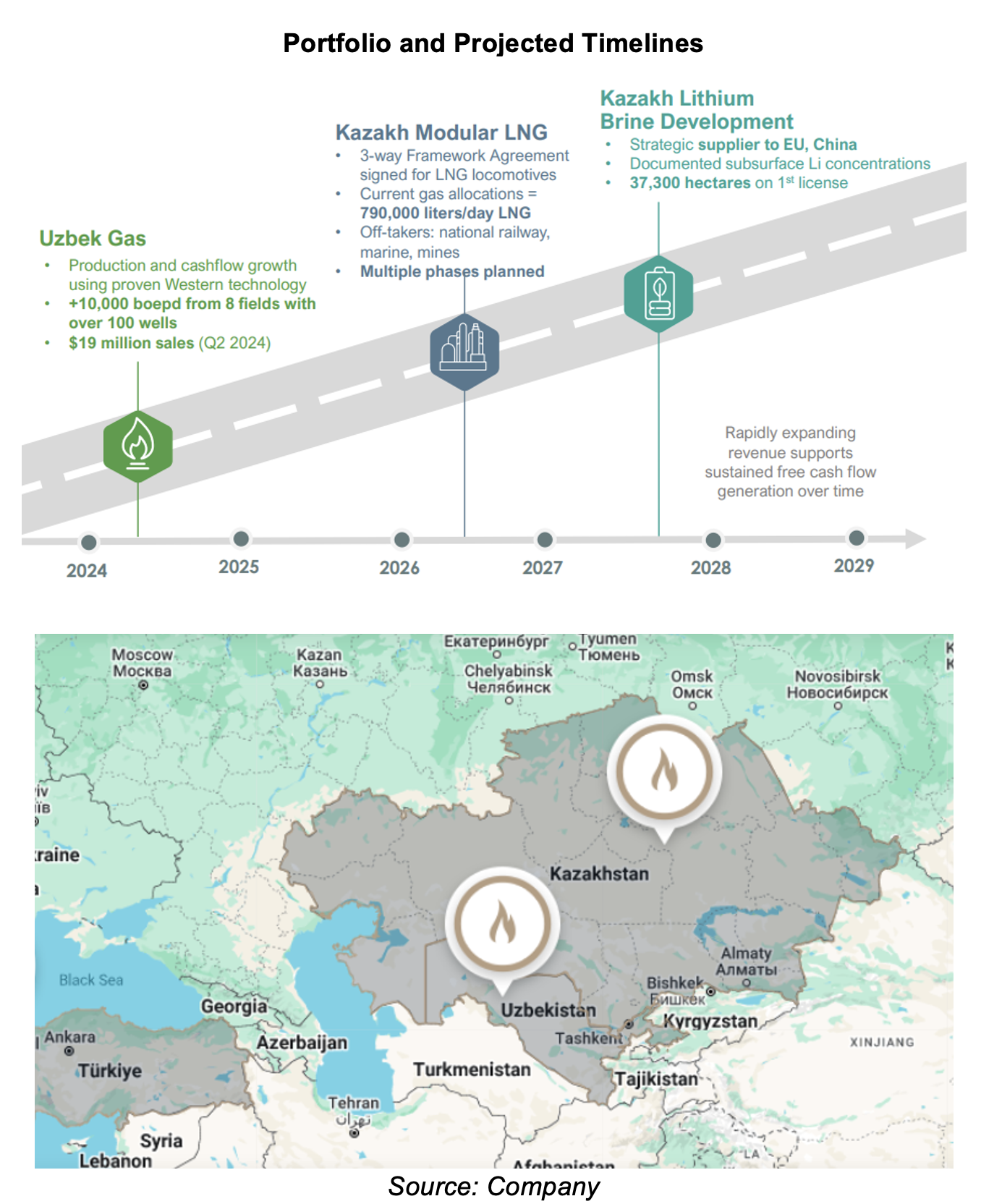

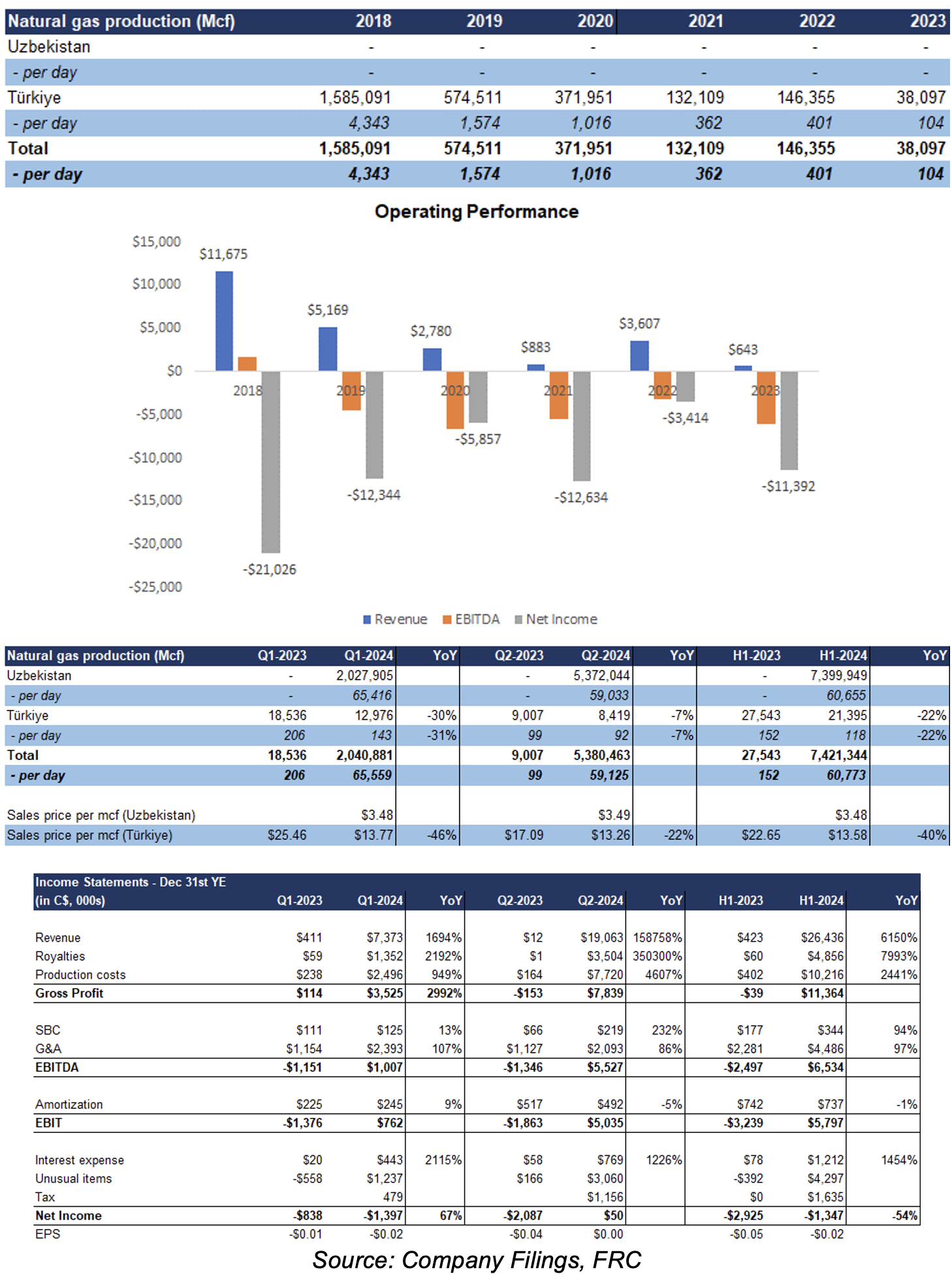

- CDR has a 20-year contract from the Government of Uzbekistan to operate eight gas fields, and enhance production using Western technologies. This is part of Uzbekistan’s efforts to revitalize domestic gas production, and reduce import dependence. As a result of this contract, CDR's Q2-2024 revenue surged to $19M (up from just $12k in Q2-2023), with EBITDA and EPS turning positive. The company plans to increase production to over 100,000 mcf/day across 120 wells through workovers, optimization programs, and new wells. Our After-Tax Net Asset Value estimate of this project is $1.20 /share.

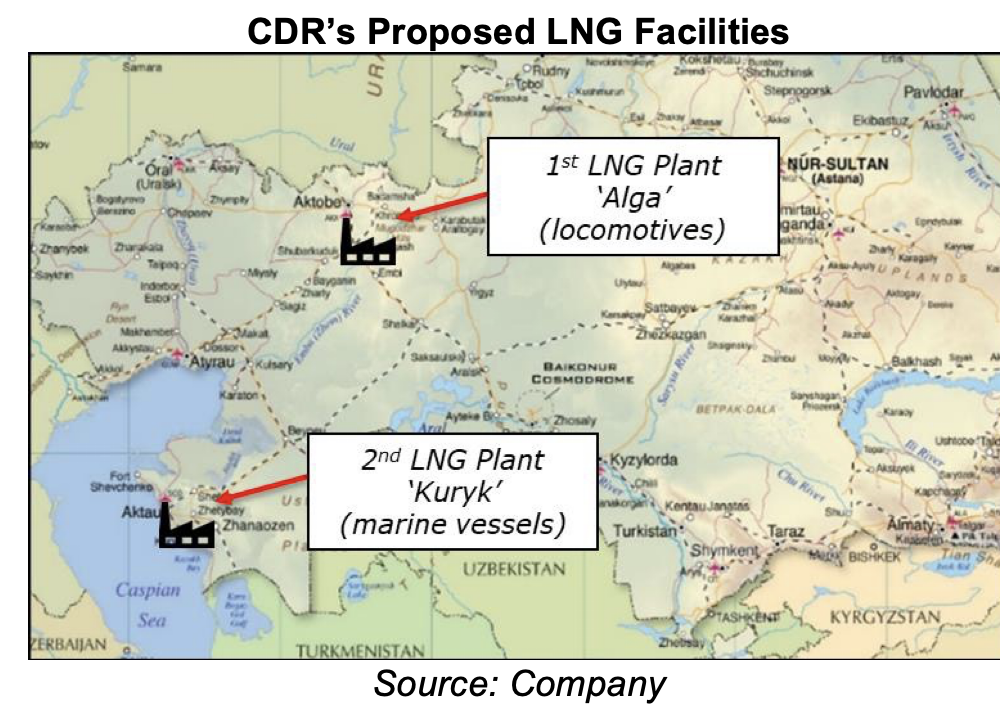

- In Kazakhstan, Condor is developing the country’s first LNG facilities to potentially replace diesel used for industrial transportation. The company has secured contracts with state-owned entities, including one for natural gas supply to produce LNG, and another for supplying LNG to Kazakhstan’s rail locomotives. While large-scale LNG facilities can cost billions of US$, Condor plans to build smaller, modular LNG facilities that are quicker and cheaper to construct. The first facility is set to start operations in 2026, while the company is exploring funding options. Our After-Tax Net Asset Value estimate of this project is $2.25/share.

- We anticipate record revenue and EPS in 2024 and 2025. Key upcoming catalysts include progress updates on the LNG project in Kazakhstan, and initiatives to boost gas production in Uzbekistan.

Price Performance (1-year)

Company Overview

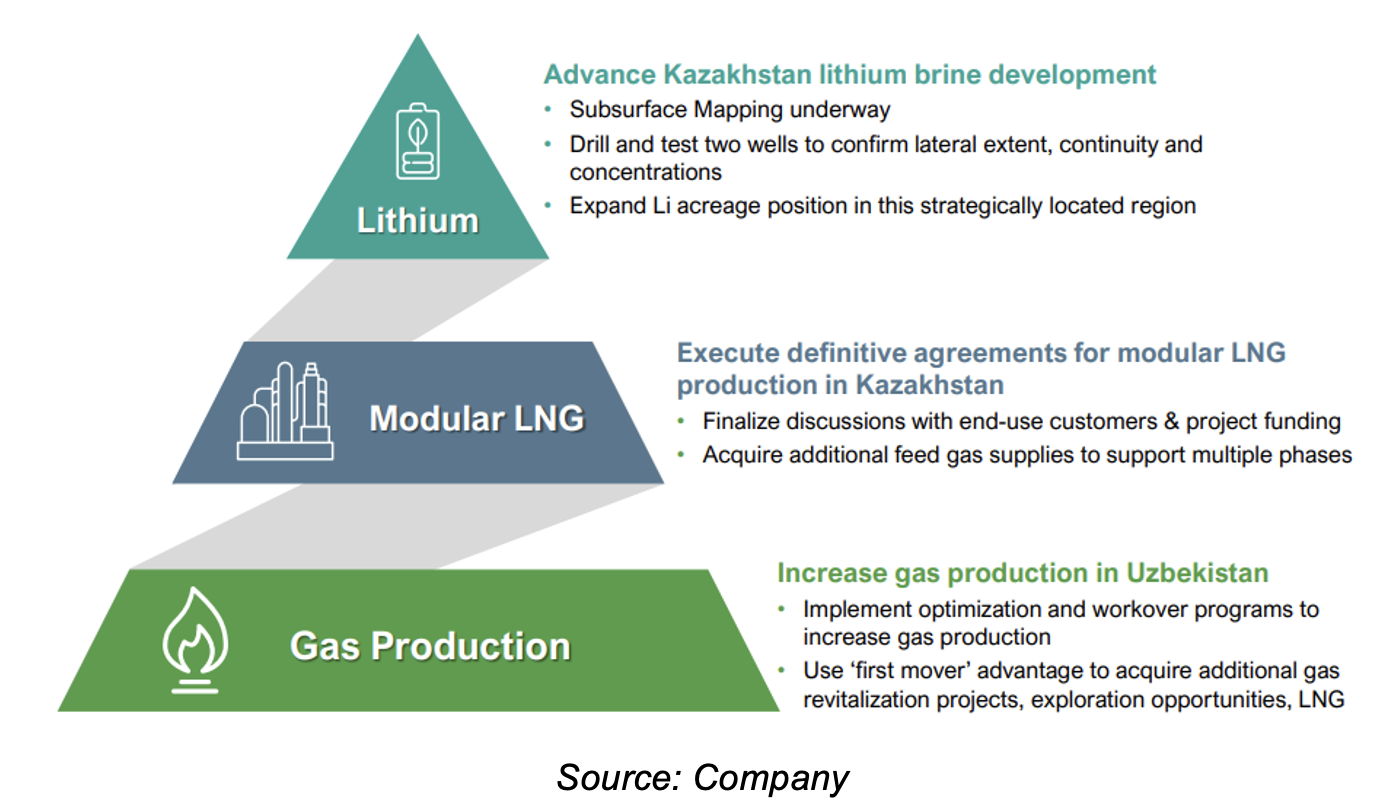

The company is focused on three main initiatives:

- Uzbek Gas: Redeveloping natural gas projects in Uzbekistan

- Modular LNG: Developing Central Asia’s first LNG facility in Kazakhstan

- Lithium Brine Exploration: Investigating lithium brine resources in Kazakhstan

Founded in 2006 by the founders of the Osisko Group of mining companies. Headquartered in Calgary with 160 full-time employees across Canada and Central Asia

The following sections summarize each of the company’s business lines/initiatives.

Until 2023, the company primarily generated revenue from gas production in Turkey. However, after depleting its reserves, CDR wrote off these assets, and is currently winding down its operations in the country

In early 2024, CDR obtained rights to gas fields in Uzbekistan, and transformed into a significant gas producer. The company is also actively developing an LNG project, and conducting lithium exploration in Kazakhstan

Natural Gas, Uzbekistan

Uzbekistan – Highlights

- GDP: US$115B; Population: 37M

- Natural Gas Reserves: Uzbekistan has significant natural gas resources, and is a major producer within Central Asia.

- Energy Supply: Natural gas dominates Uzbekistan's energy supply, accounting for approximately 85% of its total energy mix.

- Economic Importance: The oil and gas industry is about 16% of Uzbekistan's national GDP, primarily driven by natural gas production.

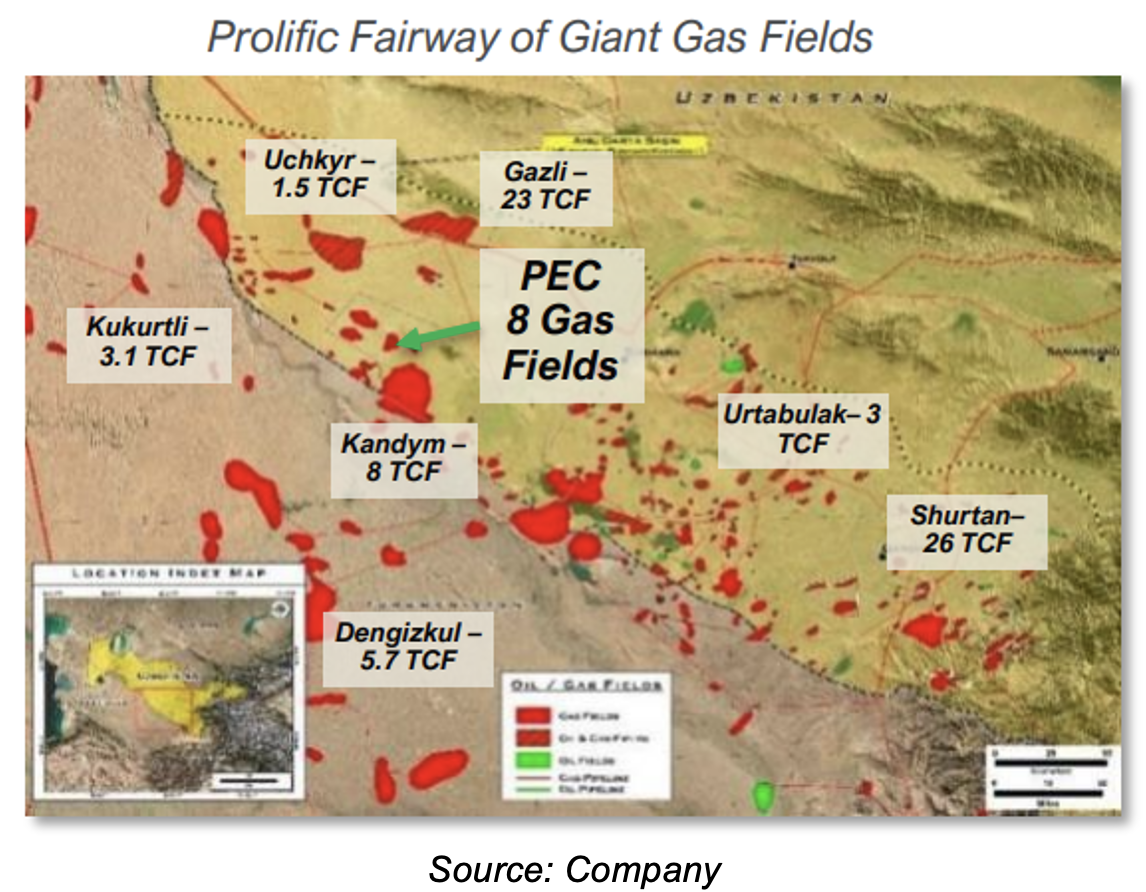

- Gas Fields: The country has over 200 gas and oil fields. Approximately 40% of these fields are owned by a state-owned gas producer; the remaining are controlled by major foreign companies like Lukoil (MCX: LKOH), Gazprom (MCX: GAZP), CNPC, Shell (LSE: SHEL), and TotalEnergies (NYSE: TTE).

- Production Challenges: The country's natural gas production dropped 23% between 2019 and 2023, while consumption rose 4% (Source: CEIC), leading to higher imports from Turkmenistan and Russia.

- Outlook: According to GlobalData, gas production is projected to decrease 4% CAGR from 2024 to 2028.

The country has an urgent need for revitalizing domestic gas production to reduce import dependence, given the country’s high reliance on natural gas for energy consumption

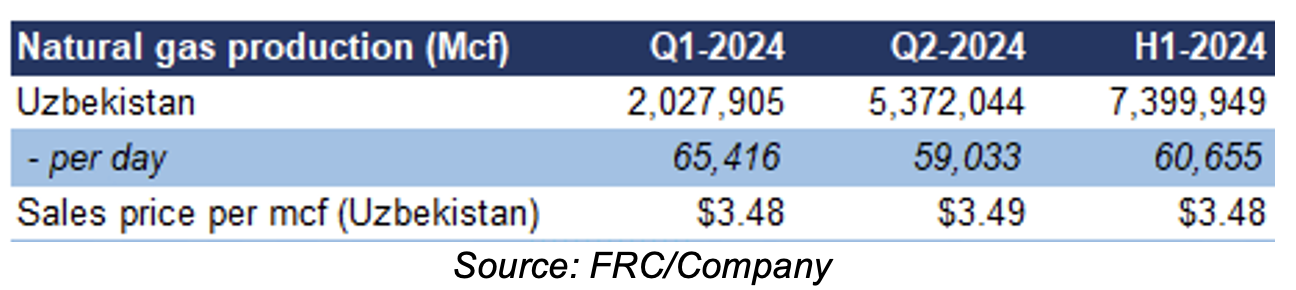

In January 2024, CDR entered into a 20-year Production Enhancement Contract (PEC) with the Government of Uzbekistan. Under this agreement, CDR will act as the operator, utilizing proven Western technologies to increase production and recovery rates from eight natural gas fields. These fields cover 279 km² (69,000 acres), and include 77 active wells and 39 shut-in wells, producing 60,000 mcf/d. Condor will sell the produced gas back to the Government, which will receive a 20% royalty on revenue, and benefit from higher tax revenue, and increased gas volumes available for domestic distribution.

CDR owns a 51% interest, while the remaining 49% is owned by their partner, a gas distributor and marketer in Kazakhstan. CDR's fields are in the Bukhara province, one of the most active natural gas producing regions in the country

Uz reservoirs are geologically similar to those in Western Canada, making them ideal for Western technology

The active wells in CDR’s fields were brought into production in the past three to 10 years. These wells have an average annual decline rate of over 20%, well above the industry norm of 5%-10%, and relatively low recovery rates. Condor intends to use the following strategies to improve recovery and production, reduce decline rates, and lower carbon emissions.

Proven Strategies/Processes

Enhanced Well Performance:

- Artificial Lift: Installing pumps to boost oil production

- Stimulation: Injecting fluids to increase reservoir productivity

- Wellbore Optimization: Replacing corroded pipes and isolating water zones

Reservoir Exploration and Development:

- Infill Drilling: Drilling new wells between existing ones to increase production

- Horizon Exploration: Investigating deeper layers for potential oil reserves

- Seismic Analysis: Using sound waves to identify new oil-bearing areas

Water Management and Efficiency:

- Water Handling: Separating water from gas at the field level to reduce pipeline pressure

- Surfactants: Using chemicals to transform water into foam for easier removal

- Infrastructure Optimization: Evaluating and improving pipelines and facilities for better water handling

Innovative Techniques:

- Plunger Lifts: Using mechanical devices to remove wellbore fluids more efficiently

- Multi-lateral Wells: Drilling wells with multiple branches to increase production

The fields feature stacked carbonate and clastic reservoirs akin to the Western Canadian Sedimentary Basin

CDR’s goal is to increase production by over 50%, reduce decline rates, and lower carbon emissions by improving well performance, exploring new reservoirs, deploying proven modern technologies, and optimizing water management

A stable price environment. In H1-2024, CDR received US$2.6/mcf, in line with U.S. prices (US$2.4/mcf), higher than Canada (US$0.8/mcf), but far below Europe’s US$11/mcf

CDR’s Development Plans: Since assuming operations in March 2024, the company has successfully flattened decline rates by implementing some of the aforementioned techniques.

Producing 60,000 mcf/d.

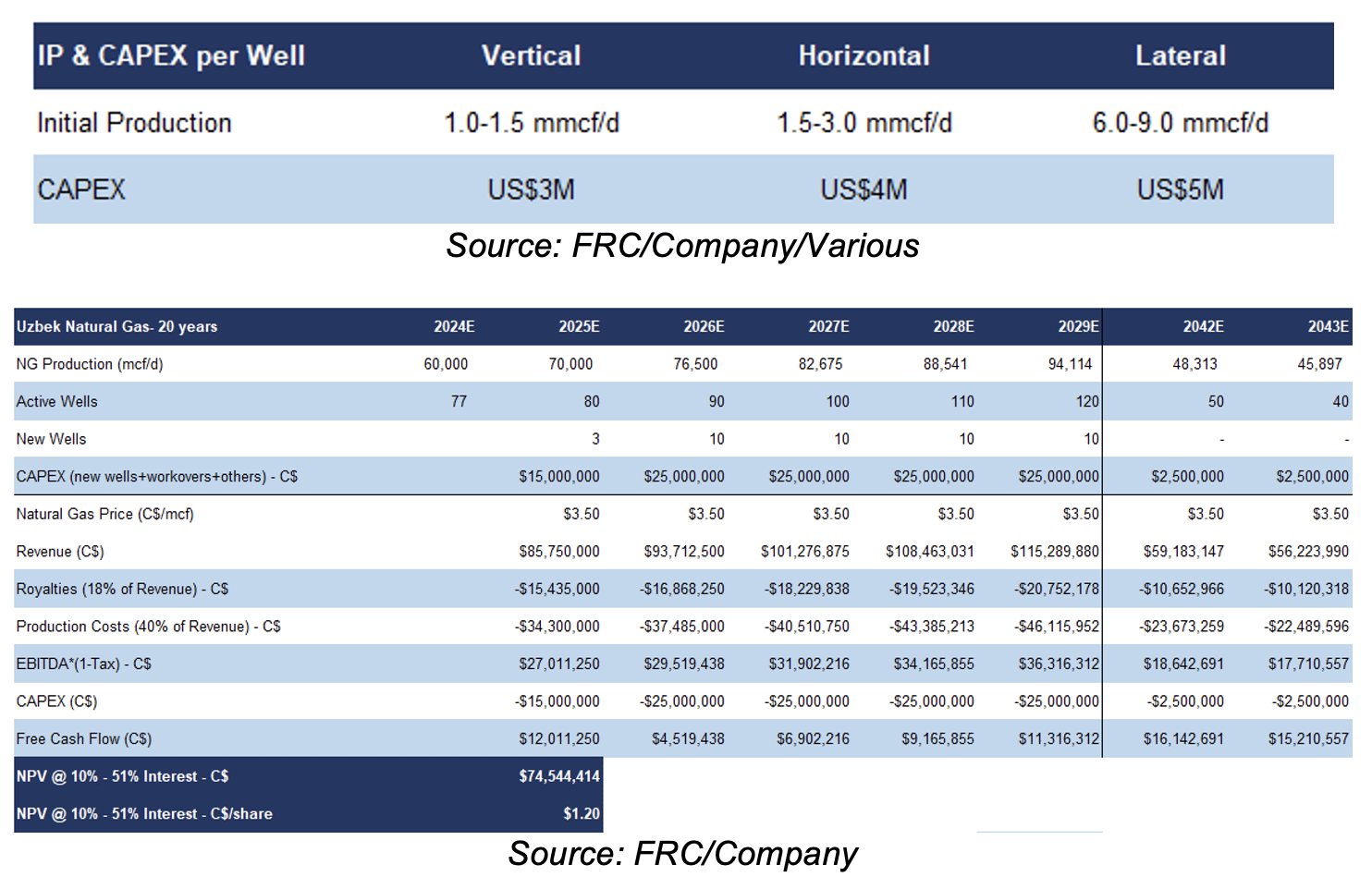

Vertical wells typically have lower initial production rates, and lower CAPEX, compared to horizontal and lateral wells. A typical well can produce for 15-20 years, with an IP of 1.0-2.0 mmcf/d, and an average annual decline rate of 5-7%

Through a combination of workovers, the strategies mentioned above, and new wells, the company aims to boost production to over 100,000 mcf/day across 120 wells (total CAPEX - $80M+). In 2025, the company plans to drill a vertical, horizontal, and a multi-lateral well. If successful, this could yield 8+ mmcf/d of new production.

Wells are 2,000-2,500 m deep. Anticipating a reserve report in early 2025. Our AT-NAV10% estimate for the 20-year PEC is $1.20/share

CDR’s long-term objective is to establish similar agreements with the government for additional fields across the country. Our valuation of the project is based solely on the production potential from the current agreement. While the project lacks an NI 51-101 compliant reserve report at this stage, management intends to have one completed by early 2025.

Modular LNG, Kazakhstan

Kazakhstan is the world’s largest uranium producer. Hosts several energy and mining majors

Kazakhstan – Highlights

- GDP: US$297B; Population: 20M

- Kazakhstan, the largest economy in Central Asia, is renowned for its abundant natural resources.

- A leading global producer of uranium, the county also hosts significant reserves of oil, gas, copper, aluminum, and zinc.

- No lithium or LNG production

- Hosts several energy and mining majors such as Chevron (NYSE: CVX), Shell (LSE: HEL), Exxon Mobil (NYSE: XOM), Rio Tinto (ASX: RIO), Cameco (NYSE: CCJ) and Glencore (LSE: GLEN)

- Country Risks: Regulatory and political instability, bureaucracy, close ties with Russia, corruption, and currency volatility.

LNG (Liquefied Natural Gas) offers a strong alternative to traditional fuels like diesel, particularly in sectors such as mining, railroads, and long-haul transportation

Unlike natural gas, LNG is easy and safe to transport and store. It can be delivered by truck or rail to regions lacking natural gas pipelines, increasing energy accessibility. Additionally, LNG burns cleaner than coal and oil, resulting in significantly lower greenhouse gas emissions.

CDR owns a 90% interest in this initiative, with the remaining 10% owned by local partners engaged in construction and marketing activities.Vital agreements in place with state-owned entities

The CAPEX for a large-scale LNG facility can range from several billions to tens of billions of US$. Condor plans to build smaller, modular LNG facilities that can be constructed much faster and cheaper than traditional facilities (12-18 months vs three-five years). More importantly, modular LNG facilities are well-suited for regions like Kazakhstan, with limited pipeline networks, and relatively low gas prices.

Condor is establishing Kazakhstan’s first LNG facilities, aiming to partially replace diesel for rail and mining haul truck transportation. This initiative is primarily driven by two key agreements:

- Condor has entered into natural gas supply agreements with the Government of Kazakhstan, with prices pre-determined and reviewed annually. Similar to Uzbekistan, natural gas prices are regulated in Kazakhstan. Gas will be liquefied at CDR’s Alga and Kuryk LNG facilities to produce up to 240k tonnes per year (1.5M liters per day) of LNG, displacing 1M liters of diesel fuel per day, which can potentially fuel over 250 rail locomotives or over 360 large mine haul trucks.

Each tonne of LNG can displace up to 1.13 tonnes of diesel.

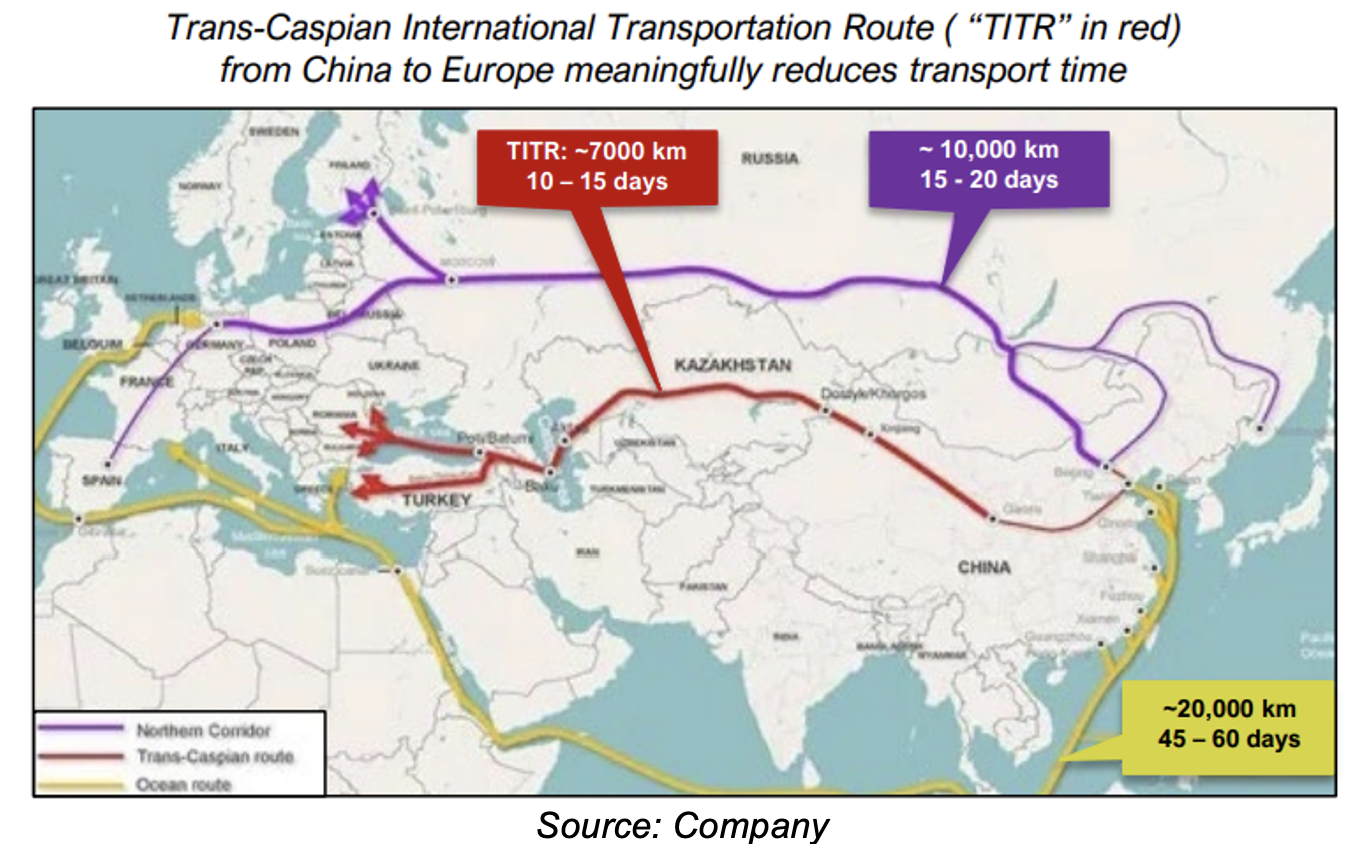

- CDR has signed a Framework Agreement to supply LNG for fueling Kazakhstan’s rail locomotives. This agreement, also signed by Kazakhstan Temir Zholy National Company JSC (KTZ), the national railway operator, and Wabtec Corporation (NYSE: WAB/MCAP: $32B), a U.S.-based locomotive manufacturer with facilities in Kazakhstan, focuses on expanding the Transcaspian International Transport Route (TITR).

The TITR is the shortest, fastest, and a geopolitically secure transit corridor for freight between Asia and Europe, bypassing Russia and the Middle East

Kazakhstan is also expanding its rail network and constructing a new dry port at the Kazakhstan–China border

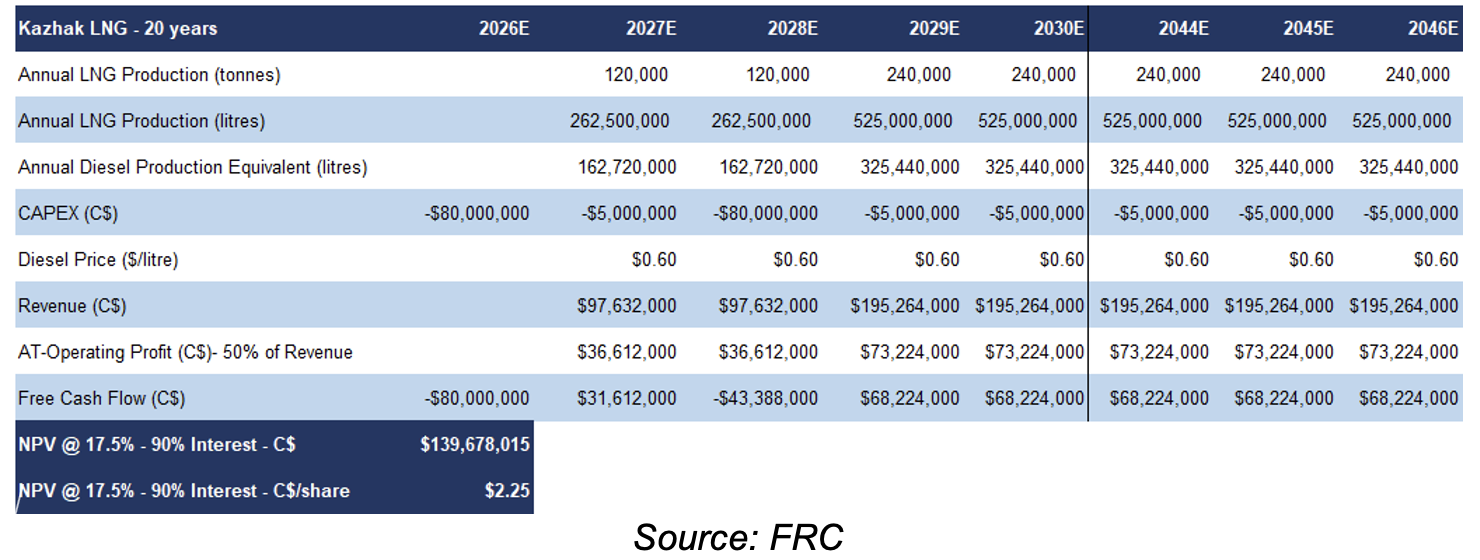

Development Plans: The company is planning to develop a series of modular LNG facility in four phases. When fully operational, these facilities will produce up to 600k tonnes of LNG annually, displacing 680k tonnes of diesel fuel. The first phase of the project is expected to produce 120k tonnes per year (CAPEX: US$80M), which is the energy equivalent volume of 440k litres of diesel per day (161M litres per year). This facility is scheduled to start operations in 2026.

Our AT-NAV17.5% estimate for the first two plants is $2.25/share. As the project is in early stages, we are using a relatively high discount rate of 17.5%

Key milestones:

- Secured feed gas supply for the first two LNG facilities, with ongoing discussions to secure additional supply

- Front-end engineering and design completed

- Detailed engineering is underway

- The company is exploring project funding alternatives

Project Economics:

Lithium Brine Exploration, Kazakhstan

Earlier this year, Rio Tinto (LSE: RIO) commenced a lithium exploration program in the country

While Kazakhstan has yet to demonstrate commercial lithium production, we believe its geological landscape holds promise. China, Germany, and South Korea have initiated lithium exploration efforts in the country. In 2023, South Korea's Korea Institute of Geoscience and Mineral Resources (KIGAM) made a significant hard rock lithium discovery in eastern Kazakhstan, with impressive lithium grades of 5.3%.

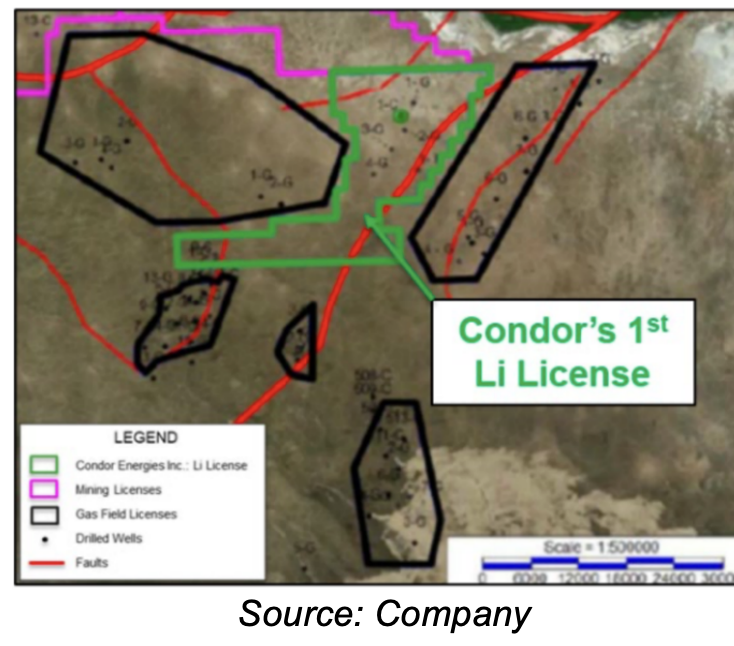

In August 2023, CDR secured a 100% interest in the 37,300-hectare Kazakh lithium project, with a six-year license term. The project’s prime location between Europe and China offers a direct route to major lithium markets.

Location Map

Prospective for lithium brine deposits

Lithium primarily occurs in three types of deposits: pegmatites (hard rock), brines, and clays. Pegmatites and brines account for most of the global resource-base. Lithium brines are typically formed in desert climates where there is a slow inflow of lithium and other metals and salts, but no outflow. Gradual evaporation over thousands of years slowly increases lithium grades to an economic level.

Around 60% of globally mined lithium currently comes from hard rock resources, with the remaining 40% sourced from brine deposits.

Determining the more economically attractive deposit type is challenging; while pegmatite deposits typically offer higher-grade lithium with lower CAPEX, they often yield lower operating margins. Subsurface mapping underway

This pre-resource stage project has undergone geophysical surveys and drilling. A historic well targeting hydrocarbons encountered lithium concentrations of up to 67 mg/L. While this grade is lower than typical lithium brine deposits, historical data shows a substantial 670 m column of mineral-rich brine reservoirs. We believe the property's large area and its location in a geothermally active, faulted region, suggests significant lithium potential due to the migration of mineralized brines.

CDR is planning to drill two exploratory wells. We note that delineating a lithium resource is a faster and cheaper process vs mainstream metals such as gold and copper.

Management is also working to secure a second lithium brine license for 6,800 hectares in a region where a historic well revealed mineralization of up to 130 mg/L Li, and identified over 1 km of lithium brine sands.

Multiple Soviet-era wells drilled in the project area that can be utilized for regional geological exploration

Upcoming Catalysts

Multiple near-term catalysts

Management and Directors

Management and board own 6.4%. Management has a successful track record in the oil and gas industry in Central Asia. Three out of four directors are independent

Brief biographies of the management team and board members, as provided by the company, follow:

Don Streu – President, Chief Executive Officer & Director

37 years of experience in the oil and gas industry including 22 years with Chevron working in Angola, Indonesia, Canada and the United States, including deepwater operations, and various operations producing 100,000-350,000 bopd. He is currently the Honorary Consul of the Republic of Kazakhstan for Alberta and a national Board Director for the Canada Eurasia Chamber of Commerce (CECC). Mr. Streu has a BSc in Mining Engineering from the University of Alberta with post graduate studies in Petroleum Engineering.

Sandy Quilty – CFO

A Chartered Accountant with over 30 years of experience working for E&P companies in Canada, Netherlands, China, Kazakhstan and other CIS countries. He was previously VP of Finance at Arawak Energy Corporation, CFO at Altius Energy Corporation and accounting manager at Fracmaster/BJ Services.

Jon Erickson – Senior VP Operations

35 years of experience with international E&P companies including Oxy, Texaco, Chevron, Tullow Oil and Burren Energy. He has been involved in onshore and offshore asset management operations in the Middle East, Russia, Kazakhstan, Turkmenistan, Africa, and South America. Mr. Erickson has managed LNG projects in several countries including Mozambique, Chad, and Gabon, for gas to power and for diesel displacement. Mr. Erickson holds a degree in Petroleum Engineering and an MBA from Eli Broad Business School.

John Baillie – Senior VP Asset Development

40 years of experience in the international upstream energy industry, 25 years of which in various Chevron companies in North America and Africa, and as Executive with Sinopec-Addax Petroleum in Switzerland. He has extensive experience leading teams on major energy operations and developments in Angola, Congo, Gabon, Cameron, Nigeria, and the UK North Sea.

Trent Mercier – VP and General Counsel

Specializes in international resource project transactions and public-private investment, and has advised E&P companies, financial institutions and governments on projects in over 25 countries. He was a Partner and global co-chair of the oilfield services group of Norton Rose Fulbright (global law firm) and most recently a Partner at Stikeman Elliot (M&A and energy law firm in Canada).

Norman Storm – Managing Director

28 years of experience in Kazakhstan across a wide array of business activities, including oil and gas exploration and production, mining, oil field services, domestic and international transportation services, and manufacturing. He is the Managing Director of Eurasia Resource Value SE, a European-based private investment fund that is the founder of Condor Energies, as well as Osisko Mining, the developer of Canadian Malartic, Canada’s largest gold mine, near Val d’Or in Quebec.

Torsten Kritzler – VP Well Services

A drilling and completion professional with over 25 years in the international oil and gas industry. His expertise encompasses diverse environments, including Saudi Arabia, Indonesia, Angola, Nigeria, Canada, and the United States. Notably, his 15-year tenure at Chevron was marked by a focus on integrating new technologies to enhance asset recovery across different operational contexts.

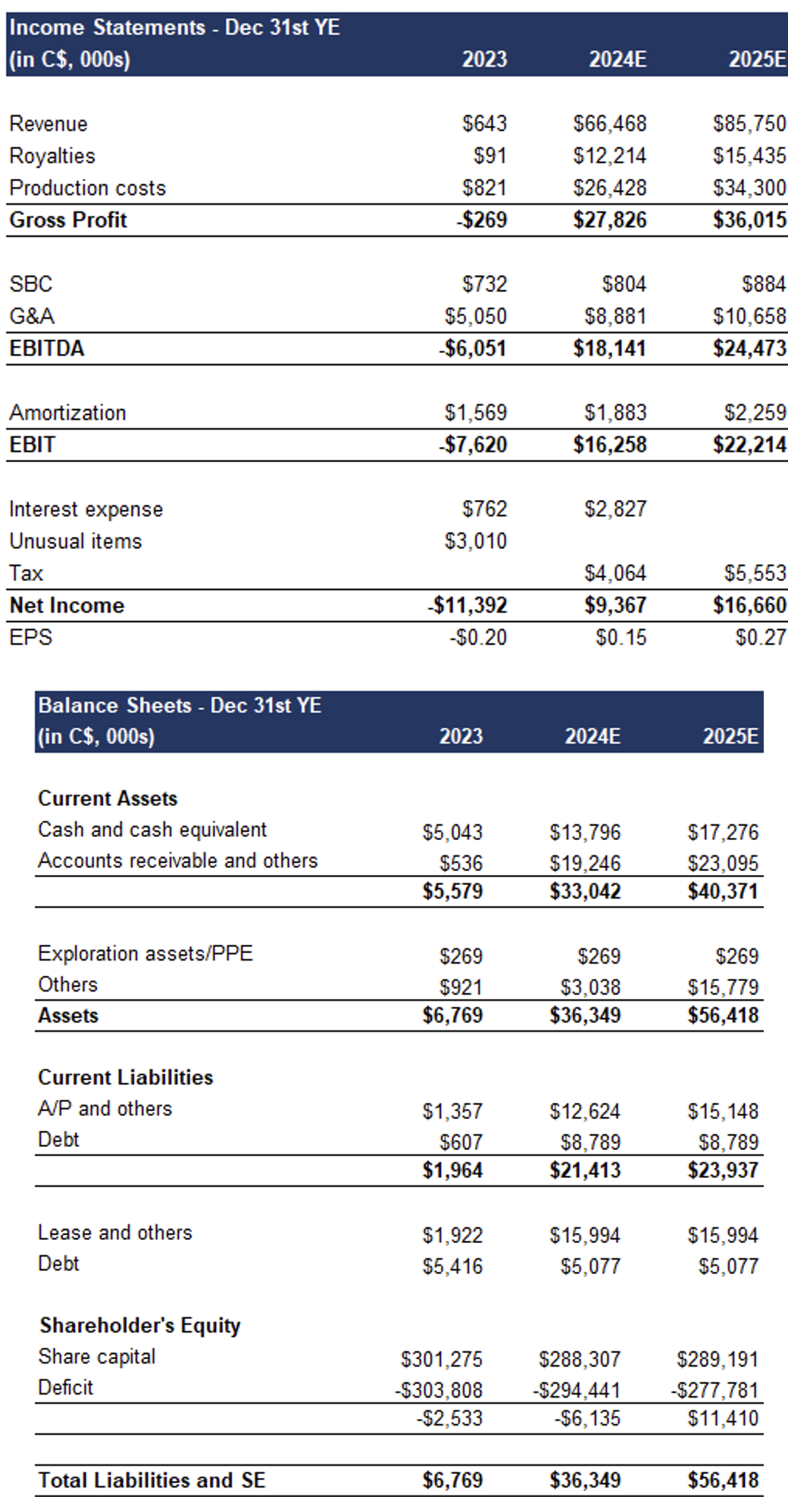

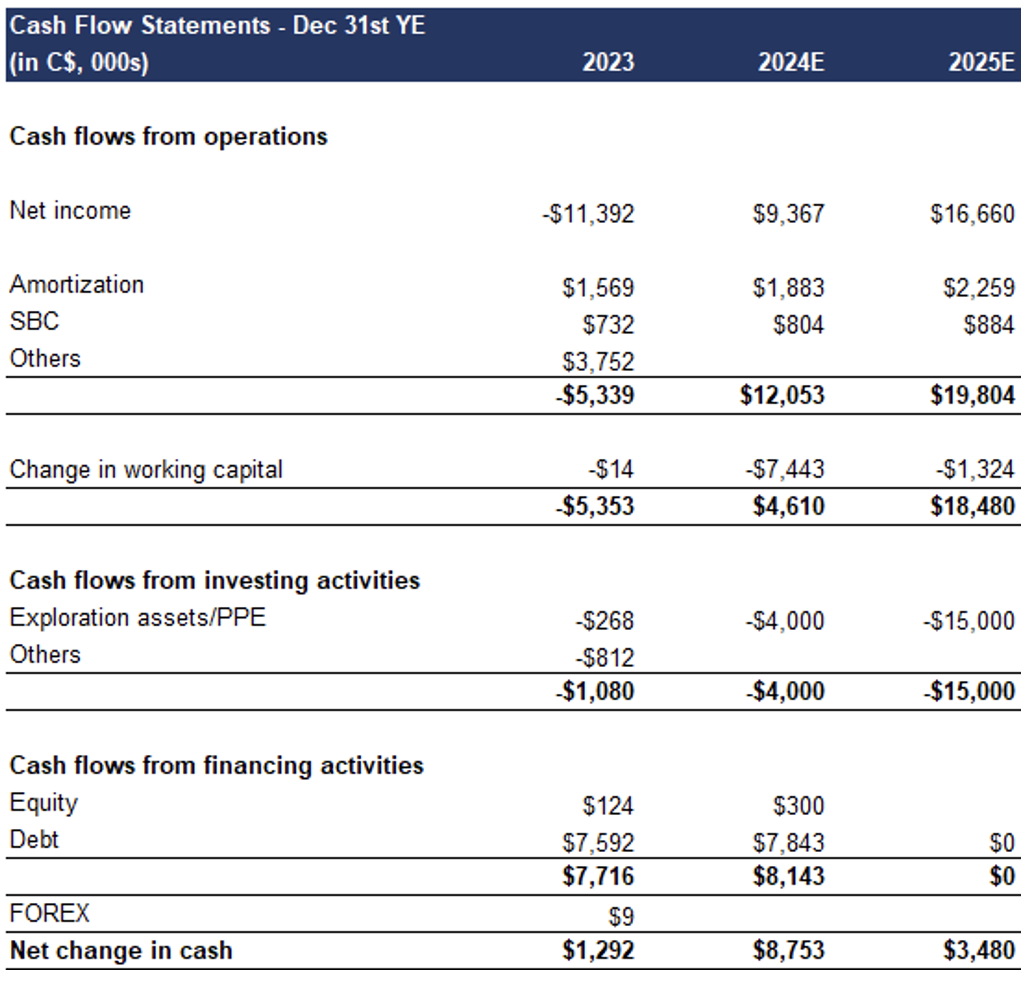

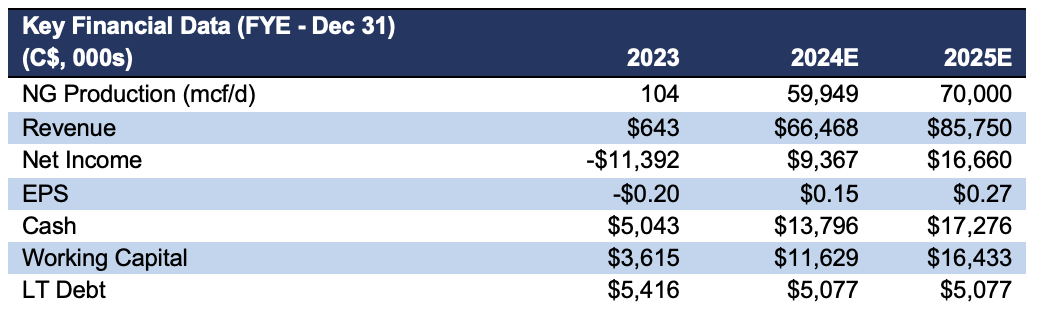

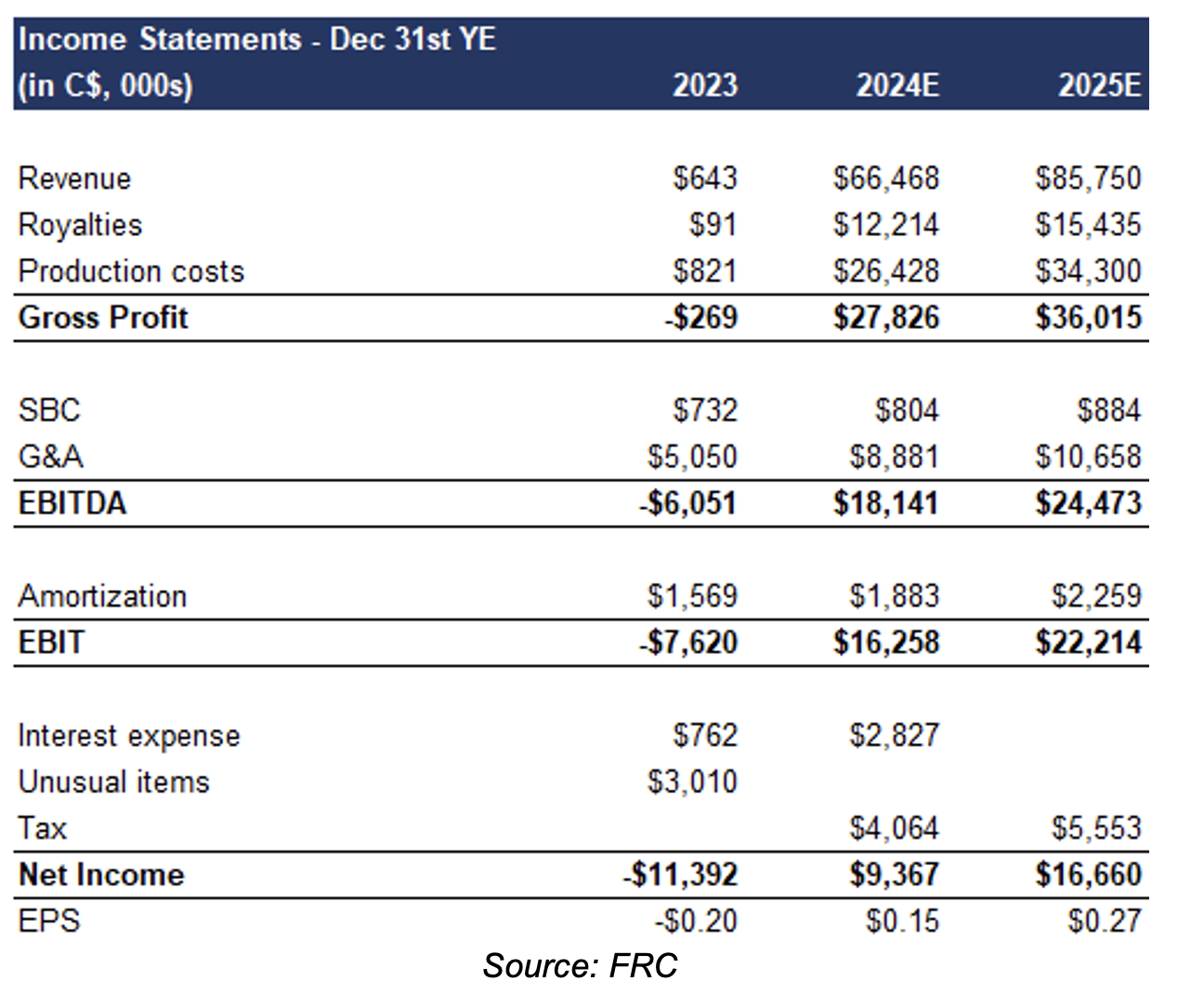

Financials (Year-End: Dec 31st)

Historic production and revenue came from its now-depleted gas fields in Turkey. Production surged in H1-2024 following the takeover of gas fields in Uzbekistan

Revenue increased from just $12k in Q2-2023, to $19M in Q2-2024. EBITDA and EPS turned positive

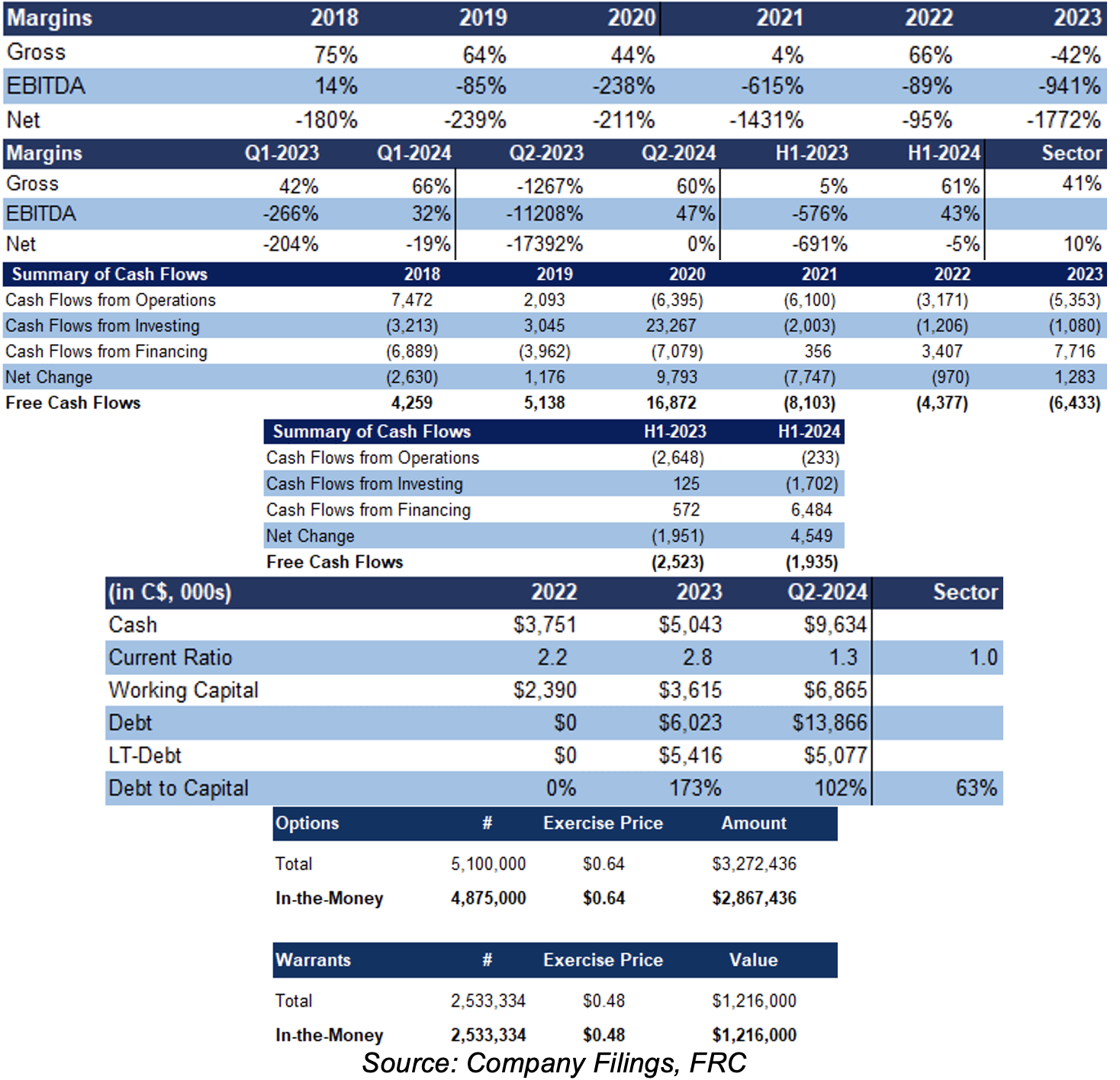

Margins, and free cash flows improved as well. Although debt/capital is currently higher than the sector average, we anticipate it will drop below the average by 2025, driven by robust free cash flows

Can raise up to $4.09M from in-the-money options and warrants

FRC Projections and Valuation

Using a sum-of-parts model, we are arriving at a fair value estimate of $3.62/share. Our valuation is highly sensitive to commodity prices

Our valuations on the Uzbek gas fields and the Kazakh LNG project are presented earlier in this report. We are valuing the early-stage lithium projects based on the sector average Enterprise Value-to-hectare ratio of pre-resource stage lithium juniors of $250/ha.

We anticipate record revenue and EPS in both 2024 and 2025

Based on our valuation models and review of the company's initiatives, we are initiating coverage with a BUY rating and a fair value estimate of $3.62/share. We believe the market has yet to grasp the true potential of CDR’s LNG initiative. Additionally, the company must demonstrate that its efforts at the recently acquired Uzbek gas field contract will lead to an increase in production. Once the market gains clarity on these points, we believe shares will move closer to our fair value estimate.

Risks

We believe the company is exposed to the following key risks (not exhaustive):

- None of its projects have resource or reserve estimates

- No guarantee that agreements with government entities in Uzbekistan and Kazakhstan will be extended

- Market liberalization in Uzbekistan may lead to volatility in gas prices

- FOREX and interest rate fluctuations

- Project financing and potential delays in development

- No guarantee that the company will be able to expand its projects simultaneously

APPENDIX