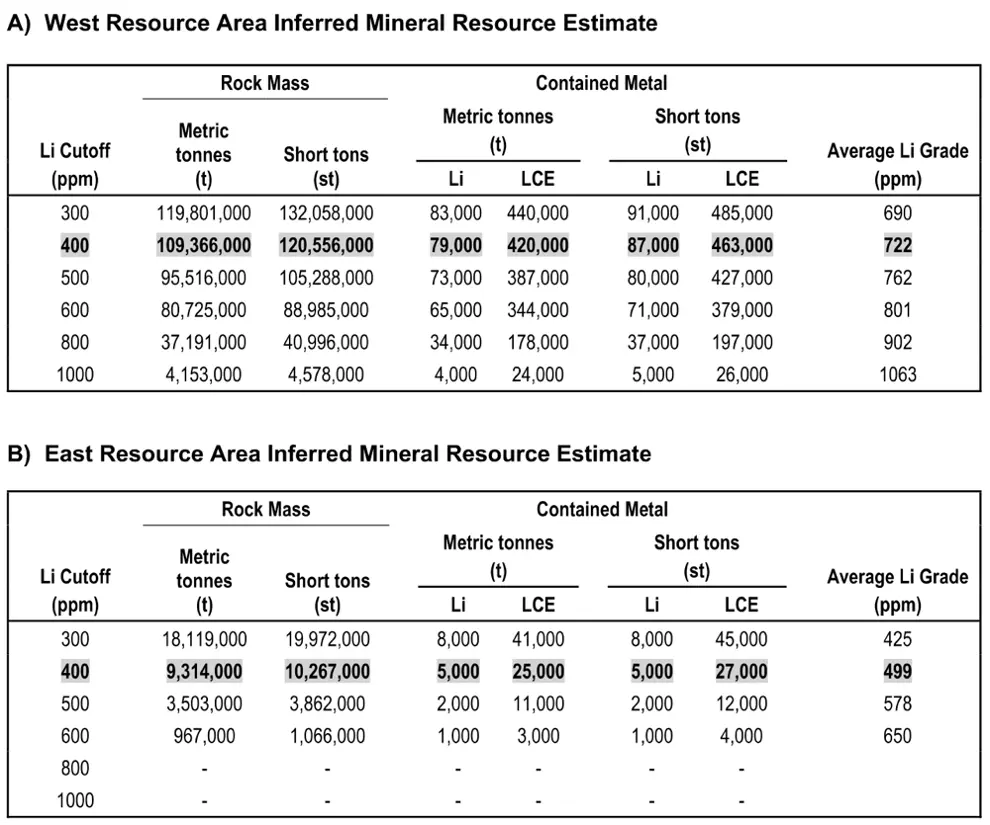

ENRT has completed a maiden resource estimate for its West Tonopah lithium project in Nevada, totaling 657 Kt LCE (lithium carbonate equivalent), averaging 674 Li. Relative to other lithium projects in the Americas, we believe this resource offers modest tonnage yet attractive grades.

West Tonopah is located next to American Battery Technology’s (NASDAQ: ABAT) Tonopah Flat project, which hosts resources totaling 16 Mt LCE (561 ppm Li), and is within a mile of American Lithium’s (TSXV: LI) TLC lithium project, hosting 10+ Mt LCE (792 ppm Li). ABAT was recently awarded a $57M grant from the U.S. Department of Energy. We see government support as an encouraging sign for lithium juniors in the region.

A major advantage of the West Tonopah project is its near surface mineralization, suggesting potential for relatively low OPEX/CAPEX. We believe the project has significant resource expansion potential along depth, given the average depth of drill holes is only 68 m. Projects in the area have been drilled up to depths of 100-200 m.

Lithium prices are down 81% YoY to US$14k/t vs the five-year average of US$21k/t. We believe lithium prices will remain under pressure, amid slower global GDP growth, and increasing supply. We believe the lithium market will move from a deficit to a surplus this year. That said, we maintain a positive outlook on EV-focused juniors, as battery/EV manufacturers, and miners, are actively seeking long-term stable sources of supply. The sector has witnessed several M&A deals this year. ENRT is trading at $6/t vs the sector average of $38/t, implying an 85% discount. Upcoming catalysts include metallurgical studies, follow-up drilling, and positive sentiment towards juniors exploring for EV metals.

Delineates a Maiden Resource for the West Tonopah Project

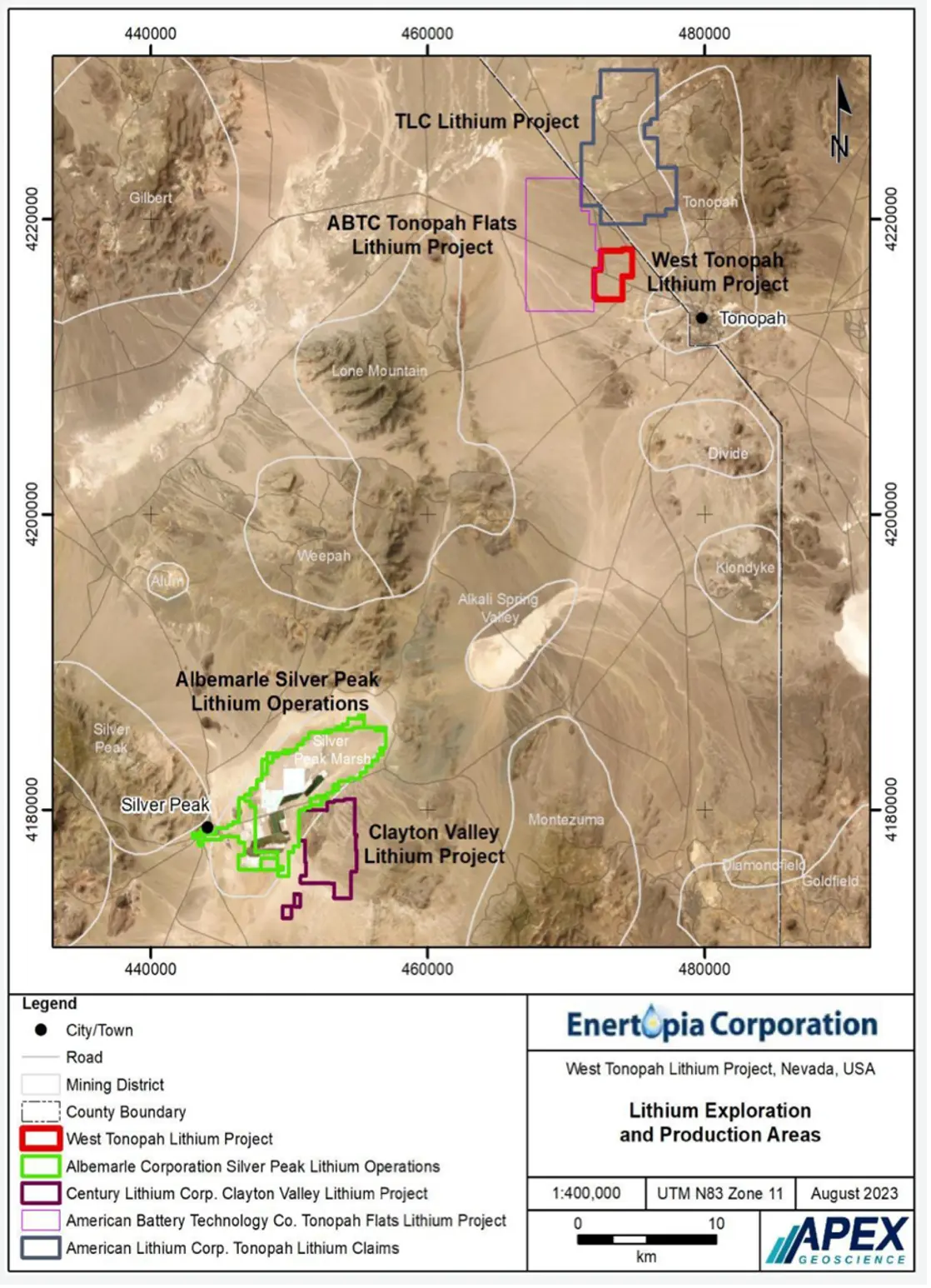

Project Location

Source: Company

100% owned by ENRT

Nevada is well-known for its lithium claystone deposits

Located next to American Battery Technology’s Tonopah Flat project (16 Mt LCE @ 561 ppm Li), and within a mile of American Lithium’s TLC lithium project (10+ Mt LCE @ 792 ppm Li)

ENRT has delineated a small-tonnage resource with attractive grades: 657 Kt LCE @ 674 ppm Li

The resource estimate was based on 22 holes, totaling 1,514 m

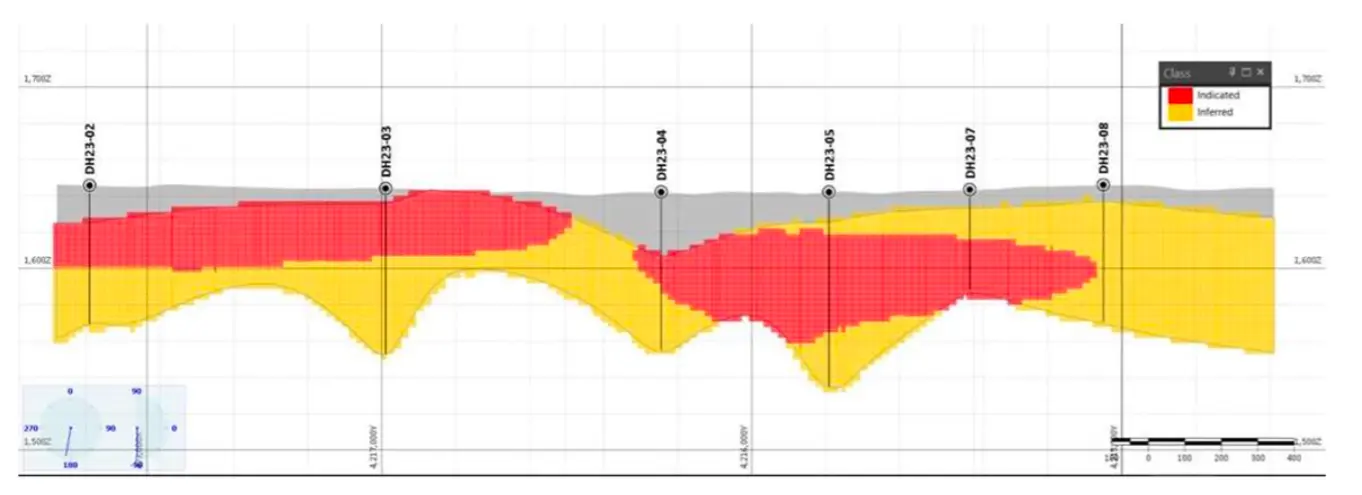

Mineralization begins at a depth of 7-15 m from the surface; we note that shallow deposits are low OPEX/CAPEX

We believe the project has resource expansion potential along depth, given that the average depth of drill holes is only 68 m

Deeper drill holes have intercepted higher grades

Resource Model Source: Company

Source: Company

In 2024, ENRT intends to conduct metallurgical tests, followed by a resource expansion drill program

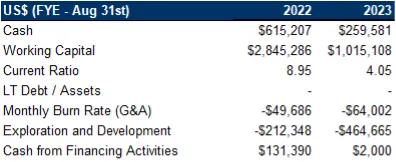

Financials

Source: FRC/Company

$1M in working capital at the end of FY2023

We believe ENRT will pursue an equity financing within the next six months

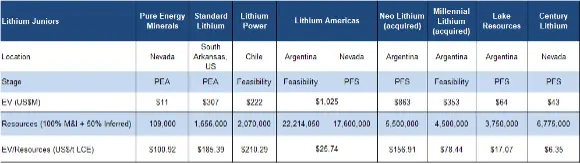

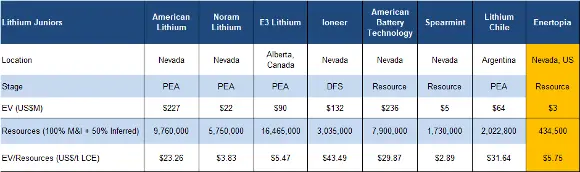

Valuation

Source: FRC / Various / S&P Capital IQ

Source: FRC / Various / S&P Capital IQ

Given the new resource estimate, we are valuing ENRT based on the average EV/Resource of comparables instead of EV/hectare

ENRT is trading at $6/t vs the sector average of $38/t, implying an 85% discount

By applying $38/t to ENRT’s resources, we arrived at a comparables valuation of $0.11/share (previously $0.13/share)

We are reiterating our BUY rating, and adjusting our fair value estimate from $0.13 to $0.11/share. Upcoming catalysts include metallurgical tests, resource expansion drilling, and positive sentiment towards juniors focused on EV metals.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

1. The value of the company is dependent on lithium prices

2. No economic studies

3. Exploration and development

4. Access to capital and share dilution